Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

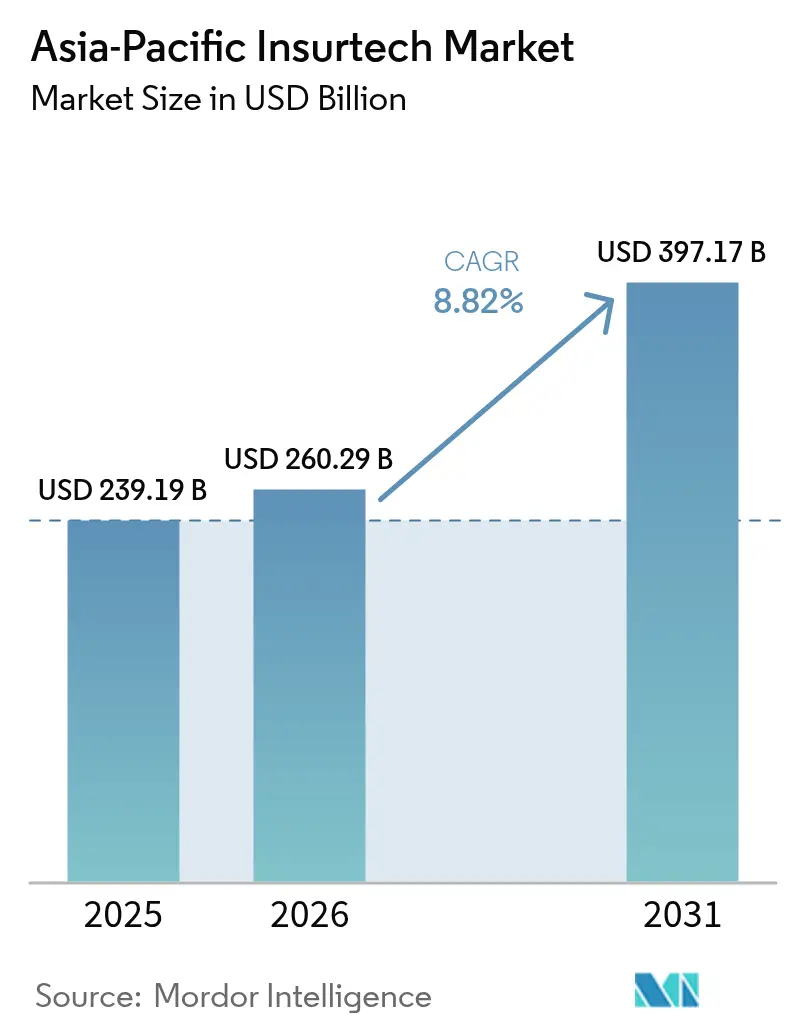

| Base Year Market Size (2025) | USD 239.19 Billion |

| Market Size (2026) | USD 260.29 Billion |

| Market Size (2031) | USD 397.17 Billion |

| Growth Rate (2026 - 2031) | 8.82% CAGR |

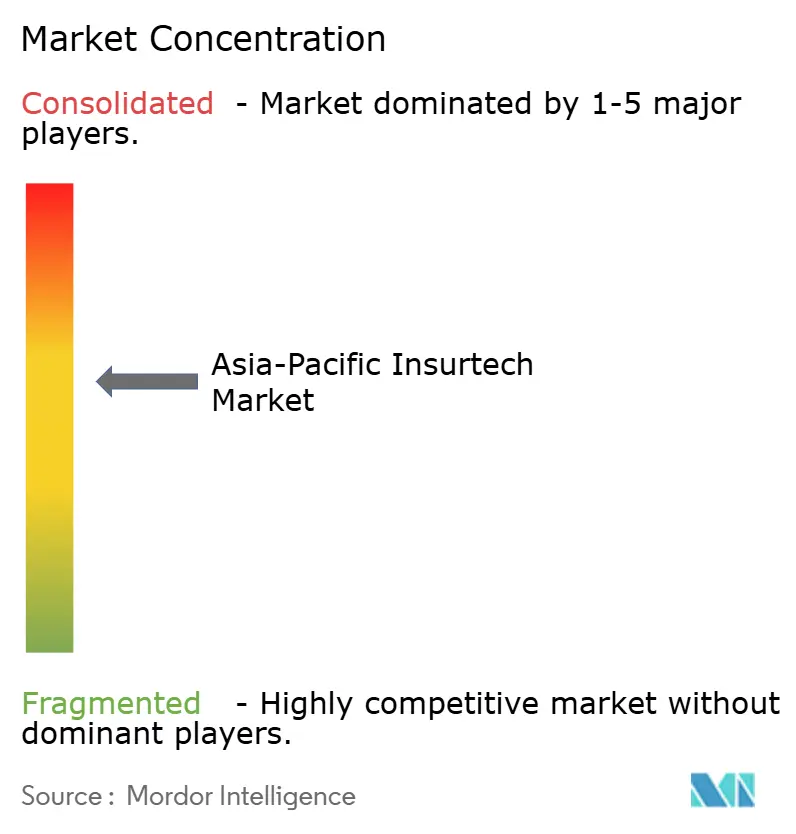

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Insurtech Market Analysis by Mordor Intelligence

The Asia-Pacific Insurtech Market size is expected to grow from USD 239.19 billion in 2025 to USD 260.29 billion in 2026 and is forecast to reach USD 397.17 billion by 2031 at 8.82% CAGR over 2026-2031.

This resilient growth is rooted in smartphone-first distribution economics, regulatory sandbox acceleration, and the use of advanced analytics that enhance underwriting precision and claims automation. Embedded-insurance ecosystems now secure previously unreachable retail and SME customers, while cross-border regulatory harmonization inside ASEAN lowers entry barriers for multi-market platforms. Falling mobile-acquisition costs, a surge in specialty-risk awareness, and fresh capital flowing into parametric solutions further reinforce the upside for the Asia-Pacific insurtech market. Competitive dynamics remain fluid as AI-enabled underwriting erodes traditional loss-ratio advantages and encourages incumbents to form strategic alliances with fintechs.

Key Report Takeaways

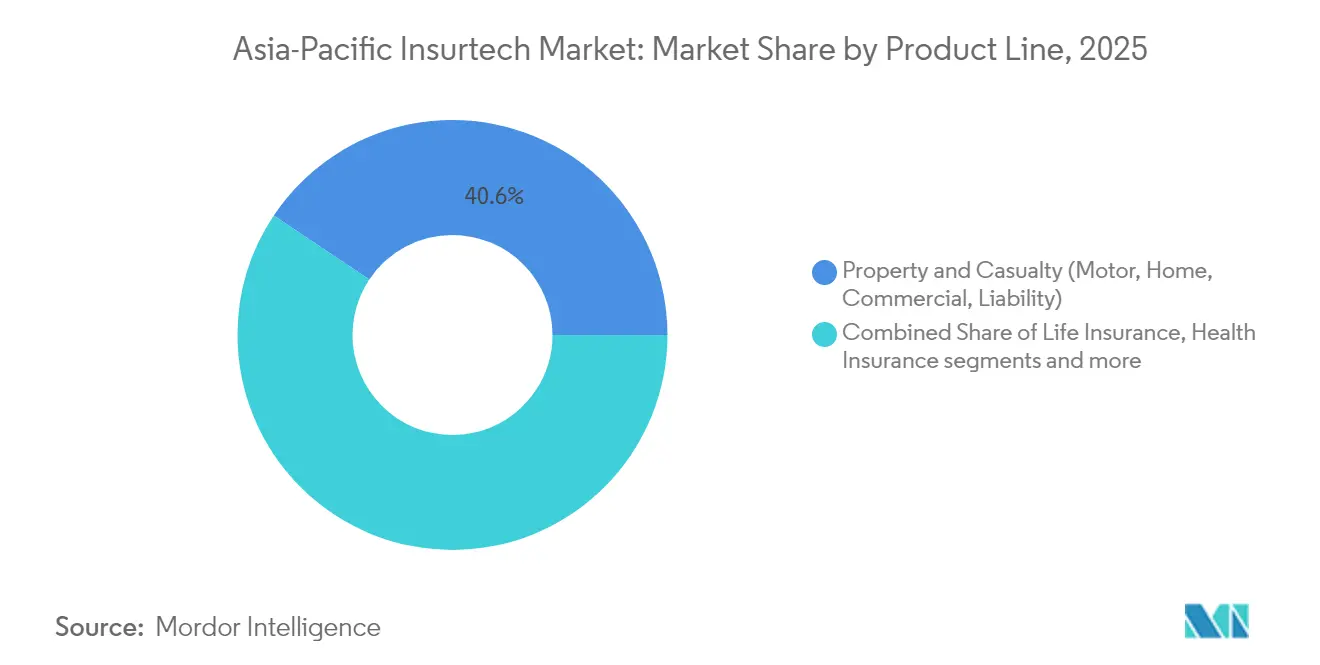

- By product line, Property & Casualty led with 40.62% revenue share of the Asia-Pacific insurtech market in 2025; Specialty Lines are projected to expand at a 9.86% CAGR through 2031.

- By distribution channel, Digital Brokers and MGAs held 28.35% of the Asia-Pacific insurtech market share in 2025, while Embedded Insurance Platforms are advancing at a 9.05% CAGR to 2031.

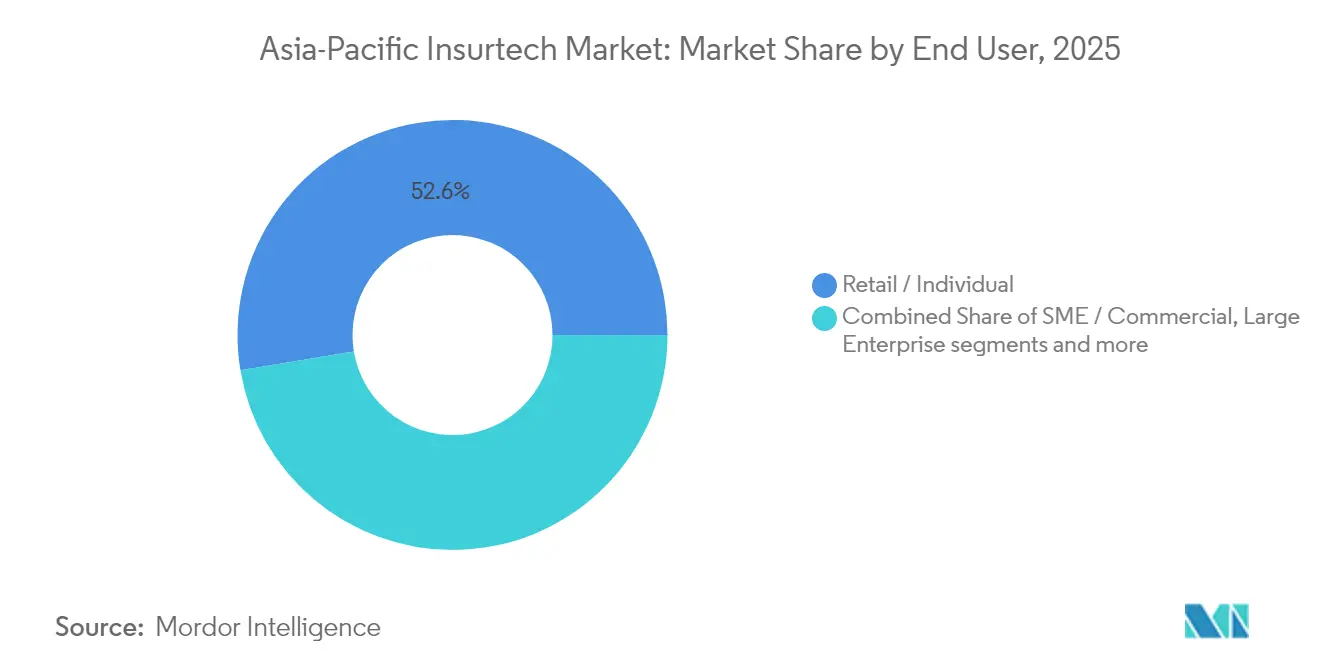

- By end user, Retail and Individual customers accounted for 52.63% of the Asia-Pacific insurtech market size in 2025, and the SME/Commercial segment is rising at a 9.74% CAGR to 2031.

- By geography, China commanded 43.10% of the 2025 revenue of the Asia-Pacific insurtech market; India is forecast to grow at a 10.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Insurtech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Embedded-insurance ecosystems | +1.8% | China, Singapore, region-wide | Medium term (2-4 years) |

| Rising cyber-risk exposure | +1.5% | All APAC cores | Short term (≤ 2 years) |

| Smartphone-first acquisition cost drop | +1.2% | India, Southeast Asia | Short term (≤ 2 years) |

| Sandbox regulatory fast-tracks | +1.0% | Singapore, India, Thailand, Indonesia | Medium term (2-4 years) |

| Advanced analytics/Gen-AI accuracy | +0.9% | Japan, Australia, Singapore, China | Long term (≥ 4 years) |

| Climate-linked parametric traction | +0.7% | Australia, Philippines, Indonesia, Pacific Islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Embedded-Insurance Ecosystems

Embedded platforms place cover inside everyday purchase journeys, letting users buy protection without leaving the host app[1]Pang-Hsiang Chye et al., “FinTech in ASEAN 2024: A Decade of Innovation,” PwC, pwc.com. This seamless flow removes agent friction and cuts acquisition costs by up to 40%, a saving that improves unit economics at scale. Ant Group’s partnership with Alibaba shows the model’s reach as premiums emerge from e-commerce, travel, and wallet transactions. Singapore’s clear API guidelines allow non-insurers to distribute products under existing fintech licenses, keeping compliance overhead low. Higher engagement across multiple touchpoints feeds behavioral data back to underwriters, raising pricing accuracy and lowering loss ratios. These network effects reinforce adoption, positioning embedded insurance as a structural growth engine for the Asia-Pacific insurtech market.

Sharp Increase in Asia-Pacific Cyber-Risk Exposure

Digital transformation widens attack surfaces across health care, finance, and manufacturing, driving urgent demand for cyber cover. Singapore’s 2024 AI Model Risk Management rules compel financial firms to prove robust controls, pushing buyers toward policies that document compliance. Insurtechs respond with parametric cyber products that pay automatically on metrics like downtime minutes, avoiding long investigations. Real-time pricing engines ingest threat-intel feeds and vulnerability scans, letting underwriters match premiums to each client’s security posture. Cloud concentration risk grows as hyperscale providers expand regional centers, adding urgency for bespoke policies[2]Luke Gallin, “Hannover Re & Parametrix launch world’s first cloud outage catastrophe bond,” Reinsurance News, reinsurancene.ws. Together, these forces raise cyber insurance penetration yet leave ample protection gaps for agile entrants.

Smartphone-First Customer Acquisition Costs Falling

Mobile penetration exceeds 80% in India and large parts of Southeast Asia, giving insurers a direct consumer channel at marginal cost. Policybazaar shows the benefit as video KYC and AI document checks shorten onboarding from weeks to minutes, lifting conversions. Social-media algorithms enable precise demographic targeting, lowering marketing spend while boosting relevance. Micro-insurance products delivered through digital wallets reach lower-income users who lack bank accounts, widening the premium base. Funding flows follow efficiency; investors raise allocations to mobile-first insurtechs given their quicker path to profitability. Falling acquisition costs therefore underpin the sustained expansion of the Asia-Pacific insurtech market.

Sandbox-Style Regulatory Fast-Tracks Across Asia-Pacific

Regulatory sandboxes in Singapore, India, Indonesia, and Thailand let firms test products with relaxed rules, trimming innovation cycles by up to two years. Singapore’s Guardian Funds Framework tokenizes insurance assets, illustrating how pilots de-risk bold concepts before wide release. India’s IRDAI motor reforms remove depreciation calculations and base sums insured on on-road prices, simplifying digital product design. Data gathered in sandboxes informs permanent policies, creating a feedback loop that aligns regulation with technology. Cross-border work on the ASEAN Digital Economy Framework promises shared standards that cut compliance duplication. Faster approvals and clearer rules stimulate capital inflows and encourage regional scaling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy fragmentation | -1.3% | All APAC, cross-border setups | Medium term (2-4 years) |

| Profit-pool lock-in among incumbents | -1.0% | China, Japan, Australia | Medium term (2-4 years) |

| Thin actuarial histories for new risks | -0.8% | Emerging markets, global specialty | Long term (≥ 4 years) |

| Rising reinsurance pricing and capacity strain | -0.7% | Cat-exposed regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Privacy Fragmentation by Jurisdiction

APAC regulators each impose unique consent, storage, and transfer rules, forcing insurtechs to build separate data stacks for every market[3]ASEAN Secretariat, “Assessing the Relationship Between ICT Infrastructure and Digital Skills,” asean.org. Compliance teams must master Singapore’s PDPA, India’s Digital Personal Data Protection Act, and China’s Cybersecurity Law, driving costs 25-35% higher than single-market peers. Fragmentation slows embedded-insurance rollouts because real-time data sharing with partners may breach residency rules. Reinsurers struggle to pool risks across borders when one jurisdiction’s strictest requirement governs all shared data. Ongoing changes add further uncertainty as governments tighten or relax clauses with short notice. The resulting complexity diverts capital from product development and constrains the Asia-Pacific insurtech market’s regional scaling.

Thin Actuarial Loss Histories for New-Risk Products

Cyber, climate parametric, and gig-economy covers often have fewer than three years of credible claims data, making pricing volatile[4]Guy Carpenter, “Global Specialties 2024 Market Update,” guycarp.com. Traditional actuarial models rely on long loss histories; without them, underwriters use proxy datasets that may misstate frequency or severity. Reinsurers respond by raising attachment points and premiums, limiting capacity for primary carriers. Higher capital charges under solvency rules further dampen appetite for unproven lines. Insurtechs employ satellite imagery, IoT sensors, and social analytics to enrich datasets, but regulators vary on accepting such inputs. Until deeper histories form, uncertainty will continue to curb specialty-line expansion within the Asia-Pacific insurtech market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Line: Specialty Lines Outpace Core Property & Casualty

Property & Casualty retained 40.62% of 2025 premiums, giving it the largest slice of the Asia-Pacific insurtech market share. Stable claim patterns, long-standing regulatory familiarity, and highly digitized motor and household lines underpin this dominance, yet growth momentum is slowing as pricing competition intensifies and catastrophe losses pressure underwriting margins. Specialty Lines, in contrast, are expanding at a 9.86% CAGR, lifting their contribution to the Asia-Pacific insurtech market size year after year as cyber, pet, and travel covers gain recognition across corporate and consumer segments. Parametric cyclone pilots in the Philippines and Fiji illustrate how rapid-payout products can fill long-standing protection gaps and attract multilateral donor funding, giving specialty carriers both social relevance and profitable scale.

Cyber insurance remains the specialty headline as ransomware costs rise, yet actuarial thinness keeps reinsurance attachment points high, tempering near-term penetration. Insurtechs mitigate data scarcity by fusing threat-intelligence feeds, endpoint telemetry, and cloud-service uptime metrics into dynamic underwriting models that reward strong security hygiene with lower premiums. Pet insurance follows a similar data-rich trajectory as tele-vet usage supplies continuous behavioral information that sharpens pricing. Marine and inland transit lines leverage satellite cargo tracking to trigger parametric payouts for voyage disruptions, cutting claims friction for exporters. Together, these innovations lift average premium growth well above the market baseline, positioning Specialty Lines as the primary long-run value engine of the Asia-Pacific insurtech market.

By Distribution Channel: Embedded Platforms Accelerate Share Migration

Digital Brokers and MGAs held 28.35% of 2025 revenue owing to mature search-engine funnels, multilingual call centers, and regulator-approved onboarding scripts that maximize completion rates. Their predictable economics attract global reinsurer sponsorship yet embedded-insurance partnerships are eroding this advantage by inserting cover directly at the digital checkout moment when purchase intent is highest. The embedded channel is expanding at a 9.05% CAGR, the fastest across distribution, and its rise is already visible in sectors such as BNPL loans and ride-hailing protections that auto-populate policy details from existing customer records.

Direct-to-Consumer websites sustain moderate growth but fight high search-marketing costs as comparison engines commoditize prices. Traditional agents pivot to hybrid models that blend in-person advice for complex covers with app-based issuance for simple risks, slowing but not reversing share loss. Bancassurance remains important for life and health policies; banks now embed quote widgets inside mobile banking dashboards to keep pace with fintech rivals. Aggregator marketplaces test subscription loyalty programs to curb user churn, though early evidence shows mixed stickiness. All signs point to a multichannel future where contextual, API-driven journeys win incremental share from stand-alone portals within the Asia-Pacific insurtech market.

By End User: SME Uptake Narrows the Retail Gap

Retail and Individual customers contributed 52.63% of 2025 premiums as smartphone-first carriers brought micro-covers to hundreds of millions of new buyers. Growth, however, is migrating toward SME and Commercial accounts that are forecast to generate a 9.74% CAGR through 2031, lifting their portion of the Asia-Pacific insurtech market size as digital bookkeeping and e-invoicing data unlock automated underwriting.

Embedded integrations with e-commerce seller dashboards, neobank treasury modules, and SaaS subscription billing services allow SMEs to bind cyber, cargo, and credit insurance in minutes without broker intervention. Alternative data, such as point-of-sale analytics, ride-sharing logs, and warehouse IoT sensors, enrich risk scoring, enabling carriers to right-size limits and deductibles for thin-file businesses. Government initiatives to digitize procurement portals add mandatory insurance requirements, further catalyzing SME adoption. Large enterprises remain a mature, heavily brokered cohort focused on program optimization rather than volume expansion, while public-sector demand is slowly emerging as municipalities protect infrastructure against climate and cyber shocks. Together, these trends position SMEs as the pivotal growth lever for the Asia Pacific insurtech market.

Geography Analysis

China held 43.10% of 2025 premiums, reflecting its deep mobile-payment penetration, multi-super-app ecosystems, and strong policy backing for fintech innovation. The Asia-Pacific insurtech market size in China exceeded USD 103.1 billion in 2025 and continues to climb on the strength of e-commerce-embedded covers and AI-based underwriting deployed by leaders such as ZhongAn. Economic headwinds and stricter tech oversight are nudging carriers toward profitability metrics, yet the market continues to innovate, notably through tokenized insurance assets that broaden reinsurance capacity via capital markets.

India, forecast to grow at a 10.42% CAGR, benefits from IRDAI motor reforms that abolish depreciation deductions for vehicles under three years old, simplifying digital quoting and expanding average sum insured. Smartphone saturation in tier-2 and tier-3 cities now approaches urban levels, letting platforms push micro-health and hospitalization covers through mobile wallets. Policybazaar’s cross-sell into telemedicine exemplifies the ecosystem playbook that deepens customer lifetime value. Regulatory sandboxes encourage pilots in crop-yield index and gig-worker accident products, widening addressable segments and cementing India’s position as the fastest-rising component of the Asia-Pacific insurtech market.

Japan, Australia, and South Korea present technologically mature, high-premium pools where GenAI triage tools, autonomous-vehicle telematics, and climate parametric carve out incremental revenue. Japan’s life insurers deploy large-language models to cut claim-file time, freeing staff for complex case management. Australia’s cyclone and flood parametric pilots supported by state disaster funds prove the commercial viability of rapid-payout solutions and suggest export potential across the Pacific Islands. Southeast Asia collectively outpaces the regional mean as ASEAN frameworks harmonize data localization and e-KYC norms, offering regional insurtechs a 600-million-person sandbox. Cross-border e-commerce, tourism rebound, and rising SME formalization further stoke premium volumes, reinforcing the bloc’s role as the next frontier for the Asia-Pacific insurtech market.

Competitive Landscape

The Asia-Pacific insurtech industry hosts a mix of digital-native scale players, carrier-backed spin-offs, and niche specialists vying for data, distribution, and capital advantages. ZhongAn, Policybazaar, and bolttech have each surpassed the USD 1 billion valuation threshold, giving them acquisition currency and regional brand recognition. Their strategies converge on ecosystem partnerships: ZhongAn plugs household covers into Ant Group wallets, Policybazaar bundles telehealth within health policies, and bolttech offers device protection inside telco subscriptions.

Incumbent insurers counter with venture investments and joint ventures. Sompo’s 2024 partnership with Palantir to embed AI in claims triage signals how legacy carriers can shorten data-science learning curves while retaining balance-sheet depth. Allianz’s move to take a majority stake in Singapore’s Income Insurance reflects the logic of securing regional licenses and established policy books before competitive price points compress margins. Reinsurers provide enabling infrastructure; Hannover Re’s cloud outage catastrophe bond showcases appetite for tech-centric retro solutions that free primary carriers to write new risks.

Competitive intensity rises as regulatory sandboxes slash entry costs and venture funds chase embedded-insurance upside. Yet barriers persist in actuarial depth, reinsurance access, and compliance scale. Players that combine AI-rich underwriting, seamless API distribution, and capital markets flexibility are consolidating share gains. Overall, the top five groups now hold roughly 55% of regional digital premiums, pointing to a moderately concentrated field within the Asia-Pacific insurtech market.

Asia-Pacific Insurtech Industry Leaders

ZhongAn Insurance

Policybazaar

Acko

PasarPolis

Singlife

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Waterdrop reported RMB 2.77 billion revenue and RMB 367.5 million net profit for 2024, marking a 5.4% year-over-year top-line rise. The firm is integrating DeepSeek’s generative-AI models into underwriting and customer service, aiming to lift automation accuracy and shorten claim-handling time.

- February 2025: Qoala closed a USD 47 million Series C round led by PayPal Ventures with follow-on backing from existing investors. The capital will fund API upgrades for e-commerce partners and accelerate embedded-insurance rollouts in Indonesia, Thailand, and Vietnam.

- January 2025: Bolttech secured fresh Series C funding from Dragon Fund, keeping its valuation above USD 1 billion. Management plans to deepen device-protection integrations with Asian telcos and extend its broker-as-a-service platform to new markets.

- December 2024: The Monetary Authority of Singapore issued AI Model Risk Management guidelines that set governance, validation, and audit standards for underwriting and claims algorithms. Insurtechs welcomed the clarity, noting it reduces compliance uncertainty for scaling GenAI applications across multiple product lines.

Asia-Pacific Insurtech Market Report Scope

Insurtech is using new technology to improve the efficiency of how insurance is sold right now. This report offers a comprehensive analysis of the Asia-Pacific insurtech market. It delves into market dynamics, highlights emerging trends across segments and regional markets, and provides insights into diverse product and application types. Additionally, the report scrutinizes key players and the competitive landscape.

The Asia-Pacific insurtech market is segmented by insurance lines, which include health, life, and non-life. By country, the market is segmented into China, India, Japan, Hong Kong, Singapore, Indonesia, and the Rest of Asia-Pacific. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Product Line (Insurance Type)

| Life Insurance |

| Health Insurance |

| Property & Casualty (Motor, Home, Commercial, Liability) |

| Specialty Lines (Cyber, Pet, Marine, Travel) |

By Distribution Channel

| Direct-to-Consumer (Digital) |

| Aggregators / Marketplaces |

| Digital Brokers / MGAs |

| Embedded Insurance Platforms |

| Traditional Agents / Brokers (digitally enabled) |

| Bancassurance (digitally enabled) |

| Other Channels |

By End User

| Retail / Individual |

| SME / Commercial |

| Large Enterprise / Corporate |

| Government / Public Sector |

By Country

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia |

| Rest of Asia-Pacific |

| By Product Line (Insurance Type) | Life Insurance |

| Health Insurance | |

| Property & Casualty (Motor, Home, Commercial, Liability) | |

| Specialty Lines (Cyber, Pet, Marine, Travel) | |

| By Distribution Channel | Direct-to-Consumer (Digital) |

| Aggregators / Marketplaces | |

| Digital Brokers / MGAs | |

| Embedded Insurance Platforms | |

| Traditional Agents / Brokers (digitally enabled) | |

| Bancassurance (digitally enabled) | |

| Other Channels | |

| By End User | Retail / Individual |

| SME / Commercial | |

| Large Enterprise / Corporate | |

| Government / Public Sector | |

| By Country | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the 2026 value of the Asia Pacific insurtech market?

The market stood at USD 260.29 billion in 2026 and is on track to reach USD 397.17 billion by 2031.

Which product line is growing fastest across the Asia Pacific?

Specialty Lines such as cyber, pet, and travel covers are expanding at a 9.86% CAGR through 2031.

Why are embedded-insurance platforms important in Asia?

They insert cover directly into digital checkout flows, cutting acquisition costs by up to 40% and raising conversion rates.

Which geography shows the highest forecast growth?

India is projected to grow at a 10.42% CAGR on the back of progressive IRDAI reforms and smartphone adoption.

How are regulatory sandboxes shaping innovation?

Sandboxes in Singapore, India, and other markets shorten product-testing cycles by up to two years while giving regulators real-time insights.

What restrains faster specialty-risk uptake?

Thin actuarial histories and fragmented data-privacy rules raise capital charges and compliance costs, slowing scale.

Page last updated on: