Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 3.98 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Animal Protein Market Analysis by Mordor Intelligence

The Asia Pacific animal protein market size stands at USD 3.01 billion in 2026 and is forecast to reach USD 3.98 billion by 2031, reflecting a 5.75% CAGR over the period. Robust demand from sports recovery, infant nutrition, and beauty-from-within applications is drawing formulators toward higher-margin functional ingredients. China’s December 2025 imposition of 21.9%–42.7% tariffs on European Union dairy has redirected whey and casein sourcing to New Zealand and Australia, tightening regional supply and accelerating localization by multinationals. Singapore’s approvals for cultivated meat in 2020 and 2024, combined with South Korea’s 2024 insect-protein labeling rules, are broadening the innovation pipeline beyond conventional livestock proteins SFA.GOV.SG. Meanwhile, dairy cooperatives are boosting process investments. Fonterra alone commissioned NZD 75 million in whey and casein capacity in December 2024, to capture premium fortification demand across bakery, beverages, and ready-to-eat meals

Key Report Takeaways

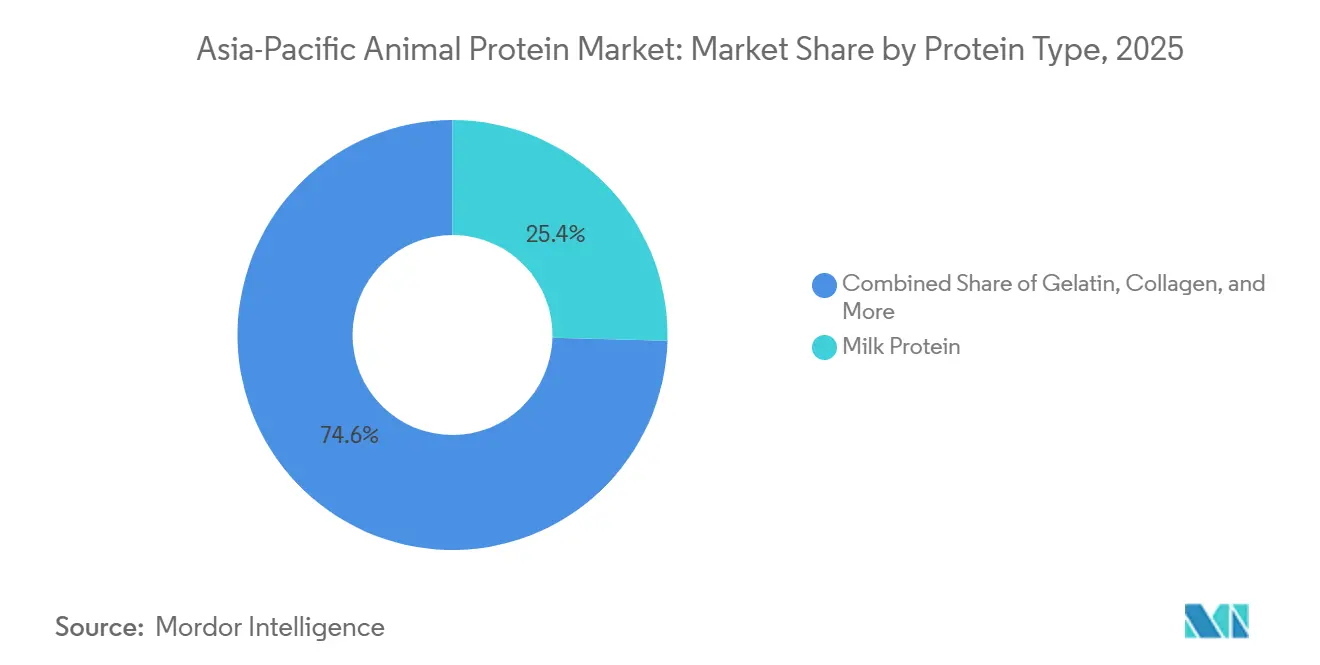

- By protein type, Milk protein led with a 25.42% Asia-Pacific animal protein market share in 2025; insect protein is advancing at a 7.25% CAGR to 2031.

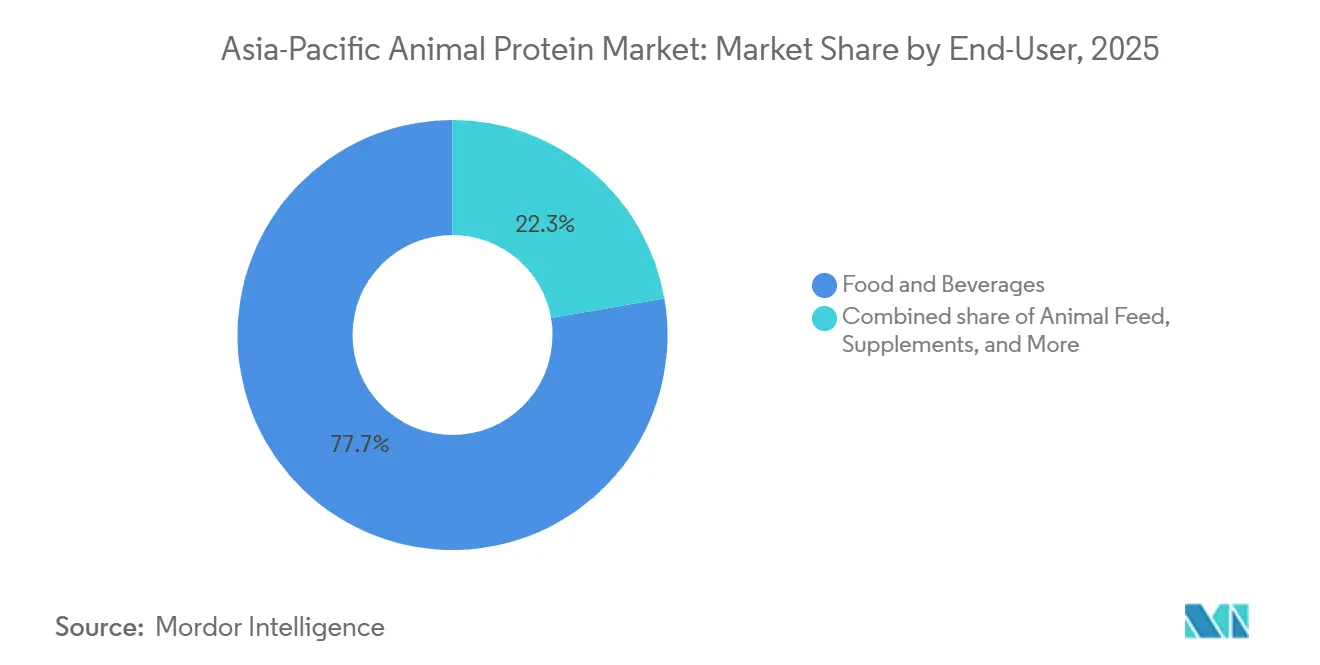

- By end-user, Food and beverages captured 77.72% of the Asia-Pacific animal protein market size in 2025, while personal care and cosmetics are projected to expand at an 8.02% CAGR through 2031.

- By geography, China held 40.56% of the Asia-Pacific animal protein market in 2025; India records the fastest regional growth at a 6.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Animal Protein Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Functional Dairy Ingredients | +1.2% | China, India, Japan, South Korea, Australia | Medium term (2-4 years) |

| Growing Health Consciousness and Awareness of Animal Protein's Nutritional Benefits | +1.0% | Global, with concentration in Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Technological Advancements in Feed Production, Farming, and Processing | +0.8% | China, Thailand, Vietnam, Australia, New Zealand | Long term (≥ 4 years) |

| Product Diversification to Meet Varied Consumer Preferences | +0.7% | China, India, Indonesia, Malaysia, Singapore | Medium term (2-4 years) |

| Rapid Urbanization Increasing Consumption of Protein-Rich Foods in Emerging Economies | +1.3% | India, Indonesia, Vietnam, Philippines, with spillover to Thailand, Malaysia | Medium term (2-4 years) |

| Government Initiatives Supporting Sustainable Animal Agriculture | +0.9% | India, China, Australia, New Zealand, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Functional Dairy Ingredients

Functional dairy ingredients are shifting from niche sports-nutrition channels to mainstream applications such as bakery products, beverages, and ready-to-eat formats. This transition is driven by formulators aiming for clean-label protein fortification without sacrificing taste or texture. In December 2024, Fonterra will commission a NZD 75 million (USD 45 million) protein-ingredients line at Studholme, reflecting the growing demand for whey protein concentrates and isolates with 80-90% protein content, designed for high-protein yogurts and meal-replacement bars. China's domestic collagen peptide market consumes 4,000 to 5,000 tonnes annually in raw-material equivalent. Products like oral liquids and solid granules are priced between RMB 300 and RMB 600 (USD 42 to USD 84) per month, demonstrating a willingness to pay premium prices for bioavailable formats that combine marine collagen with vitamin C to enhance absorption. In Japan, per-capita meat expenditure is forecast to increase from USD 633.70 in 2023 to USD 751.50 by 2028, representing a 3.5% annual growth rate. This rise, which outpaces population growth, indicates a shift toward higher-protein cuts and value-added products such as collagen-enriched broths. These trends create opportunities for ingredient suppliers to secure higher margins by offering technical support—such as solubility optimization, heat stability, and flavor masking—that commodity whey or casein cannot provide.

Growing Health Consciousness and Awareness of Animal Protein's Nutritional Benefits

Post-pandemic health awareness has driven increased adoption of animal protein products, which are marketed for benefits such as immunity support, muscle maintenance, and metabolic health. These products have gained popularity, particularly among aging populations and fitness-conscious millennials. A 2024 survey conducted across six Asia-Pacific markets provided key insights: 51% of collagen users prioritize beauty and skin health, while 29% focus on joint health. This dual-purpose positioning merges the boundaries between food supplements and cosmeceuticals. In Japan, the population aged 90 and above is growing at an annual rate of 4.4% through 2040, fueling consistent demand for easily digestible whey protein isolates and hydrolyzed collagen peptides. These ingredients are essential for preventing sarcopenia and supporting wound healing in elderly care settings, as noted in the Japan Ministry of Health, Labor and Welfare's 2024 Population Projections[1]Source: Japan Ministry of Health, Labor and Welfare, "Population Projections for Japan: 2024 to 2040," mhlw.go.jp. Glanbia's Performance Nutrition segment reported first-half 2024 revenue of EUR 1.48 billion, reflecting a 10.7% increase in constant currency. This growth, particularly strong in China and India, is driven by expanding e-commerce channels and rising gym memberships. Amid this scenario, hybrid blends combining 75% animal protein with 25% plant protein could attract the 28% of consumers willing to replace at least half of their meat intake. This approach offers a practical solution for industry players to maintain market share while addressing sustainability concerns.

Government Initiatives Supporting Sustainable Animal Agriculture

China, India, and Australia are implementing national policies to promote methane reduction, improve feed efficiency, and establish traceability systems. These initiatives aim to align animal protein production with climate commitments but also introduce compliance costs that benefit larger, well-capitalized operators. Between 2021 and 2026, India's National Programme for Dairy Development allocated INR 2,880 crore (USD 346 million) to modernize milk procurement infrastructure, install bulk milk coolers, and develop dairy processing plants in underserved regions. These efforts are crucial in addressing post-harvest losses, which previously reached 15-20% during the summer months. In 2024, Singapore's framework for insect protein, managed by the Singapore Food Agency, approved 16 insect species for human consumption and animal feed. This positions Singapore as a regulatory leader for novel proteins, with the potential to replace fishmeal in aquaculture, where protein content requirements exceed 40%. Similarly, Australia's Department of Foreign Affairs and Trade issued guidance in 2024 to assist exporters with Indonesia's halal certification mandate, effective October 2026[2]Source: Australia Department of Foreign Affairs and Trade. "Indonesia Halal Certification Guide 2024," dfat.gov.au. The guidance noted that 12 Australian halal certification bodies have secured accreditation from Indonesia's BPJPH, a process that previously required 6-12 months.

Product Diversification to Meet Varied Consumer Preferences

Ingredient suppliers are shifting away from generic commodity whey by introducing specialized protein formats such as hydrolyzed peptides, microencapsulated powders, and heat-stable isolates to address specific challenges in beverages, bakery, and personal care. In November 2024, Arla Foods launched "Arla Protein," a high-protein pudding, along with lactose-free dairy lines in China. This initiative targets consumers with digestive sensitivities and those seeking convenient, portion-controlled snacks that provide 15-20 grams of protein per serving. In February 2025, Morinaga Milk partnered with PT ABC Kogen Dairy to introduce dairy products in Singapore. This partnership highlights a strategy to develop formulations tailored for tropical climates, where temperatures exceed 30°C. These conditions require ultra-high-temperature processing and aseptic packaging to ensure shelf life without refrigeration. Yili's commissioning of a 100,000-tonne-per-year ice cream factory in Huanggang, Hubei, in the first half of 2024, represents a significant move toward vertical integration. This approach allows Yili to capture margins across the value chain, from raw milk procurement and protein extraction to consumer branding. Meiji's USD 90 million investment in a Shanghai ice cream plant, also in the first half of 2024, reflects a focus on premiumization. Collagen-infused and low-sugar variants in this segment command a 30-50% price premium over standard offerings.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Feed Costs Impacting Production Profitability | -0.7% | China, India, Thailand, Vietnam, Indonesia | Short term (≤ 2 years) |

| Stringent Regulations on Antibiotics, Additives, and Food Safety Standards | -0.5% | Indonesia, Malaysia, Singapore, Japan, Australia | Medium term (2-4 years) |

| Competition from Plant-Based Protein Alternatives Gaining Popularity | -0.4% | Singapore, Japan, South Korea, urban China | Medium term (2-4 years) |

| Biosecurity Threats and Zoonotic Disease Risks | -0.6% | China, Japan, Vietnam, South Korea, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuating Feed Costs Impacting Production Profitability

Margin erosion remains a significant challenge for dairy, poultry, and pork producers due to fluctuations in corn and soybean meal prices. In intensive livestock systems, feed accounts for 60-70% of total production costs, forcing operators to either bear financial losses or pass on the increased costs to downstream buyers. According to the USDA's December 2024 feed outlook, corn is projected at USD 4.10 per bushel and soybean meal at USD 310 per short ton for the 2024-25 marketing year. These projections represent a 15-20% rise from the lows of 2023, driven by weather disruptions in the U.S. Midwest and strong export demand from China. In 2023, China produced 288.84 million tonnes of corn domestically but imported 27.16 million tonnes to meet the feed requirements of its hog and poultry operations recovering from African swine fever. This reliance makes China particularly vulnerable to global supply shocks. Thailand's poultry sector, which exports USD 3.2 billion worth of chicken annually, faced margin pressures in 2024 due to a 25% surge in soybean meal prices caused by drought in Argentina, the world's largest exporter. This situation highlights how regional producers remain exposed to South American weather conditions despite the geographical distance. In 2020, Indonesia imported USD 2.91 billion worth of animal fodder (HS code 23), emphasizing its reliance on external supply chains that are susceptible to freight-rate fluctuations and changes in trade policies.

Biosecurity Threats and Zoonotic Disease Risks

Outbreaks of avian influenza, African swine fever, and foot-and-mouth disease result in culling operations, trade restrictions, and disruptions to consumer confidence. These events significantly impact protein supply chains, causing unpredictable shifts in demand across various species categories. In December 2024, Japan experienced a highly pathogenic avian influenza outbreak, leading to the culling of 160,000 chickens in Hokkaido. In November 2024, Miyazaki prefecture culled 41,000 birds. These measures triggered temporary export bans in the affected zones and caused price increases for eggs and poultry meat. In December 2024, China's Sichuan province culled 17,828 birds following the detection of H5N1 at a commercial poultry farm. This followed reports from Guangxi in November 2024, where cases were identified in migratory birds, highlighting the endemic presence of avian influenza along Asia's flyways. Outbreaks in 2024-2025 required localized culling and movement restrictions, disrupting pork supply to coastal processing plants, as detailed in the FAO ASF Situation Report Asia 2024[3]Source: FAO, “Aquaculture Feed Guidelines 2024,” fao.org. In Vietnam, outbreaks in northern provinces during 2024 led to culling operations that delayed herd recovery. Similarly, the Philippines imposed trade restrictions on Luzon in response to ASF detections.

Segment Analysis

By Protein Type: Dairy Leads but Insects Ascend

Milk protein held 25.42% of the Asia Pacific animal protein market in 2025, benefiting from entrenched use in infant formula, sports powders, and bakery glazes. Whey isolates deliver 90% protein with minimal lactose, supported by Glanbia’s USD 100 million Idaho plant that began supplying Asia in 2024. Caseinates continue as emulsifiers in coffee whiteners, yet European suppliers face redirected trade flows after China’s dairy tariffs, potentially boosting Southeast Asian imports. Collagen maintains premium positioning in Japan and South Korea, where 51% of users link intake to skin benefits. Gelatin straddles food and pharma, with Darling Ingredients expanding Asian rendering capacity. Egg protein struggled with 2024 avian-influenza-driven shortages yet remains indispensable for mayonnaise and confectionery texture.

Insect protein is projected to record a 7.25% CAGR to 2031, the fastest among sub-segments, as Singapore’s 2024 framework and South Korea’s labeling rules open channels for human food and aquafeed. Early adopters target shrimp and tilapia feeds, substituting fishmeal while trimming greenhouse emissions. Hydrolyzed fish proteins, bone-broth concentrates, and other niche animal proteins are also gaining share by aligning with clean-label demands. Collectively, these shifts illustrate how the Asia Pacific animal protein market rewards suppliers who combine regulatory foresight with targeted formulation support.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Beauty-Driven Personal Care Races Ahead

Food and beverages represented 77.72% of the Asia-Pacific animal protein market size in 2025, anchored by bakery, dairy, and beverage fortifications that rely on whey concentrates and caseinates for structure and rapid amino-acid delivery. Ready-to-drink shakes use whey isolate to deliver 25 grams of protein while maintaining low viscosity, addressing on-the-go recovery needs. Hydrolyzed collagen and gelatin enhance moisture in frozen entrées, minimizing ice-crystal damage during storage. Animal feed remains significant as aquaculture seeks 40%–50% protein rations; insect meal is emerging as a cost-effective alternative that also supports circular-economy objectives.

Personal care and cosmetics, though smaller, are forecast to expand at an 8.02% CAGR through 2031, outpacing food growth as ingestible beauty supplements gain traction. Chinese consumers spend up to RMB 600 per month on marine collagen liquids blended with vitamin C for enhanced absorption. Japanese and Korean brands market collagen-infused broths and low-sugar ice creams that command 30%–50% premiums over standard variants. Sports and performance nutrition remains vibrant, with Optimum Nutrition and domestic challengers pushing bars and chips that provide 15 grams of protein without elevating sugar. The convergence of nutrition and cosmetics is therefore redefining growth pockets within the Asia Pacific animal protein industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China contributed 40.56% of the Asia Pacific animal protein market in 2025, underpinned by 39.2 million tonnes of milk output and vertical integration moves such as Yili’s 100,000-tonne ice-cream complex commissioned in H1 2024. December 2025 tariffs on European dairy raised landed costs by 30%, pushing multinationals to locate whey and casein production closer to Chinese consumers, while benefiting New Zealand exporters. Collagen liquids priced between RMB 300 and RMB 600 per month continue to capture beauty-conscious buyers, reflecting rising disposable incomes. Ongoing African swine fever outbreaks force periodic culls that redirect consumption to poultry and fish, spurring cross-category volatility.

India is projected to grow at a 6.85% CAGR through 2031, driven by INR 2,880 crore in dairy-infrastructure funding under the National Programme for Dairy Development and complementary breed-improvement incentives under Rashtriya Gokul Mission. E-commerce channels distribute international whey and casein brands to a rising gym-going middle class, while local cooperatives accelerate milk-collection modernization. However, fragmented cold-chain infrastructure and smallholder dominance constrain export competitiveness. Japan’s median age will reach 54.3 years by 2040, with a 90-plus cohort expanding at 4.4% yearly, sustaining demand for easily digested whey isolates and collagen-rich medical foods MHLW.GO.JP. Per-capita meat spending is rising to USD 751.50 by 2028, signaling trade-up behavior despite population decline. December 2024 avian-influenza culls raised egg prices, revealing supply-chain fragility that favors diversified protein portfolios.

Indonesia’s October 2026 halal-certification deadline affects USD 2.5 billion in meat and dairy trade, propelling exporters to secure BPJPH accreditation or risk exclusion. Malaysia streamlined halal approval to 15 days, enabling its halal industry to target 10.8% of GDP by 2030. South Korea’s cultivated-meat labeling rules from May 2024 position the country as a regulatory peer to Singapore, fostering cross-border research and development. Vietnam, Thailand, Singapore, and New Zealand round out a region where regulatory heterogeneity and infrastructure disparities shape divergent growth curves within the Asia Pacific animal protein market.

Competitive Landscape

The Asia-Pacific animal protein market exhibits low concentration, as regional dairy cooperatives, multinational ingredient suppliers, and emerging insect-protein startups compete across overlapping application segments without a single player commanding a dominant share. Fonterra's August 2025 agreement to sell its Consumer brands business to Lactalis for NZD 3.845 billion (USD 2.3 billion) exemplifies a strategic retreat from retail toward higher-margin B2B ingredients and foodservice channels, where the company invested NZD 150 million in a Studholme protein-ingredients facility and NZD 150 million in a Whareroa cool store during December 2024. This pivot mirrors broader industry dynamics where scale advantages in commodity whey and casein are eroding as customers demand specialized formats, hydrolyzed peptides, microencapsulated powders, heat-stable isolates that require technical service and formulation expertise rather than raw tonnage.

White-space opportunities center on insect protein for aquaculture feed, where Singapore's 2024 regulatory framework permitting 16 species creates a pathway to substitute fishmeal in shrimp and tilapia diets, potentially reducing reliance on wild-caught fish stocks. Emerging disruptors include precision fermentation startups targeting casein and whey production without cows, though production costs remain 3-5 times higher than conventional dairy, limiting near-term market penetration to premium restaurant channels. Technology deployment is bifurcating the market: Kerry Group's May 2024 acquisition of Niacet for EUR 844 million (USD 920 million) brought bioscience capabilities in food preservation and animal nutrition, enabling integrated solutions that extend shelf life and improve feed conversion ratios, while smaller players lack the capital to invest in membrane filtration or spray-drying innovations that improve solubility and flavor profiles.

Halal certification is becoming a competitive moat in Indonesia and Malaysia, where streamlined processes favor established multinationals with dedicated compliance teams over smaller exporters who struggle to navigate BPJPH or JAKIM requirements. Arla Foods. However, biosecurity threats, avian influenza, African swine fever, and foot-and-mouth disease create volatility that favors vertically integrated players with diversified protein portfolios over specialists concentrated in a single species or geography, as demonstrated by Japan's December 2024 culling of 160,000 chickens in Hokkaido and China's ongoing ASF outbreaks.

Asia-Pacific Animal Protein Industry Leaders

-

Arla Foods amba

-

Darling Ingredients Inc.

-

Fonterra Co-operative Group Limited

-

Kerry Group PLC

-

Koninklijke FrieslandCampina N.V.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: New Zealand-based Leaft Foods has entered the pet food market with Alfalfa Protein Concentrate (APC), a Rubisco-based protein extracted from alfalfa leaves, offering meat-like nutrition with 99% lower carbon emissions than beef or lamb per independent LCA.

- July 2025: Chiyoda Corporation successfully launched Japan's first "Plant Biofoundry" in Yokohama as a demonstration platform for plant bio-manufacturing. This facility was developed under a NEDO initiative to enable large-scale, animal-free production of useful proteins—including the world's first human type II collagen produced in tobacco plants.

- May 2025: Darling Ingredients and Tessenderlo Group announced the formation of a new joint company to accelerate growth in collagen-based health, wellness, and nutrition sectors, combining complementary capabilities and market access to expand addressable market opportunities across multiple application segments.

Asia-Pacific Animal Protein Market Report Scope

Animal protein is protein from animal sources like meat, poultry, fish, eggs, and dairy.

The Asia-Pacific animal protein market is segmented by protein type into casein and caseinates, collagen, egg protein, gelatin, insect protein, milk protein, whey protein, and other animal protein. By end-user, the market is segmented into animal feed, food and beverages, personal care and cosmetics, and supplements. The food and beverages are further segmented into bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy-alternative products, RTE/RTC foods, and snacks. Supplements are further segmented into baby food and infant formula, elderly and medical nutrition, and sport/performance nutrition. The market is segmented by geography into China, India, Japan, Australia, South Korea, Indonesia, Thailand, Singapore, Vietnam, Malaysia, New Zealand, Rest of Asia-Pacific. The market sizing has been done in value terms in USD for all the abovementioned segments.

Protein Type

| Casein and Caseinates |

| Collagen |

| Egg Protein |

| Gelatin |

| Insect Protein |

| Milk Protein |

| Whey Protein |

| Other Animal Protein |

End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments / Sauces | |

| Confectionery | |

| Dairy and Dairy-Alternative Products | |

| RTE / RTC Foods | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly and Medical Nutrition | |

| Sport / Performance Nutrition |

Geography

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| New Zealand |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Protein Type | Casein and Caseinates | |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments / Sauces | ||

| Confectionery | ||

| Dairy and Dairy-Alternative Products | ||

| RTE / RTC Foods | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sport / Performance Nutrition | ||

| Geography | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| New Zealand | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF