Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

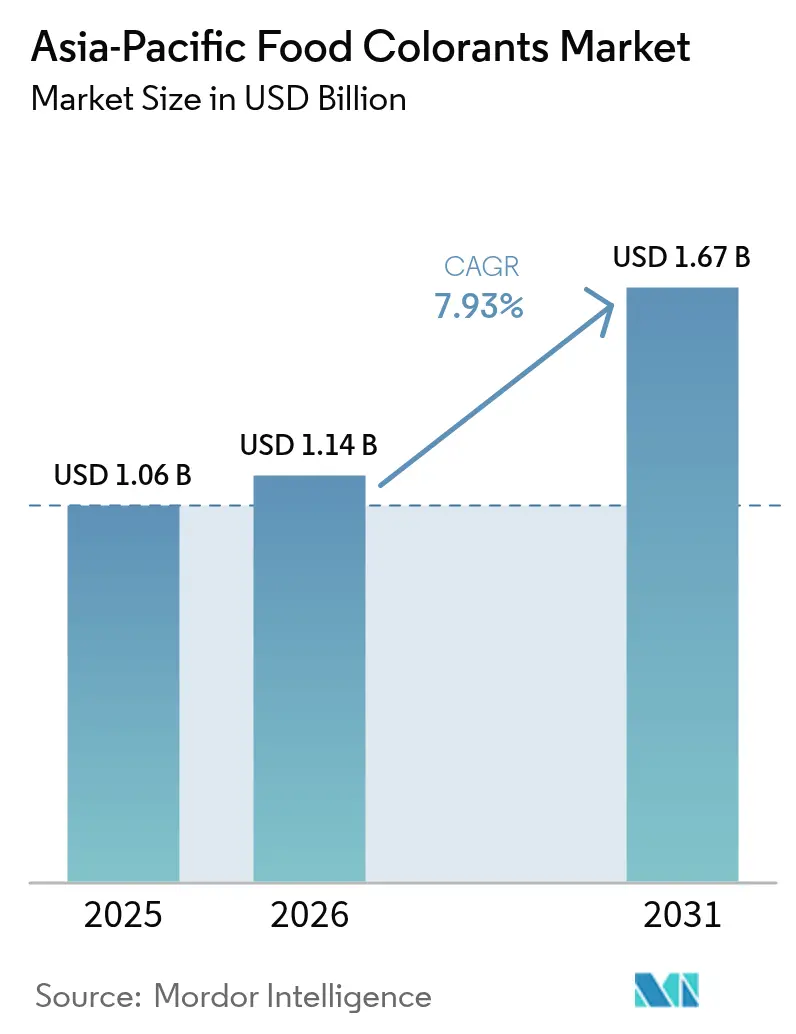

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

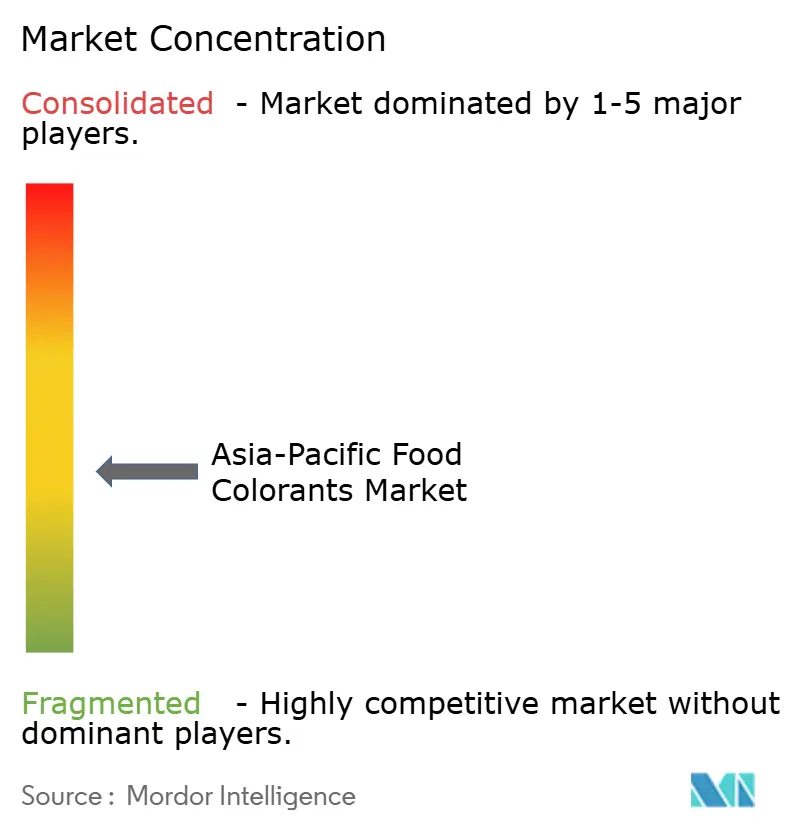

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Food Colorants Market Analysis by Mordor Intelligence

Asia-Pacific food colorants market size in 2026 is estimated at USD 1.14 billion, growing from 2025 value of USD 1.06 billion with 2031 projections showing USD 1.67 billion, growing at 7.93% CAGR over 2026-2031. The market is experiencing significant growth due to increasing consumer demand for natural and organic food products, particularly in China and India's expanding food processing industries. While the beverage and confectionery sectors drive demand for colorants, the regulatory landscape across Asia-Pacific influences market dynamics through varying standards and maximum permissible limits for synthetic colors. Health concerns, including studies linking synthetic colorants to hyperactivity in children, have prompted manufacturers to shift toward natural alternatives, despite challenges related to higher costs and stability. This transition aligns with growing consumer preference for clean-label products, although manufacturers must navigate different regulatory requirements across regional markets. As the industry continues to evolve, the successful adaptation to natural alternatives and compliance with regional regulations will be crucial for manufacturers to maintain their market position and meet consumer expectations.

Key Report Takeaways

- By product type, natural colors led with 52.15% revenue share in 2025, whereas the same category is projected to expand at a 9.02% CAGR through 2031.

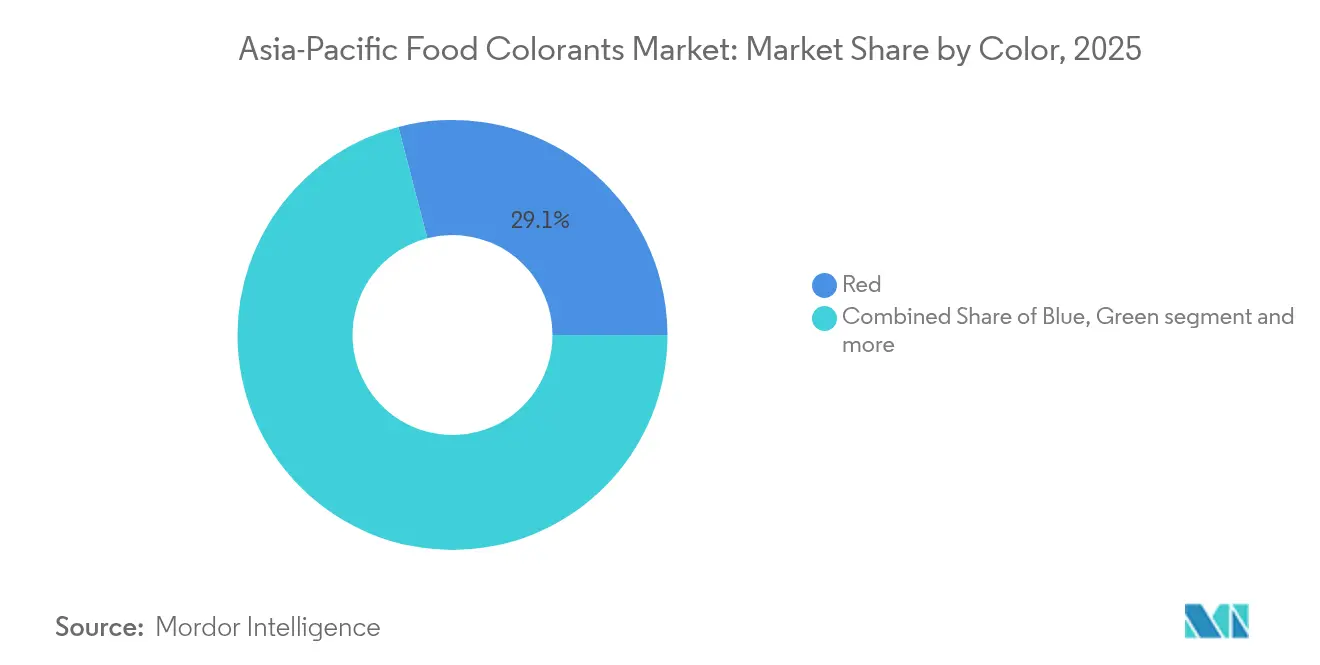

- By color, red accounted for 29.05% of the Asia-Pacific food colorant market share in 2025, while blue is forecast to grow at a 9.48% CAGR between 2026-2031.

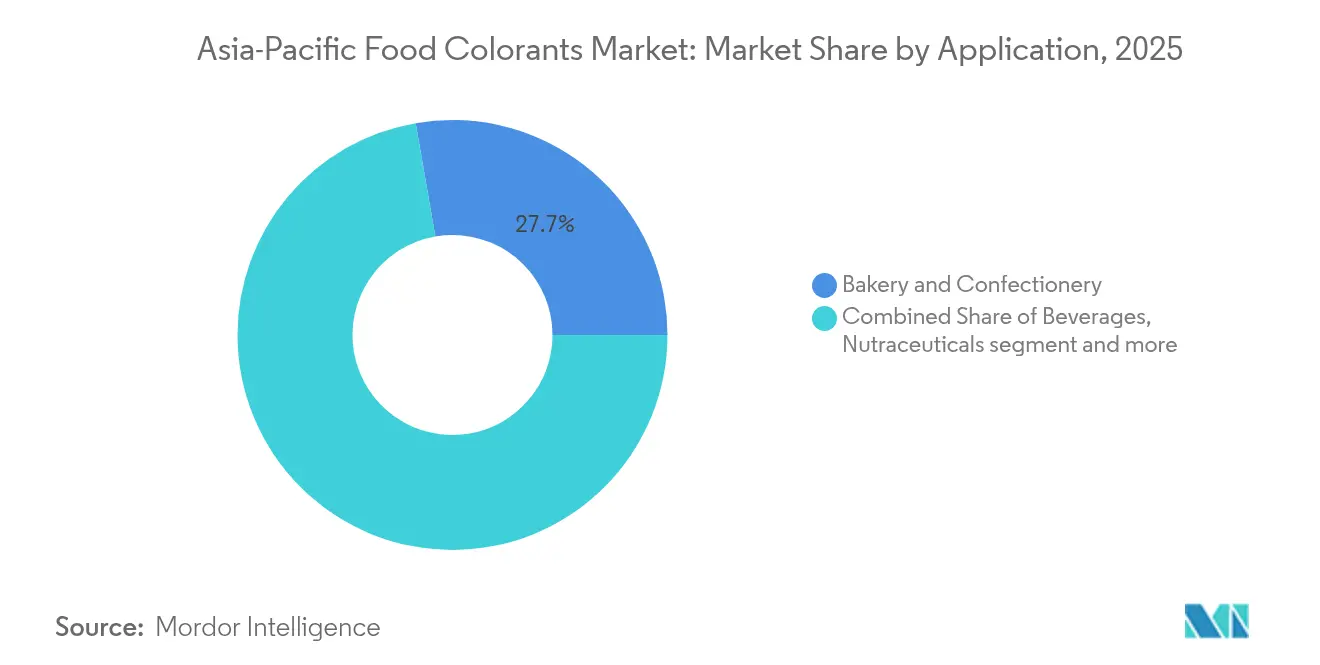

- By application, bakery and confectionery captured 27.74% of the Asia-Pacific food colorant market size in 2025; nutraceuticals register the fastest 8.41% CAGR during the forecast period.

- By form, powder held 63.72% of the Asia-Pacific food colorant market size in 2025, whereas liquid forms are advancing at a 6.74% CAGR to 2031.

- By geography, China dominated with a 40.62% share in 2025; India is set to record the highest 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Food Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of processed food industry | +2.5% | China, India, SE Asia | Long term (≥ 4 years) |

| Growing influence of Western dietary pattern | +0.8% | Urban APAC, Japan, Australia | Medium term (2-4 years) |

| Increasing demand in bakery and confectionery industries | +1.6% | Japan, India, Australia | Long term (≥ 4 years) |

| Investments in research and development for innovative color solutions | +1.2% | China, India | Long term (≥ 4 years) |

| Rising demand for visually appealing food products | +1.0% | Urban APAC, China, South Korea | Medium term (2-4 years) |

| Changing consumer preferences toward convenience foods | +0.7% | India, China, SE Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Processed Food Industry Leading Regional Manufacturing Boom

The expansion of the processed food industry across Asia-Pacific is driving significant growth in the food colorant market, fueled by increasing urbanization, rising disposable incomes, and changing consumer preferences toward convenience foods. Manufacturers require stable and vibrant colorants capable of withstanding various processing conditions, particularly in countries like China, India, and Indonesia, where significant investments in food processing facilities and technological advancements are occurring. China exemplifies this trend, with its food processing industry experiencing substantial growth, supported by government initiatives focused on modernizing the agricultural sector and food supply chain. However, according to UNCTAD-WHO analysis published in March 2024, developed economies in Asia, including the Republic of Korea and Singapore, maintain processed foods at 40% or less of their total food imports[1]Source: UNCTAD, “New UNCTAD-WHO analysis reveals trends in processed foods trade,” unctad.org. This diverse landscape of processed food consumption and regulatory frameworks across Asia-Pacific continues to shape the trajectory of the food colorant market, creating opportunities for innovation and market expansion.

Growing Influence of Western Dietary Pattern

The increasing adoption of Western dietary patterns across the Asia-Pacific region has transformed the food colorants market, driven by the growing middle-class population and their changing food preferences. This shift is particularly evident in the rising consumption of packaged foods, beverages, confectionery, and bakery products. Consumers, especially in urban areas with higher disposable incomes, expect food products to match the visual characteristics of Western counterparts. The expansion of international fast-food chains, cafes, and modern retail formats has improved access to Western-style food products, while social media and international travel have increased consumer awareness of global food trends. Local and international food manufacturers are expanding their production capacities to meet this growing demand, particularly in emerging economies. According to the World Migration Report, Europeans comprise the largest group of migrants from outside Asia in the region, including migrants from the European part of the former Soviet Union now living in Central Asia, further influencing these dietary preferences[2]Source: International Organization for Migration, “World Migration Report 2024 – Asia,” worldmigrationreport.iom.int. This trend is expected to continue as urbanization increases and Western food products become more integrated into local food cultures.

Increasing Demand of Colorant in Bakery and Confectionery Industries

The rising consumer preference for visually appealing bakery and confectionery products is driving significant growth in food colorant usage across the Asia-Pacific region. Manufacturers are focusing on premium product positioning through visual differentiation, incorporating various natural and synthetic food colorants. In Japan, where food aesthetics hold cultural importance, consumers demonstrate higher willingness to pay premium prices for visually appealing products. Countries like China, Japan, South Korea, and India are experiencing increased consumption of cakes, pastries, and candies, particularly among the younger population. This trend is evident in India, where a November 2023 Local Circles survey revealed that most respondents consume sweet confectioneries at least one to two times a month, with 7% consuming them daily. The expansion of bakery chains and confectionery manufacturers in the region has intensified the demand for food colorants, further amplified during festival seasons and by the growing trend of customized cakes and designer confectionery products. Manufacturers are developing compliant colorant solutions to meet consumer expectations for visual appeal while adhering to regulatory requirements.

Investments in Research and Development to Create Innovative and Stable Food Coloring Solutions

Investments in research and development are driving the growth of the Asia-Pacific food colorants market. Major companies are establishing specialized facilities and expanding their research capabilities across the region. Chr. Hansen's Application and Technology Center in Singapore and Sensient Technologies' expanded facilities in China and Japan demonstrate this commitment to innovation. The research focuses primarily on developing stable, natural, and clean-label food colorants that maintain their properties during processing and storage. Companies are also improving existing colorants by enhancing heat resistance and creating application-specific solutions for beverages, confectionery, and processed foods. These research and development initiatives respond to the growing consumer preference for natural ingredients and clean-label products in the Asia-Pacific region. The continuous investment in research and development is expected to result in more innovative and sustainable food coloring solutions in the coming years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns limiting market growth of food colorant | −1.8% | India, South Korea, Australia | Long term (≥ 4 years) |

| Industry compliance impacts market development | −0.9% | All APAC | Medium term (2-4 years) |

| Strict regulations regarding the use of synthetic food colors | −1.5% | Australia, India, Japan | Long term (≥ 4 years) |

| Price volatility of raw materials used in natural food colorants | −0.7% | India, China, ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Limiting Market Growth of Food Colorant

The increasing awareness of health issues associated with synthetic food colorants in the Asia-Pacific region poses significant challenges to market growth. Several studies have linked artificial food colors to behavioral problems in children, allergic reactions, and potential carcinogenic effects. Countries like Japan and South Korea have implemented strict regulations on synthetic food colors, particularly those derived from petroleum-based sources. Consumer advocacy groups in major markets, including China and India, are pushing for clearer labeling requirements and restrictions on artificial colorants in food products. The growing preference for clean-label products and natural ingredients has led many food manufacturers to reformulate their products, moving away from synthetic colorants. Additionally, media coverage highlighting the potential risks of artificial food colors has influenced consumer purchasing decisions, particularly among urban populations and parents of young children. These factors collectively create barriers for synthetic food colorant manufacturers and impact overall market expansion in the region.

Industry Compliance Impacts Market Development

The diverse regulatory requirements across the Asia-Pacific region pose significant challenges for food colorant manufacturers. Each country maintains distinct standards and approval processes, particularly in the ASEAN region where harmonization of food safety standards remains incomplete. While the ASEAN Principles and Guidelines for the Establishment of Maximum Use Level for Food Additives provides a framework for standardization based on JECFA safety assessments, substantial variations persist in permitted colorants and their maximum usage levels across different countries. These regulatory inconsistencies increase compliance costs and necessitate investments in quality control measures, limiting market entry for smaller manufacturers and creating complexity in product formulation. Furthermore, the push toward natural food colors, driven by both regulatory preferences and consumer demand, requires manufacturers to adapt their production processes and supply chains accordingly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Color: Blue Innovations Driving Growth

Red dominates the color segment with a 29.05% market share in 2025, establishing its position as the primary choice in the market. This dominance reflects the color's widespread acceptance across various food and beverage applications, particularly in products requiring warm, appetizing hues. However, blue is emerging as the fastest-growing color segment, projected to grow at a CAGR of 9.48% during 2026-2031. This growth pattern highlights a significant shift in market dynamics, where traditional preferences meet evolving consumer demands. The shift is particularly evident in regions with high social media penetration and younger consumer demographics.

The expansion of the blue segment is particularly significant given the historical challenges in sourcing natural blue colorants. This scarcity has historically limited product development options for manufacturers seeking natural alternatives. Manufacturers are addressing this through innovations in extracting and stabilizing blue pigments from natural sources such as butterfly pea flower (Clitoria ternatea) and spirulina. The trend is further supported by increasing consumer preference for clean-label products and natural ingredients, pushing manufacturers to invest more in natural blue colorant research and development.

By Product Type: Natural Colors Outpace Synthetics

Natural colors command a dominant 52.15% share of the Asia-Pacific food colorant market in 2025, with projections indicating a robust CAGR of 9.02% from 2026-2031. This market leadership stems from increasing health consciousness and stricter regulations against synthetic alternatives, particularly evident in markets like Japan and Australia, where consumer awareness and regulatory frameworks favor natural options. While synthetic colors continue to maintain their presence due to their cost-effectiveness and stability, the trend is further supported by technological advancements in extraction and stabilization techniques, with microencapsulation technology improving the performance of natural colorants in complex food applications.

The transition toward natural colorants has created significant agricultural opportunities across the Asia-Pacific region. India, in particular, has expanded its cultivation of color-rich crops such as turmeric and beetroot to meet the growing market demand. According to the Ministry of Agriculture and Farmers Welfare, during fiscal year 2023, the volume of turmeric production in India accounted for 1.23 million metric tons, which was 0.86 million metric tons in 2018 . This agricultural expansion, coupled with improved processing capabilities, is strengthening the natural colorant supply chain and supporting the market's continued growth trajectory.

By Application: Nutraceuticals Emerge as Growth Leader

The bakery and confectionery segment maintains its dominant market share of 27.74% in 2025, while the nutraceuticals segment demonstrates the highest growth rate of 8.41% during the forecast period. This shift reflects the evolving consumer preferences in Asia-Pacific, where the food and pharmaceutical industries increasingly overlap. The regulatory landscape for colorants in nutraceuticals varies across the region, with countries like India implementing structured frameworks through organizations such as the Food Safety and Standards Authority (FSSAI).

The nutraceutical segment's growth has spurred demand for colorants that deliver both aesthetic appeal and functional benefits. Natural colorants, particularly anthocyanins from berries and curcumin from turmeric, have gained significant traction due to their dual role as visual enhancers and antioxidant providers. These developments align with the broader trend of consumers seeking nutritional benefits from their food choices, while manufacturers work within established regulatory guidelines to ensure product safety and innovation.

By Form: Powder Dominates, Liquid Accelerates

Powder forms maintain a dominant position with a market share of 63.72% due to their inherent advantages of stability, ease of storage, and longer shelf life. These characteristics make powder colorants particularly effective for applications in dry mixes and processed foods where extended shelf life is crucial. The regulatory environment, exemplified by Indonesia's Regulation of the Minister of Health No. 033 Year 2012 on Food Additives, provides clear guidelines for both powder and liquid colorants, establishing a framework that balances innovation with consumer safety.

Liquid colorants are gaining momentum in the market, demonstrating a robust growth rate of 6.74% CAGR from 2026-2031. This growth is primarily attributed to their manufacturing efficiency and superior color distribution capabilities in specific applications. The regulatory specifications for both forms address purity standards and permitted use levels, requiring manufacturers to comply with established safety protocols while developing their product offerings. The increasing adoption of liquid colorants across various food and beverage applications indicates a shift in manufacturer preferences, particularly in products requiring precise color consistency.

Geography Analysis

China dominates the Asia-Pacific food colorant market with a significant market share of 40.62% in 2025, driven by its massive food processing industry and rapidly evolving consumer preferences. The country's regulatory framework, governed by the GB 2760-2011 Food Safety National Standard, creates a structured environment for colorant innovation while ensuring consumer safety. This standard specifies over 180 approved food additives, including colorants, and uses a positive list approach that clearly defines permitted substances and their maximum use levels. The market is experiencing a shift toward natural colorants, with domestic manufacturers investing in research and development to meet growing demand.

India is positioned as the fastest-growing market in the region with a projected CAGR of 9.22% from 2026-2031, driven by its expanding food processing sector and increasing consumer awareness of food ingredients. The regulatory environment, overseen by the Food Safety and Standards Authority of India (FSSAI), permits eight synthetic colors while encouraging the development and use of natural alternatives. The country's rich agricultural heritage provides abundant sources for natural colorants, with turmeric, saffron, and beetroot being traditional sources that are now finding commercial applications. The growth is particularly pronounced in the bakery, confectionery, and beverage segments, where colorants play a crucial role in product differentiation and consumer appeal.

Japan and Australia represent mature markets with sophisticated regulatory frameworks and consumers who prioritize natural and clean-label products. In Japan, the cultural significance of food aesthetics drives demand for high-quality colorants that can deliver precise visual outcomes. The country's regulatory approach includes a unique list of permitted colors with specific restrictions, creating a structured environment for innovation. Australia's food colorant market is influenced by its alignment with European regulatory approaches, with Food Standards Australia New Zealand (FSANZ) conducting thorough safety assessments before approving colorants for use. Both countries are seeing growing demand for natural colorants, with manufacturers investing in research to overcome technical limitations related to stability and color intensity.

Regulatory Landscape

Food colorant use across Asia-Pacific is shaped by additive positive lists, maximum use levels, and labeling rules that vary by country, which affects market access and reformulation planning. China is anchored by the GB 2760 framework (updated to GB 2760-2024, implemented in February 2025), while Japan uses a positive list under its Food Sanitation Act, permitting only designated additives for use. In Australia and New Zealand, Food Standards Australia New Zealand (FSANZ) administers the Food Standards Code and issued Amendment No. 250 in June 2026, reinforcing the need for suppliers to monitor schedule changes that affect permitted additives and conditions of use.

Across Southeast Asia, Codex Alimentarius and JECFA safety assessments act as reference points, but harmonization remains incomplete. ASEAN provides regional guidance through the ASEAN Principles and Guidelines for establishing maximum use levels for food additives and published updated ASEAN maximum use levels in April 2026, while individual member states still implement national requirements that can differ by permitted colors and limits. Singapore regulates additives under the Sale of Food Act through its Food Regulations, requiring safety assessment and inclusion in the permitted list before use, a relevant constraint for newer production routes such as fermentation-derived ingredients.

Value Chain Analysis

The value chain starts with feedstocks and intermediates, then moves into extraction or synthesis, formulation and blending, application support, and distribution to food and beverage manufacturers. Natural colorants depend on agricultural inputs (for example, turmeric, beetroot, spirulina, and butterfly pea), followed by extraction, standardization, and stabilization. Synthetic colors rely more on chemical precursors and integrated chemical infrastructure. Suppliers then convert pigments into application-ready powders and liquids, supported by quality testing against country-specific standards, before reaching end users in bakery and confectionery, beverages, dairy, snacks, and nutraceuticals.

Within Asia-Pacific, manufacturing and sourcing footprints vary substantially, with a concentration of synthetic production capacity in China and broader import reliance in Japan, South Korea, and parts of Southeast Asia. This creates lead-time and compliance-documentation requirements for cross-border shipments. Formulators and global ingredient companies differentiate through localized application labs and R&D networks (for example, Sensient highlights a multi-site APAC footprint of R&D centers and manufacturing plants), helping them adapt more quickly to local regulations, processing conditions, and clean-label specifications. Distribution partners and regional blenders also influence execution through last-mile regulatory steps such as labels, permitted-use checks, and documentation, especially where ASEAN harmonization does not fully remove national differences in additive lists and maximum use levels.

Competitive Landscape

The Asia-Pacific food colorant market demonstrates a moderately fragmented competitive landscape, characterized by the presence of global companies like Chr. Hansen Holding A/S, Sensient Technologies Corporation, and Givaudan SA alongside regional specialists such as Roha Dyechem and Synthite Industries. Companies are strategically focusing on natural colorant portfolios and investing in proprietary extraction and stabilization technologies to differentiate their offerings. The competitive dynamics are influenced by regulatory expertise, as successful players must navigate the complex and varied regulatory landscape across the region.

Global players are expanding their presence in the region through strategic acquisitions of regional companies. For instance, Oterra acquired India's Akay Group in 2022, subsequently establishing a new color blending facility in Kerala, India in February 2025. This facility serves the Indian, Asia-Pacific, and Middle East markets, demonstrating the importance of local manufacturing capabilities in competitive positioning. These strategic moves enable global companies to strengthen their market presence while benefiting from established local networks and expertise.

The market presents opportunities in developing stable, cost-effective natural blue colorants, which remain technically challenging despite increasing demand. Regional players like San-Ei Gen F.F.I. in Japan are effectively competing with global companies by leveraging their understanding of local market preferences and regulatory requirements, particularly in specialized applications such as confectionery and traditional foods. Technology serves as a key differentiator, exemplified by Chr. Hansen's investments in fermentation technology to produce natural colors with enhanced stability and performance characteristics.

Asia-Pacific Food Colorants Industry Leaders

Sensient Technologies Corporation

Döhler

Kalsec Inc

Givaudan S.A.

Chr. Hansen Holding A/S

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The shift from synthetic to natural colorants remains a key opening across applications where stability and shade matching are technically difficult, especially for blues and for demanding matrices such as beverages and nutraceutical formats. Natural colors already led the region in 2025 with a 52.15% revenue share, and supplier investments indicate active reformulation work among manufacturers. Sensient announced a USD 250 million investment in April 2026 to expand natural color production capacity, and Oterra expanded production capacity in India in November 2024 to shorten lead times and increase localization for APAC. Together, these steps support demand from regional buyers looking for plant-based colors with more secure supply and consistent performance across processing conditions.

Regulatory updates are also generating near-term formulation and compliance work that rewards suppliers with strong documentation and local technical support. China implemented GB 2760-2024 in February 2025, and ASEAN published updated maximum use levels in April 2026, which raises the value of portfolios engineered to meet differing national limits and labeling practices without repeated reformulation. Channel partnerships provide another route to capture fragmented demand, illustrated by GNT's January 2026 distribution partnership for EXBERRY plant-based colorings in Indonesia. In parallel, inorganic pigment capacity additions in India (including Ultramarine and Pigments approving a USD 30 million greenfield project in Tamil Nadu in May 2026) point to continued activity in broader colorant supply ecosystems that can affect availability, procurement strategies, and technical know-how across color categories.

Recent Industry Developments

- June 2026: Food Standards Australia New Zealand (FSANZ) published Amendment No. 250 to the Food Standards Code, updating parts of the schedules that govern permitted additives and conditions of use. The change reinforces the need for colorant suppliers and food manufacturers selling into Australia and New Zealand to maintain ongoing compliance monitoring and rapid label and specification updates.

- February 2025: China implemented GB 2760-2024, the National Food Safety Standard for the use of food additives, updating the baseline rulebook that governs permitted substances and usage conditions. The implementation tightens the importance of China-specific formulations, documentation, and supplier quality systems for products distributed across multiple APAC markets.

- July 2024: GNT expanded its EXBERRY natural colors roadmap by moving into fermentation technology as a new production approach alongside plant-based sourcing. The step broadens the technology toolkit for improving stability and sustainability attributes, which are key adoption barriers for natural colors in beverages and confectionery applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers food grade colorants sold into food and beverage manufacturing across Asia-Pacific, measured as the value of colorant ingredients used to create or restore color in finished products.

Scope exclusions: It excludes non-food uses (such as cosmetics or pharma), lab-only dyes, and the value of finished foods that only contain colorants as a minor input.

Segmentation Overview

- By Product Type

- Natural Color

- Synthetic Color

- By Color

- Blue

- Red

- Green

- Yellow

- Others

- By Application

- Bakery and Confectionery

- Dairy-based Products

- Beverages

- Alcoholic Beverages

- Non-alcoholic Beverages

- Nutraceuticals

- Snacks and Cereals

- Other Applications

- By Form

- Powder

- Liquid

- By Country

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for the model and to anchor country demand drivers that influence ingredient consumption. We referenced public sources such as national food safety regulators in the region, FAO statistics, UN Comtrade trade flows, World Bank macro indicators, and customs or tariff schedules that clarify ingredient categories and reporting lines.

We also reviewed company annual reports, investor decks, and credible press to understand capacity additions, sourcing shifts toward natural colors, and application momentum in beverages, bakery, and dairy. For hard-to-find context, paid subscriptions were used only for items like company financials, patent activity around color sources and extraction, and import export shipment-level signals on ingredient movement. The desk sources listed here are illustrative and not exhaustive, and many other public references were used for cross-checking and clarification.

Primary Interviews and Surveys

Primary work focused on verifying how demand is actually formed and priced in each major APAC market, including China, Japan, India, Australia, and the Rest of Asia-Pacific. We spoke with a mix of ingredient suppliers, distributors, and end users in food and beverage manufacturing so that assumptions on application shares, natural versus synthetic mix, and typical price bands could be corrected when needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | |

| Mid tier: 60% | Functional/Unit leaders: 32% | |

| Smaller Players: 14% | Managers: 54% |

Market-Sizing & Forecasting

The sizing starts with a top-down build that reconstructs the demand pool by linking food and beverage output and trade indicators to the likely intensity of colorant usage by application. After that structure is set, the totals are corroborated through selective bottom-up checks using sampled price per kilogram ranges and volume approximations by form (powder versus liquid), followed by channel feedback on what is actually being purchased.

Key inputs used in the model include the natural versus synthetic mix shift, changes in processed food and beverage production, country-level import dependency for colorant ingredients, application weightings across bakery and confectionery, dairy-based products, and beverages, and typical ASP movement tied to raw material availability. Where inputs were missing for smaller countries, proxy ratios were used based on similar consumption profiles and then refined through distributor and manufacturer feedback. For forecasting, scenario analysis was used, and the base case was chosen after aligning expert expectations on regulatory tightening, clean-label adoption, and regional manufacturing expansion that tends to influence ingredient demand over time.

Data Validation & Update Cycle

Outputs are validated through several passes, where checks are run against independent signals such as trade direction, food processing growth, and reported ingredient price ranges in key markets. If an assumption creates an unusual jump in a country series or an application share, it is flagged, reviewed by another analyst, and then re-tested with a different data cut before sign-off.

Reports are refreshed annually, and interim updates are made when material events occur (such as regulatory actions, supply disruptions, or major capacity changes). Before delivery, we run a fresh review pass so the final numbers reflect the most recent public data and any new confirmations received during follow-ups.

Mordor Intelligence's Asia Pacific Food Colorants Market Market Estimate Compared With Other Published Estimates

Published market sizes for APAC food colorants can look far apart, even when the topic sounds identical, because each publisher uses its own boundaries and data anchors. Differences usually come from what is counted as a colorant, which year is treated as the base, and how pricing and mix shifts are handled across countries.

Key gaps also show up when one estimate leans heavily on broad ingredient spend assumptions without checking them against trade flows, application demand, and realistic price bands. Currency conversion timing, whether coloring foodstuffs are grouped with additives, and how fast natural color adoption is assumed to rise can all move the total in a noticeable way.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.06 B (2025) | |

| Industry Data Publisher A | USD 1.10 B (2025) | Uses a close APAC definition but provides limited clarity on how natural versus synthetic mix changes are priced through the forecast, which can slightly shift the base-year total by country. |

| Global Consultancy B | USD 5.80 B (2023) | Appears to use a broader boundary that can group coloring foodstuffs and adjacent additive spend into the same bucket, and the older base year also amplifies differences after currency and inflation adjustments. |

Import export trade direction, food and beverage output growth, and interview-verified price bands are the evidence checks that keep Mordor Intelligence's estimate tied to the colorant ingredient demand pool, instead of drifting into wider additive spend. Looking across the table, the tighter spread comes from similar year and scope choices, and the larger number is best explained by broader inclusions plus a different base year, which makes like-for-like comparison harder.

Key Questions Answered in the Report

What is the current value of the Asia-Pacific food colorant market?

The market stands at USD 1.14 billion in 2026 and is projected to reach USD 1.67 billion by 2031, reflecting an 7.93% CAGR.

Which product type leads the Asia-Pacific food colorant market?

Natural colors lead with 52.15% share in 2025 and show the strongest growth momentum.

Why is blue pigment demand rising in Asia Pacific?

Social-media driven beverage trends and technological advances in spirulina and butterfly-pea extraction support a 9.48% CAGR for blue pigments.

What segment is the fastest-growing application for colorants?

Nutraceuticals, including functional gummies and effervescent tablets, are set to grow at 8.41% CAGR as consumers seek products that combine health benefits with appealing colors.

Which geography records the highest growth rate?

India is forecast to expand at a 9.22% CAGR due to a modernizing food-processing sector and abundant botanical resources suitable for natural color extraction.

Page last updated on: