Asia-Pacific Waterproofing Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

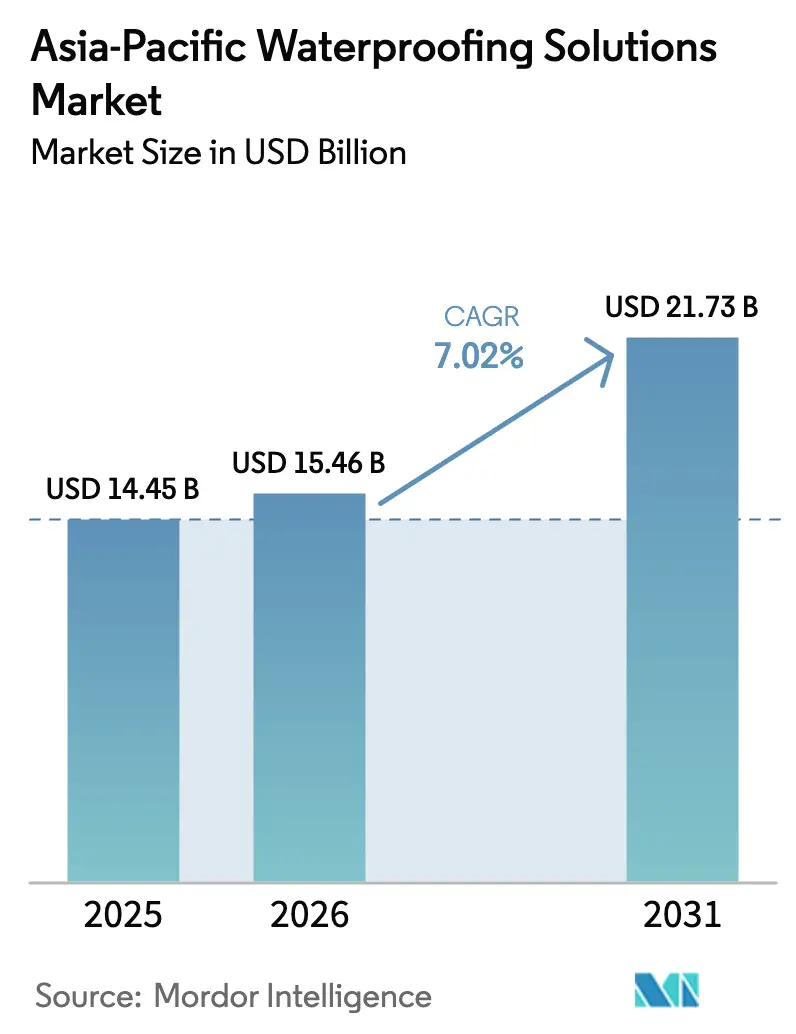

| Base Year Market Size (2025) | USD 14.45 Billion |

| Market Size (2026) | USD 15.46 Billion |

| Market Size (2031) | USD 21.73 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

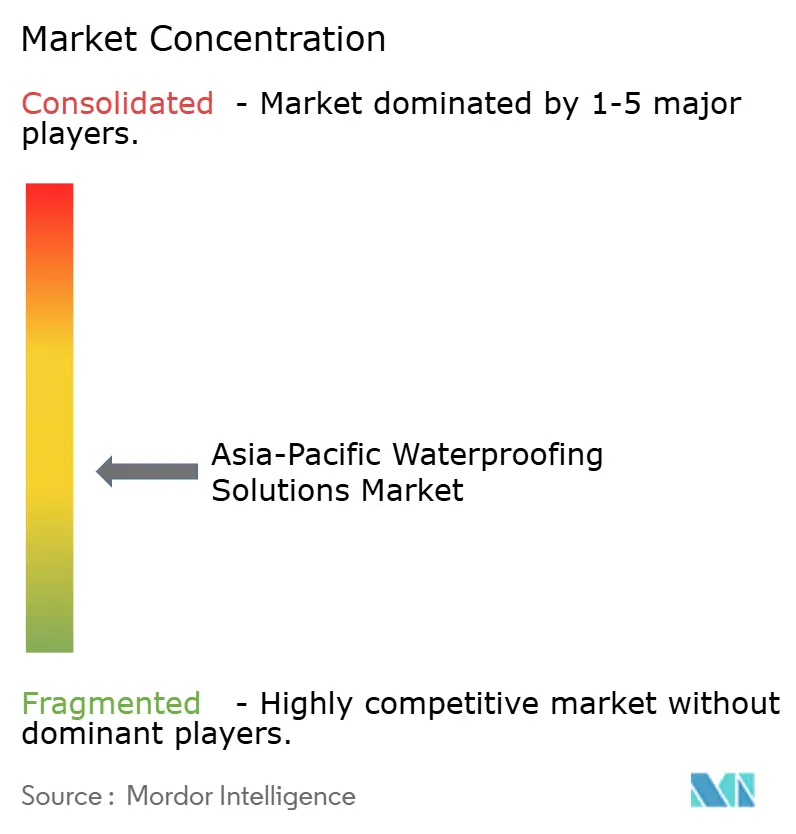

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Waterproofing Solutions Market Analysis by Mordor Intelligence

The Asia-Pacific Waterproofing Solutions Market size was valued at USD 14.45 billion in 2025 and estimated to grow from USD 15.46 billion in 2026 to reach USD 21.73 billion by 2031, at a CAGR of 7.02% during the forecast period (2026-2031). Underpinning this expansion are the region’s large-scale infrastructure modernization programs, rapidly growing urban populations, and climate-adaptation policies that elevate performance requirements for moisture protection systems. The shift from price-based procurement toward lifecycle-cost optimization widens the addressable opportunity for premium membranes and chemically enhanced coatings, while supportive building-energy regulations accelerate adoption in both new construction and retrofits. Intensifying project complexity encourages the specification of integrated monitoring features, thereby favoring suppliers who can pair materials science with digital technologies. Finally, raw material cost volatility and labor shortages temper near-term growth, yet simultaneously motivate end users to prefer products that offer installation efficiency and longer service life.

Key Report Takeaways

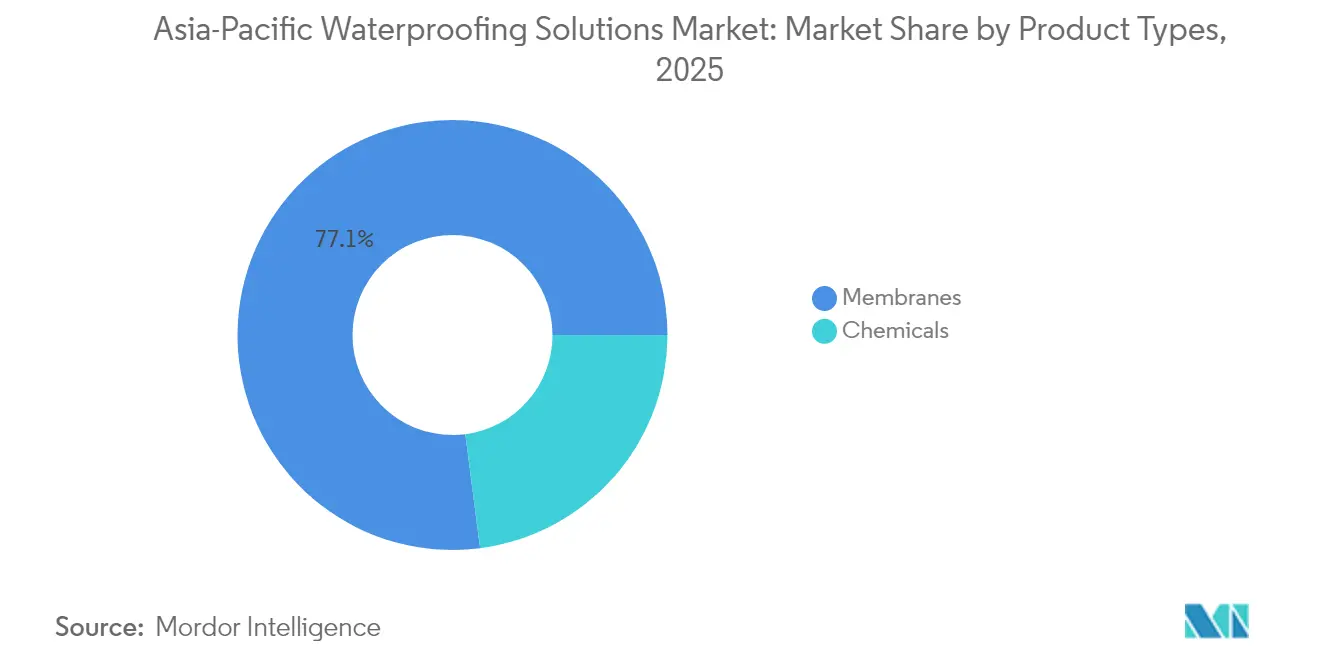

- By product type, membranes led with 77.05% revenue share in 2025 and are forecasted to expand at an 7.64% CAGR through 2031.

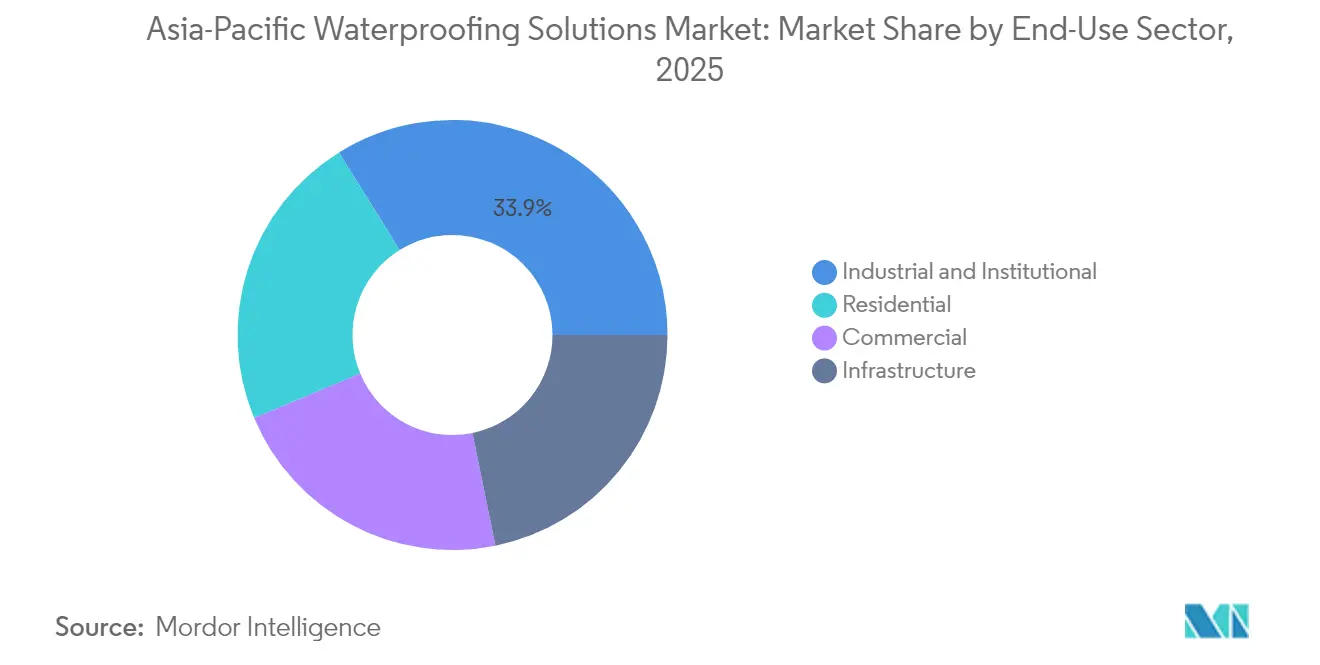

- By end-use sector, industrial and institutional applications accounted for 33.85% of the Asia-Pacific waterproofing solutions market share in 2025, while residential is advancing at an 8.05% CAGR through 2031.

- By geography, China captured a 62.10% share of the Asia-Pacific waterproofing solutions market size in 2025 and is set to grow at a 7.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Waterproofing Solutions Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and infrastructure build-out | +1.5% | China, India, core ASEAN markets | Medium term (2-4 years) |

| Green-roof and energy-efficient building codes | +1.2% | Singapore, Hong Kong, Japan, South Korea | Long term (≥ 4 years) |

| Government waterproofing mandates in public works | +0.8% | Australia, China, Thailand | Short term (≤ 2 years) |

| Rapid expansions of logistics hubs | +0.6% | ASEAN, India, Australia | Medium term (2-4 years) |

| Offshore wind substation construction | +0.3% | China, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Infrastructure Build-out

Urban populations in China, India, and fast-growing ASEAN economies continue to increase, prompting governments to prioritize the development of new rail corridors, expressways, and municipal utility tunnels. These large assets demand waterproofing systems that can accommodate thermal cycling, differential settlement, and seismic movement over multi-decade service lives. Performance specifications increasingly bundle membrane durability with embedded leak-detection sensors to reduce maintenance downtime. Market participants that combine material supply with turnkey application support secure preferred-vendor status on megaproject frameworks. Strict warranty obligations, often extending beyond 20 years, are normalizing the uptake of premium solutions, thereby reinforcing price-insensitive demand for high-grade bituminous, PVC, and TPO membranes.

Green-Roof and Energy-Efficient Building Codes

Stricter building-energy regulations across the region draw direct links between envelope moisture performance and operational emissions. Singapore’s latest Green Mark criteria, Japan’s planned 2025 wooden-building longevity rules, and South Korea’s zero-energy building roadmap all stipulate root-resistant, vapor-permeable membranes that integrate condensation management. Research shows that well-designed green roofs can lower surface temperatures by up to 30 °C, provided that waterproof layers demonstrate strong puncture resistance and a balance of vapor diffusion. Harmonizing taxonomies across jurisdictions reduces specification uncertainty and enables multinational developers to standardize procurement, benefiting suppliers with region-wide certifications.

Government Waterproofing Mandates in Public Works

Public agencies increasingly move beyond minimum code compliance toward lifecycle-cost contracting. Australia’s WestConnex M4-M5 Link tunnels exemplify this shift, where crystalline admixtures were chosen to withstand high hydrostatic pressure throughout a 100-year design life. Similar policies apply to dam refurbishments, mass transit expansions, and potable water reservoirs, creating an addressable backlog for additive-enhanced concretes, spray-applied membranes, and dual-layer sheet systems. Vendors that document accelerated-aging data and maintain extended warranty programs gain priority within prequalification registers.

Rapid Expansions of Logistics Hubs

Regional supply-chain diversification drives an unprecedented wave of automated distribution centers. Floor-to-wall transitions, densely loaded racking foundations, and cold-storage zones require specialized membranes with high abrasion resistance and flexibility at low temperatures. Multinational operators demand consistent product performance across all ASEAN members, encouraging suppliers to harmonize formulations for both tropical and subtropical climates. Smart facility managers embed leak sensors that interface with warehouse-management platforms, turning waterproofing performance into an operational key performance indicator rather than a construction afterthought.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.9% | Global, particularly China and India | Short term (≤ 2 years) |

| Shortage of skilled applicators | -0.7% | ASEAN, India, Australia | Medium term (2-4 years) |

| Solvent-borne chemistry under regulatory scrutiny | -0.5% | Singapore, Hong Kong, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Polyurethane and epoxy feedstocks sourced from petrochemicals exhibit double-digit annual price swings, compressing converter margins and complicating project budgeting. Anti-dumping measures on key intermediates further raise landed costs in India and Southeast Asia. Currency depreciation in several emerging markets widens variability between contracted and actual material costs, forcing suppliers to adopt shorter quotation validity periods. Membrane producers emphasize polymer blends with higher recycled content shares to moderate input exposure, while forward-buying strategies and toll manufacturing partnerships help spread volatility risk.

Shortage of Skilled Applicators

Modern waterproofing systems, especially fully adhered membranes with active leak-detection layers, demand certified installers who understand substrate preparation, environmental curing windows, and electronic integrity testing. Training capacity lags behind construction growth, resulting in project delays and increased rework costs. Australia’s state-level licensing schemes mandate continuous professional development, yet many small contractors struggle to allocate time for formal accreditation. Manufacturers expand academy programs and on-site coaching to uphold warranty validity and mitigate reputational risk stemming from installation errors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Types: Membranes Capture Performance-Led Demand

Membrane solutions dominated the Asia-Pacific waterproofing solutions market, accounting for a 77.05% share in 2025, and are forecasted to post an 7.64% CAGR from 2026 to 2031. Within this group, fully adhered thermoplastic sheets win preference on large commercial roofs and below-grade infrastructure because they create continuous barriers that tolerate structural movement. Cold-liquid-applied membranes are gaining traction in retrofits where complex geometries or congested mechanical penetrations hinder the installation of sheet rolls.

Nanofibrous composites and polymer-bitumen hybrids are emerging as technology front-runners, exhibiting higher elongation, self-healing properties, and lower installation temperatures. Suppliers highlight reduced volatile organic compound content to meet tightening indoor air quality rules and site safety constraints. Conversely, chemically cured coatings retain roles in secondary containment, potable-water tanks, and chemically aggressive industrial zones where point-load abrasion and solvent exposure exceed membrane tolerances. Overall, membrane leadership illustrates how buyers prioritize lifecycle reliability over initial savings, especially when performance warranties align with building-owner asset-management objectives.

By End-Use Sector: Industrial Dominance Meets Residential Momentum

Industrial and institutional facilities contributed 33.85% to 2025 revenue, underscoring the criticality of waterproofing for uninterrupted operations in semiconductor fabs, power plants, and healthcare complexes. Failures in these environments generate costly downtime and can compromise safety regimes. Accordingly, specifiers demand products that combine chemical resistance, high tensile strength, and predictive-maintenance sensors. Chemical admixtures that crystallize within concrete matrices offer redundant protection for critical containment structures such as desalination basins and wastewater reactors.

Residential construction, however, is expected to record the fastest growth at an 8.05% CAGR through 2031. Rising multi-story housing in India, Indonesia, and the Philippines is facing stricter wet-area standards, including the use of vapor-permeable membranes behind tiled shower walls. The Asia-Pacific waterproofing solutions market share for residential applications is expected to increase as homebuyers increasingly value mold prevention and assurances of indoor air quality. Builders respond by shifting from cementitious coatings toward high-flexibility liquid membranes that reduce cracking at dynamic joints.

Geography Analysis

China leads the region with a 62.10% revenue share in 2025 and is projected to grow at a rate of 7.32% annually through 2031, supported by sustained public investment in rail, renewable energy bases, and smart city districts. State-owned design institutes increasingly mandate dual-layer membranes on subterranean transit corridors to mitigate hydrostatic pressure during extreme rainfall events. Beijing-based Oriental Yuhong’s 2025 acquisition of a Hong Kong contractor exemplifies local champions exporting expertise to nearby high-specification markets.

ASEAN members collectively contribute a rising portion of demand as governments channel capital toward airports, logistics corridors, and social housing. Vietnam’s northern industrial zones contract regional suppliers for fast-curing spray membranes that shorten construction cycles, while Thailand’s green-building incentives catalyze demand for water-based coatings with low environmental impact.

Australia, Japan, and South Korea form a mature yet technically advanced cluster. Australia’s National Construction Code 2024 amendments require the use of vapor-permeable membranes in all climate zones, solidifying a stable demand baseline. Japan’s forthcoming wooden-structure longevity standards emphasize moisture management at exterior-wall interfaces, stimulating investment in breathable yet watertight sheet systems. South Korea, meanwhile, couples green-building certification schemes with ambitious offshore wind targets, boosting both commercial building and marine-grade product adoption. Collectively, these markets value documented long-term durability more than initial acquisition cost, encouraging suppliers to deliver premium warranties and cradle-to-grave technical support.

Competitive Landscape

The Asia-Pacific waterproofing solutions market is fragmented. Global multinationals strengthen their regional presence through acquisitions and greenfield investments to localize supply chains, reduce logistics expenses, and comply with distinct national standards. Saint-Gobain completed the USD 1.025 billion acquisition of Fosroc, extending its admixture and liquid-applied membrane portfolio while deepening distribution in India and Southeast Asia[2]Saint-Gobain, “Completion of Fosroc Acquisition,” saint-gobain.com. Regional champions develop competitive moats around specialized application know-how. Product differentiation now pivots on sustainability credentials, with several suppliers launching bio-based polyols and recycled-content SBS modifiers. Digitalization also shapes rivalry; companies that bundle cloud-connected leak-detection grids with warranty packages enjoy upselling advantages in high-value commercial and industrial projects. Looking ahead, rising performance standards and owner-led maintenance contracts are likely to spur further consolidation as small formulators struggle to meet certification costs. Nevertheless, niche players focused on marine-grade coatings or high-altitude cold-climate membranes continue to find attractive pockets of demand, particularly where project volumes remain below thresholds that interest global conglomerates.

Asia-Pacific Waterproofing Solutions Industry Leaders

Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

Sika AG

Saint-Gobain

Ardex Group

Hongyuan Waterproof Technology Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Beijing Oriental Yuhong Waterproof Technology Co., Ltd. has finalized the purchase of a Hong Kong-based waterproofing company, Man Cheong Metals and Building Materials and Specialist Products, creating a platform for expansion in Southeast Asian.

- February 2025: Saint-Gobain finalized the acquisition of Fosroc, strengthening its ASEAN construction-chemicals footprint, particularly in waterproofing.

Asia-Pacific Waterproofing Solutions Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Chemicals, Membranes are covered as segments by Sub Product. Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Vietnam are covered as segments by Country.| Chemicals | Epoxy-based |

| Polyurethane-based | |

| Water-based | |

| Other types | |

| Membranes | Cold Liquid Applied |

| Fully Adhered Sheet | |

| Hot Liquid Applied | |

| Loose Laid Sheet |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Product Types | Chemicals | Epoxy-based |

| Polyurethane-based | ||

| Water-based | ||

| Other types | ||

| Membranes | Cold Liquid Applied | |

| Fully Adhered Sheet | ||

| Hot Liquid Applied | ||

| Loose Laid Sheet | ||

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Country | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Market Definition

- END-USE SECTOR - Waterproofing solutions consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of waterproofing solutions such as membranes, coatings, and chemicals are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms