Size and Share of Artificial Intelligence Market In Sports

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

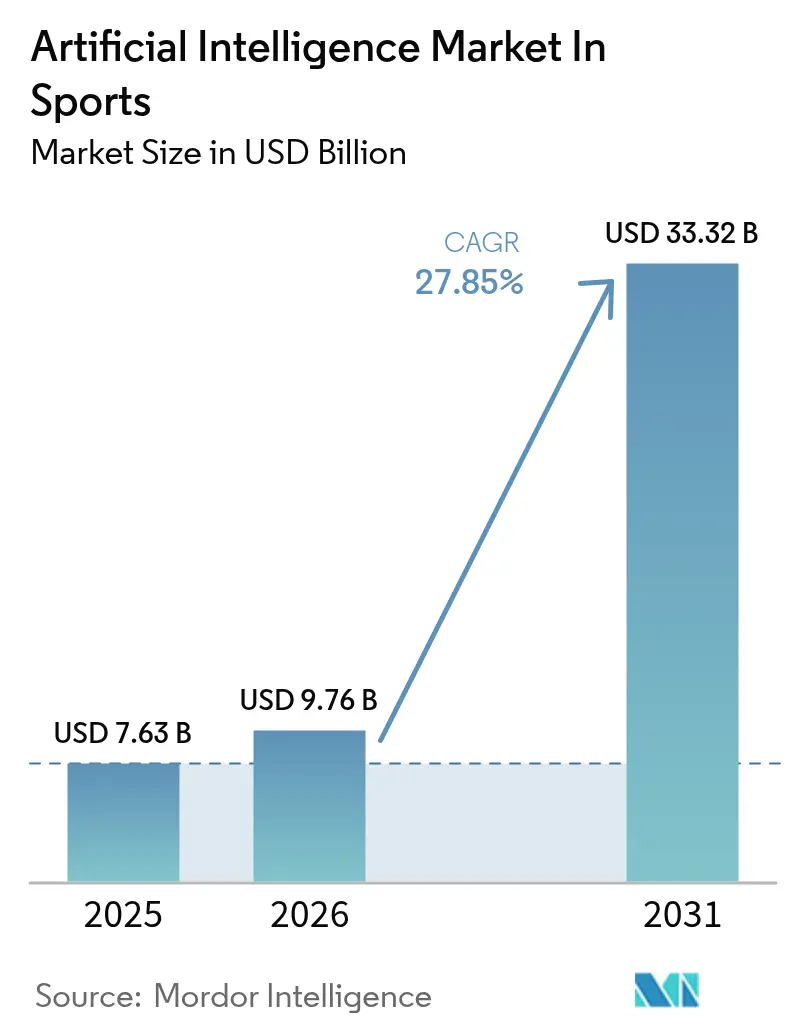

| Market Size (2026) | USD 9.76 Billion |

| Market Size (2031) | USD 33.32 Billion |

| Growth Rate (2026 - 2031) | 27.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Artificial Intelligence Market In Sports by Mordor Intelligence

The Artificial Intelligence Market size in sports market was valued at USD 7.63 billion in 2025 and estimated to grow from USD 9.76 billion in 2026 to reach USD 33.32 billion by 2031, at a CAGR of 27.85% during the forecast period (2026-2031). Demand growth reflects the professional leagues’ race to monetize data and refine on-field decisions while keeping fans engaged in real-time. Intensifying investment in edge computing, optical-tracking systems, and generative content engines is shortening the insight-to-action cycle, allowing coaches to adjust tactics mid-game and rights-holders to create tailored viewing experiences. Computer vision accuracy improvements are propelling automated event detection, and cloud hyperscalers’ expanding edge nodes are reducing latency for live analytics. Meanwhile, data-governance standards such as ISO 42001 persuade risk-averse clubs to modernize without losing control of sensitive biometrics. Consolidation, exemplified by Sportradar’s Vaix takeover, signals a platform race where scale, proprietary datasets, and service depth decide winners.

Key Report Takeaways

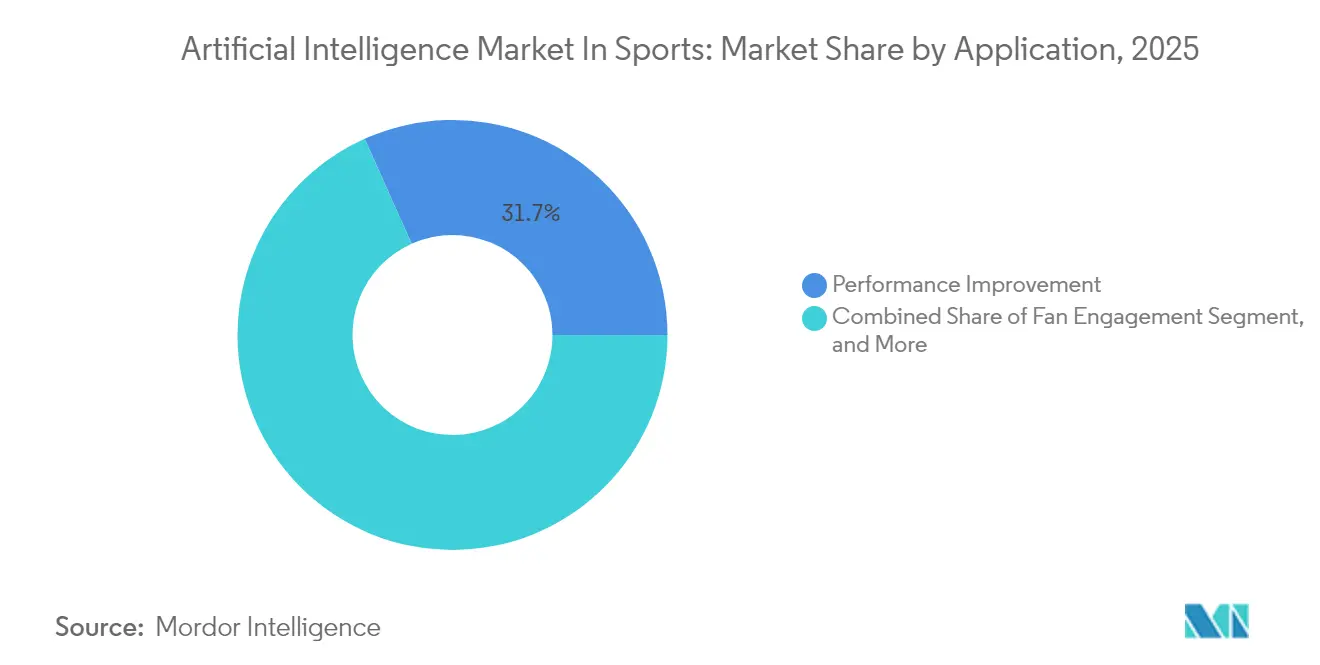

- By application, Performance Improvement held 31.70% of the Artificial Intelligence Market in Sports; market share in 2025, while Injury Prevention is projected to climb at a 33.25% CAGR to 2031.

- By component, Software commanded a 60.85% share of the Artificial Intelligence Market in Sports; market size in 2025; Services are advancing at a 33.10% CAGR through 2031.

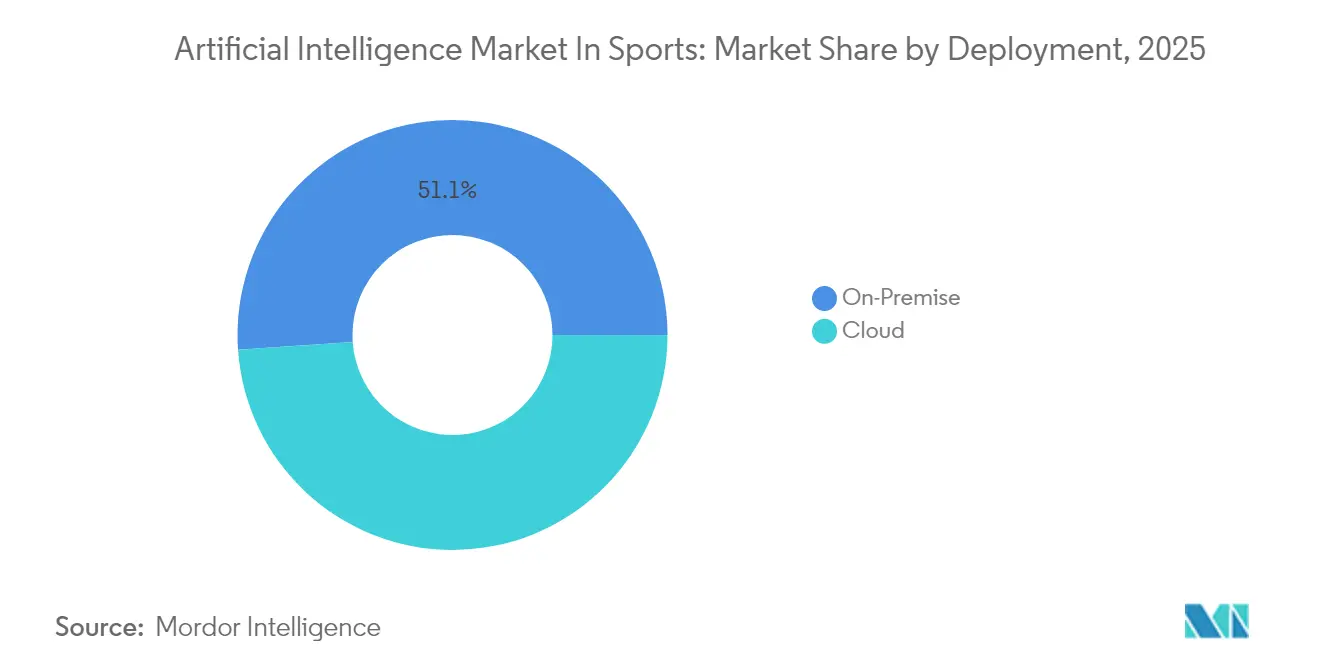

- By deployment, on-premise installations controlled 51.10% of the Artificial Intelligence Market in Sports; market share in 2025, whereas cloud solutions are expanding at a 36.20% CAGR to 2031.

- By technology, Machine Learning and Deep Learning captured 40.20% of the Artificial Intelligence Market in Sports; market share in 2025, but Computer Vision is expected to grow at a 29.10% CAGR through 2031.

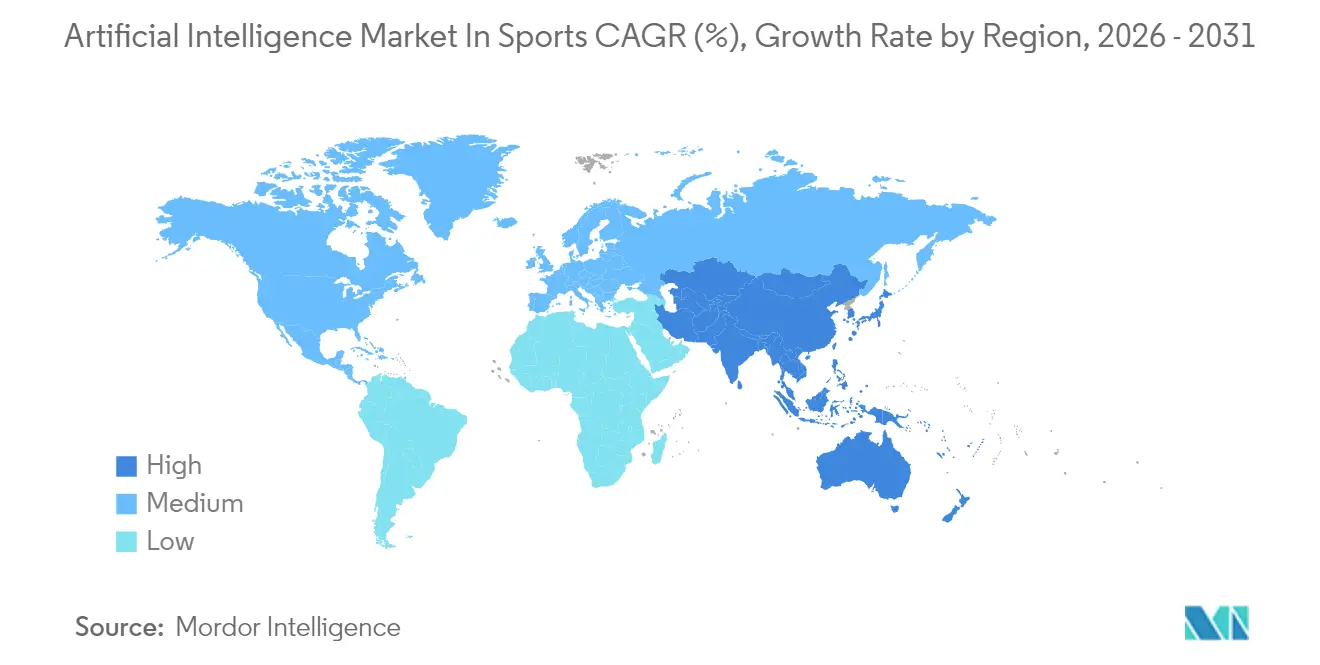

- By geography, North America led with 37.95% of the Artificial Intelligence Market in Sports; market share in 2025; Asia-Pacific is the fastest-growing region at a 30.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Artificial Intelligence Market In Sports

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of AI-driven fan-engagement solutions | +5.2% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of affordable cloud-based AI services | +4.9% | Global, emerging markets accelerating | Long term (≥ 4 years) |

| Proliferation of wearables and IoT athlete tracking | +5.7% | North America and Europe, Asia-Pacific fast uptake | Medium term (2-4 years) |

| Rise of digital-twin valuation models for scouting | +3.1% | Europe and North America; selective APAC adoption | Long term (≥ 4 years) |

| Monetization via AI-generated short-form content | +2.2% | Global, social-media led | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing demand for real-time performance analytics

Real-time analytics has migrated from post-game dashboards to edge-enabled systems that deliver second-by-second feedback to coaches. Sportradar’s 28% year-over-year revenue jump in Q1 2024 underscores commercial traction for live data feeds. The Los Angeles Rams collaborated with SprintAI on a Google Cloud platform that centralizes biometrics and tactical video, letting staff adjust workloads mid-drive.[1]Mikko Simon, “News — Sprint AI,” sprint.ai Edge devices process sensitive data in-stadium, so teams gain speed without risking leaks. This practice blends competitive advantage with privacy compliance, accelerating adoption across contact sports where split-second calls decide outcomes.

Rapid adoption of AI-driven fan-engagement solutions

Broadcasters and leagues now embed betting widgets, auto-generated highlights, and chatbots into streams to convert passive spectators into paying superfans. Genius Sports’ GeniusIQ platform fuses optical tracking with generative content to power BetVision, integrating live NFL video and interactive wagers. ESPN applies generative AI to craft real-time recaps for lacrosse and women’s soccer, cutting editing costs while lifting engagement. Start-ups such as Cerebro Sports bring AI chatbots to grassroots basketball, widening the fan-data funnel. [2]Cerebro Sports, “Cerebro Sports to Launch Game-Changing Basketball AI-Powered Chatbot on Google Cloud,” cerebrosports.com Monetization stems from targeted ads and micro-transactions, turning engagement software into a core revenue pillar.

Expansion of affordable cloud-based AI services

Hyperscalers are pouring capital into AI infrastructure, slashing compute costs for sports franchises. Oracle’s 52% Infrastructure-as-a-Service surge and Microsoft’s multi-billion-dollar AI budget reflect a capacity race that lowers entry barriers for second-tier clubs. Pay-per-use pricing lets amateur leagues access the same inference engines that elite teams employ, aligning cost with seasonal peaks. Low-latency edge zones process positional data during live games, while bulk historical datasets stay in regional clouds to satisfy sovereignty laws. Subscription models transform capital expense into operating outlays, freeing cash for player development.

Proliferation of wearables and IoT athlete tracking

Sensor prices keep falling, and multi-modal wearables now capture heart rate, micro-g accelerations, and perspiration chemistry. Global wearable revenue is forecast to climb from USD 70.30 billion in 2024 to USD 152.82 billion by 2029, an underpinning for data-hungry sports applications. TrackMan’s USD 750 million golf business shows how radar-based swing metrics spawn entire training franchises. Fusing wearable streams with video and environmental data yields granular fatigue indices that inform load-management and injury-avoidance protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High end-to-end implementation cost | -3.4% | Global, emerging markets hardest hit | Short term (≤ 2 years) |

| Shortage of sports-AI talent | -2.8% | North America and Europe, spreading worldwide | Medium term (2-4 years) |

| Emerging biometric-data privacy restrictions | -2.1% | Europe leading, widening geographically | Long term (≥ 4 years) |

| GPU supply-chain concentration and cost volatility | -1.9% | Global, APAC manufacturing dependency | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High end-to-end implementation cost

Comprehensive AI rollouts demand cameras, sensors, cloud capacity, and skilled staff, lifting total cost beyond initial license fees. Hybrid offerings that bundle hardware and SaaS, such as TrackMan’s simulator plus software subscription, mitigate sticker shock yet lock buyers into multi-year payments. Cloud migration eases capital strain, but integration and change management still require external consultants whose fees weigh on semi-pro budgets.

Shortage of sports-AI talent

Combining biomechanics insight with machine-learning expertise is rare. SprintAI’s audit across 114 Olympic training centers exposed broad readiness gaps despite hardware availability. Competitive salary bidding pits leagues against big-tech recruiters, inflating wages beyond what minor clubs can sustain. Graduate programs lag behind demand, so the pipeline stays thin through at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Performance Analytics Drives Professional Adoption

Performance Improvement captured the largest slice of the Artificial Intelligence Market in sports, with a market share of 31.70% in 2025, indicating that teams prioritize a competitive edge from data-driven insights. Injury Prevention, however, will expand at a 33.25% CAGR as clubs quantify the cost of sidelined stars. The Artificial Intelligence Market in Sports, tied to health analytics, is projected to multiply as predictive algorithms flag fatigue early, allowing medical staff to intervene before minor strains escalate. Automated highlight creation, chat-based fan services, and referee assistance tools further boost demand but still trail performance and injury modules in spending.

The shift toward preemptive health management reflects the economics of insurance. Wearable telemetry integrates with computer vision video to identify asymmetries and deceleration spikes that precede muscle tears. Salary-cap leagues reap direct financial benefits when high-paid athletes avoid lengthy layoffs, thereby incentivizing enterprise-wide buy-in. Meanwhile, fan-engagement bots draw lessons from performance datasets to generate content in a voice authentic to each club, blending both sporting and commercial outcomes.

By Component: Services Growth Signals Implementation Complexity

Software retained 60.85% of the Artificial Intelligence Market in sports, with a market size of $4.65 billion in 2025, thanks to established analytics suites. However, services will surge at a 33.10% CAGR, outstripping pure product sales. Clubs now understand that dashboards alone do not translate into wins; they need data engineers, sports scientists, and change managers. The Artificial Intelligence Market in Sports; market share for managed services, therefore, rises as vendors wrap continuous optimization and compliance monitoring around their platforms.

SprintAI’s delivery model includes onsite performance consultants embedded with coaching staff, illustrating how services revenue often eclipses licensing fees. Custom integrations align feeds from GPS vests, LIDAR stadium cameras, and medical EMR systems. The labor-intensive nature of these rollouts underpins sustained demand for services through 2031, even as software modules become more user-friendly.

By Deployment: Cloud Acceleration Despite Security Concerns

On-premise architectures still controlled 51.10% of the Artificial Intelligence Market in Sports, maintaining a market share in 2025, as franchises view datasets as trade secrets. Yet cloud subscriptions will post a 36.20% CAGR, narrowing the gap as ISO 42001 frameworks codify controls. Hybrid designs that keep biometric gold in local servers while streaming anonymized fan data to public clouds strike a workable balance. Artificial Intelligence Market in Sports; market size gains from cloud come largely from mid-tier leagues that cannot fund private data centers.

Hyperscalers now offer “sports clouds” with pre-built ingestion pipelines and edge caching, slashing deployment time from months to weeks. Automatic scaling during major tournaments avoids the sunk cost of idle off-season hardware. Data-residency zones meet national requirements, persuading European football clubs and North American college programs to migrate non-sensitive workloads.

By Technology: Computer Vision Emerges as Growth Leader

Machine Learning and Deep Learning held a 40.20% share in 2025, but Computer Vision is forecast to be the fastest riser at a 29.10% CAGR, as 8K cameras and edge GPUs enable real-time pose estimation. The Artificial Intelligence Market in Sports; market size linked to video analytics is lifted by leagues that monetize event-level data through betting feeds and smart-replay packages. Artificial Intelligence Market in the Sports; industry chatbots leverage NLP to convert those clips into human-readable narratives, closing the loop between raw pixels and audience engagement.

Optical tracking, coupled with generative AI, such as GeniusIQ’s suite, classifies every pass, shot, and sprint within seconds, providing broadcasters with cut-downs before the next play. Edge inferencing minimizes bandwidth costs by transmitting only event metadata, rather than full video, which is crucial in venues with patchy connectivity.

Geography Analysis

North America generated the highest spending in 2024, driven by established professional leagues, robust sponsorship dollars, and early adoption of cloud analytics. Franchise valuations balloon when proprietary datasets underpin new revenue categories such as micro-betting and real-time merchandise offers. Collaborations among rights-holders, broadcasters, and sportsbooks sharpen the commercialization flywheel. Regulatory oversight remains light-touch, but looming federal privacy proposals prompt clubs to invest in encryption and consent management.

The Asia-Pacific region is scaling swiftly as state-sponsored infrastructure and domestic device supply chains cut costs. Government grants subsidize AI labs in national training centers, and telecom operators bundle 5G edge services with sports-specific SLAs. High smartphone penetration enables direct-to-fan micro-content that monetizes rural viewers who were previously unreachable through linear TV. The region’s share of the Artificial Intelligence in Sports market size is expected to widen once Kai Tak Sports Park in Hong Kong and similar complexes open, as public procurement often mandates AI telemetry platforms.

Europe blends innovation with stringent privacy statutes. Clubs must architect AI systems around GDPR constraints, elevating demand for on-premise processing and federated analytics. National football leagues partner with tech vendors on privacy-preserving vision models that strip identifiers at the camera source. The European Commission’s backing for trustworthy AI labs channels grants toward the development of explainable algorithms, making compliance a competitive edge for vendors able to certify their models. Language diversity and cross-border rights deals add complexity, yet also drive demand for automated localization and multilingual commentary bots.

Competitive Landscape

The market structure is moderately fragmented, with niche performance-tracking specialists coexisting alongside global cloud providers. Sportradar’s January 2025 acquisition of Vaix strengthens its generative content stack and signals a pivot from raw data distribution to end-to-end storytelling.[4]Le Lézard Editors, “Italian K-Sport Acquires Australia's SPT to Boost Global Presence in AI-Driven Soccer Analytics,” lelezard.com K-Sport’s EUR 50 million acquisition of SPT plants an Italian wearables firm into 1,100 client sites, evidencing regional roll-up strategies that raise entry barriers for start-ups. Data-rights ownership emerges as the main moat; vendors with exclusive league partnerships monetize both B2B analytics and B2C fan apps.

Technology giants leverage economies of scale. Microsoft courts franchises with integrated cloud, analytics, and media workflow pipelines, bundling AI credits into long-term stadium naming rights deals. Oracle positions its autonomous databases for low-touch back-office analytics, while Google Cloud markets sport-specific APIs that accelerate time-to-insight for developers. Sports-focused challengers answer by specializing: Cerebro Sports concentrates on basketball, combining proprietary youth datasets with chat interfaces, whereas TrackMan dominates swing and launch-monitor metrics across golf and baseball.

Strategic moves cluster around AI governance. Vendors obtaining early ISO 42001 certification win bids from public-sector sports bodies and collegiate programs wary of compliance risk. Edge-optimized inference accelerators tailored for 120-frame-per-second feeds become a hardware battleground. Intellectual-property skirmishes surface over pose-estimation algorithms, pushing companies to amass patent portfolios or seek cross-licensing deals. Co-development pacts between clubs and tech suppliers ensure feedback loops that harden products against real-world edge cases.

Leaders of Artificial Intelligence Market In Sports

Stats Perform

Sportradar AG

IBM Corporation

SAP SE

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TrackMan showcased Tee Box’s rollout of 21 indoor golf venues using its simulators as growth engines.

- January 2025: Sportradar sealed the Vaix acquisition to embed generative-content engines that auto-craft highlights, boosting cross-platform fan engagement.

- January 2025: Sportradar sealed the Vaix acquisition to embed generative-content engines that auto-craft highlights, boosting cross-platform fan engagement.

- December 2024: PlayersTV acquired Cloud Media Center, integrating AI ad-insertion to raise CPM yields for athlete-driven channels.

- October 2024: Los Angeles Rams entered a multi-year pact with SprintAI to deploy a Google Cloud platform that synthesizes biometrics and video for real-time coaching.

Scope of Report on Artificial Intelligence Market In Sports

Artificial Intelligence is a part of computer science deployed to mimic human functions like reading, answering, and recognizing images or voices of things to transform or improve decision-making based on data received from other sources. Artificial intelligence in sports is being employed to track player performance and help improve the health of the player through suggestions on injury - but now AI and machine learning are being used in sports enterprise applications to enhance sports planning.

The artificial intelligence market in sports is segmented into application (player analysis, fan engagement, data interpretation & analysis, and other applications), deployment (on-premises and cloud), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Player Analysis |

| Fan Engagement |

| Coaching and Game Strategy |

| Broadcast and Media Production |

| Refereeing and Officiating Support |

| Operations and Venue Management |

| Software | |

| Services | Managed Services |

| Professional Services |

| On-Premises |

| Cloud |

| Machine Learning and Deep Learning |

| Computer Vision |

| Natural Language Processing |

| Data-Analytics Platforms |

| Edge AI and Real-Time Streaming |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Application | Player Analysis | ||

| Fan Engagement | |||

| Coaching and Game Strategy | |||

| Broadcast and Media Production | |||

| Refereeing and Officiating Support | |||

| Operations and Venue Management | |||

| By Component | Software | ||

| Services | Managed Services | ||

| Professional Services | |||

| By Deployment | On-Premises | ||

| Cloud | |||

| By Technology | Machine Learning and Deep Learning | ||

| Computer Vision | |||

| Natural Language Processing | |||

| Data-Analytics Platforms | |||

| Edge AI and Real-Time Streaming | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Artificial Intelligence Market in Sports industry in 2031?

It is forecast to reach USD 33.32 billion, growing at a 27.85% CAGR between 2026-2031.

Which application area is growing the fastest?

Injury Prevention solutions are expected to post a 33.25% CAGR through 2031 as clubs seek predictive health analytics.

Why are services revenue rising so quickly?

Complex integrations and the need for embedded data-science teams push Services to a 33.10% CAGR, outpacing software sales.

Which region offers the highest growth opportunity?

Asia-Pacific shows a 30.60% CAGR, supported by government investment and local device manufacturing advantages.

Page last updated on: