Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

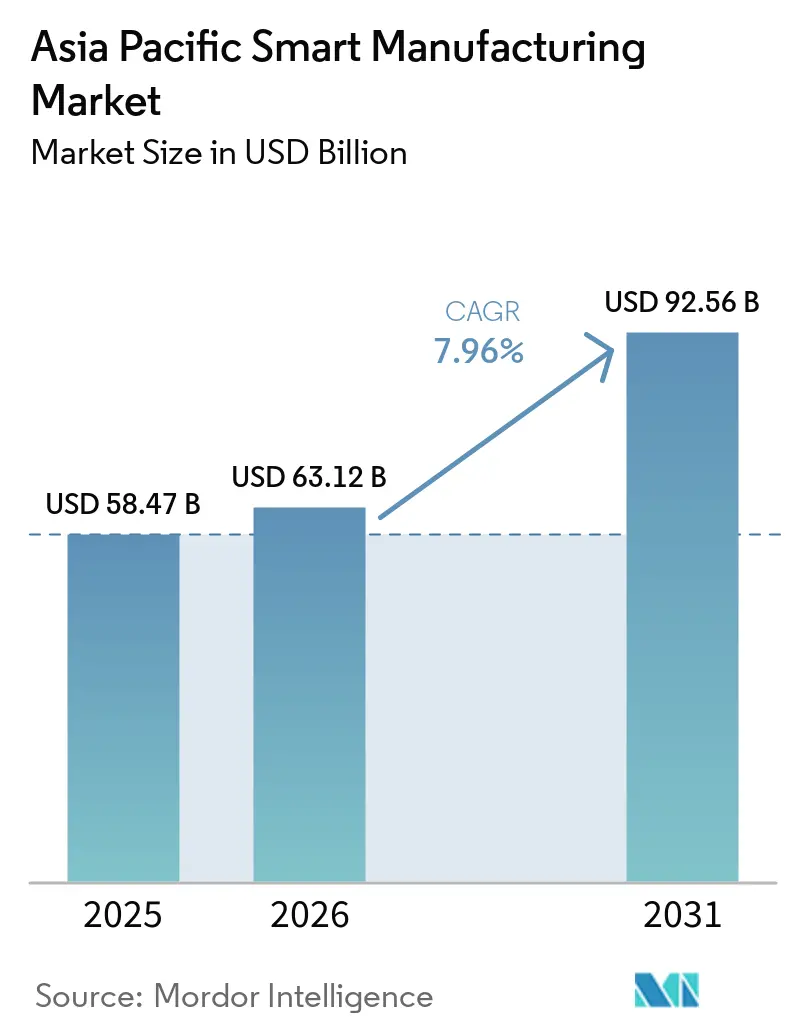

| Base Year Market Size (2025) | USD 58.47 Billion |

| Market Size (2026) | USD 63.12 Billion |

| Market Size (2031) | USD 92.56 Billion |

| Growth Rate (2026 - 2031) | 7.96% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Smart Manufacturing Market Analysis by Mordor Intelligence

The Asia-Pacific smart manufacturing market size was valued at USD 58.47 billion in 2025 and estimated to grow from USD 63.12 billion in 2026 to reach USD 92.56 billion by 2031, at a CAGR of 7.96% during the forecast period (2026-2031). Adoption is accelerating as government subsidies compress payback periods, labour shortages drive automation-first budgets, and semiconductor build-outs demand tightly controlled processes. Private-5G pilots deliver sub-10 millisecond latency for mobile robots and augmented-reality inspection, expanding use cases that were once connectivity constrained.[1]Huawei Technologies, “Huawei Unveils Upgraded Intelligent Factory Solution,” Huawei, huawei.com Hardware still captures the largest revenue slice, yet service-based contracts that bundle integration, cybersecurity, and analytics are growing faster as factories favour outcome guarantees over capex purchases. The Asia-Pacific smart manufacturing market is also shaped by supply-chain diversification; multinationals are spreading production across India, Vietnam, and Malaysia to limit single-country exposure, which in turn lifts regional demand for flexible, cloud-connected equipment. Rising cyber-risk on converged OT-IT networks further pushes spending toward zero-trust architectures and managed detection services.[2]Government of Japan, “AI in Manufacturing: New Japanese Software Takes on Skilled Work,” Japan Gov, japan.go.jp

Key Report Takeaways

- By geography, China led with 48.33% share in 2025, while India is projected to advance at a 11.62% CAGR through 2031.

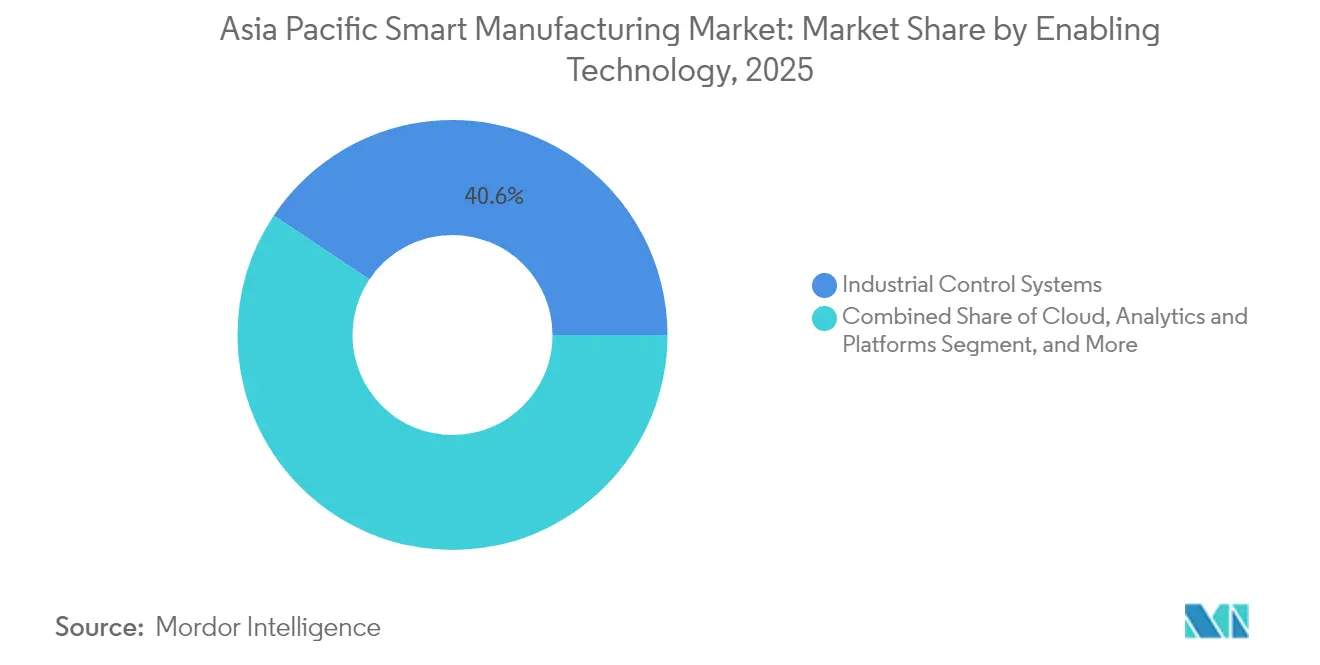

- By enabling technology, industrial control systems accounted for 40.62% of the Asia-Pacific smart manufacturing market share in 2025, while cloud, analytics and platforms are expected to grow at a 9.76% CAGR to 2031.

- By component, hardware captured 53.78% share of the Asia-Pacific smart manufacturing market size in 2025, whereas services are set to increase at an 10.91% CAGR through 2031.

- By deployment mode, on-premises solutions held 62.54% revenue share in 2025, and cloud deployments are forecast to post a 9.42% CAGR to 2031.

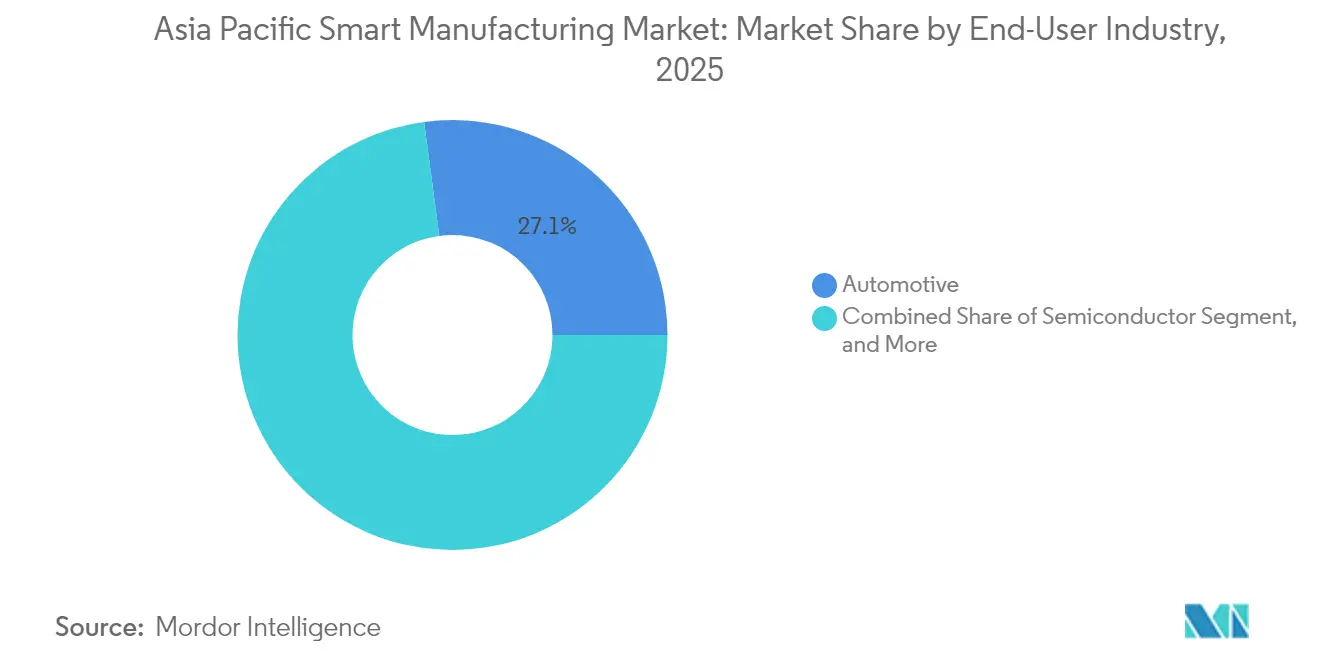

- By end-user industry, automotive contributed 27.11% share in 2025 and semiconductor and electronics are on track for a 10.08% CAGR through 2031.

- By enterprise size, large enterprises commanded 61.22% share in 2025, while SMEs are poised to progress at an 11.21% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Smart Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed digital transformation incentives | +1.80% | China, India, Singapore, Malaysia | Medium term (2-4 years) |

| Labor cost inflation and skill shortages | +1.50% | Global APAC, strongest in China, Japan, Singapore | Short term (≤ 2 years) |

| Post-COVID reshoring and supply-chain resilience | +1.20% | Global APAC, spill-over from North America and EU | Medium term (2-4 years) |

| Rapid 5G private-network rollouts in factories | +0.90% | China, South Korea, Japan, early gains in Singapore | Long term (≥ 4 years) |

| Semiconductor capacity race driving automation | +0.70% | Taiwan, South Korea, China, spill-over to Southeast Asia | Long term (≥ 4 years) |

| Carbon-neutrality mandates pushing energy-efficient operations | +0.60% | Japan, South Korea, China, expanding to ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed digital transformation incentives

Malaysia’s Industry4WRD fund, Singapore’s Digital Transformation Support Pilot Programme, Japan’s Asia Digital Transformation initiative, and India’s SAMARTH Udyog Bharat 4.0 collectively subsidize equipment, training, and cross-border R&D collaborations to accelerate Asia Pacific Digital Transformation initiatives. Matching grants in Malaysia have already disbursed RM 109.2 million to 299 SMEs, lowering automation entry barriers. Singapore offers HKD 50,000 per SME for pre-approved solutions that can be installed within nine months. METI sponsors joint projects that link Japanese system integrators with Southeast Asian manufacturers to co-develop use cases. India’s demonstration centers have trained 9,800 individuals and validated plug-and-play kits suitable for resource-constrained factories. Collectively, these policies de-risk investments, compress learning curves, and shorten time to scale, driving the Asia-Pacific smart manufacturing market toward sustained double-digit expansion.

Labor cost inflation and skill shortages

Average Chinese manufacturing wages more than doubled between 2015 and 2024, eroding the historical cost advantage and pushing firms toward lights-out production lines. Japan’s precision-machining workforce shrank by roughly 100,000 over two decades, spurring AI-enabled CAM software that slashes programming time from hours to minutes. Singapore’s tight labour pool forces its 2,700 precision-engineering firms to blend collaborative robots with human operators to keep uptime high. Cisco Networking Academy has already trained 20 million learners, helping bridge digital-skills gaps that slow automation projects. Rising personnel costs, coupled with demographic pressures, are therefore accelerating capex reallocation from headcount to smart equipment across the Asia-Pacific smart manufacturing market.

Post-COVID reshoring and supply-chain resilience

Eighty-three percent of manufacturing leaders plan to move some production nearer to demand centers, and one-third have executed reshoring pilots. Malaysia attracted new RFID lines from Xindeco IoT that serve regional IoT device makers, highlighting how supply-chain risk mitigation directly drives automation orders. PwC surveys show 76% of CEOs now diversify vendor bases, catalysing demand for modular, cloud-connected machines that can be replicated across multiple geographies without long commissioning cycles. Distributed production footprints also necessitate real-time visibility, elevating analytics and edge-platform spending within the Asia-Pacific smart manufacturing market. Vendors capable of delivering multi-plant dashboards and predictive maintenance across borders stand to capture share as decentralization reshapes sourcing calculus.

Rapid 5G private-network rollouts in factories

Sub-10 millisecond latencies achieved in Siemens’ Amberg plant and NTT Docomo pilot sites enable untethered AGVs, AR-based training, and high-density sensor grids. GSMA estimates private 5G can cut cabling costs by 30-40% while preserving deterministic performance. Manufacturers in South Korea have begun integrating edge servers with 5G radios to run AI vision that detects micro-defects in memory wafers in real time. Early adopters report double-digit OEE gains, validating the long-term upside of upgrading from Wi-Fi or wired Ethernet to spectrum-licensed networks. As spectrum policies across Asia liberalize, the Asia-Pacific smart manufacturing market will increasingly pivot toward 5G-native architectures that re-configure lines without physical network changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and ROI uncertainty | -1.40% | Global APAC, strongest impact on SMEs | Short term (≤ 2 years) |

| Fragmented vendor ecosystem and integration complexity | -0.80% | Global APAC, particularly complex in multi-vendor environments | Medium term (2-4 years) |

| Cybersecurity vulnerabilities in OT-IT convergence | -0.60% | Global APAC, critical in regulated industries | Long term (≥ 4 years) |

| Legacy equipment interoperability gaps | -0.50% | Global APAC, acute in established manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX and ROI uncertainty

Full-scale smart factory conversions often require USD 2–5 million per mid-sized site, deterring family-owned workshops and contract assemblers. Telstra surveys found 67% of respondents delay IoT projects due to cost concerns. Benefits accrue across energy, quality, and logistics, making single-metric ROI approvals challenging. Honeywell data show 45% of executives postpone predictive-maintenance rollouts because financial models cannot isolate the contribution of downtime reduction. Government grants offset only a fraction of total budgets, and many programs apply strict eligibility filters, leaving smaller firms to self-fund investments that may take three to five years to break even. Until financing models mature, this restraint will shave near-term growth off the Asia-Pacific smart manufacturing market.

Cybersecurity vulnerabilities in OT-IT convergence

Rockwell Automation reports 65% of factories suffered at least one breach in 2024, with ransomware attacks on production lines up 87 % year-over-year. Legacy PLCs lack encryption, forcing expensive retrofits or replacements. Cloud analytics and remote SCADA access expand the attack surface, pushing compliance requirements such as IEC 62443 into procurement checklists. The regional shortage of OT-focused security talent compounds risk; manufacturers often rely on third-party MSSPs that may not understand real-time control constraints. High-profile shutdowns in semiconductor fabs have prompted board-level mandates for zero-trust architectures, but the added cost and complexity slow decision cycles. Cyber-risk will therefore temper the Asia-Pacific smart manufacturing market until turnkey security platforms become mainstream.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enabling Technology: Control systems anchor digital evolution

Industrial control systems generated 40.62 % of the Asia-Pacific smart manufacturing market share in 2025, underscoring their role as the real-time backbone for thousands of discrete and process plants. PLCs and SCADA remain procurement mainstays because they guarantee deterministic operation under harsh shop-floor conditions. Manufacturers, however, increasingly overlay these controls with cloud dashboards that unify OEE, energy, and quality KPIs. The Asia-Pacific smart manufacturing market is consequently witnessing hybrid architectures where edge gateways stream encrypted data to AI engines that detect anomalies well before alarms fire.

Cloud, analytics and platforms are growing at a 9.76 % CAGR as firms migrate from isolated historians to predictive-maintenance models that cut unplanned downtime by up to 20 %. Machine-vision systems, once limited to single-camera checks, now integrate deep-learning libraries that flag sub-micron defects in semiconductors. Industrial robotics adoption is moving beyond automotive paint lines into low-volume high-mix sectors such as medical devices. Connectivity stacks ranging from Time-Sensitive Networking to Wi-Fi 6E sustain these intelligence layers. Vendors that package controls, analytics, and cybersecurity into subscription tiers are broadening addressable budgets within the Asia-Pacific smart manufacturing market.

By Component: Services capture accelerating wallet-share

Hardware accounted for 53.78 % of the Asia-Pacific smart manufacturing market size in 2025, reflecting demand for robots, sensors, and controllers that automate repetitive tasks. Nevertheless, services are scaling faster at 10.91 % CAGR as brownfield plants seek turnkey upgrades rather than do-it-yourself rollouts. System integrators now bundle consulting, commissioning, and managed-security operations in multiyear contracts that shift spending from capex to opex.

Software stakes continue rising because algorithmic differentiation such as adaptive path planning for collaborative robots delivers productivity boosts impossible with hardware tweaks alone. Edge-to-cloud service engagements let SMEs pilot features without owning entire stacks, accelerating democratization across the Asia-Pacific smart manufacturing market. The blurring line between software and services means vendors must maintain continuous improvement roadmaps, not just versioned releases, to keep renewal rates high.

By Deployment Mode: Cloud adoption gains but hybrid prevails

On-premises installations still held 62.54 % of revenue in 2025, driven by data-sovereignty mandates in pharmaceuticals and defense as well as latency demands for motion control. Plants that must meet GxP or ITAR rules prefer air-gapped networks. Even so, the Asia-Pacific smart manufacturing market is adding cloud nodes at a 9.42 % CAGR as predictive-maintenance algorithms and multi-facility dashboards require elastic compute.

Hybrid and edge-to-cloud architectures solve the latency-compliance dilemma. Edge servers execute millisecond-grade controls, while non-critical data sync to public clouds for AI model training. Semiconductor fabs in Taiwan already run virtual twins in cloud sandboxes to test process tweaks before deploying recipes to physical tools. As sovereign-cloud offerings proliferate, more sectors will offload analytics, trimming on-premises footprints across the Asia-Pacific smart manufacturing market.

By End-user Industry: Auto scale meets chip precision

Automotive plants commanded 27.11 % of 2025 revenue, benefiting from long-established robot density and the EV shift that requires reconfigurable body-in-white lines. Car makers leverage vision-guided torque tools and digital threads to manage mixed-model sequencing without downtime.

Semiconductor and electronics, growing at 10.08 % CAGR, are the fastest risers; fabs demand sub-micron accuracy, making AI-based run-to-run control indispensable. Pharmaceutical outfits invest in continuous manufacturing skids to strengthen traceability, while food processors adopt IoT sensors for hazard analysis. Aerospace primes use additive manufacturing cells tied to PLM systems that trace every powder batch. This diversity demonstrates how the Asia-Pacific smart manufacturing market flexes to sector-specific regulatory and throughput imperatives.

By Enterprise Size: SME momentum reshapes vendor playbooks

Large enterprises still generated 61.22 % of 2025 spending, reflecting deep pockets and multi-site rollouts. Yet SMEs are advancing at an 11.21 % CAGR thanks to starter kits that bundle sensors, cloud dashboards, and pay-per-use financing. Standardized templates allow a two-week proof of concept that demonstrates yield gains without disrupting production.

Medium-size firms often serve as supply-chain Tier 1s and thus face top-down digital mandates from OEMs. They choose modular MES subscriptions that scale as lines are added. The Asia-Pacific smart manufacturing market is therefore widening its customer base, compelling providers to price in local currencies, offer remote onboarding, and embed multilingual support.

Geography Analysis

China’s 48.33 % revenue share in 2025 is the product of state policy, dense supplier ecosystems, and aggressive 5G factory pilots that reduce integration costs. Provincial subsidies reimburse up to 50 % of qualifying automation purchases, encouraging SMEs to leapfrog incremental upgrades. Major OEMs such as Midea operate lighthouse plants where robotic arms outnumber workers, proving scalability for copy-exact replication. Yet trade tensions and rising wages are nudging some multinationals to diversify footprints, tempering China’s future share gains within the Asia-Pacific smart manufacturing market.

India, advancing at 11.62 % CAGR, benefits from the SAMARTH Udyog Bharat 4.0 test beds and an English-speaking software workforce that simplifies IT-OT integration. Automotive OEMs expanding EV output in Tamil Nadu and Maharashtra embed digital twins from day one, avoiding legacy retrofits. Pharmaceutical clusters in Hyderabad embrace continuous manufacturing to meet export quality norms, widening market scope. Critical enablers include power-quality upgrades and the rollout of dedicated industrial corridors that integrate logistics nodes with data centers.

Japan, South Korea, and Singapore represent mature but innovation-intensive pockets. Japan couples’ decades-old robot density with AI scheduling that offsets skilled-labour gaps. South Korea’s chip giants deploy edge-AI to boost lithography yield, while Singapore leverages Jurong Innovation District as a sandbox for 5G-enabled cobots and predictive maintenance solutions. Elsewhere, Vietnam and Thailand capture investment spills from China-plus-one strategies, focusing on electronics assembly lines that preinstall cloud connectors. Australia applies smart-manufacturing know-how to mining equipment rebuilds, underscoring the breadth of the Asia-Pacific smart manufacturing market.

Competitive Landscape

The Asia-Pacific smart manufacturing market exhibits moderate fragmentation: traditional automation majors dominate controls and drives, but cloud analytics, AI vision, and cybersecurity niches invite aggressive entrants. ABB, Siemens, and Schneider Electric leverage installed bases to upsell subscription analytics that turn hardware footprints into data platforms. Fanuc, Yaskawa, and Omron push low-payload cobots suited to SME budgets, expanding addressable revenue beyond automotive body shops.

Regional specialists such as Keyence and Advantech capitalize on proximity and rapid engineering cycles to tailor sensors and gateways for local compliance standards. Chinese players including Huawei and Inovance target the control-to-cloud stack, often bundling private-5G and edge servers at discounts. Strategic alliances are multiplying; Omron’s partnership with Cognizant melds 200,000 hardware SKUs with IT integration skills to deliver end-to-end digital migrations.

Cybersecurity capability is emerging as a key differentiator as boards demand proof-of-resilience. Vendors embed IEC 62443 compliance into proposals and tap MSSPs for 24/7 monitoring. Consolidation is likely among mid-tier MES providers seeking scale to compete on global support. Overall, leaders that can prove ROI via reference sites, offer consumption-based pricing, and maintain local service crews will outpace hardware-only rivals within the Asia-Pacific smart manufacturing market.

Asia Pacific Smart Manufacturing Industry Leaders

ABB Ltd

Honeywell International Inc.

Siemens AG

Schneider Electric SE

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Omron and Cognizant announced a strategic partnership to integrate IT and OT for factory digital transformation.

- January 2025: Huawei unveiled an upgraded Intelligent Factory Solution featuring integrated production networks and AI-driven platforms.

- December 2024: Schaeffler AG agreed to acquire Dhruva Automation to bolster Asia-Pacific engineering services.

- August 2024: Cisco and Rockwell Automation signed an MoU to accelerate digital transformation across Asia Pacific, Japan, and Greater China.

Asia Pacific Smart Manufacturing Market Report Scope

Smart manufacturing utilizes big data analytics, robotics, machine vision systems, sensors, and transmitters to refine complicated processes and manage supply chains. These solutions allow an enterprise to use smart manufacturing to shift from reactionary practices to predictive ones. This change targets improved efficiency of the process and performance of the product.

The Asia Pacific Smart Manufacturing Market is segmented By Enabling Technologies (Industrial Control Systems, Industrial Robotics, Machine Vision Systems, Cloud, Analytics and Platforms, Cybersecurity, Sensors & Transmitters, Connectivity/Communication, and Other Field, Control and Safety Solutions), By End-user Industry (Automotive, Semiconductor, Oil and Gas, Chemical and Petrochemical, Pharmaceutical, Aerospace and Defense, Food and Beverages) and By Country. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Enabling Technology

| Industrial Control Systems | Programmable Logic Controller (PLC) |

| Supervisory Control and Data Acquisition (SCADA) | |

| Distributed Control System (DCS) | |

| Human Machine Interface (HMI) | |

| Manufacturing Execution System (MES) | |

| Product Lifecycle Management (PLM) | |

| Industrial Robotics | |

| Machine Vision Systems | |

| Cloud, Analytics and Platforms | |

| Cybersecurity | |

| Sensors and Transmitters | |

| Connectivity and Communication | |

| Other Field, Control and Safety Solutions |

By Component

| Hardware |

| Software |

| Services |

By Deployment Mode

| On-premise |

| Cloud |

| Hybrid |

| Edge-to-Cloud |

By End-user Industry

| Automotive |

| Semiconductor and Electronics |

| Oil and Gas |

| Chemical and Petrochemical |

| Pharmaceutical and Biotechnology |

| Aerospace and Defense |

| Food and Beverages |

| Metals and Mining |

| Logistics and Warehousing |

| Other End-User Industries |

By Enterprise Size

| Small Enterprises |

| Medium Enterprises |

| Large Enterprises |

By Country

| China |

| India |

| Japan |

| South Korea |

| Taiwan |

| Singapore |

| Thailand |

| Vietnam |

| Australia |

| Rest of Asia-Pacific |

| By Enabling Technology | Industrial Control Systems | Programmable Logic Controller (PLC) |

| Supervisory Control and Data Acquisition (SCADA) | ||

| Distributed Control System (DCS) | ||

| Human Machine Interface (HMI) | ||

| Manufacturing Execution System (MES) | ||

| Product Lifecycle Management (PLM) | ||

| Industrial Robotics | ||

| Machine Vision Systems | ||

| Cloud, Analytics and Platforms | ||

| Cybersecurity | ||

| Sensors and Transmitters | ||

| Connectivity and Communication | ||

| Other Field, Control and Safety Solutions | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| Hybrid | ||

| Edge-to-Cloud | ||

| By End-user Industry | Automotive | |

| Semiconductor and Electronics | ||

| Oil and Gas | ||

| Chemical and Petrochemical | ||

| Pharmaceutical and Biotechnology | ||

| Aerospace and Defense | ||

| Food and Beverages | ||

| Metals and Mining | ||

| Logistics and Warehousing | ||

| Other End-User Industries | ||

| By Enterprise Size | Small Enterprises | |

| Medium Enterprises | ||

| Large Enterprises | ||

| By Country | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Singapore | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What are the current and projected values of the Asia-Pacific smart manufacturing market?

The market stands at USD 63.12 billion in 2026 and is projected to reach USD 92.56 billion by 2031, growing at an 7.96% CAGR.

Which country contributes the highest revenue?

China accounts for 48.33% of 2025 revenue due to its large industrial base and policy incentives.

Which technology segment is expanding the fastest?

Cloud, analytics and platforms are forecast to grow at a 9.76% CAGR through 2031 as manufacturers shift to data-driven operations.

What is the main barrier slowing adoption among SMEs?

High upfront capital expenditure and uncertain ROI remain the foremost obstacles, especially for smaller firms.

How quickly are private-5G factory networks being adopted?

Rollouts are accelerating, with latency improvements enabling AGVs and AR inspection, and the driver is estimated to add +0.9% to overall CAGR.

Which end-user vertical shows the fastest growth?

Semiconductor and electronics manufacturing is projected to expand at a 10.08% CAGR through 2031 thanks to capacity expansions across the region.

Page last updated on: