Asia-Pacific Polyether Ether Ketone (PEEK) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

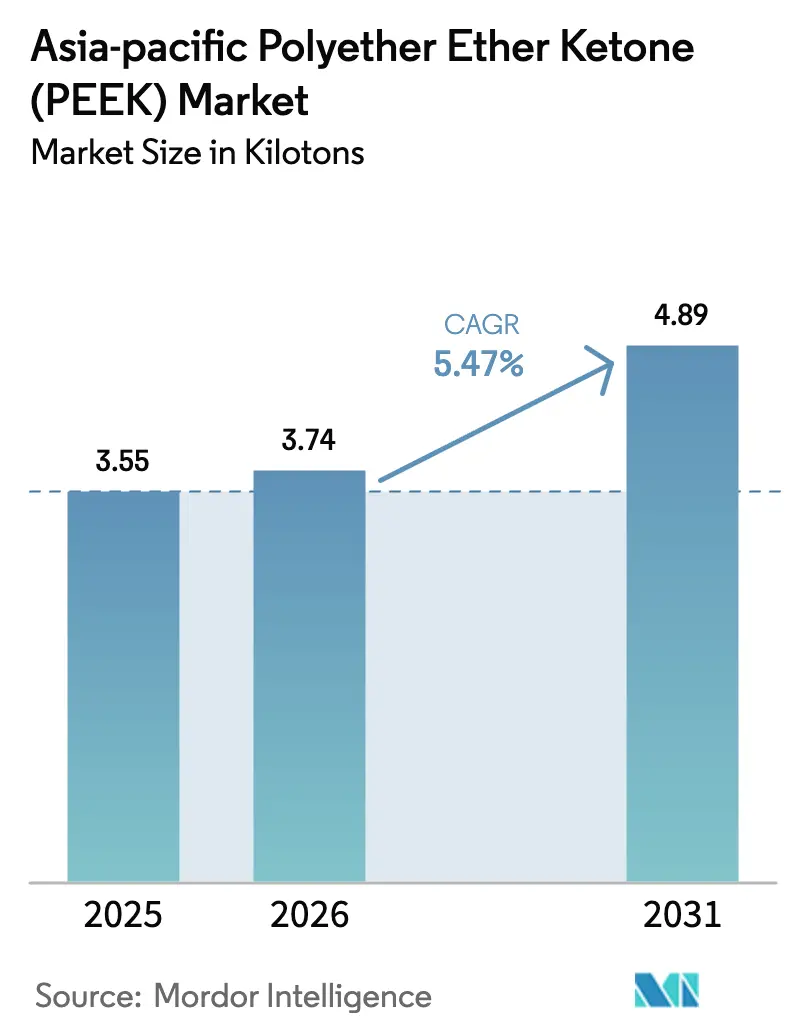

| Base Year Market Size (2025) | 3.55 kilotons |

| Market Volume (2026) | 3.74 kilotons |

| Market Volume (2031) | 4.89 kilotons |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Polyether Ether Ketone (PEEK) Market Analysis by Mordor Intelligence

The Asia-pacific Polyether Ether Ketone Market size was valued at 3.55 kilotons in 2025 and estimated to grow from 3.74 kilotons in 2026 to reach 4.89 kilotons by 2031, at a CAGR of 5.47% during the forecast period (2026-2031). Robust demand from aerospace, electronics, medical devices, and automotive lightweighting anchors this solid trajectory, while China’s policy-backed capacity build-out compresses regional input costs and broadens application viability. Commercial aerospace revenue in the region rebounded 54% above 2019 levels in 2024, accelerating the adoption of high-temperature thermoplastics in flight-critical components. Semiconductor fabrication investments across China, South Korea, and Japan amplify short-cycle pull for ultra-pure grades, whereas India’s industrial modernization enlarges the future addressable base for performance polymers. Sustained localization of DFBP feedstocks lowers conversion costs, and vertically integrated producers leverage this advantage to contend with established global incumbents.

Key Report Takeaways

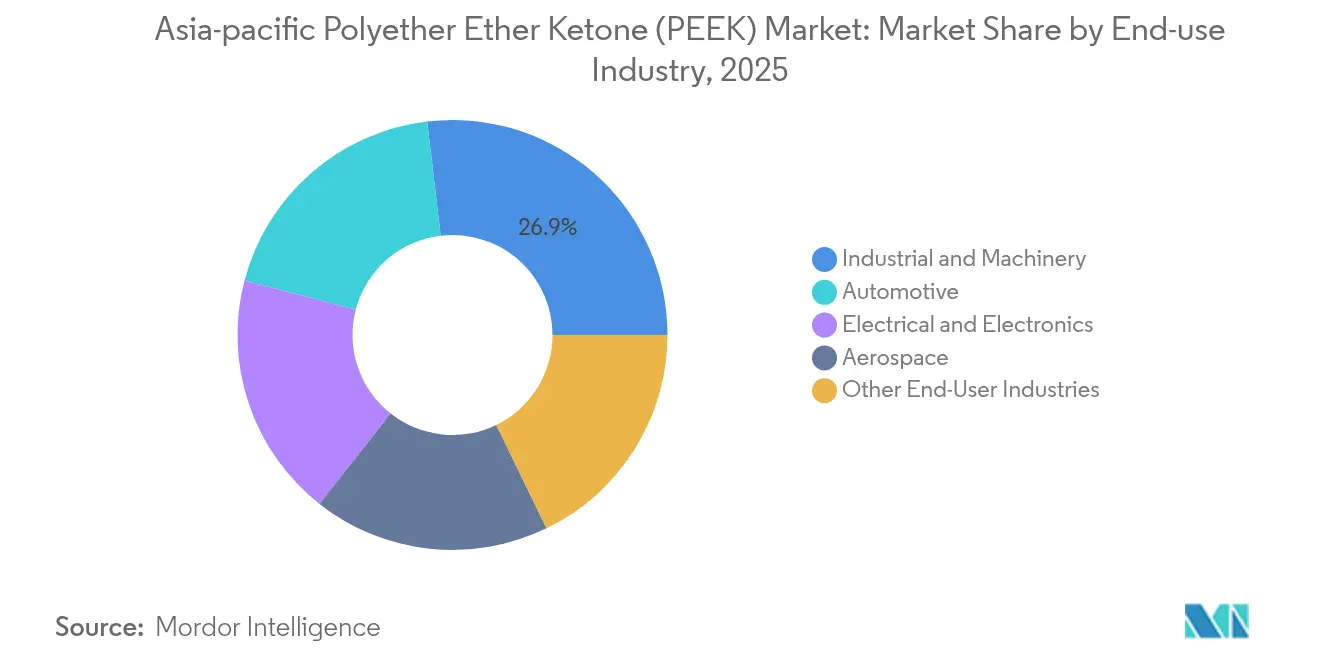

- By end-user industry, industrial machinery accounted for 26.88% of the Asia-Pacific PEEK market size in 2025; automotive leads volume expansion at a 5.99% CAGR to 2031.

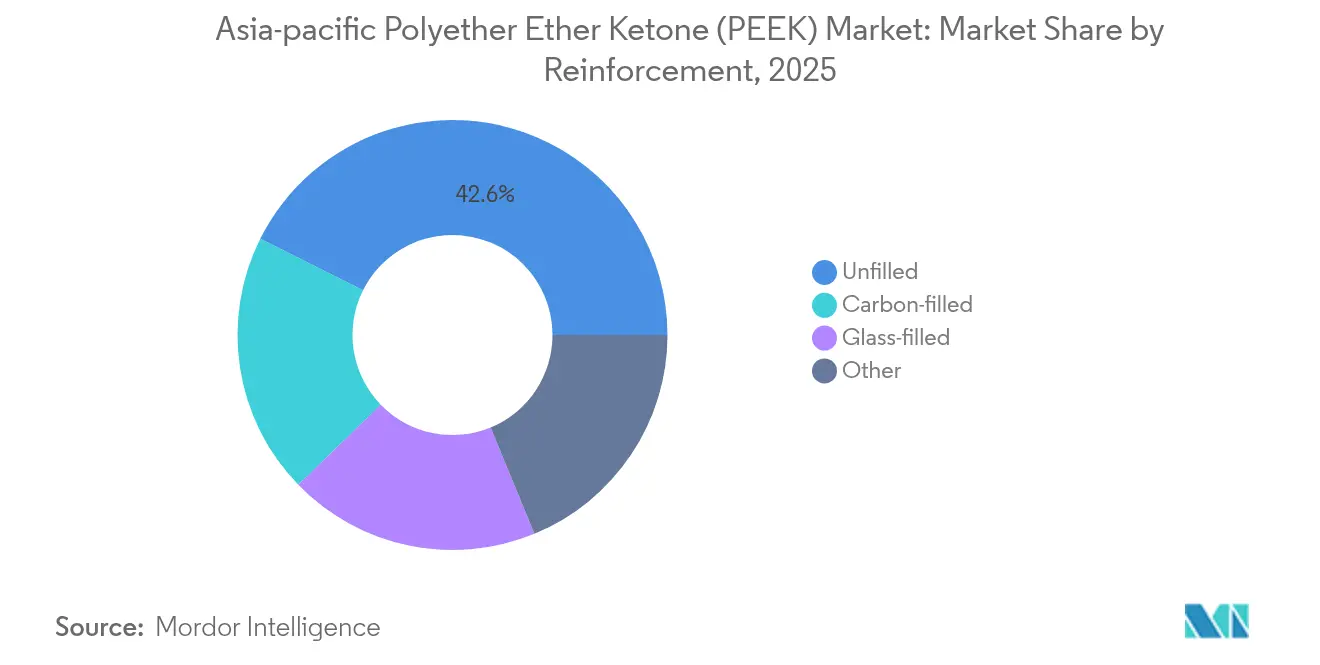

- By reinforcement, unfilled grades held a 42.62% Asia-Pacific PEEK market share in 2025, while carbon-filled variants are advancing at a 6.45% CAGR through 2031.

- By geography, China dominated with a 59.59% Asia-Pacific PEEK market share in 2025, but India is projected to register the fastest 5.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Polyether Ether Ketone (PEEK) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting push in aerospace and automotive | +1.8% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Electronics and semiconductor capacity boom | +1.2% | China, South Korea, Japan, Malaysia | Short term (≤ 2 years) |

| Growth in medical implants and devices | +0.9% | Japan, South Korea, Australia, China | Long term (≥ 4 years) |

| Local Chinese capacity expansions lowering cost | +1.1% | China, APAC spillover | Short term (≤ 2 years) |

| China “New Materials” localisation incentives | +0.7% | China, APAC spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electronics and Semiconductor Capacity Boom

Semiconductor fabs across China, South Korea, and Japan add multiple 300 mm lines, each consuming several tonnes of ultra-high-purity PEEK for CMP retaining rings, wafer carriers, and plasma-etch fixtures. Government incentive packages accelerate greenfield projects, while fab toolmakers specify PEEK for thermal stability above 250 °C and dimensional retention under corrosive chemistries. On-board 800 V EV inverter designs also capitalize on PEEK’s dielectric profile, reinforcing demand synergies between automotive and chip industries. Rapid commissioning timelines favor localized resin supply, tightening the link between electronic capital expenditure and near-term volume gains for the Asia-Pacific PEEK market. Materials suppliers that certify contamination-free grades capture sticky qualification positions, thereby embedding long-run offtake.

Lightweighting Push in Aerospace and Automotive

Asia-Pacific carriers ordered 1,365 aircraft in 2023, exceeding the prior year by 133%, and each single-aisle platform integrates 20–25 kg of PEEK across brackets, ducts, and seat structures to cut fuel burn. Electric vehicle makers in China, Japan, and South Korea substitute metal for carbon-filled PEEK in battery housings and e-motor insulation, shaving 1–2 kg per vehicle without compromising crash integrity. OEMs report that a 10% weight reduction in propulsion components can extend EV range by roughly 5%, enhancing regulatory compliance and consumer acceptance. Composite leaf springs, thermal-runaway shields, and power-electronics mounts now routinely specify PEEK, pushing the Asia-Pacific PEEK market toward higher-margin formulations. As aerospace recovery sustains double-digit growth in Asia, lightweighting remains a long-cycle catalyst for continuous volume escalation.

Growth in Medical Implants and Devices

Biocompatible, radiolucent PEEK spinal cages enable surgeons to monitor bone fusion without imaging artifacts, accelerating postoperative assessment. India’s National Medical Device Policy aims for 10-12% global share within 25 years, signaling future procurement pull for domestic manufacturers adopting PEEK. ASEAN regulatory harmonization shortens time-to-market, and additive manufacturing now prints patient-matched cranial plates using sterilizable PEEK filaments. These developments collectively ensure that medical applications secure a durable growth pillar for the Asia-Pacific PEEK market through 2030 and beyond.

Local Chinese Capacity Expansions Lowering Cost

Producers such as Zhongyan lifted pure PEEK nameplate to 1,000 tpa and achieved 112.36% utilization in 2024; phase-II debottlenecking adds 5,000 tpa downstream compounding to supply aerospace and electronics processors directly. Parallel upstream projects—most notably Zhongxin Fluorochemical’s 5,000 tpa DFBP line—drive feedstock self-sufficiency and reduce import reliance. Localized aromatic-ketone capacity trims resin prices by up to 15% relative to 2023 spot quotes, widening the cost-performance envelope for mid-tier processors. Lower delivered cost broadens the Asia-Pacific PEEK market user base, inviting substitution in moderate-temperature uses previously served by PPS or PSU. Multinationals respond by negotiating tolling arrangements in China to preserve share and recapture cost competitiveness.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High resin and processing cost | -1.3% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Stringent medical/aerospace certification | -0.8% | Japan, Australia, South Korea | Long term (≥ 4 years) |

| Volatile DFBP feedstock supply | -0.6% | China, APAC spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Resin and Processing Cost

Even after the recent decline, unfilled PEEK resin trades at a premium multiple times that of standard engineering plastics because DFBP synthesis requires high-temperature fluorination and strict moisture control. Injection processors must run barrel temperatures above 400 °C, consuming 10–15% more energy than polyamide molding, and screw metallurgy upgrades add capital cost. Price sensitivity caps adoption in commodity housings, leaving the Asia-Pacific PEEK market focused on mission-critical applications that justify elevated cost through performance or weight savings. Tier-2 OEMs with low volume often delay material switchovers until resin price volatility stabilizes. Cost remains the most immediate brake on widespread substitution despite unit costs inching downward on domestic expansions.

Stringent Medical/Aerospace Certification

Medical manufacturers must clear country-specific biocompatibility and sterilization tests that can stretch beyond 24 months, while aerospace suppliers navigate stringent AS9100 and NADCAP audits, plus traceability mandates across the entire value chain. Smaller Chinese and Indian entrants face proportionally higher compliance costs, curbing near-term share gains. Extended qualification cycles slow the pace at which next-generation PEEK grades displace metal incumbents even when technical superiority is evident. Consequently, the Asia-Pacific PEEK market experiences a lag between material innovation and revenue recognition in these regulated segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Industrial Machinery Holds Volume Edge as Automotive Accelerates

The industrial and machinery segments led with a 26.88% share of the Asia-Pacific PEEK market in 2025, driven by chemical plant retrofits and factory automation investments that favor long-life, self-lubricating materials. Robotics, compressor seals, and centrifugal pump wear rings exemplify applications where downtime costs dwarf resin premiums. Yet automotive parts show the highest 5.99% CAGR to 2031 because EV powertrains expose components to 180 °C–200 °C continuous temperatures and aggressive coolants that exceed the capabilities of PPS or PA. Busbars made from PEEK carry 800 V loads while remaining lightweight and corrosion-free, and battery-module side plates insulate against thermal runaway.

Electronics and semiconductor tooling maintain strong single-digit expansion, adding stable baseline volume to the Asia-Pacific PEEK market. Aerospace remains a strategic beachhead, and medical devices absorb specialized high-margin grades such as radiopaque barium-sulfate-loaded PEEK for trauma screws. In downstream verticals where regulatory barriers loom, close teamwork between resin suppliers and OEMs accelerates qualification, but the payoff includes multi-year exclusivity and sticky EBITDA streams. Across sectors, convergence of electrification, automation, and sustainability themes keeps the addressable opportunity set expanding well past 2031.

By Reinforcement: Unfilled Leadership Giving Way to Carbon-Filled Momentum

In 2025, unfilled grades captured 42.62% of the Asia-Pacific PEEK market size thanks to broad use in industrial valves, compressor rings, and chemical-process linings that demand high temperature stability without the added expense of fiber reinforcement. Carbon-filled versions record the steepest advance at a 6.45% CAGR to 2031 as aerospace and EV makers prioritize mechanical strength-to-weight performance. Glass-filled formulations bridge cost and modulus requirements for electronics connectors, delivering dimensional control during lead-free solder reflow. Niche hybrid systems that blend carbon and PTFE are being trialed in wear-critical bearings, underscoring a migration from base functionality to differentiated property matrices.

Manufacturers increasingly shift capacity toward reinforced grades because pricing premiums comfortably offset incremental compounding costs. Robotics component makers in China report double-digit growth for carbon-fiber reinforced PEEK gears that cut inertia and noise in high-speed joints. These developments reinforce the pattern of value migration within the Asia-Pacific PEEK market toward formulations that maximize weight savings and mechanical integrity, sustaining unit profitability even amid resin price deflation.

Geography Analysis

China commanded 59.59% of the Asia-Pacific PEEK market size in 2025, underpinned by its integrated value chain that now spans DFBP feedstocks through finished compounds. Domestic producers leverage favorable energy tariffs, targeted tax credits, and expedited permitting under the “New Materials” plan to reduce variable costs. Tier-one resin makers collaborate with local aircraft interiors suppliers to secure qualification and shorten design cycles. Rising EV output—surpassing 9 million units in 2024—adds fresh demand for motor insulation films and coolant-facing fittings. Industrial OEMs further entrench PEEK in high-temperature pump casings for sulfur-acid service, locking in base load consumption.

India trails with a modest share today but boasts a 5.82% CAGR to 2031, outpacing the regional total. Automotive policies incentivize lightweight components; at the same time, nascent aerospace supply chains benefit from government-led offset requirements tied to widebody procurement. Domestic implant makers ramp spinal cage production as reimbursement frameworks expand in tertiary care, introducing a stabilizing pull for medical-grade PEEK. State initiatives such as “Make in India” reinforce inward manufacturing, gradually cultivating a localized ecosystem that will underpin a larger Asia-Pacific PEEK market over the next five years.

Competitive Landscape

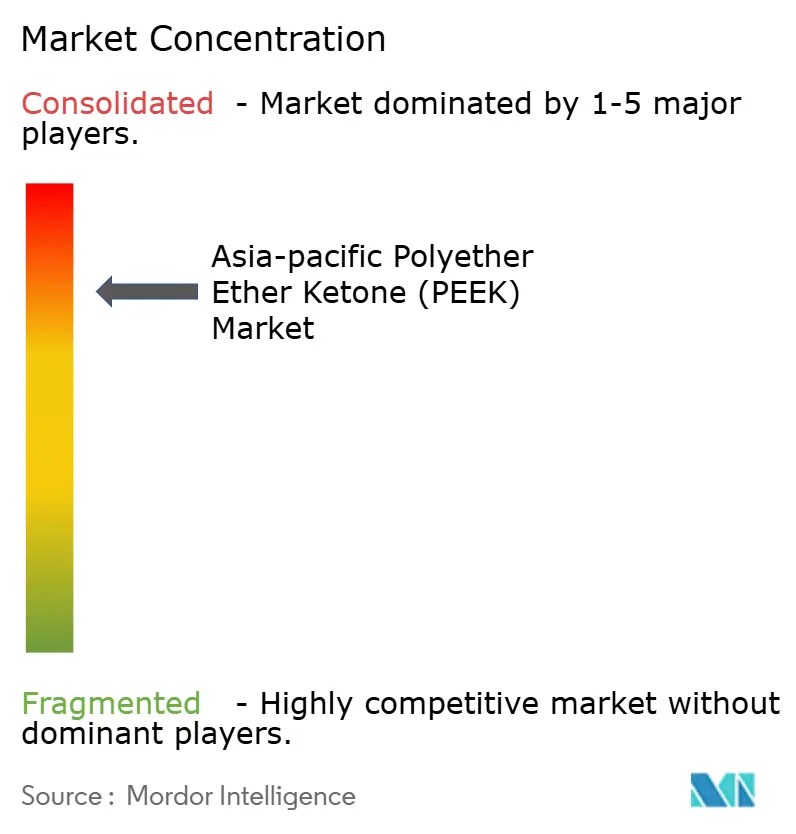

The Asia-Pacific PEEK market demonstrates consolidation. Victrex and Solvay remain technology leaders, offering ultraclean and medical-implant certified grades that command significant price premiums. Evonik’s focus on 3-D printable carbon-fiber filaments captures additive manufacturing niches in medical and aerospace spares. Strategic plays include long-term supply agreements with electric powertrain OEMs and joint research and development projects for heat-dissipative film. Global incumbents are localizing compounding in Suzhou and Wuxi to tap into China’s EV corridor, while retaining European melt filtration assets for ultrapure semiconductor grades.

Asia-Pacific Polyether Ether Ketone (PEEK) Industry Leaders

Evonik Industries AG

Jilin Joinature Polymer Co., Ltd.

Pan Jin Zhongrun High Performance Polymer Co., Ltd.

Syensqo

Victrex plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Essentra Components released a line of high-temperature PEEK fasteners for fuel systems and ultra-high vacuum assemblies.

- October 2023: Evonik Industries introduced a carbon-fiber reinforced PEEK filament for extrusion-based 3-D printing of medical implants.

Asia-Pacific Polyether Ether Ketone (PEEK) Market Report Scope

Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Australia, China, India, Japan, Malaysia, South Korea are covered as segments by Country.| Aerospace |

| Automotive |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-User Industries |

| Unfilled |

| Glass-filled |

| Carbon-filled |

| Other |

| China |

| India |

| Japan |

| South Korea |

| Malaysia |

| Australia |

| Rest of Asia-Pacific |

| By End-User Industry | Aerospace |

| Automotive | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Other End-User Industries | |

| By Reinforcement | Unfilled |

| Glass-filled | |

| Carbon-filled | |

| Other | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Australia | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyether ether ketone market.

- Resin - Under the scope of the study, virgin polyether ether ketone resin in primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms