Asia-Pacific Legal Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 13.56 Billion |

| Market Size (2026) | USD 14.2 Billion |

| Market Size (2031) | USD 17.86 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Legal Services Market Analysis by Mordor Intelligence

Asia-Pacific legal services market size in 2026 is estimated at USD 14.2 billion, growing from 2025 value of USD 13.56 billion with 2031 projections showing USD 17.86 billion, growing at 4.72% CAGR over 2026-2031. The trajectory is underpinned by rising cross-border investment, regulatory harmonization, and growing economic complexity that compel corporates to seek sophisticated counsel. Digital transformation is reshaping workflows as firms automate research, review, and documentation while alternative legal service providers capture standardized mandates. Diversified client demand, from multinationals to tech-enabled SMEs, supports resiliency, even as talent shortages and price sensitivity test margins[1]Asian Development Bank, “Regional Comprehensive Economic Partnership: Legal Implications 2024,” adb.org . Competitive intensity remains moderate; global firms, regional champions, and tech-driven entrants vie for share by scaling platforms and deepening expertise.

Key Report Takeaways

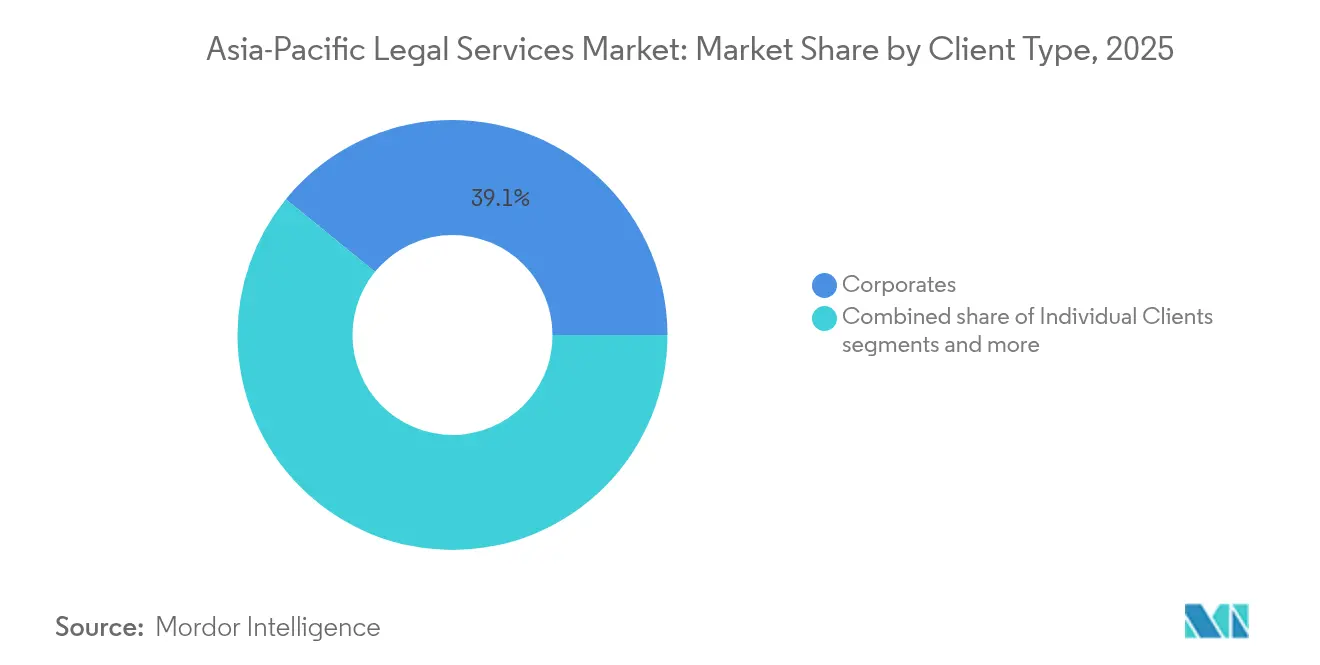

- By client type, corporates commanded 39.12% revenue share of the Asia-Pacific legal services market in 2025; SMEs are the fastest-growing cohort at a 8.78% CAGR to 2031.

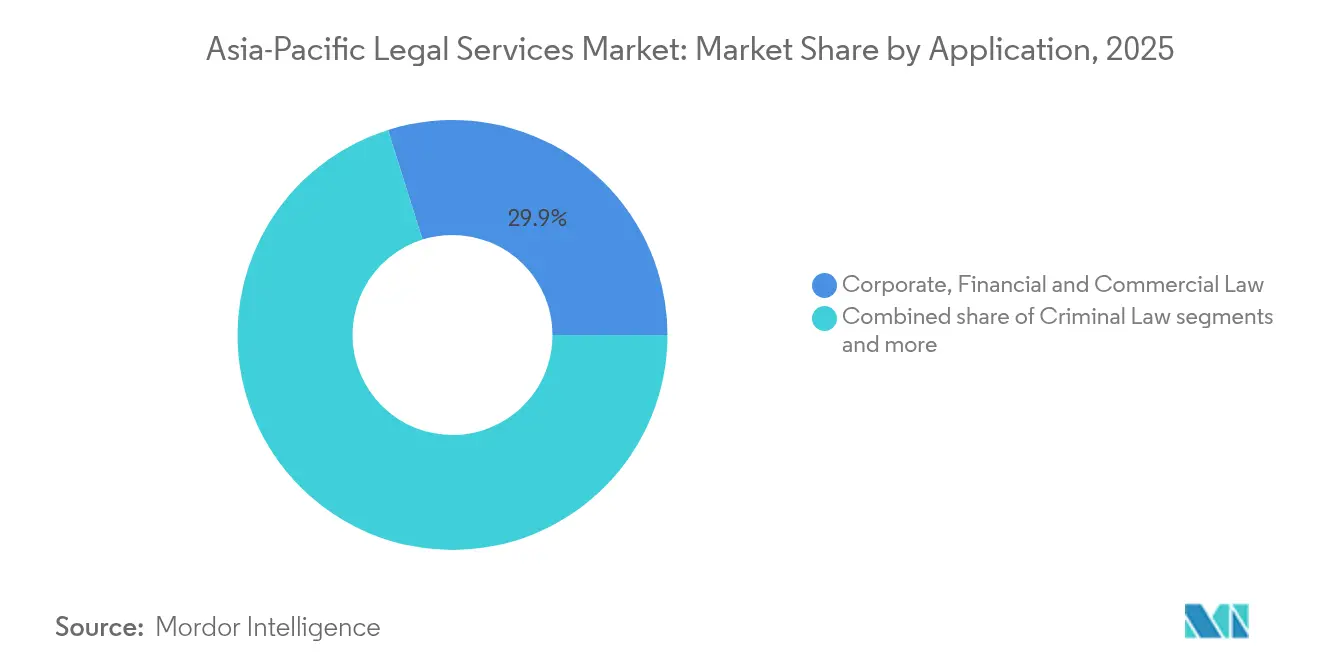

- By application, corporate, financial, and commercial law accounted for 29.85% of the Asia-Pacific legal services market size in 2025, whereas intellectual-property and technology law is slated to advance at a 10.25% CAGR through 2031.

- By service, representation and advocacy made up 28.35% share of the Asia-Pacific legal services market size in 2025, yet legal research and documentation is pacing ahead at a 11.64% CAGR to 2031.

- By geography, China held 32.25% of the Asia-Pacific legal services market share in 2025, while India is projected to deliver a 9.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Legal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid economic growth & FDI inflows | +0.7% | China, India, core ASEAN states | Medium term (2-4 years) |

| Increasing regulatory complexity | +1.0% | Japan, Australia, cross-border operations | Long term (≥ 4 years) |

| Digital transformation & legal-tech adoption | +0.9% | Singapore, Australia, South Korea | Short term (≤ 2 years) |

| Expansion of RCEP & other trade pacts | +0.6% | All 15 RCEP members, spill-over to wider Asia-Pacific | Medium term (2-4 years) |

| Litigation-financing market growth | +0.5% | Hong Kong, Singapore, Australia | Medium term (2-4 years) |

| Rising ESG-related advisory demand | +0.7% | Japan, Australia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Economic Growth & FDI Inflows

Large-scale transactions necessitate comprehensive processes, including joint-venture structuring, merger approvals, and national-security screenings across various jurisdictions. Additionally, initiatives such as the Belt-and-Road project and other mega-infrastructure undertakings introduce intricate frameworks involving layered concession agreements and dispute-resolution mechanisms that span financial, construction, and public-law domains. To address these complexities, law firms are strategically expanding their regional operations to provide end-to-end advisory services, covering all stages from transaction origination to post-closing activities. Given the sustained strength of capital inflows, the demand for cross-border legal expertise is projected to remain robust throughout the forecast period.

Increasing Regulatory Complexity

More than 14 Asia-Pacific jurisdictions now enforce dedicated data-protection statutes with disparate consent, localization, and breach-notification rules. ESG disclosure frameworks anchored to Task Force on Climate-related Financial Disclosures (TCFD) guidelines multiply compliance checkpoints for listed companies, especially in Japan and Australia. Rapid fintech innovation triggers new licensing sandboxes, particularly in Singapore and Hong Kong, demanding specialist legal guidance. ASEAN and APEC harmonization initiatives alleviate some divergence, yet simultaneously introduce fresh standards firms must interpret. Consequently, multinationals prize advisors capable of delivering coordinated, multi-market compliance strategies.

Digital Transformation & Legal-Tech Adoption

The integration of generative AI in contract drafting has significantly reduced first-pass preparation times by over 50%, enabling legal professionals to allocate more time to high-value, strategic activities. The adoption of cloud-based practice management software has facilitated seamless, real-time collaboration across geographically dispersed offices, a critical capability for managing complex cross-border transactions. Additionally, alternative legal service providers are increasingly utilizing automation to deliver fixed-fee compliance solutions, thereby capturing a growing share of the market for standardized legal tasks and challenging the dominance of traditional law firms. Furthermore, blockchain technology pilots for smart contracts within Singapore's financial sector underscore the substantial cost-efficiency potential of emerging technologies in the legal domain.

Expansion of RCEP & Other Trade Pacts

The Regional Comprehensive Economic Partnership (RCEP) now accounts for a substantial share of the global GDP. It establishes harmonized rules of origin, simplifies tariff classifications, and implements robust investor-state safeguards, thereby fostering a more integrated and predictable trade environment across member nations [2]Law Society of Singapore, “Legal Talent Development Challenges 2024,” lawsociety.org.sg . Companies restructuring supply chains seek counsel on preferential-treatment eligibility and dispute-settlement architecture. Digital-trade chapters governing data flows and cybersecurity create niches for privacy and technology lawyers. Overlapping bilateral agreements add complexity, prompting demand for cost-benefit mapping across multiple regimes. Firms equipped with experienced trade benches across member countries capture significant advisory volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity among SMEs | -0.4% | India, tier-2 ASEAN economies | Short term (≤ 2 years) |

| Shortage of specialized legal talent | -0.3% | Japan, Australia, niche fields | Medium term (2-4 years) |

| Fragmented data-protection regimes | -0.2% | Cross-border transactional hubs | Long term (≥ 4 years) |

| Cultural reluctance toward legal action | -0.2% | Japan, South Korea, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Among SMEs

Cost remains a significant barrier for SMEs in the Asia-Pacific region when engaging external legal counsel, highlighting a critical challenge in the market. The adoption of fixed-fee subscription models and unbundled service modules is gaining momentum; however, the increasing downward pressure on pricing for standardized legal tasks is compressing profit margins. Inflationary pressures are further exacerbating the situation, prompting smaller firms to delay non-essential legal expenditures, even at the potential cost of future compliance risks. The proliferation of online platforms offering automated filing solutions and template-based contracts is expanding access to legal services but simultaneously driving the commoditization of entry-level offerings. To address these dynamics, law firms targeting the SME segment are increasingly focusing on outcome-based pricing strategies and developing scalable, cost-efficient do-it-yourself toolkits to meet the evolving needs of this market.

Shortage of Specialized Legal Talent

In Tokyo and Sydney, the vacancy rates for legal professionals specializing in cybersecurity, AI regulation, and ESG have exceeded double digits, creating significant challenges for the legal services market. This shortage has led to salary inflation that surpasses the average increases observed across the broader professional services sector. The lack of specialized capabilities is causing delays in deal execution and limiting firms' ability to compete for complex cross-border assignments, thereby impacting their growth potential. Efforts to address these gaps, such as implementing continuous professional development programs and facilitating overseas secondments, are underway but require substantial investments of time and financial resources. Additionally, virtual collaboration tools have emerged as a partial solution, enabling firms to leverage global talent pools for Asia-Pacific-related matters. However, the persistent scarcity of specialists continues to constrain market expansion, with sustainable improvement dependent on the maturation of training pipelines and talent development initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Client Type: Corporates Maintain Primacy While SMEs Accelerate

Corporates generated 39.12% of 2025 revenue, reflecting their need for complex structuring, antitrust clearance, and multi-jurisdictional compliance. This cohort retains full-service panels, ensuring recurring advisory work across competition, tax, and ESG lanes. SMEs, growing at a 8.78% CAGR, leverage cloud platforms that package documentation and filings at fixed fees, broadening participation in the Asia-Pacific legal services market. Government clients produce steady demand tied to infrastructure procurement and regulatory reform, while individuals still rely on counsel for family, real estate, and estate-planning matters. Differing technology adoption patterns—enterprise contract-lifecycle platforms for corporates versus consumer-facing apps for SMEs—shape service-delivery models.

Outcome-based pricing expands as both corporates and SMEs demand predictability. Corporate law departments benchmark external-counsel spend using analytics dashboards, pressuring firms to track matter-level profitability. SMEs gravitate toward subscription bundles providing compliance calendars and templated contracts. Regional network expansion by law firms follows corporate mandates for seamless cross-border coverage, whereas SMEs support a vibrant domestic-specialist ecosystem. Together, these dynamics position corporates as revenue anchors and SMEs as growth accelerants in the Asia-Pacific legal services market.

By Application: IP and Technology Law Captures Growth Momentum

Corporate, financial, and commercial law remained the largest application at 29.85% of the 2025 value, propelled by sustained M&A, capital-raising, and restructuring volumes. Intellectual property and technology law are forecast to expand at a 10.25% CAGR through 2031 as AI deployment, semiconductor innovation, and digital asset tokenization heighten protection needs. Real-estate law stays resilient amid urbanization and logistics-hub construction, though growth moderates in mature markets. Labor-law advisory remains vital as hybrid-work regulations and diversity mandates evolve across jurisdictions. Alternative-dispute-resolution practices flourish with the greater acceptance of arbitration clauses in cross-border contracts.

Tax and regulatory services intersect with new profit-allocation rules and e-commerce levies, reinforcing the need for specialized counsel. Cybercrime and fraud prosecutions rise as digital transformation widens attack surfaces, lifting white-collar criminal-law workloads. Family-law practitioners adopt online case-management tools for routine matters while reserving high-touch services for complex disputes. Broadly, application diversity mitigates cyclical risk across the Asia-Pacific legal services market.

By Service: Research and Documentation Outpaces Traditional Advocacy

Representation and advocacy still produced 28.35% of 2025 revenue, underscoring the importance of court and arbitral advocacy. Yet legal research and documentation are scaling fastest at a 11.64% CAGR as regulatory text and precedent databases proliferate. Advisory and consultancy lanes grow alongside proactive compliance and risk-management demand. Tax services remain sturdy due to complex cross-border profit-allocation rules, while bankruptcy and restructuring volumes swing with credit cycles. Digital notarization pilots in Singapore and Australia reduce wait times and enhance authenticity, signalling modernization across formalities.

AI engines now sift millions of judgments in seconds, allowing attorneys to pivot from retrieval to interpretation. Process standardization enables near-shoring of documentation to lower-cost regional centres, freeing partner bandwidth for strategic counsel. Fixed-fee research packages give clients cost clarity, while subscription models turn one-off projects into recurring revenue. Altogether, research and documentation epitomize technology’s role in reshaping value pools within the Asia-Pacific legal services market.

Geography Analysis

China commanded 32.25% of revenue in 2025 owing to its vast economy, dense regulatory landscape, and outbound-investment appetite. Ongoing antitrust enforcement and data-security legislation generate regular advisory pipelines. Foreign firms use joint ventures with mainland practices to satisfy bar restrictions and deepen service capacity. Domestic firms deploy AI for due diligence, reducing costs for domestic clients. Meanwhile, Belt-and-Road projects funnel multilayered mandates in financing, construction law, and dispute resolution.

India is projected to grow at 9.46% CAGR through 2031, fueled by record FDI and a burgeoning fintech ecosystem. Partial liberalization of foreign-firm entry sparks collaborations, enhancing service sophistication. A large English-speaking talent pool sustains the country’s prominence in legal process outsourcing. Online legal platforms cater to startups, widening access for early-stage enterprises. Corporate-governance reforms and GST compliance requirements ensure a steady pipeline of advisory work.

Japan, Australia, and South Korea each exhibit mature yet vibrant legal markets. Japan’s stewardship-code revisions and mandatory climate disclosures expand corporate-governance mandates. Australia functions as a regional arbitration hub, underpinned by clear litigation-funding rules that draw international claimants. South Korea’s tech-focused export base spurs IP-protection and antitrust needs as firms globalize. Singapore anchors Southeast Asia’s legal ecosystem with top-tier arbitration facilities and fintech-friendly regulations. Vietnam, Indonesia and the Philippines register IPO and infrastructure upticks, expanding addressable demand across emerging ASEAN economies.

Competitive Landscape

The regional market demonstrates a moderate degree of fragmentation, with the top five firms collectively accounting for a significant portion of total revenue. This level of concentration highlights the substantial influence of leading players while presenting opportunities for smaller competitors to expand their presence. Prominent global firms, including Dentons, King & Wood Mallesons, and Baker McKenzie, leverage their extensive international networks to provide comprehensive services to multinational clients across corporate, regulatory, and dispute resolution domains. In contrast, domestic firms such as Rajah & Tann and Zhong Lun capitalize on their deep-rooted local relationships and cost efficiencies, often forming strategic alliances with international firms to manage inbound transactions. The rise of alternative legal service providers, driven by advancements in AI and automation, continues to disrupt the market by capturing a growing share of standardized legal work, thereby intensifying competition. Investment in technology remains a critical component of strategic initiatives within the market.

For instance, Baker McKenzie has established a technology center in Singapore focused on developing proprietary AI tools to enhance due diligence processes, while Clifford Chance Asia has implemented document-review automation across four operational hubs to streamline workflows. Despite these advancements, significant growth opportunities persist in underdeveloped segments such as ESG (Environmental, Social, and Governance), cyber-risk management, and e-discovery. These areas exhibit a notable gap between the demand for specialized expertise and the current supply, creating a white-space opportunity for firms to differentiate themselves and capture unmet market needs. This dynamic underscores the importance of innovation and specialization as key drivers of competitive advantage in the evolving legal services landscape.

Asia-Pacific Legal Services Industry Leaders

Dentons

King & Wood Mallesons

Baker McKenzie

Clifford Chance Asia

Nishimura & Asahi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Baker McKenzie has inaugurated an Asia-Pacific Legal Technology Center in Singapore, emphasizing AI-driven contract analytics and compliance.

- September 2024: WongPartnership launched a legal-tech incubator in Singapore to co-create client-facing solutions with startups.

- June 2024: Ashurst acquired a 50-lawyer Singapore technology and IP team for USD 25 million to sharpen AI and data-protection capabilities.

- May 2024: Herbert Smith Freehills has unveiled its global Digital Legal Delivery practice, uniting its most innovative legal and tech experts.

Asia-Pacific Legal Services Market Report Scope

Legal services, provided by lawyers and legal professionals, assist individuals, businesses, and organizations in navigating legal complexities and ensuring law compliance. These services include contract advice, court representation, and document assistance. Lawyers often specialize in family, real estate, or criminal law, tailoring their expertise to specific needs. Legal services uphold justice, safeguard rights, and resolve disputes within the legal framework. Access to these services ensures legal guidance, protection, and resolution, fostering a fair and orderly society.

The Asia-Pacific legal services market is segmented by end user, application, service, and geography. By end user, the market is segmented into legal aid consumers, private consumers, SMEs, charities, large businesses, and government. By application, the market is segmented into corporate, financial, and commercial law, personal injury, commercial and residential property, wills, trusts, and probate, family law, employment law, and criminal law. By service, the market is segmented into representation, taxation, litigation, bankruptcy, advice, notarial activities, and research. By geography, the market is segmented into India, China, Japan, and Rest of Asia-Pacific. The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Corporates |

| Small and Medium Enterprises (SMEs) |

| Individual Clients |

| Government and Public Sector |

| Corporate, Financial, and Commercial Law |

| Real Estate and Property Law |

| Family and Personal Law |

| Employment and Labor Law |

| Criminal Law |

| Intellectual Property and Technology Law |

| Dispute Resolution and ADR |

| Taxation and Regulatory Law |

| Representation and Advocacy |

| Taxation Services |

| Advisory and Consultancy |

| Bankruptcy and Restructuring |

| Notarial and Certification Services |

| Legal Research and Documentation |

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) |

| Rest of Asia-Pacific |

| By Client Type | Corporates |

| Small and Medium Enterprises (SMEs) | |

| Individual Clients | |

| Government and Public Sector | |

| By Application | Corporate, Financial, and Commercial Law |

| Real Estate and Property Law | |

| Family and Personal Law | |

| Employment and Labor Law | |

| Criminal Law | |

| Intellectual Property and Technology Law | |

| Dispute Resolution and ADR | |

| Taxation and Regulatory Law | |

| By Service | Representation and Advocacy |

| Taxation Services | |

| Advisory and Consultancy | |

| Bankruptcy and Restructuring | |

| Notarial and Certification Services | |

| Legal Research and Documentation | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value and projected growth rate for Asia-Pacific legal services?

The segment is valued at USD 14.2 billion in 2026 and is projected to reach USD 17.86 billion by 2031, reflecting a 4.72% CAGR.

Which client group is expanding quickest within Asia-Pacific legal counsel?

Small and medium enterprises are advancing at a 8.78% CAGR, outpacing corporates, government bodies and individual clients.

How is legal-tech adoption altering service delivery across the region?

A significant share of large firms now deploy AI-driven review tools, cutting first-pass drafting time by more than half and enabling fixed-fee, tech-enabled offerings.

Why is India regarded as the fastest-growing geography for legal services?

Strong FDI inflows, regulatory modernization, and a booming fintech ecosystem push India to a forecast 9.46% CAGR through 2031.

What impact do ESG requirements have on legal-service demand in Asia-Pacific?

Mandatory climate-risk disclosures and supply-chain due diligence laws in markets such as Australia, Japan, and Singapore are creating steady, high-value advisory pipelines.

How concentrated is competition among Asia-Pacific legal advisers?

The largest firms hold more than one-fourth of regional revenue, giving the field leaving room for regional specialists and tech-led entrants.

Page last updated on: