Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

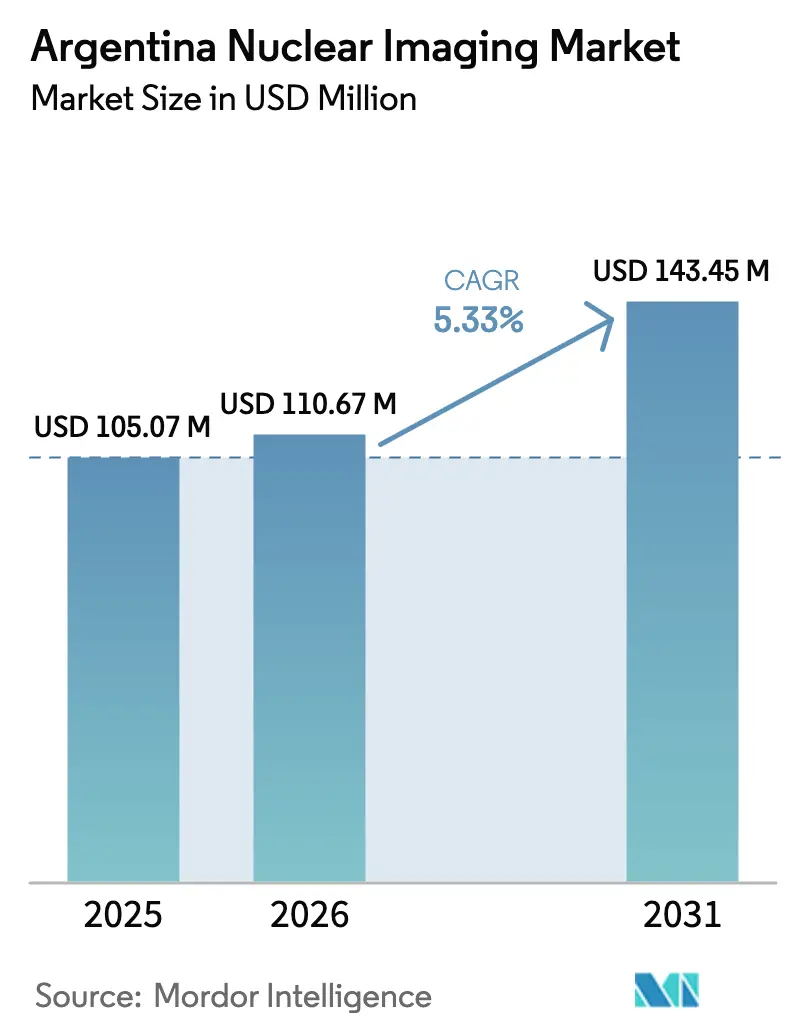

| Base Year Market Size (2025) | USD 105.07 Million |

| Market Size (2026) | USD 110.67 Million |

| Market Size (2031) | USD 143.45 Million |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

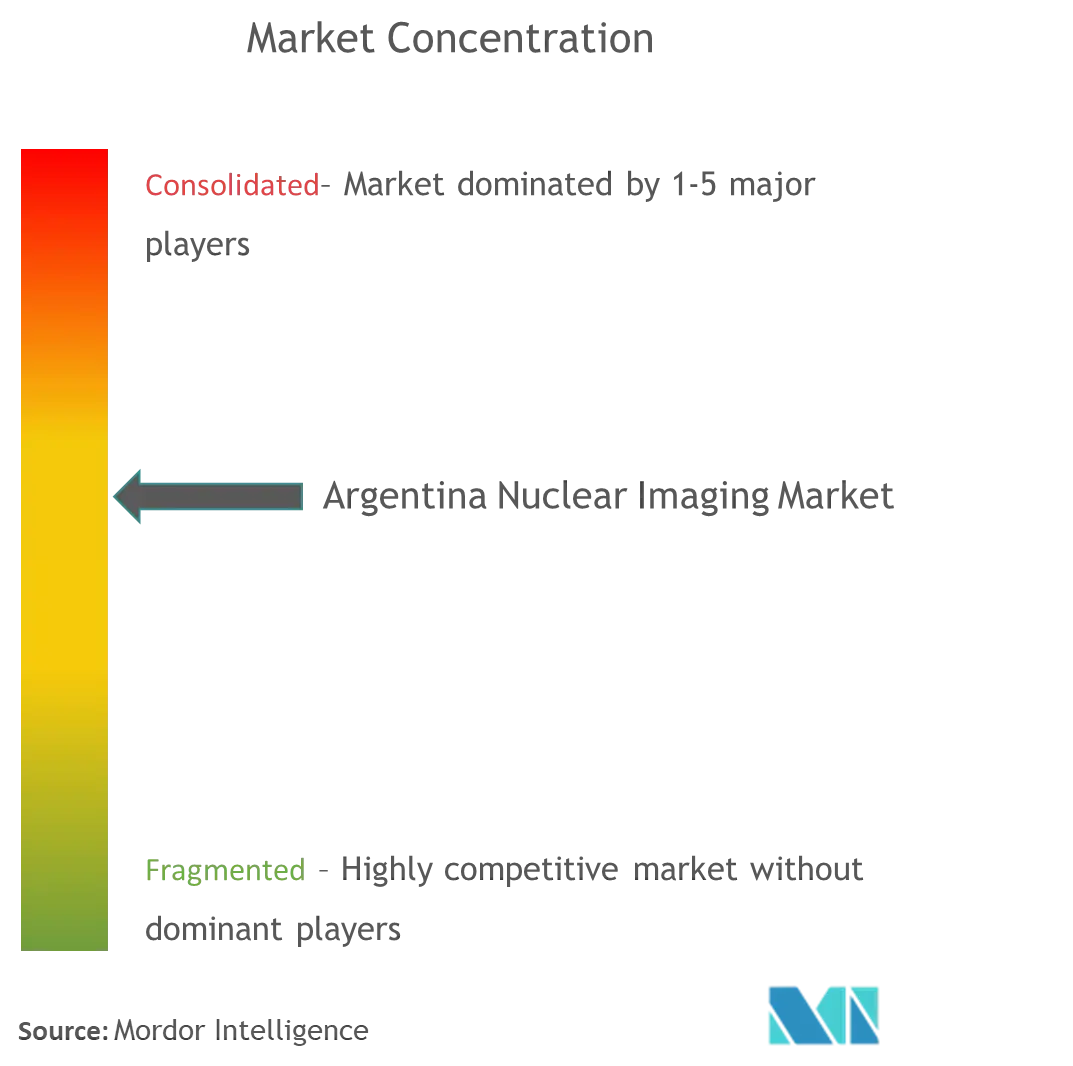

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Nuclear Imaging Market Analysis by Mordor Intelligence

The Argentina nuclear imaging market size is expected to grow from USD 105.07 million in 2025 to USD 110.67 million in 2026 and is forecast to reach USD 143.45 million by 2031 at 5.33% CAGR over 2026-2031. This solid trajectory reflects growing domestic isotope production, expanded public reimbursement, and private investment in hybrid imaging centers. Oncology‐driven demand, bolstered by Argentina’s National Cancer Control Program, is lifting PET/CT procedure volumes while cardiology continues to underpin SPECT utilization. The forthcoming RA-10 reactor promises supply self-reliance for molybdenum-99, a key precursor for technetium-99m scans, which reduces exposure to currency swings and global supply shocks. Parallel adoption of AI dose-optimization platforms is raising scanner throughput and lowering patient radiation, encouraging hospitals to refresh aging equipment stocks. In addition, National Atomic Energy Commission (CNEA) grants for theranostic tracer trials are accelerating the shift toward precision imaging applications across the Argentina nuclear imaging market.

Key Report Takeaways

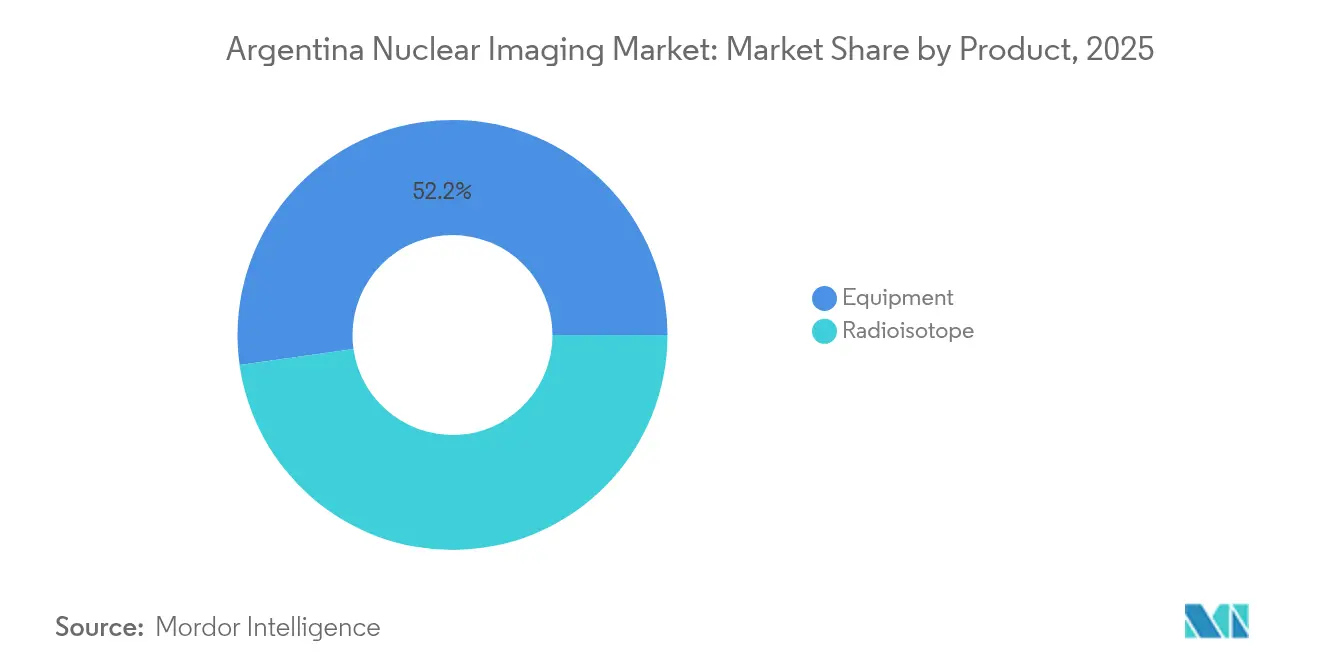

- By product, equipment led with 52.22% of Argentina nuclear imaging market share in 2025, whereas radioisotopes are forecast to expand at a 5.56% CAGR through 2031.

- By application, cardiology accounted for 58.19% of the Argentina nuclear imaging market size in 2025, while neurology exhibits the highest projected CAGR at 7.78% to 2031.

- By end user, hospitals held 60.65% revenue share in 2025; diagnostic imaging centers are advancing at a 5.93% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public reimbursement expansion for PET/CT scans | +1.2% | National, concentrated in Buenos Aires and major urban centers | Medium term (2-4 years) |

| Private-sector investment in hybrid imaging centers | +0.8% | Buenos Aires, Córdoba, Rosario metropolitan areas | Short term (≤ 2 years) |

| Growing oncology caseload and precision-medicine shift | +1.5% | National, with higher concentration in urban areas | Long term (≥ 4 years) |

| Installation of domestic Mo-99 production reactor (2025) | +0.9% | National supply chain impact | Medium term (2-4 years) |

| AI-enabled dose-optimization software adoption | +0.4% | Major hospitals and diagnostic centers | Short term (≤ 2 years) |

| CONEA grants for theranostic tracer trials | +0.3% | Academic and research institutes nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public Reimbursement Expansion for PET/CT Scans

The Programa Médico Obligatorio now covers PET/CT and gamma-camera oncology procedures without co-payments, removing a key affordability barrier and expanding access for lower-income populations. Procedure volumes in the Argentina nuclear imaging market are therefore rising at double-digit rates, particularly in provincial hospitals that previously limited advanced imaging due to budget constraints. The policy dovetails with national cancer initiatives that prioritize early detection and standardized follow-up protocols. Equipment utilization rates are climbing, prompting facilities to plan scanner upgrades within three years. Vendors offering flexible service contracts and remote diagnostics gain an edge because public hospitals must balance expanded demand with tight operating budgets.

Private-Sector Investment in Hybrid Imaging Centers

Currency-control reforms in late 2023 streamlined medical device imports, spurring private hospital groups to build dedicated PET/CT and SPECT/CT suites in major cities. These centers target affluent urban patients seeking concierge-style diagnostics and same-day reporting. Higher cash flows allow rapid adoption of AI reconstruction algorithms that cut scan times by up to 30%, lifting daily throughput. The Argentina nuclear imaging market thus benefits from a virtuous cycle of technology refresh and premium pricing. Domestic integrators such as INVAP partner with multinationals to supply turnkey facilities, embedding local support teams that mitigate peso volatility risks for investors.

Growing Oncology Caseload and Precision-Medicine Shift

Argentina recorded 130,878 new cancer diagnoses in 2020 and faces a projected 70% rise in per-capita cancer spending by 2050. This epidemiological pressure drives continuous demand for nuclear imaging in staging, therapy planning, and theranostics. The National Family Cancer Program promotes gene-panel testing that pairs with radiolabeled therapies, deepening tracer utilization. As tertiary centers expand molecular tumor boards, the Argentina nuclear imaging market gains visibility among oncologists who historically defaulted to CT or MRI. Vendors capable of offering both radiopharmaceuticals and cloud-based image analytics are increasingly preferred by multidisciplinary teams.

Installation of Domestic Mo-99 Production Reactor (RA-10)

RA-10 is 80% complete and scheduled for 2026 commissioning, with capacity to supply 20% of global Mo-99 requirements. Domestic isotope output slashes import lead times, stabilizes technetium-99m pricing, and lowers procedure cancellations tied to flight delays. INVAP’s supply agreements with 80 Argentine contractors also stimulate job creation and technology diffusion. Once operational, the reactor will add lutetium-177 production, establishing Argentina as a theranostics exporter to neighboring markets. The Argentina nuclear imaging industry consequently gains strategic autonomy that cushions it from forex volatility and geopolitical supply risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso volatility raising imported device prices | -1.1% | National, affecting all equipment procurement | Short term (≤ 2 years) |

| Short half-life isotope logistics outside Buenos Aires | -0.7% | Provincial hospitals and remote diagnostic centers | Medium term (2-4 years) |

| Skilled technologist shortage in provincial hospitals | -0.5% | Provincial and rural healthcare facilities | Long term (≥ 4 years) |

| Limited reimbursement for cardiac SPECT studies | -0.3% | National, particularly affecting cardiology applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Peso Volatility Raising Imported Device Prices

Roughly 80% of scanners and cyclotrons are sourced abroad and invoiced in U.S. dollars; sharp peso depreciation balloons procurement budgets and prompts payment-term renegotiations. Revised import rules now stagger settlement over four months, straining cash flow for public buyers. Some provincial tenders have been postponed, temporarily tempering the Argentina nuclear imaging market’s equipment refresh pace. Vendors mitigate risk by quoting in pesos at forward-hedged rates or offering operating leases that shift currency exposure onto manufacturers. Local assembly initiatives under discussion could offset volatility over the medium term.

Short Half-Life Isotope Logistics Outside Buenos Aires

Technetium-99m and fluorine-18 decay rapidly, making timely distribution to remote provinces difficult. Flights into Patagonia can be disrupted by weather, extending transport times beyond viable radiochemical purity windows. Consequently, procedure cancellations reach 12% in winter months, constraining provincial scan volumes. Mobile generator technologies and regional cyclotron projects are proposed but remain unfunded. Until RA-10 derived supplies enable broader regional dispatch, geographic inequity will persist in the Argentina nuclear imaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Sustained Equipment Dominance and Isotope Upswing

Equipment accounted for 52.22% of the Argentina nuclear imaging market size in 2025, anchored by 389 SPECT and 42 PET scanners across public and private networks. Hospitals are cycling out first-generation gamma cameras, replacing them with SPECT/CT hybrids that support oncology staging and bone metastasis assessment. Vendors bundle five-year service contracts and AI upgrades, creating predictable cost structures that align with public-budget cycles. Local manufacturer INVAP supplies shielded hot cells and quality-control instruments, capturing niche demand and injecting domestic value into the supply chain.

Radioisotopes, though presently smaller in revenue terms, are forecast to grow at 5.56% CAGR as RA-10 brings molybdenum-99, lutetium-177, and iodine-131 production in-country. Domestic supply eliminates flight-dependent logistics for imported isotopes, lowering costs and spurring utilization, which feeds back into higher tracer demand. Contract manufacturing opportunities emerge for Dioxitek and Tecnonuclear to export surplus isotopes to Chile, Uruguay, and Paraguay. Consequently, the product mix will tilt gradually toward consumables, generating recurring revenue streams and broadening the Argentina nuclear imaging market.

By Application: Cardiology Reigns While Neurology Accelerates

Cardiology retained 58.19% of Argentina nuclear imaging market share in 2025, driven by widespread uptake of SPECT myocardial perfusion imaging in tertiary hospitals. Rising obesity and diabetes prevalence sustains referral volumes, and new F-18 labeled perfusion tracers promise superior accuracy at lower doses. However, reimbursement bottlenecks and alternative CT modalities may temper long-term dominance.

Neurology is set to expand at a 7.78% CAGR through 2031 as dementia screening becomes national public-health policy and alpha-synuclein tracers enter clinical trials. PET imaging with amyloid and tau agents detects preclinical Alzheimer’s disease, enabling timely therapeutic interventions. Provincial memory clinics integrate tele-neurology consults to broaden access, boosting tracer consumption outside Buenos Aires. Oncology, although not the fastest mover, benefits from theranostic rollout, ensuring stable double-digit tracer growth. This evolving mix underscores shifting clinical priorities and technological maturation within the Argentina nuclear imaging market.

By End User: Hospital Supremacy Meets Private-Center Momentum

Hospitals controlled 60.65% of 2025 revenues owing to integrated care pathways and captive inpatient populations. University hospitals serve as referral hubs for complex oncology and neurology cases, anchoring national training programs for technologists and radiopharmacists. Capital-budget allocations, though pressured by fiscal austerity, are partially offset by multilateral loans that earmark oncology equipment procurement.

Diagnostic imaging centers, expanding at 5.93% CAGR, cater to insured middle-income patients who value shorter wait times and premium service. Chain operators deploy aggressive marketing and loyalty programs tied to employer health plans, diverting outpatient demand from public facilities. Many centers co-locate cyclotrons with radiopharmacies, enabling on-site F-18 production that circumvents transport constraints. Academic and research institutes remain niche users but play an outsized role in clinical trials that seed future tracer adoption across the Argentina nuclear imaging market.

Geography Analysis

Buenos Aires Metropolitan Area concentrates nearly 70% of national scanner inventory, supported by dense specialist networks and proximity to isotope distribution nodes at Ezeiza International Airport. Flagship institutions such as Hospital de Clínicas and the Argentine Proton Therapy Centre anchor multimodality oncology programs, driving high daily throughput. Private centers leverage affluent demographics to sustain premium price points and early adoption of AI decision-support tools.

Córdoba and Rosario form secondary hubs, boasting university hospitals that run accredited radiopharmacy programs and host CNEA-funded theranostic trials. These provinces benefit from highway connections that shorten isotope transit times, enabling reliable same-day tracer delivery. Expansion of mobile PET units further spreads access across peri-urban localities.

Northern and southern provinces confront persistent capacity gaps due to sparse populations, challenging terrain, and limited specialist staffing. Technetium-99m generator exchanges occur only twice weekly, constraining scan scheduling flexibility. Telemedicine initiatives and planned mini-cyclotrons aim to shrink disparities, yet funding uncertainties slow deployment. Upon RA-10 start-up, CNEA intends to route isotopes via regional consolidation points, potentially reducing shipping times by up to 30%. As these logistics mature, provincial procedure volumes are expected to rise, broadening the geographic footprint of the Argentina nuclear imaging market.

Competitive Landscape

The competitive arena blends multinational vendors with homegrown nuclear technology firms, yielding a moderately concentrated structure. GE HealthCare, Siemens Healthineers, and Philips supply most hybrid scanners, capitalizing on global R&D pipelines and deep service networks. Collective contracts with top public hospitals cover comprehensive training, uptime guarantees above 98%, and AI add-ons that lock in customer loyalty for multiple upgrade cycles.

Domestic champions INVAP, Dioxitek, and Tecnonuclear specialize in reactor engineering, isotope processing, and radiopharmacy kits, leveraging regulatory familiarity and peso-denominated cost bases to win public tenders. INVAP’s involvement in the RA-10 project cements long-term service agreements, while Dioxitek’s forthcoming lutetium-177 line targets high-margin theranostic demand. Partnerships between global OEMs and local firms create integrated offerings that bundle scanners, generators, and maintenance under unified contracts, smoothing procurement workflows for budget-constrained public buyers.

Strategic moves in 2024-2025 emphasize portfolio integration. Siemens Healthineers’ acquisition of Advanced Accelerator Applications added 13 European PET-tracer plants, signaling intent to replicate end-to-end radiopharmaceutical supply in Latin America. GE HealthCare’s purchase of the remaining stake in Nihon Medi-Physics enhances isotope capabilities in Asia, providing a template for similar expansions in South America. Curium Pharma’s acquisition of Monrol boosts lutetium-177 capacity, aligning with Argentina’s future theranostic demand. These maneuvers intensify competition on the supply side, likely compressing tracer prices once domestic production scales up, to the benefit of the Argentina nuclear imaging market.

Argentina Nuclear Imaging Industry Leaders

GE Healthcare

Siemens AG

Bracco Imaging Spa

Koninklijke Philips N.V.

Canon Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Argentina's Proton Therapy Centre installed 230-tonne cyclotron in Buenos Aires, marking progress toward becoming the first proton therapy facility in the southern hemisphere with testing scheduled for late 2025

- June 2024: Argentina's Nuclear Regulatory Authority (ARN) renewed Atucha 2 operating license until May 2026, following 10-month shutdown for safety improvements and reactor modifications

Argentina Nuclear Imaging Market Report Scope

As per the scope of this report, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. Argentina's Nuclear Imaging Market is segmented by Product (Equipment, Diagnostic Radioisotopes), and Application (SPECT Applications, PET Applications). The report offers the value (in USD million) for the above segments.

By Product

| Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) |

| Thallium-201 (TI-201) | ||

| Gallium (Ga-67) | ||

| Iodine (I-123) | ||

| Other SPECT Radioisotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (RB-82) | ||

| Other PET Radioisotopes | ||

By Application

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

By End User (Value)

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotope | SPECT Radioisotopes | Technetium-99m (TC-99m) | |

| Thallium-201 (TI-201) | |||

| Gallium (Ga-67) | |||

| Iodine (I-123) | |||

| Other SPECT Radioisotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (RB-82) | |||

| Other PET Radioisotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User (Value) | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the projected value of the Argentina nuclear medicine market in 2031?

It is forecast to reach USD 143.45 million, reflecting a 5.33% CAGR over 2026-2031.

How will the RA-10 reactor influence domestic isotope supply?

RA-10 will supply 20% of global molybdenum-99 once operational in 2026, eliminating import reliance and stabilizing tracer costs.

Which application segment is growing fastest?

Neurology leads with a 7.78% CAGR through 2031, driven by rising dementia diagnostics.

Why do private imaging centers gain share against hospitals?

They offer shorter waiting times, advanced AI protocols, and premium services appealing to insured urban patients.

How does peso volatility affect equipment procurement?

Imported scanners are priced in U.S. dollars, so devaluation inflates costs and delays purchasing decisions, particularly for provincial hospitals.

What role does AI play in scan optimization?

Dose-optimization platforms reduce radiation by 25% and increase scanner throughput, improving patient safety and financial returns.

Page last updated on: