Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

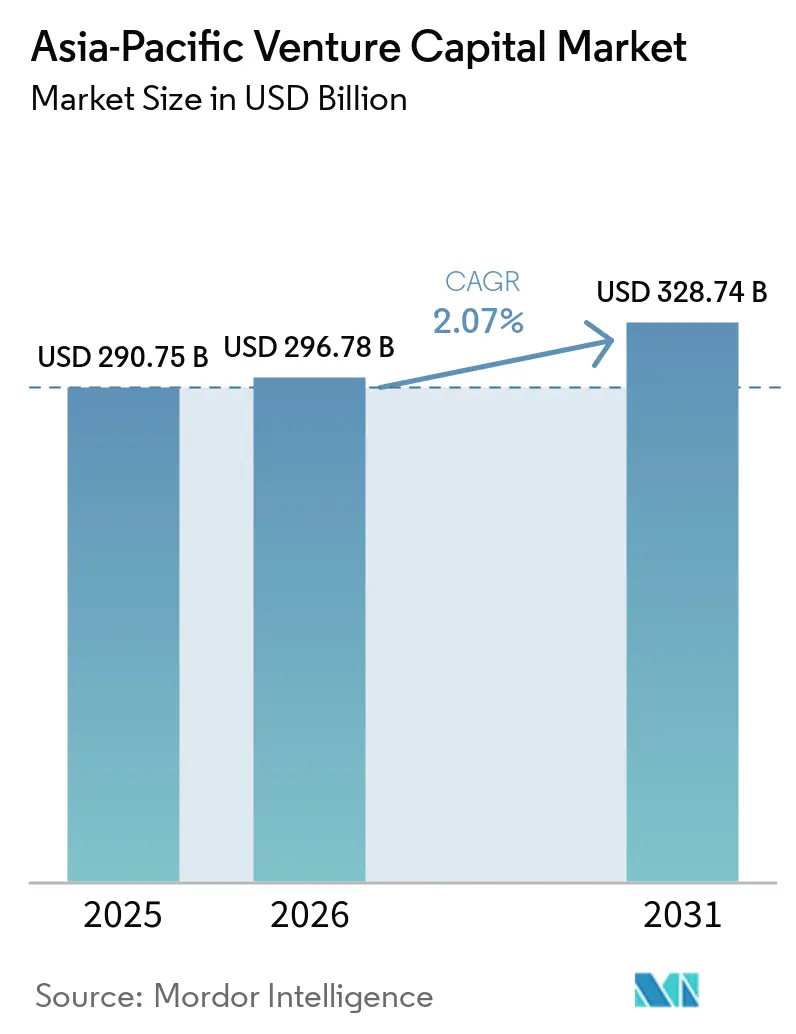

| Base Year Market Size (2025) | USD 290.75 Billion |

| Market Size (2026) | USD 296.78 Billion |

| Market Size (2031) | USD 328.74 Billion |

| Growth Rate (2026 - 2031) | 2.07% CAGR |

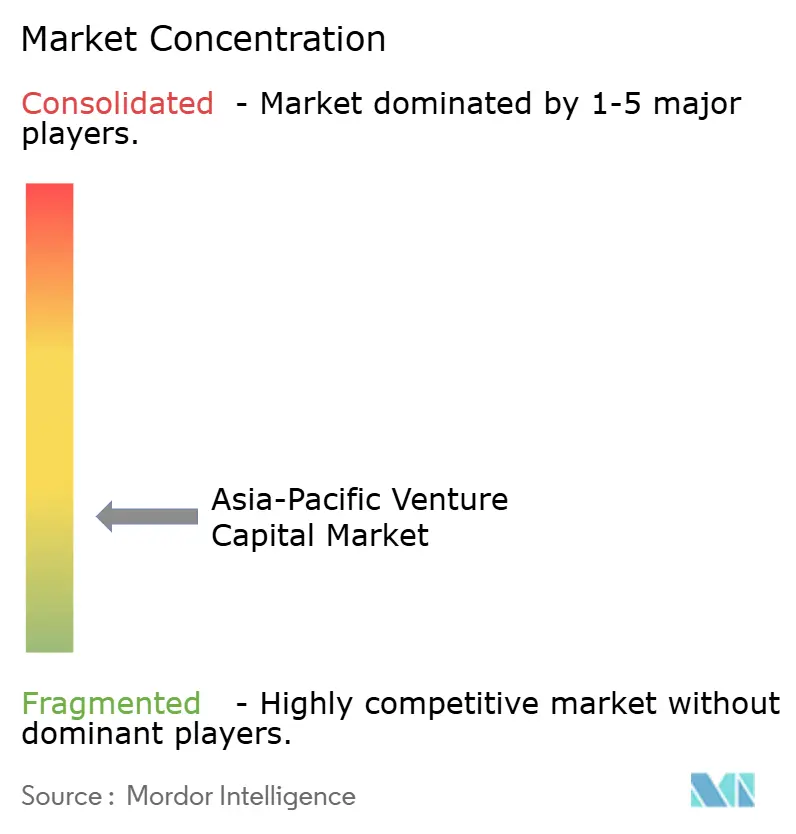

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Venture Capital Market Analysis by Mordor Intelligence

Asia-Pacific venture capital market size in 2026 is estimated at USD 296.78 billion, growing from 2025 value of USD 290.75 billion with 2031 projections showing USD 328.74 billion, growing at 2.07% CAGR over 2026-2031. Investors continue to channel capital toward technology sectors that align with government digital-economy priorities, yet heightened compliance requirements in China and stricter listing standards across regional stock exchanges temper late-stage deal flow. Fintech remains the dominant theme because mobile-first adoption drives surging demand for embedded payments and Banking-as-a-Service solutions, while cross-border syndication allows funds to mitigate single-country exposure risks. Structural tailwinds from sovereign startup programs encourage early-stage deployment, and the emergence of secondary markets broadens liquidity options for limited partners. At the same time, currency volatility challenges USD-denominated funds active in Indonesia, India, and Australia, prompting greater use of hedging instruments and local-currency vehicles. Overall, the Asia-Pacific venture capital market is transitioning from a period of exuberant growth toward disciplined capital allocation strategies that balance regulatory compliance, portfolio diversification, and long-term value creation.

Key Report Takeaways

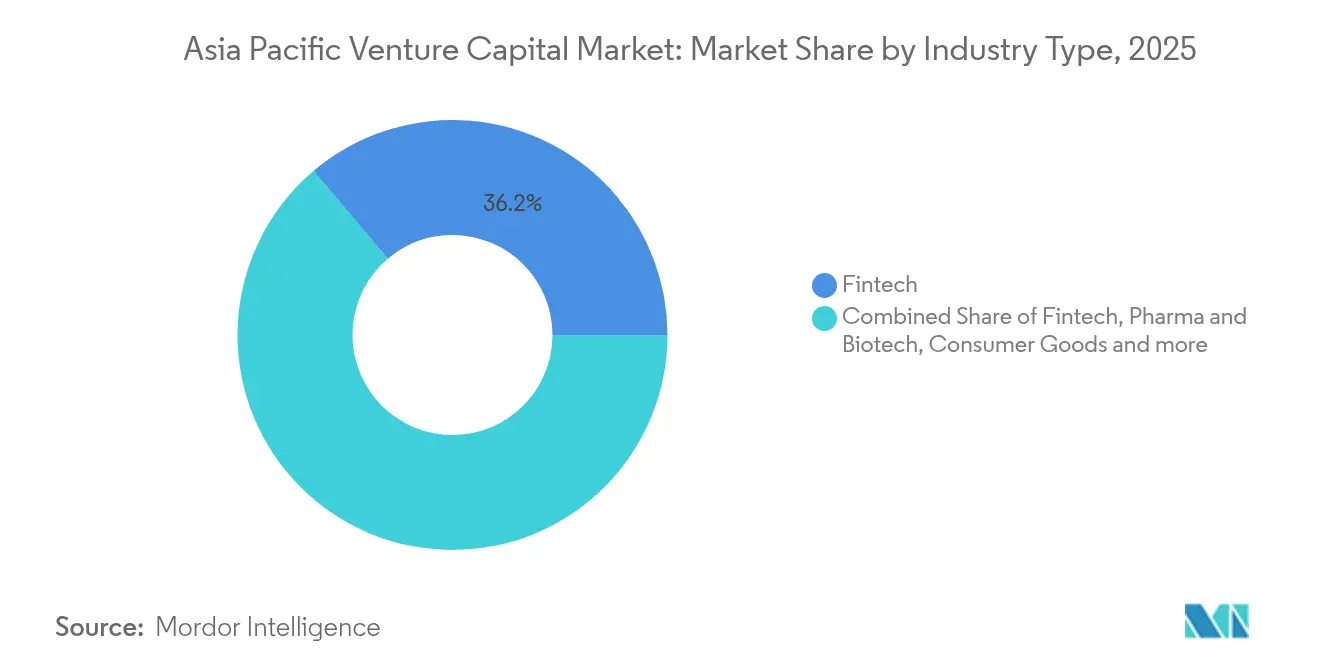

- By industry type, fintech accounted for 36.20% of the Asia-Pacific venture capital market share in 2025, while pharma and biotech posted the fastest segment expansion at a 16.09% CAGR through 2031.

- By the startup stage, later-stage investing companies attracted 30.00% of the Asia-Pacific venture capital market share in 2025, whereas angel/seed investing funding is expected to increase at a 18.59% CAGR between 2026 and 2031.

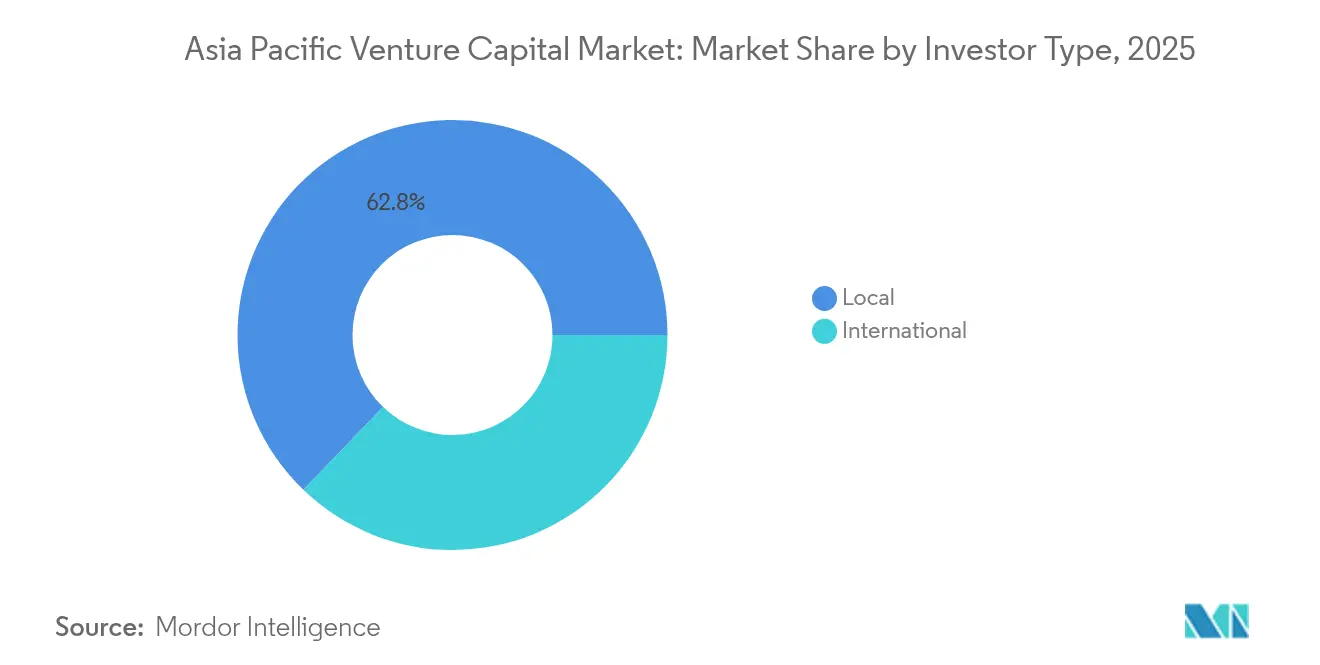

- By investor type, local funds held 62.80% of the Asia-Pacific venture capital market share in 2025, while international commitments are set to advance at a 24.06% CAGR through 2031.

- By geography, China commanded 28.90% of the Asia-Pacific venture capital market share in 2025, and India is projected to grow at a 14.05% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Venture Capital Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in digital adoption & fintech funding boom | +0.8% | APAC core and India, Southeast Asia | Medium term (2-4 years) |

| Government-backed startup stimulus funds | +0.6% | India, Singapore, Japan, South Korea | Long term (≥ 4 years) |

| Record VC returns versus public equities | +0.4% | Global, with concentration in India, Australia | Short term (≤ 2 years) |

| Emergence of secondary markets for LP liquidity | +0.3% | Singapore, Hong Kong, Australia | Medium term (2-4 years) |

| Rise of climate-tech & sustainability funds | +0.5% | APAC core, early gains in Singapore, Australia | Long term (≥ 4 years) |

| Cross-border syndication via ASEAN CIS & pacts | +0.2% | Southeast Asia and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Digital Adoption & Fintech Funding Boom

Mobile-centric behavior in Southeast Asia and India continues to elevate venture appetite as digital-payment penetration surpasses 85% in Singapore and Thailand, allowing fintech valuations to remain resilient despite global fundraising moderation [2]Source: Financial Times, “Southeast Asia Fintech Boom Continues,” ft.com. Corporate investors such as DBS Bank and OCBC spearhead strategic rounds to embed financial services in e-commerce and ride-hailing platforms, resulting in USD 12.3 billion of fintech investment during 2024. Regulatory sandboxes operating in Singapore, Hong Kong, and Malaysia accelerate experimentation by lowering compliance hurdles for early-stage firms. Central-bank digital-currency pilots further catalyze infrastructure spending that attracts venture attention. Neo-bank adoption in India and Indonesia strengthens the pipeline for credit-scoring and micro-lending solutions. Collectively, these dynamics explain why fintech captured 34% of regional deal count in 2024, reinforcing its structural prominence within the Asia-Pacific venture capital market.

Government-Backed Startup Stimulus Funds

Sovereign vehicles deployed USD 45 billion into startups across Asia-Pacific during 2024, with Singapore’s Temasek expanding venture exposure by 23% and India’s National Investment and Infrastructure Fund announcing a USD 2.3 billion deep-tech mandate. Japan’s Innovation Network Corporation steered USD 1.8 billion toward AI and quantum computing, while Korea Development Bank created a USD 900 million climate-tech facility. Tax incentives for angel investors and fast-track visa programs complement direct capital infusions, lowering risk premiums for private funds that co-invest alongside the state. Because objectives focus on semiconductors, biotechnology, and cybersecurity, stimulus funds trim early-stage financing gaps and shorten commercialization cycles. Over the long term, such public-private alignment lifts the Asia-Pacific venture capital market by expanding investable opportunities across strategic sectors.

Record VC Returns Versus Public Equities

Asia-Pacific venture funds produced a median 18.4% internal rate of return in 2024, beating regional public indexes by 540 basis points and catalyzing allocation shifts among pensions and insurers. Australian superannuation schemes increased alternative-asset exposure by 15%, and Japanese institutions followed suit to diversify yield sources. Secondary-market bid–ask spreads tightened as pricing improved 22%, letting limited partners harvest liquidity while maintaining upside via continuation funds. Although rising fund sizes risk capital overhang, superior historical performance reinforces the venture’s attractiveness relative to equities. The outcome is a steady supply of fresh commitments that fuels growth-stage deal capacity throughout the Asia-Pacific venture capital market.

Emergence of Secondary Markets for LP Liquidity

Transaction volume on regional secondary platforms surged 180% in 2024, reaching USD 3.2 billion through venues such as Forge Global and CartaX [3]Source: Wall Street Journal, “Venture Capital Secondary Markets Gain Traction,” wsj.com. Investors employ secondaries to rebalance portfolios without waiting for IPO windows, while buyers capture mature stakes at discounted values. Greater data transparency and harmonized valuation guidelines diminish information asymmetry, encouraging broader institutional participation. Continuation vehicles allow general partners to hold outperforming assets longer, injecting fresh capital for late-stage scaling. Enhanced liquidity infrastructure supports larger fund sizes and longer support cycles, which in turn stabilizes returns for the Asia-Pacific venture capital market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory crack-downs on tech sectors | -0.9% | China with Southeast Asia spillover | Short term (≤ 2 years) |

| Exit bottlenecks amid valuation corrections | -0.7% | Broad APAC, concentrated in China and India | Medium term (2-4 years) |

| Deep-tech talent scarcity | -0.4% | Global, acute in Japan and South Korea | Long term (≥ 4 years) |

| FX volatility for USD-denominated funds | -0.3% | Southeast Asia, India, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Crack-downs on Tech Sectors

China's technology sector regulations impose data localization requirements and antitrust enforcement that reduce late-stage venture capital deployment by 35% during 2024, as investors reassess regulatory risk in platform businesses and consumer internet companies. The Cybersecurity Law and Personal Information Protection Law create compliance costs that disproportionately impact early-stage startups lacking dedicated legal resources, while cross-border data transfer restrictions limit international expansion opportunities for venture-backed companies. Vietnam's new securities law introduces stricter foreign ownership limits and disclosure requirements that complicate venture capital structuring, particularly for cross-border funds seeking portfolio diversification across Southeast Asian markets. Regulatory uncertainty extends investment decision timelines as venture firms conduct enhanced due diligence on regulatory compliance and government relations capabilities of potential portfolio companies.

Exit Bottlenecks Amid Valuation Corrections

Initial public offering activity in Asia-Pacific declined 42% by value during 2024, with only 23 venture-backed companies completing listings compared to 67 in the previous year, creating liquidity constraints that extend fund holding periods and pressure internal rates of return. Strategic acquisition activity remains subdued as corporate buyers adopt conservative valuation methodologies, leading to pricing gaps between venture investors' expectations and acquirer willingness to pay, particularly for growth-stage companies with high revenue multiples. The Hong Kong Stock Exchange's revised listing requirements and Shanghai STAR Market's tightened profitability thresholds reduce exit pathway options for technology companies, forcing venture investors to provide additional growth capital to extend the runway until market conditions improve. Secondary buyout activity increases as growth equity firms acquire venture-backed companies at intermediate valuations, providing partial liquidity while maintaining upside exposure through continued ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industry Type: Pharma and Biotech Innovation Drives Alpha Generation

Fintech maintains dominance with a 36.20% market share in 2025, supported by digital payment infrastructure expansion and regulatory sandbox programs across Southeast Asia and India. However, pharma and biotech emerge as the fastest-growing segment at 16.09% CAGR through 2031, driven by aging demographics and government healthcare digitization initiatives. Consumer goods capture steady institutional interest through direct-to-consumer brand development, while industrial and energy sectors benefit from sustainability mandates and supply chain digitization trends. IT hardware and services experience consolidation pressure as cloud infrastructure matures, though edge computing and AI chip development create specialized investment opportunities.

The healthcare segment's acceleration reflects structural demand shifts following pandemic-driven adoption of telemedicine and digital therapeutics. EQT's Asian healthcare report identifies USD 12 billion in unmet funding needs across biotech R&D and medical device innovation, creating opportunities for specialized life sciences funds. Regulatory frameworks like Japan's PMDA fast-track approval processes and Singapore's Health Sciences Authority digital health guidelines provide clearer pathways for healthcare startup commercialization. Climate-tech investments within the industrial sector surge as corporate sustainability mandates create demand for venture-backed solutions in carbon capture, renewable energy storage, and circular economy technologies.

By Startup Stage: Angel/Seed Investing Stage Capital Formation Accelerates

Later-stage investing commands 30.00% market share in 2025, reflecting institutional preference for lower-risk, growth-stage opportunities with established revenue models. Angel and seed investing accelerates at 18.59% CAGR through 2031, supported by government co-investment programs and angel tax incentive expansions across Australia, Japan, and India. Early-stage investing maintains steady growth as corporate venture capital arms increase strategic investments in innovation pipeline development. The stage distribution reflects risk appetite evolution among institutional investors seeking diversified exposure across company maturity levels.

Government stimulus programs particularly impact early-stage capital formation through risk-sharing mechanisms that encourage private investor participation. Australia's Early Stage Venture Capital Limited Partnership program provides tax flow-through benefits that attract high-net-worth individuals to angel investing Australian Government. Japan's angel tax credit system offers 25% investment tax deductions, while Malaysia's angel investor tax incentive provides a 200% deduction for qualifying investments. These policy frameworks address traditional funding gaps in seed-stage capital by subsidizing private risk-taking through tax policy mechanisms.

By Investor Type: International VC Gains Strategic Advantage

Local investors control 62.80% of market activity in 2025, leveraging regional market knowledge and regulatory familiarity to identify investment opportunities ahead of international competitors. International participation grows at 24.06% CAGR through 2031, driven by cross-border syndication frameworks and currency hedging innovations that reduce FX risk for USD-denominated funds. Corporate venture capital emerges as a hybrid category, combining strategic insights with financial returns objectives across both local and international investment strategies.

Cross-border syndication benefits from ASEAN Capital Market Integration initiatives that standardize investment frameworks and reduce regulatory friction for multi-jurisdiction deals. Wellington Management's analysis shows that international co-investment structures reduce due diligence costs by 23% while improving portfolio company access to global markets. The ASEAN Comprehensive Investment Agreement provides legal frameworks that protect foreign investor rights, encouraging increased international participation in regional venture ecosystems. Currency hedging instruments developed by regional banks enable USD-denominated funds to reduce FX volatility exposure, addressing a traditional barrier to cross-border investment.

Geography Analysis

China accounted for 28.90% share within the Asia-Pacific venture capital market, but regulatory surveillance steers capital toward industrial automation, biotech, and climate solutions aligned with national priorities. Domestic funds leverage large check-writing capacity and established founder networks, yet IPO restrictions and tougher antitrust reviews extend exit horizons. Government guidance funds add patient capital, but compliance burdens push international GPs to seek co-investments where policy risk is lower. This reorientation maintains China’s scale while moderating headline momentum.

India’s trajectory is the region’s fastest, with a 14.05% CAGR expected through 2031 as UPI-led digital-payment ubiquity and government startup credits attract both local and global managers. Demographics skew young and consumption-oriented, yielding large addressable markets for fintech, health-tech, and ed-tech. Sovereign schemes, such as the Fund of Funds for Startups, deliver co-investment capital that de-risks early-stage deals, while corporate giants Reliance and Tata infuse strategic support, collectively ensuring India’s share of the Asia-Pacific venture capital market grows in both absolute and relative terms.

Southeast Asia offers portfolio diversification via Singapore’s regulatory clarity, Indonesia’s consumer-internet boom, Vietnam’s manufacturing digitization, and Thailand’s e-government expansion. Cross-border syndication under the ASEAN Capital Investment Scheme reduces single-country exposure, whereas bilateral tax treaties streamline fund structures. Japan and Australia maintain institutional participation thanks to pension and superannuation reforms, while South Korea channels chaebol-centric CVC through targeted deep-tech vehicles. Frontier markets such as Bangladesh and Sri Lanka emerge as optionality plays given the improving digital infrastructure. Together, these geographies ensure the Asia-Pacific venture capital market remains a multifaceted landscape with varying growth vectors and risk profiles.

Competitive Landscape

The Asia-Pacific venture capital market remains highly fragmented, reflected in a low market concentration. The leading firms hold a significant share of the market in 2024, leaving ample room for emerging fund managers and sector-focused investors to establish themselves. This fragmentation creates opportunities for differentiated strategies to thrive. Smaller players can compete by targeting underserved regions, industries, or funding stages. As a result, the competitive landscape continues to evolve with new entrants challenging established norms. This dynamic encourages differentiated investment strategies that can challenge incumbents. Peak XV Partners draws on its Sequoia Capital roots and deep local knowledge to maintain a notable market presence. Meanwhile, SoftBank Vision Fund benefits from its large fund size and growth-stage focus, though portfolio performance concerns and greater scrutiny from limited partners temper its investment pace.

Strategic specialization is reshaping competitive dynamics, as investors increasingly focus on sectors such as climate tech, healthcare, and deep tech. These thematic funds often build advantage through technical expertise and strong partnerships with corporates and research institutions. Such specialization enhances sourcing quality and post-investment value creation. In parallel, established firms are investing in technology to improve efficiency and competitiveness. Artificial intelligence is being adopted for deal sourcing and due diligence, while innovations like blockchain-based fund administration and tokenized investment vehicles are gaining traction.

A new wave of disruptors is entering the space, including corporate venture arms of tech companies, sovereign wealth funds increasing their venture allocations, and family offices opting for direct deals. These players often sidestep traditional fund structures, seeking greater control and alignment with strategic interests. The fragmented nature of the market allows new entrants to carve out a position through regional focus, domain expertise, or specific stage preferences. Established firms are increasingly required to offer more than just capital, providing operational support, market access, and strategic mentorship. In this evolving landscape, firms that combine investment acumen with specialized capabilities are best positioned to grow market share.

Asia-Pacific Venture Capital Industry Leaders

SoftBank Vision Fund

Granite Asia

Peak XV Partners (Sequoia India & SEA)

Temasek Holdings

Tiger Global Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DBS and Granite Asia announced a partnership and the closing of a USD 110 million AI IPO fund aimed at supporting Asia’s next generation of companies.

- January 2025: SoftBank Vision Fund completed a USD 2.1 billion Series C investment in Indian AI unicorn Ola Electric, marking the largest venture capital deployment in Asia-Pacific's mobility sector and signaling renewed confidence in India's electric vehicle ecosystem despite global funding constraints.

- December 2024: Temasek Holdings launched a USD 1.8 billion Southeast Asia Climate Tech Fund targeting carbon capture, renewable energy, and sustainable agriculture startups across Indonesia, Thailand, and Vietnam, representing the largest climate-focused venture capital initiative in the region.

- November 2024: Peak XV Partners announced the final close of its USD 2.85 billion Fund XI, exceeding initial target by 14% despite challenging fundraising environment, with commitments from sovereign wealth funds and institutional investors seeking Asia-Pacific venture exposure.

- October 2024: Samsung Ventures established a USD 500 million deep-tech fund focused on quantum computing, advanced semiconductors, and AI infrastructure startups across Japan, South Korea, and Taiwan, leveraging parent company's technology roadmap for strategic investment decisions.

Asia-Pacific Venture Capital Market Report Scope

Venture capital in Asia has played a significant economic role in the region's development and is expected to play an even more significant role in the future. Asia's start-up scene is presenting increased investment potential as the pandemic has shifted dynamics for the long term, one of the region's leading venture capital firms said. The Asia Pacific Venture Capital Market can be segmented by the various countries in the region ( China, India, Japan, South Korea, Indonesia, Malaysia and others), by the Industry or sector invested in ( fintech, logistics or LogiTech, healthcare, IT, education & EdTech, and others), and by stage ( early stage, growth & expansion stage, and late stage).

By Industry Type

| Fintech |

| Pharma and Biotech |

| Consumer Goods |

| Industrial/Energy |

| IT/Hardware and Services |

| Other Industries |

By Startup Stage

| Angel/Seed Investing |

| Early Stage Investing |

| Later Stage Investing |

By Investor Type

| Local |

| International |

By Geography

| India | |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | Singapore |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

| By Industry Type | Fintech | |

| Pharma and Biotech | ||

| Consumer Goods | ||

| Industrial/Energy | ||

| IT/Hardware and Services | ||

| Other Industries | ||

| By Startup Stage | Angel/Seed Investing | |

| Early Stage Investing | ||

| Later Stage Investing | ||

| By Investor Type | Local | |

| International | ||

| By Geography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific venture ecosystem in 2026?

The Asia-Pacific venture capital market size reached USD 296.78 billion in 2026 and is forecast to reach USD 328.74 billion by 2031 at a 2.07% CAGR.

Which sector attracts the most venture dollars today?

Banking and Financial Services leads with a 36.20% share of 2025 deal value, fueled by embedded payments and digital-banking platforms.

Where is investor momentum strongest geographically?

India shows the fastest pace, with forecast growth of 14.05% CAGR through 2031 thanks to supportive policy, large addressable markets, and digital infrastructure.

Why are exit timelines lengthening for Asia-Pacific startups?

IPO windows narrowed and valuation corrections widened pricing gaps, cutting 2024 listings by 42% and pushing funds toward secondary sales and continuation vehicles.

What role do corporate venture arms play in the region?

Corporate VC commitments are expanding at a 24.06% CAGR because strategic investors seek technology acquisition, market positioning, and regulatory advantages.

Page last updated on: