Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.70 Trillion |

| Market Size (2026) | USD 1.81 Trillion |

| Market Size (2031) | USD 2.46 Trillion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific ETF Market Analysis by Mordor Intelligence

The Asia-Pacific ETF market size is expected to grow from USD 1.70 trillion in 2025 to USD 1.81 trillion in 2026 and is forecast to reach USD 2.46 trillion by 2031 at 6.37% CAGR over 2026-2031. Strong retail inflows via mobile trading apps, growing acceptance of fixed-income ETFs for balance-sheet liquidity, and tax-advantaged savings reforms are steering this expansion. Japan remains the largest single market, yet surging volumes in China, India, and South Korea signal a wider regional rebalancing. Issuers are racing to launch active, thematic, and ESG funds to capture millennial demand, while digital platforms are compressing fees and accelerating distribution. Cross-border schemes such as ETF Connect are breaking down legacy barriers and setting the stage for a more integrated Asia-Pacific ETF market.

Key Report Takeaways

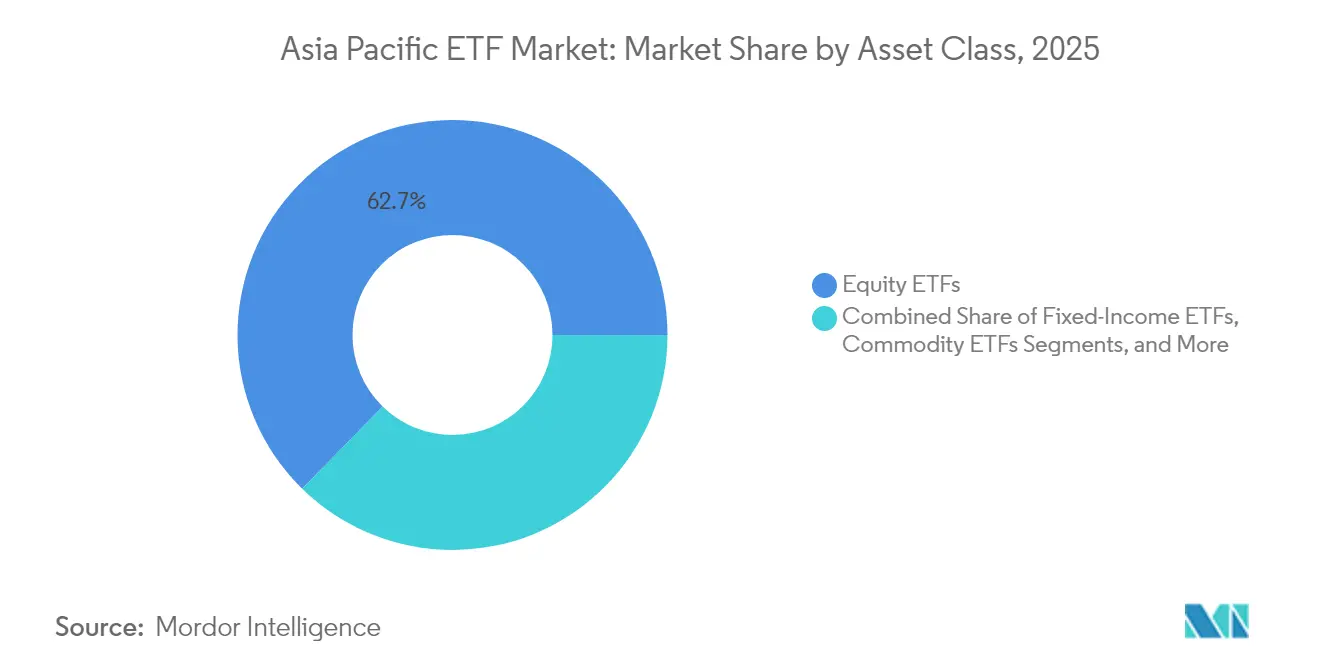

- By asset class, equity ETFs led with 62.68% of Asia-Pacific ETF market share in 2025; alternative ETFs are projected to grow at a 9.34% CAGR to 2031.

- By investment strategy, passive vehicles held 81.12% of the Asia-Pacific ETF market share in 2025, whereas active ETFs are forecasted to expand at a 12.03% CAGR through 2031.

- By investor type, retail investors accounted for 61.72% of the Asia-Pacific ETF market size in 2025 and are expected to grow at an 8.41% CAGR.

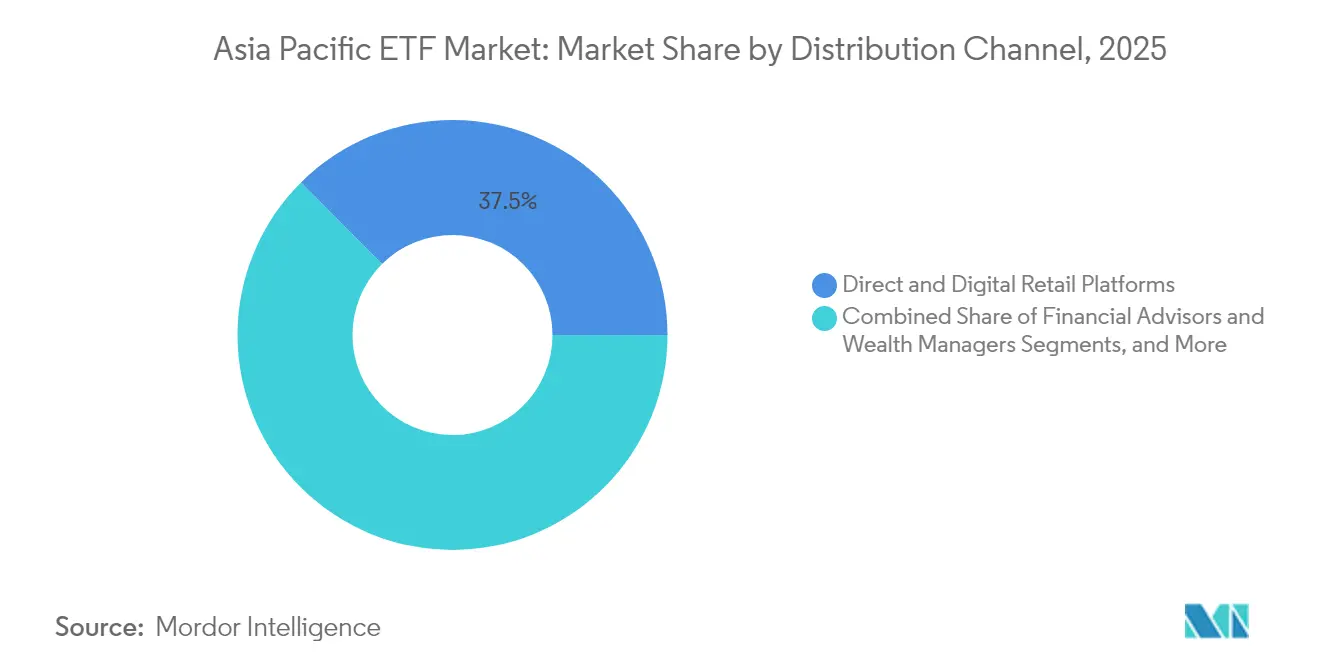

- By distribution channel, direct digital platforms captured 37.45% of the Asia-Pacific ETF market in 2025 and are projected to advance at a 9.88% CAGR.

- By country, Japan retained 31.58% Asia-Pacific ETF market share in 2025, while India is the fastest-growing market at 10.92% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific ETF Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail participation surge via digital platforms | +1.8% | China, Taiwan, South Korea | Medium term (2-4 years) |

| Government-led tax incentives | +1.2% | Japan, South Korea, Singapore | Medium term (2-4 years) |

| Institutional use of fixed-income ETFs | +0.9% | Japan, Australia, Singapore, Hong Kong | Short term (≤2 years) |

| Cross-border fund passport schemes | +0.7% | Hong Kong–China, ASEAN ARFP | Long term (≥4 years) |

| Millennial demand for thematic & ESG ETFs | +1.1% | Australia, Japan, Singapore | Medium term (2-4 years) |

| Expansion of active ETF structures | +1.3% | Australia, South Korea, Taiwan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Retail Participation Surge Fueled by Digital Investment Platforms

Retail investors now hold 61.4% of regional ETF assets, a sharp shift from the institutional skew in North America. Mobile-first brokerage apps have removed minimum ticket sizes and simplified KYC, drawing new savers into the Asia-Pacific ETF market. Taiwan’s retail cohort is especially deep, while mainland China has recorded a rapid climb in individual activity. Issuers are redesigning education content and launching fixed-income and thematic funds once aimed at pensions. Surveys indicate that 96% of surveyed investors intend to lift ETF allocations within 12 months, with millennials leading the appetite for cryptocurrency tails[1]Brown Brothers Harriman, “2025 Global ETF Investor Survey,” bbh.com.

Government-Led Tax Incentive Programs Boosting ETF Savings Vehicles

Japan’s 2024 NISA overhaul deleted expiry windows and doubled annual limits to ¥3.6 million (USD 24,000), injecting more than ¥15 trillion (USD 100 billion) into investment accounts during FY 2024. Similar revisions to South Korea’s ISA and Singapore’s SRS are channeling household cash into low-cost ETFs. Regulators see these accounts as tools to convert dormant savings into productive capital, underpinning long-run growth for the Asia-Pacific ETF market.

Growing Appetite for Thematic & ESG Strategies Among Millennials

Millennial investors favor targeted themes such as AI, automation, and clean energy, propelling ESG inflows of ¥1.2 trillion (USD 8 billion) in Japan alone during 2024. Australia shows similar momentum, and 80% of surveyed Asian investors expect to boost cryptocurrency ETF allocations[2]Brown Brothers Harriman, “2025 Global ETF Investor Survey,” bbh.com. Issuers are accordingly racing to seed niche thematic funds.

Expansion of Active ETF Structures Under Relaxed Regulations

South Korea hosts the region’s highest active ETF penetration, while Taiwan listed its first active fund in May 2025, following rule changes that encourage multi-asset strategies[3]Taiwan Stock Exchange, “Active ETF Listing Notice,” twse.com.tw. Australia projects active products will exceed 50% of new ETF launches in 2025. Active wrappers blend stock-picking with ETF tax and trading efficiencies, diversifying the Asia-Pacific ETF market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory regimes | -0.7% | Pan-APAC, cross-border issuers | Long term (≥4 years) |

| Limited on-exchange liquidity in emerging ASEAN | -0.5% | Thailand, Indonesia, Malaysia, Philippines | Medium term (2-4 years) |

| Misconceptions about ETF risk among retail investors | -0.3% | China, India, Indonesia | Short term (≤2 years) |

| Concentration risk from Japan-focused equity funds | -0.4% | Japan, regional allocations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Regimes Creating High Listing & Compliance Costs

Varied disclosure and operational rules add 15-20% to issuer expense, deterring smaller entrants and curbing innovation. Although ARFP aims to harmonize, member states still impose country-specific filings, unlike Europe’s UCITS template.

Limited On-Exchange Liquidity in Emerging ASEAN Markets

Low trading volumes widen bid-ask spreads and elevate tracking error in Indonesia, Thailand, and Malaysia[4]FTSE Russell, “ASEAN ETF Liquidity Snapshot,” lseg.com. Fixed-income ETFs suffer most where bond price transparency is thin, keeping institutional desks on the sidelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Equity ETFs Dominate While Alternatives Surge

Equity funds commanded 62.68% Asia-Pacific ETF market share in 2025, anchored by Japan-listed Nikkei and TOPIX trackers. Core equity remains a first-stop allocation for both retail and pensions, sustaining turnover and liquidity. Yet alternatives—spanning commodities, private-credit replicas, and digital-asset baskets—are progressing at a 9.34% CAGR, outstripping the wider Asia-Pacific ETF market. Fixed-income ETFs, bolstered by Taiwanese demand, supply cheap duration exposure and intraday price transparency. Commodity products are gaining appeal as inflation hedges, especially in resource-importing economies, while currency-hedged ETFs stay niche tools for sophisticated accounts.

The Asia-Pacific ETF market size tied to alternatives is projected to grow significantly by 2031, expanding product diversity well beyond vanilla beta. Equity dominance will ease incrementally as new wrappers democratize once-esoteric strategies. Investors deploying balanced portfolios increasingly blend equity core positions with commodity and real-asset ETFs for shock absorption.

By Investment Strategy: Passive Dominance Challenged by Active Innovation

Passive vehicles retained an 81.12% share of the Asia-Pacific ETF market in 2025, the legacy of early broad-index launches. However, active ETFs are compounding at 12.03%, more than double the Asia-Pacific ETF market CAGR. South Korea hosts index-beating quant funds wrapped in ETF form, while Australia expects active products to form half of new listings in 2025. Taiwan’s May 2025 debut marks regulatory acceptance of the structure, and Japanese advisers increasingly model portfolios around risk-smart active ETFs.

Across fixed income, managers tout security selection and duration tilts as alpha drivers unattainable in strict index replication. A Brown Brothers Harriman poll shows 33% of investors plan to shift allocations from passive to active ETFs in 2025. The Asia-Pacific ETF market size attributed to active strategies is expected to grow significantly by 2031, carving out a sustainable premium‐fee niche.

By Investor Type: Retail Investors Drive Growth Through Digital Adoption

Retail accounts controlled 61.72% of the share of the Asia-Pacific ETF market in 2025 and are expected to climb at an 8.41% CAGR, outpacing institutional growth. Low entry barriers, cashback promotions, and gamified interfaces encourage first-time savers to choose ETFs as their default wrapper. Mainland Chinese fintech platforms process millions of micro-orders daily, funneling liquidity into flagship CSI-linked funds. Institutional desks remain vital for block liquidity and model portfolio design, yet their proportional share is shrinking as retail expands the Asia-Pacific ETF market.

High-frequency user feedback is also shaping product design. Investors crowd-sourced suggestions for new green-hydrogen ETFs in South Korea, while Indian platforms run real-time education modules to deepen understanding of tracking error. The Asia-Pacific ETF market share claimed by retail investors could edge past 64.85% by 2031 if current digital trends persist.

By Distribution Channel: Digital Platforms Reshape Access Paradigms

Direct digital routes held 37.45% of the share of the Asia-Pacific ETF market in 2025 and are projected to grow at a 9.88% CAGR, displacing legacy bank branches and full-service brokers. Chinese super-apps anchor multi-asset dashboards, while South Korea’s mobile banking ecosystem executes ETF trades in seconds. Advisory and wealth channels remain essential for high-net-worth clients and structured mandates but are pivoting to low-touch, model-based delivery. Traditional banks in Hong Kong and Singapore are retrofitting interfaces to retain relevance.

The Asia-Pacific ETF market size routed via digital platforms is expected to grow significantly, placing technology vendors and API aggregators at the heart of distribution. For issuers, omnichannel presence that blends robo + human touchpoints is swiftly becoming the norm.

By Country: Japan Leads While India Accelerates

Japan’s 31.58% Asia-Pacific ETF market share in 2025 rests on deep liquidity, BOJ support, and NISA-driven retail inflows. India’s 10.92% CAGR is the region’s fastest, reflecting demographic dividends and structural reforms.

Australia’s ETF stack is anticipated to grow significantly as investors diversify globally, while South Korea leads active-ETF penetration. Taiwan holds significant assets, with bond ETFs dominating the market. ASEAN early-stage markets present optionality, though liquidity hurdles linger. Overall, divergent country growth patterns compel issuers to tailor listings, education, and marketing.

Geography Analysis

Japan and China together hold more than half of the regional assets. Japan, supported by NISA reforms and governance-focused stock-exchange policies, logged robust net inflows in 2024. China recorded heightened retail turnover and operationalized ETF Connect, granting offshore users simplified access and letting mainland investors tap Hong Kong listings. India’s double-digit expansion underscores macro tailwinds as the economy climbs the global rankings.

South Korea blends high retail trading activity with the region’s densest line-up of active ETFs. Average daily turnover positions Seoul among the most liquid ETF marketplaces. Australia shows a sustained appetite for offshore equity and ESG themes, propelling its Asia-Pacific ETF market share. Taiwan’s bond-heavy profile mirrors local yield hunting, yet the May 2025 active-ETF debut signals a gradual pivot toward diversified offerings.

Emerging ASEAN venues illustrate contrasting maturity. Singapore’s wealth-hub status and regulatory clarity attract cross-border listings, especially in sustainability-linked funds. Indonesia, Thailand, and Malaysia are improving disclosure norms but still grapple with thin secondary-market liquidity, dampening institutional participation. Vietnam’s young investor base and increasing smartphone penetration hint at latent upside once trading infrastructure scales. Collectively, intra-Asian passport schemes aim to knit these markets into a larger, more fluid Asia-Pacific ETF market.

Competitive Landscape

Large global issuers—BlackRock’s iShares, State Street’s SPDR, and Vanguard—anchor multi-country line-ups and leverage scale for cost leadership. They replicate US or European flagships in local wrappers while customizing indexes for domestic benchmarks. Regional champions such as Nikko Asset Management, Samsung Asset Management, and Mirae Asset Global Investments exploit local brand equity and adviser networks to defend home-turf share and are extending reach into neighboring jurisdictions.

Chinese managers—ChinaAMC, E Fund, Harvest—benefit from policy support and fast-growing A-share liquidity, creating a formidable mainland roster. Product innovation defines the current battleground: 2025 saw launches of AI chipsets, semiconductor supply chains, and electric-vehicle battery ETFs. Active structures are another differentiator; South Korean providers license quant engines, while Australian boutiques seed concentrated high-conviction funds.

Distribution technology is a second competitive lever. Providers partner with robo-advisers and super-apps for one-click purchases, using data analytics to fine-tune education and retention campaigns. Cross-listing strategies, enabled by ETF Connect and ARFP, also boost float and visibility. In early-stage territories such as India, first-mover advantage remains up for grabs, suggesting white-space for both global and home-grown issuers to cement footprints.

Asia-Pacific ETF Industry Leaders

BlackRock iShares

State Street Global Advisors

Nikko Asset Management

Samsung Asset Management

Mirae Asset Global Investments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Taiwan listed its first active ETF after rule changes fostering multi-asset formats.

- April 2025: Asia-Pacific (ex-Japan) ETF assets hit USD 1.25 trillion with USD 61.47 billion monthly net inflows.

- February 2025: Samsung Asset Management unveiled AI and semiconductor thematic ETFs, tapping tech demand.

- January 2025: StashAway enabled Bitcoin and Ethereum ETFs on its platform, broadening digital-asset access.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Asia-Pacific exchange-traded fund market as the total assets under management in open-ended funds that are listed on regional stock exchanges, priced continuously throughout the trading day, and can be created or redeemed in blocks through authorized participants, whether the funds follow passive indexes or disclose active strategies.

Scope exclusions: exchange-traded notes, leveraged certificates, and closed-end investment trusts are left outside the boundary to prevent product-level noise.

Segmentation Overview

- By Asset Class

- Equity ETFs

- Fixed-Income ETFs

- Commodity ETFs

- Currency ETFs

- Real-Estate ETFs

- Alternative ETFs

- By Investment Strategy

- Active

- Passive

- By Investor Type

- Retail

- Institutional

- By Distribution Channel

- Direct and Digital Retail Platforms

- Financial Advisors and Wealth Managers

- Institutional Channels

- Traditional Banks and Full-Service Brokers

- By Country

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Vietnam

- Malaysia

- Philippines

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Conversations with ETF product heads, market-makers, and digital broker executives across Tokyo, Mumbai, Sydney, and Seoul provided live color on creation basket costs, bid-ask drivers, and retail onboarding hurdles, enabling us to ground check secondary ratios and stress-test modeled fee compression paths.

Desk Research

Mordor analysts began with granular monthly AUM tables from regulators such as Japan's FSA, Australia's ASIC, India's SEBI, and China's CSRC, which clarify product counts, domicile shifts, and cross-listings. Broad regional snapshots from ETFGI, IOSCO statistics, and Bank for International Settlements' portfolio flow data helped us trace retail versus institutional penetration trends. We then validated pricing spreads and traded values with exchange bulletins from JPX, HKEX, and SGX. Company filings lodged on EDGAR and regional exchanges supplied fee ladders, while press releases captured new thematic or active launches. Proprietary pulls from Dow Jones Factiva and D&B Hoovers rounded out sponsor financials. The sources named illustrate, rather than exhaust, the material consulted during desk work.

Market-Sizing & Forecasting

We reconstructed 2024 AUM using a top-down roll-up of country regulator totals, which are then reconciled with exchange-level trade values and unit counts. Select bottom-up checks, sampled sponsor AUM disclosures and channel audits, fine-tuned country splits before aggregation. Key model fingerprints include: (1) net creation volume, (2) average expense-ratio glide paths, (3) digital brokerage retail account growth, (4) sovereign pension allocation targets, and (5) cross-border fund passport approvals. A multivariate regression links these drivers to annual AUM change; scenario analysis brackets macro swing factors such as yen policy shifts or PRC stimulus. Where sponsor data lagged, we bridged gaps through three-year moving averages of regulator series.

Data Validation & Update Cycle

Outputs face variance checks against ETFGI and Lipper quarterly snapshots, with anomalies flagged to senior reviewers. The model is refreshed each year and reopened mid-cycle if material events, large regulatory changes or >5% AUM swings, occur, ensuring clients always receive the latest vetted view.

Why Mordor's Asia-Pacific ETF Industry Size & Share Analysis Baseline Commands Reliability

Published figures often diverge because firms mix domiciled and cross-listed funds, toggle between face value and market value, or freeze refreshes for multiple years. Our disciplined scope, country-level regulator feeds, and annual update cadence cut these pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.70 tn (2025) | Mordor Intelligence | - |

| USD 2.15 tn (2023) | Regional Consultancy A | Combines ETFs with exchange-traded notes and uses pre-COVID currency rates |

| USD 0.40 tn (2024) | Global Consultancy B | Limits scope to funds domiciled inside APAC, omitting Japan-listed cross-border ETFs |

| USD 1.51 tn (2025) | Industry Association C | Excludes Japan entirely, focusing on "APAC ex-Japan" data |

The comparison shows that headline gaps stem less from forecasting math and more from what is counted. By anchoring our baseline to audited regulator totals and by aligning inclusion rules to practical investor access, Mordor Intelligence offers a dependable, transparent starting point for strategic decisions.

Key Questions Answered in the Report

What is the current size of the Asia-Pacific ETF market?

The Asia-Pacific ETF market is valued at USD 1.81 trillion in 2026 and is projected to reach USD 2.46 trillion by 2031.

Which country holds the largest share of Asia-Pacific ETF assets?

Japan leads with 31.58% Asia-Pacific ETF market share in 2025, though China is expected to overtake in the near future.

How fast are active ETFs growing in the region?

Active ETFs are expanding at a 12.03% CAGR, almost twice the overall Asia-Pacific ETF market growth rate.

Why are digital platforms important for ETF distribution?

Digital channels captured 37.45% of assets in 2025, growing at 9.88% CAGR, thanks to low fees, seamless onboarding, and broad mobile adoption.

What role do tax-advantaged accounts play in ETF adoption?

Programs such as Japan’s NISA and Singapore’s SRS direct household savings into low-cost ETFs, providing a structural tailwind for long-term growth.

Which asset class inside ETFs is attracting the fastest inflows?

Alternative ETFs, covering commodities and digital assets, are the fastest-growing segment, advancing at a 9.34% CAGR.

Page last updated on: