Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

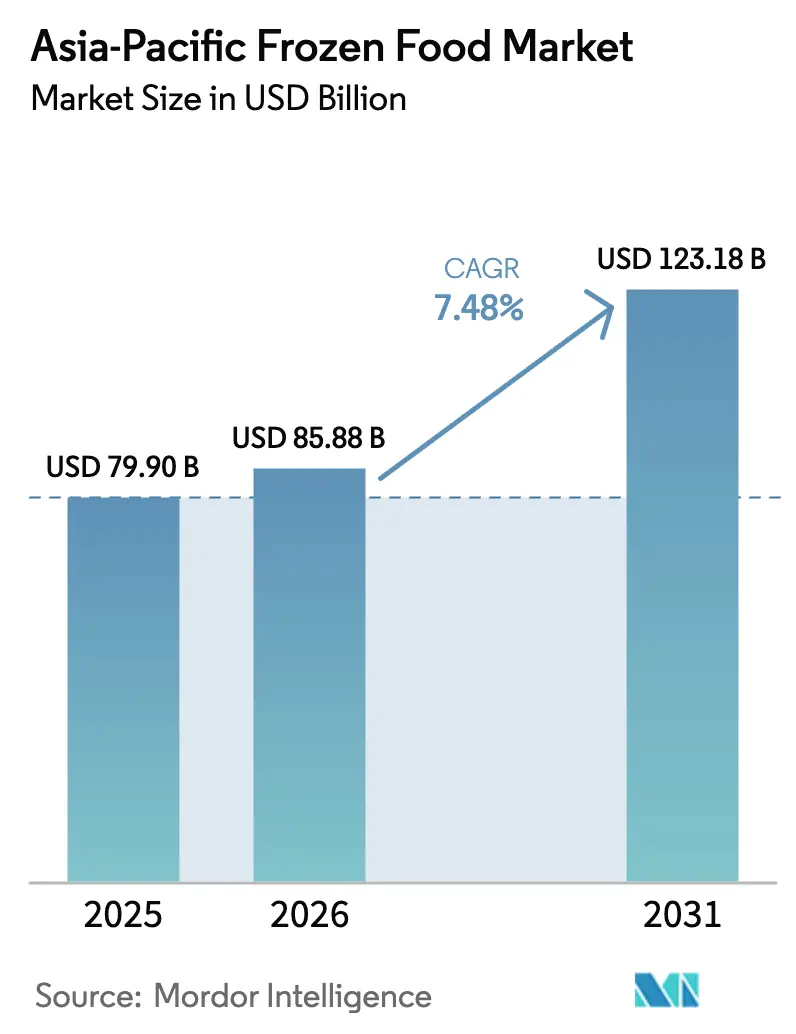

| Base Year Market Size (2025) | USD 79.90 Billion |

| Market Size (2026) | USD 85.88 Billion |

| Market Size (2031) | USD 123.18 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Frozen Food Market Analysis by Mordor Intelligence

The Asia-Pacific frozen food market size was valued at USD 79.90 billion in 2025 and estimated to grow from USD 85.88 billion in 2026 to reach USD 123.18 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031). The rapid expansion of the Asia-Pacific frozen food market is driven by evolving household dynamics, a surging demand for convenience, and enhancements in cold-chain infrastructure facilitating wider distribution. The most robust growth is observed in ready-to-eat and ready-meal segments, with innovations like ethnic-fusion recipes and single-serve options resonating with urban lifestyles. China stands as the dominant market, bolstered by robust logistics and governmental support. Meanwhile, India is making strides, propelled by investments in cold-chain infrastructure and e-commerce delivery models. In mature markets such as Japan and South Korea, there's a noticeable pivot towards premium offerings catering to an aging demographic. Southeast Asia, on the other hand, is experiencing double-digit growth, buoyed by the expansion of modern trade channels. The competitive landscape is moderately consolidated: global giants harness scale, local players leverage cultural insights, and the emergence of plant-based products alongside online grocers heightens the competition.

Key Report Takeaways

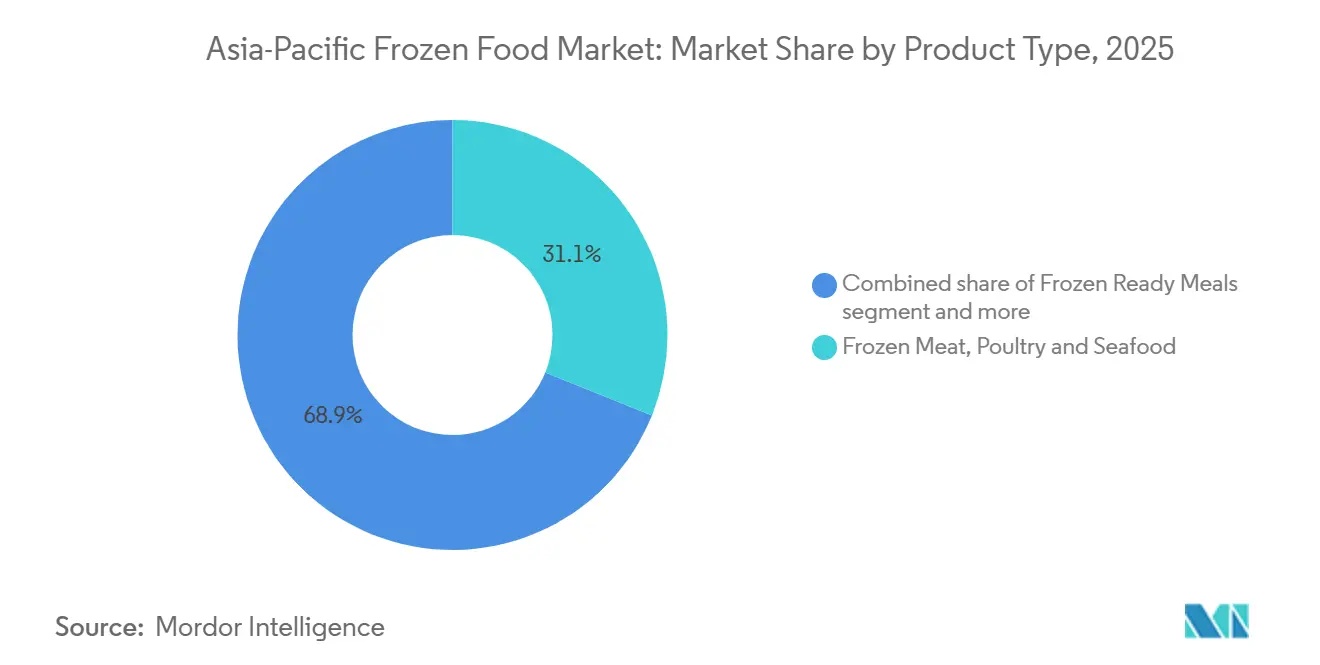

- By product type, frozen meat, poultry, and seafood led with 31.10% of the Asia-Pacific frozen food market share in 2025, while frozen ready meals are set to grow the fastest at a 7.52% CAGR through 2031.

- By category, ready-to-cook items commanded 67.25% of sales in 2025, whereas ready-to-eat offerings are projected to advance at a 7.55% CAGR to 2031.

- By nature, conventional formats accounted for 94.10% of volume in 2025, yet organic alternatives are forecast to expand at a 8.96% CAGR over the same period.

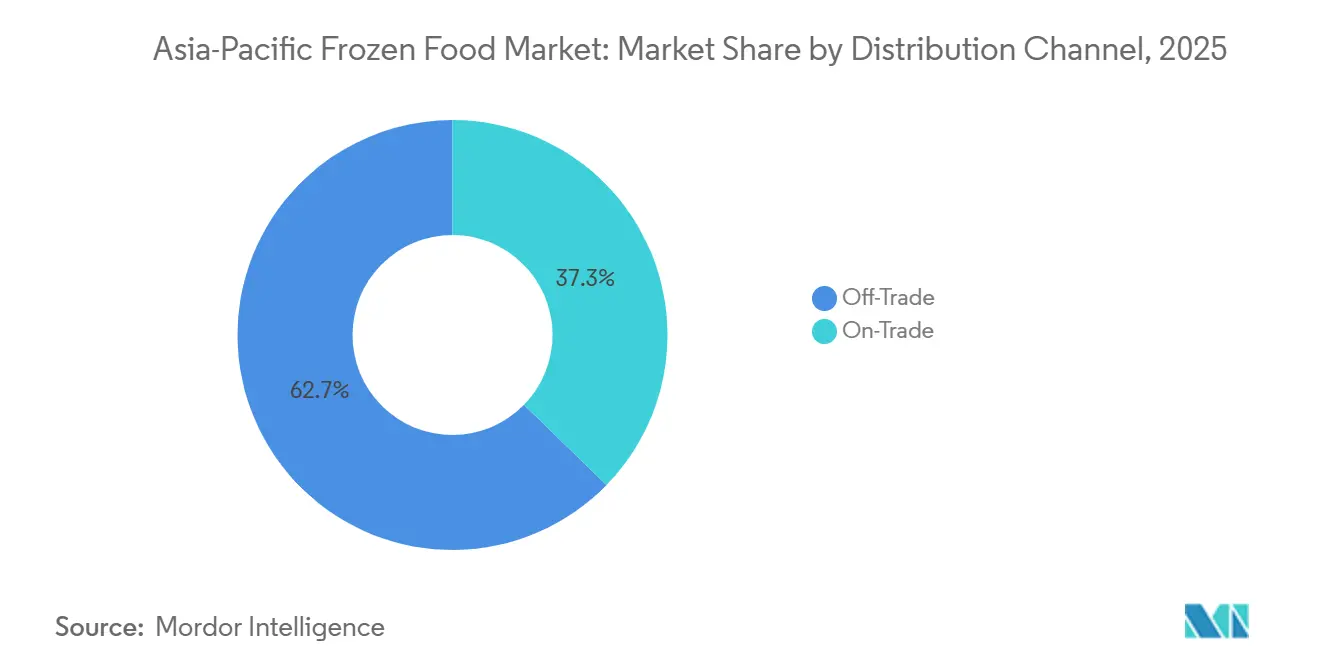

- By distribution channel, retail/off-trade channels captured 62.70% of 2025 revenue, while HoReCa/on-trade is expected to post the quickest rise at an 8.10% CAGR through 2031.

- By Geography, China held 31.05% of regional revenue in 2025, whereas India is on track for the highest growth with an 8.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in convenient meal solutions demand | +1.8% | China, India, Indonesia, urban ASEAN corridors | Short term (≤ 2 years) |

| Innovations in freezing and packaging technology | +1.3% | Global, with early adoption in Japan, South Korea, Australia | Medium term (2-4 years) |

| Longer shelf life enhances demand | +1.0% | India, Philippines, Vietnam, rural distribution zones | Medium term (2-4 years) |

| Rising health-consciousness leads to clean label preferences | +1.2% | Australia, New Zealand, Singapore, premium urban segments in China | Long term (≥ 4 years) |

| Expansion of plant-based frozen food options | +0.9% | Singapore, Hong Kong, metro India, coastal China | Medium term (2-4 years) |

| Online grocery and delivery channel adoption | +1.4% | China, India, South Korea, urban Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth In Convenient Meal Solutions Demand

As urbanization progresses across the Asia-Pacific region, there is a significant increase in demand for convenient meal solutions, driven by the working population's need for time-efficient food options. Thailand's ready-to-eat food industry exemplifies this trend, with domestic ready meals projected to experience annual growth through 2026, supported by economic recovery and shifting household dynamics. Urban centers in China and India are leading this demand surge. The growing prevalence of nuclear families and single-person households in these countries presents substantial market opportunities for frozen convenience products. This growth is further propelled by the expansion of modern retail formats and advancements in cold chain infrastructure, which facilitate the broader distribution of frozen ready meals to previously underserved markets. The rise of electronic commerce (e-commerce) platforms has transformed market accessibility, enabling consumers to conveniently order frozen meals for home delivery. Additionally, the increasing participation of women in the workforce across the region has driven higher demand for quick meal solutions that reduce cooking time. For instance, World Bank data indicates that in India, the female labor participation rate increased from 27.72% in 2021 to 32.80% in 2024 [1]Source: World Bank, "Female labor force participation rate across India", data.worldbank.org. Simultaneously, as consumer awareness regarding food safety and quality grows, manufacturers are responding by developing premium frozen meal options that emphasize cleaner labels and healthier ingredients.

Innovations In Freezing And Packaging Technology

In the Asia-Pacific region, technological advancements in freezing and packaging are enhancing product quality, safety, and distribution efficiency, thereby propelling the frozen food market. Innovations like cryogenic immersion freezing and state-of-the-art refrigeration systems curtail ice-crystal formation. This preservation of texture, flavor, and nutritional integrity boosts consumer acceptance of frozen seafood, fruits, and ready meals. Concurrently, smart packaging solutions, featuring time-temperature indicators and Quick Response (QR)-enabled traceability, are bolstering transparency and trust in the cold chain. These solutions, already embraced in markets like Japan and South Korea, are complemented by modified-atmosphere packaging. This latter innovation bolsters product resilience during last-mile delivery, especially in infrastructure-challenged regions like India. Together, these technological strides mitigate operational risks for processors and retailers, broaden their geographic reach, and hasten the adoption of frozen foods across both emerging and established markets in the Asia-Pacific.

Rising Health-Consciousness Lead to Clean Label Preferences

In the Asia-Pacific frozen food market, rising health consciousness is prompting consumers to closely examine ingredient lists, particularly for artificial additives, preservatives, and high sodium content. In Australia, updated front-of-pack labeling standards are driving manufacturers to reformulate their products[2]Source: Australia Government "Policy statement on front-of-pack labelling", foodregulation.gov.au. These regulatory actions push manufacturers to reduce sodium, eliminate controversial ingredients, and enhance overall nutritional profiles. Responding to this trend, major players like Nestlé have reformulated significant portions of their frozen portfolios, replacing certain oils and bolstering product health credentials to boost premium retail performance. In markets such as Singapore and New Zealand, clean-label claims like “no artificial ingredients,” “non-GMO,” and “organic certified” are increasingly common in new product launches. This trend is carving out a distinct premium tier, resonating with health-conscious millennials and Gen Z consumers who prioritize transparency and quality over price.

Expansion of plant-based frozen food options

Driven by the rise of plant-based options, the Asia-Pacific frozen food market is witnessing a significant transformation. As flexitarian diets gain traction and sustainability messages resonate, these once-niche products are now finding a prominent place in mainstream frozen sections. Leading the charge, brands like OmniFoods and Haofood are innovating with offerings such as dumplings, spring rolls, and protein analogs, specifically targeting younger, environmentally conscious consumers. Meanwhile, streamlined certification processes are paving the way for quicker market entries by smaller players. Retailers are increasingly allocating shelf space to plant-based proteins, underscoring the category's long-term viability. However, it is worth noting that high price premiums pose a challenge in more price-sensitive markets. In essence, the surge of plant-based frozen foods is not only diversifying the category but also broadening its appeal among urban and health-conscious consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from fresh foods | -0.8% | Southeast Asia, India, markets with robust wet-market infrastructure | Short term (≤ 2 years) |

| Limited rural market cold chain penetration | -0.6% | Rural India, Indonesia, Vietnam, Philippines, inland China | Long term (≥ 4 years) |

| Complex regulatory and labeling compliance barriers | -0.5% | ASEAN cross-border trade, fragmented national regimes | Medium term (2-4 years) |

| Sensory texture and taste acceptance concerns | -0.4% | Traditional consumer segments, older demographics across Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From Fresh Foods

In the Asia-Pacific, the frozen food market faces significant competition from fresh produce. This is particularly evident in regions where wet markets and daily shopping are deeply embedded cultural practices. Many consumers, influenced by tradition, often perceive frozen products as less flavorful and less nutritious compared to fresh alternatives, despite evidence to the contrary. For example, in India, the unorganized fresh-meat sector benefits from same-day slaughter and customization options, effectively addressing religious and regional preferences. Fresh vendors capitalize on hyper-local supply chains and competitive pricing, which becomes especially advantageous in areas lacking comprehensive cold-chain infrastructure. Consequently, frozen foods encounter challenges in penetrating markets outside metropolitan areas and among households with more flexible schedules, reinforcing the dominance of fresh produce across much of the region.

Complex Regulatory And Labeling Compliance Barriers

Regulatory complexity across Asia-Pacific markets creates compliance challenges for frozen food manufacturers, particularly for cross-border trade. Japan's implementation of positive list systems for food contact materials in June 2025 requires manufacturers to ensure that synthetic resin packaging uses only approved polymers and additives. China's updated food safety standards, including GB 2760-2024 for food additives, necessitate formulation adjustments and increased compliance costs [3]Source: USDA Foreign Agricultural Services, "China: Usage Standard for Food Additives Finalized", fas.usda.gov. These regulatory requirements, while ensuring food safety, create barriers for smaller manufacturers and complicate regional expansion strategies. South Korea's stringent labeling requirements for frozen foods mandate detailed ingredient disclosure and nutritional information in both Korean and English. The harmonization efforts between ASEAN member states through the ASEAN Food Safety Regulatory Framework aim to streamline cross-border trade but introduce additional documentation requirements. Indonesia's recent implementation of halal certification requirements for all food products, including frozen foods, adds another layer of complexity for manufacturers operating in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Dominates While Ready Meals Accelerate

Driven by the demand for single-serve ethnic-fusion bowls and restaurant-quality entrees catering to busy urban lifestyles, the frozen ready meals segment is set to grow at a 7.52% CAGR through 2031. This segment is rapidly becoming the fastest-growing in the Asia-Pacific frozen food market. While traditional categories, including frozen meat, poultry, and seafood, still hold significance, accounting for 31.10% of the market share in 2025, ready meals are increasingly capturing market share as consumers prioritize convenience and consistent quality. Frozen bakery products are gaining traction through in-store bake-off models that offer a fresh sensory appeal. Meanwhile, frozen fruits and vegetables remain staples, with organic and pre-cut formats particularly resonating with health-conscious shoppers.

Frozen dairy products, while reaching saturation in mature markets, are witnessing expansion in emerging economies. This growth is fueled by rising disposable incomes and the spread of modern retail into smaller cities. Niche categories, such as frozen desserts and novelty items, are innovating with plant-based and low-sugar formulations to align with wellness trends. Overall, the rising popularity of ready meals underscores broader lifestyle shifts, including shrinking household sizes and tighter labor markets, positioning them as the primary growth engine for the category in the coming years.

By Category: Ready-to-Cook Leads Despite Ready-to-Eat Growth

In 2025, conventional frozen foods command a dominant 94.10% share of the Asia-Pacific market, buoyed by their affordability and widespread presence in mass-market channels. For mainstream buyers, these products are the go-to choice, offering taste and convenience on par with organic alternatives, but without the premium price tag. Yet, organic frozen foods are making waves, boasting an impressive 8.96% CAGR through 2031. Starting from a niche foothold, they're gaining traction, fueled by rising disposable incomes and a heightened health consciousness. Markets like Australia, New Zealand, and urban China stand out, with consumers increasingly willing to splurge on certified organic vegetables, fruits, and plant-based proteins.

Retailers are responding to this trend, allocating more shelf space to organic frozen products. This shift is further bolstered by streamlined certification processes, making it easier for smaller producers to enter the market. While India's organic frozen segment faces hurdles, such as limited certified farmland and underdeveloped cold-chain infrastructure, pilot launches in metropolitan areas hint at untapped potential. As organic offerings surge, the market is witnessing a split: premium tiers are reaping significant value. This trend is nudging processors towards adopting dual-brand strategies and creating tiered portfolios, catering to both the cost-sensitive and the health-conscious consumer.

By Nature: Organic Scales from Niche Base

Conventional items continued to account for 94.10% of volume in 2025, reflecting affordability and established supply relationships. Bulk commodity pricing remains favorable for processors who negotiate annual contracts with agribusiness suppliers, ensuring competitive retail shelf pricing. The stability of conventional supply chains enables manufacturers to maintain consistent production schedules throughout the year. Nonetheless, sustainability commitments from multinational processors push regenerative agriculture practices into mainstream acreage, improving soil health and lowering emissions. These initiatives have gained significant traction among major agricultural producers, who are implementing soil conservation and water management techniques across their operations.

Organic lines, though niche, record a 8.96% CAGR, fueled by affluent shoppers in Japan, Singapore, and Australia who value certification logos and transparent sourcing. The Asia-Pacific frozen food market size for certified organic produce in ready blends is projected to climb as retailers allocate premium freezer space and e-commerce filters allow quick discovery. The expansion of organic product lines has been particularly notable in urban markets, where health-conscious consumers demonstrate strong brand loyalty. Story-telling on pack, highlighting non-synthetic pest controls and biodiversity benefits, cements consumer trust and justifies higher price points. Consumer education initiatives and digital marketing campaigns have successfully communicated the environmental and health benefits of organic products, driving sustained category growth.

By Distribution Channel: On-Trade Rebounds Post-Pandemic

In 2025, off-trade retail channels, spearheaded by supermarkets, hypermarkets, convenience stores, and swiftly growing online platforms, dominated frozen food sales in the Asia-Pacific region, capturing a 62.70% market share. These modern retail formats leverage strong visibility in freezer aisles, promotional pricing, and impulse buying. Meanwhile, e-commerce is propelling growth with hyperlocal fulfillment and swift delivery services in major metropolitan areas. The emergence of dark stores, coupled with integrated cold-chain logistics, is bolstering online frozen food distribution, enhancing the convenience and accessibility of at-home consumption.

Simultaneously, the on-trade foodservice channel is projected to witness a robust 8.10% CAGR through 2031. Hotels, restaurants, and quick-service chains are increasingly turning to frozen ingredients, not just for cost control and menu consistency, but also to address labor shortages. Hospitality operators are now favoring pre-portioned proteins and vegetables, streamlining kitchen operations and facilitating scalable growth. In response, suppliers are offering dedicated foodservice SKUs and just-in-time delivery. This shift towards a more professional and efficiency-centric procurement approach is poised to bolster the on-trade channel, even as off-trade retail remains dominant.

Geography Analysis

In 2025, China is set to dominate the Asia-Pacific market with a commanding 31.05% share. This dominance is bolstered by a robust cold-chain infrastructure, government-backed subsidies, and a surge in e-commerce platforms that promise same-day frozen deliveries in major cities. While community-group-buying models are making frozen foods accessible in smaller urban centers, Japan and South Korea, already deeply entrenched in the market, are pivoting towards premium single-serve formats, catering to their aging demographics. Meanwhile, Australia and New Zealand have carved out a niche as export powerhouses, delivering grass-fed meats and organic berries. These products, prized for their traceability, fetch premium prices in markets like China and Singapore.

India is on track to become the fastest-growing market, boasting an impressive 8.12% CAGR through 2031. This growth is fueled by initiatives to expand cold-chain infrastructure and the swift rise of online grocery platforms that promise ultra-fast frozen deliveries in metropolitan areas. Modern retail chains are increasingly allocating space to frozen food aisles. At the same time, Southeast Asian nations, including Indonesia, Thailand, Vietnam, and the Philippines, are witnessing robust growth as hypermarkets extend their reach beyond just capital cities. Singapore and Malaysia are emerging as hotbeds for innovation in premium frozen products. However, smaller markets in South Asia are lagging, grappling with infrastructure challenges and a cultural inclination towards fresh foods.

The Asia-Pacific frozen food landscape is a tapestry of mature markets, burgeoning growth, and untapped potential. With China and India leading the charge through infrastructural advancements and retail evolution, Japan and South Korea are honing in on premium convenience. Southeast Asia is reaping the rewards of a modern trade expansion, while Australia and New Zealand bolster the region's export strength. Yet, it's the smaller South Asian markets that hold promise, poised for growth as urbanization and retail development take root.

Competitive Landscape

In 2025, China is set to dominate the Asia-Pacific market with a commanding 31.05% share. This dominance is bolstered by a robust cold-chain infrastructure, government-backed subsidies, and a surge in e-commerce platforms that promise same-day frozen deliveries in major cities. While community-group-buying models are making frozen foods accessible in smaller urban centers, Japan and South Korea, already deeply entrenched in the market, are pivoting towards premium single-serve formats, catering to their aging demographics. Meanwhile, Australia and New Zealand have carved out a niche as export powerhouses, delivering grass-fed meats and organic berries. These products, prized for their traceability, fetch premium prices in markets like China and Singapore.

India is on track to become the fastest-growing market, boasting an impressive 8.12% CAGR through 2031. This growth is fueled by initiatives to expand cold-chain infrastructure and the swift rise of online grocery platforms that promise ultra-fast frozen deliveries in metropolitan areas. Modern retail chains are increasingly allocating space to frozen food aisles. At the same time, Southeast Asian nations, including Indonesia, Thailand, Vietnam, and the Philippines, are witnessing robust growth as hypermarkets extend their reach beyond just capital cities. Singapore and Malaysia are emerging as hotbeds for innovation in premium frozen products. However, smaller markets in South Asia are lagging, grappling with infrastructure challenges and a cultural inclination towards fresh foods.

The Asia-Pacific frozen food landscape is a tapestry of mature markets, burgeoning growth, and untapped potential. With China and India leading the charge through infrastructural advancements and retail evolution, Japan and South Korea are honing in on premium convenience. Southeast Asia is reaping the rewards of a modern trade expansion, while Australia and New Zealand bolster the region's export strength. Yet, it's the smaller South Asian markets that hold promise, poised for growth as urbanization and retail development take root.

Asia-Pacific Frozen Food Industry Leaders

-

McCain Foods Limited

-

Ajinomoto Co., Inc.

-

General Mills Inc.

-

Conagra Brands, Inc.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Europastry, a Spanish manufacturer specializing in frozen bakery products, bolstered its foothold in the Asia-Pacific by securing a 60% majority stake in Thailand's Art of Baking. Art of Baking, known for its ready-to-eat (RTE) and frozen bakery offerings, boasts four primary product lines: sweet pastries (including croissants, puff pastries, and Danish dough), savoury pastries, flatbreads, and pizza bases, alongside a variety of other items.

- July 2025: Happy Monk unveiled India's premium packaged frozen dim sum brand, catering to the modern consumer's demand for convenience, authenticity, and quality in home dining. The brand's new lineup boasts over 20 handcrafted dumpling varieties, including unique offerings like Edamame Truffle, Smoked Chicken with Cheddar Cheese, and Sriracha Chicken, cementing its status as a trailblazer in the gourmet frozen food arena.

- June 2025: Iceland Foods, in partnership with BTG WeLink, launched its first Asia-Pacific store in Beijing, China. Branded as 'Iceland Lab', the store features a curated selection of innovative and cost-effective frozen products. This strategic collaboration enhances Iceland's global market presence while introducing its distinctive frozen product portfolio to Chinese consumers. From late June, over 100 of Iceland's frozen products became accessible to shoppers in China through multiple e-commerce platforms.

- January 2025: Ferrero launched its frozen bakery line in Australia, introducing the Nutella Croissant and Nutella Muffin to its food service partners. To ensure freshness, Ferrero froze its Nutella Bakery Range. The Nutella Muffin can be enjoyed just two hours after being left at room temperature, while the Nutella Croissant is prepped by freezing it immediately after rising, allowing it to be baked directly from the freezer.

Asia-Pacific Frozen Food Market Report Scope

Frozen food is defined as food products that are preserved under low temperatures and used over a long period. The Asia-Pacific frozen food market is segmented by product type, category, nature, distribution channel, and geography. By product type, the market is segmented intofrozen meat, poultry, and seafood, frozen bakery and confectionery, frozen fruits and vegetables, frozen ready meals, frozen dairy products, and other types. By category, the market is segmented into ready-to-eat and ready-to-cook. By nature, the market is segmented into conventional and organic. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into China, Japan, India, South Korea, Australia, New Zealand, Thailand, Singapore, and rest of Asia-Pacific. The market forecasts are provided in terms of value (USD).

By Product Type

| Frozen Meat, Poultry and Seafood |

| Frozen Bakery and Confectionery |

| Frozen Fruits and Vegetables |

| Frozen Ready Meals |

| Frozen Dairy Products |

| Other Types |

By Category

| Ready-to-Eat (RTE) |

| Ready-to-Cook (RTC) |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| HoReCa/On-Trade | |

| Retail/Off-Trade | Supermarkets/ Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| China |

| India |

| Japan |

| Australia |

| New Zealand |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Frozen Meat, Poultry and Seafood | |

| Frozen Bakery and Confectionery | ||

| Frozen Fruits and Vegetables | ||

| Frozen Ready Meals | ||

| Frozen Dairy Products | ||

| Other Types | ||

| By Category | Ready-to-Eat (RTE) | |

| Ready-to-Cook (RTC) | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | HoReCa/On-Trade | |

| Retail/Off-Trade | Supermarkets/ Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the forecast value of the Asia-Pacific frozen food market by 2031?

It is projected to reach USD 123.18 billion, reflecting a 7.48% CAGR over 2026-2031.

Which product category currently leads sales?

Frozen meat, poultry, and seafood held 31.10% share of sales in 2025.

Which country will record the fastest demand increase?

India is expected to advance at an 8.12% CAGR through 2031.

How fast are ready-to-eat frozen foods growing?

This segment is expanding at a 7.55% CAGR as urban lifestyles favor quick-serve options.

Page last updated on: