Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

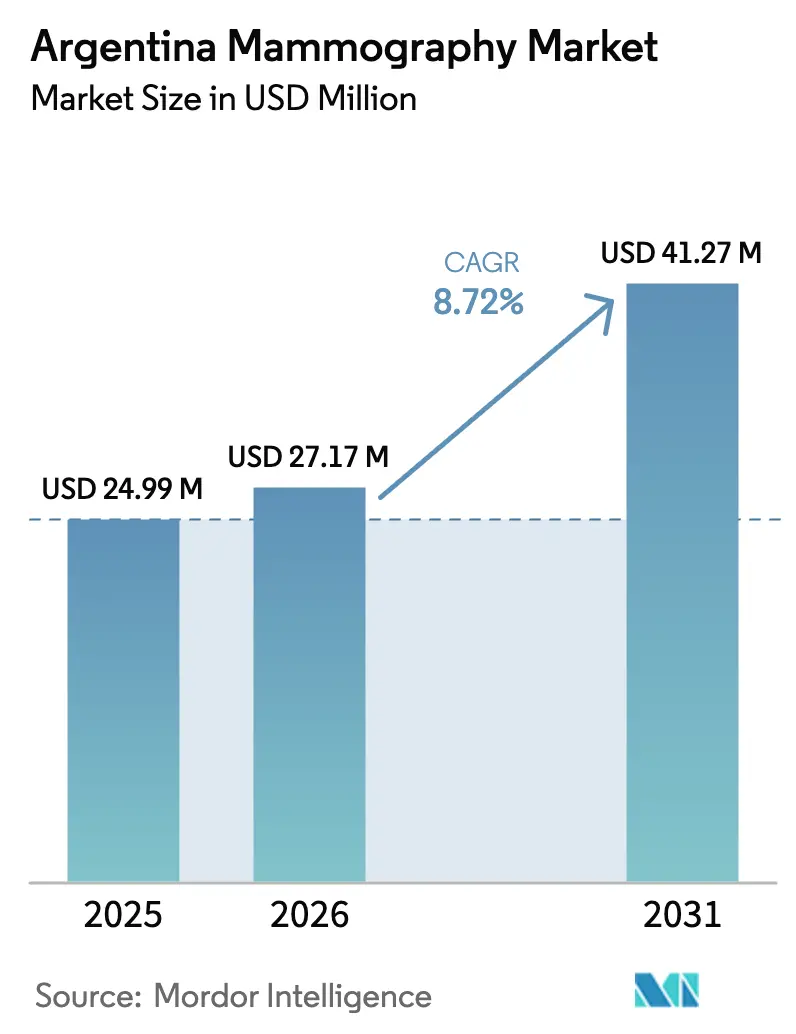

| Base Year Market Size (2025) | USD 24.99 Million |

| Market Size (2026) | USD 27.17 Million |

| Market Size (2031) | USD 41.27 Million |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Mammography Market Analysis by Mordor Intelligence

The Argentina mammography market size was valued at USD 24.99 million in 2025 and estimated to grow from USD 27.17 million in 2026 to reach USD 41.27 million by 2031, at a CAGR of 8.72% during the forecast period (2026-2031). The market’s trajectory reflects Argentina’s urgent goal of lowering breast-cancer mortality—currently the second-highest in Latin America—and the government’s commitment to biennial screening for women aged 50-69, a policy that guarantees recurring demand even within a fragmented health system. Rising adoption of 3-D digital breast tomosynthesis (DBT), mobile screening programs serving rural provinces, and reimbursement reforms that now include advanced imaging are reshaping procurement strategies across public, social-security, and private channels. At the same time, economic volatility, peso devaluation, and customs bottlenecks push many budget-constrained hospitals toward locally refurbished digital units rather than new imports. The competitive landscape remains moderately fragmented; global manufacturers rely on local distributors for after-sales support, while domestic refurbishers leverage currency swings to win cost-sensitive tenders.

Key Report Takeaways

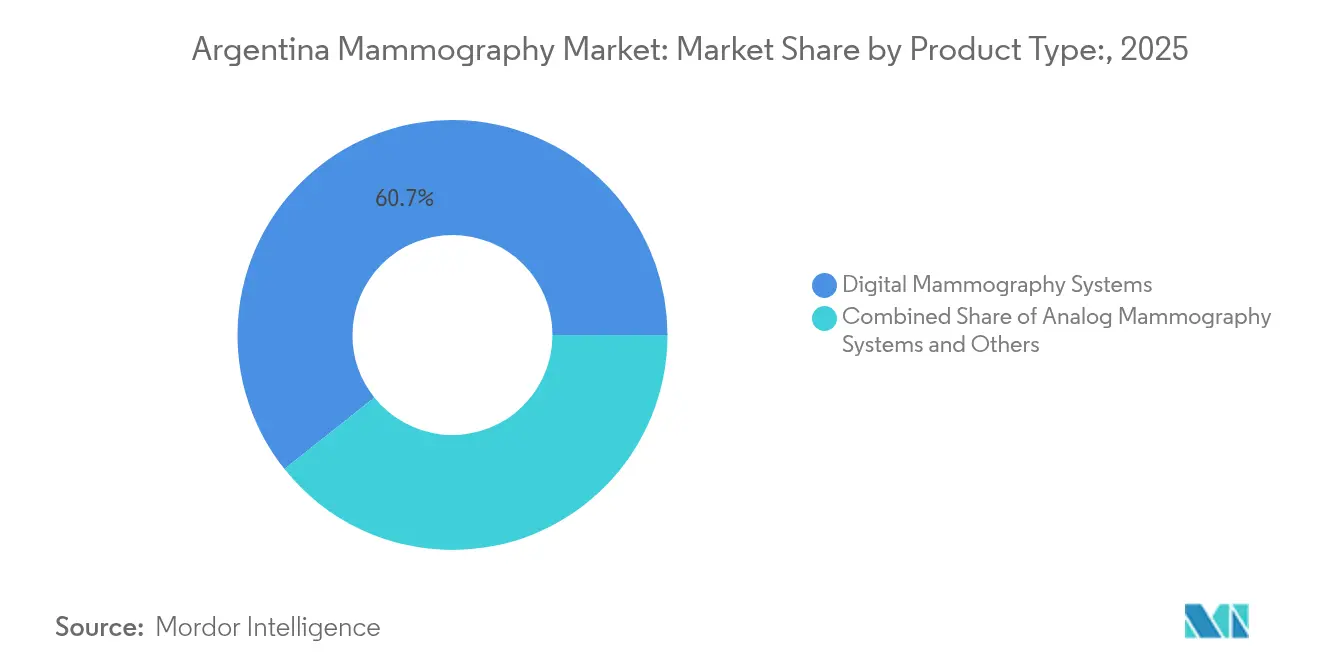

- By product type, digital mammography systems led with 60.72% of Argentina mammography market share in 2025, whereas the “Others” category is forecast to grow at a 9.38% CAGR through 2031.

- By technology, 2-D full-field digital mammography accounted for 54.12% of the Argentina mammography market size in 2025, while 3-D digital breast tomosynthesis is advancing at a 9.68% CAGR to 2031.

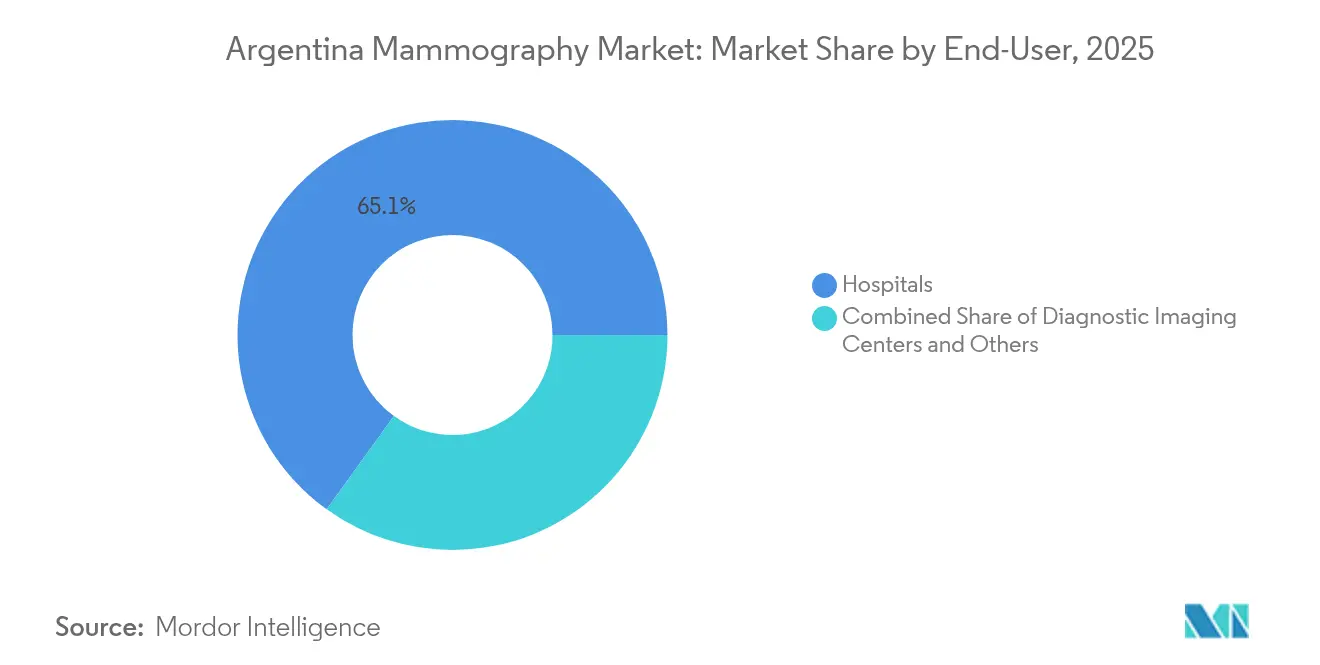

- By end user, hospitals captured 65.05% of the Argentina mammography market size in 2025, yet diagnostic imaging centers are set to expand at a 9.87% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of breast cancer | +2.1% | National; strongest in Buenos Aires, Córdoba, Santa Fe | Long term (≥ 4 years) |

| Technological advancements in digital & 3-D imaging | +1.8% | National; early adoption in Buenos Aires, Mendoza | Medium term (2-4 years) |

| Expansion of national screening program | +1.5% | National; priority for underserved provinces | Long term (≥ 4 years) |

| Reimbursement for DBT | +1.2% | National; concentrated in Buenos Aires, Córdoba | Medium term (2-4 years) |

| Roll-out of mobile units | +0.9% | Northern & Southern rural provinces | Medium term (2-4 years) |

| Currency devaluation favoring refurbished systems | +0.7% | National; strongest in public facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Breast Cancer

Breast cancer incidence in Argentina has reached 73 cases per 100,000 women, while mortality stands at 17.6 per 100,000, making the disease the country’s most prevalent female cancer. Public-health economists estimate that enhanced screening and therapy could avert half of premature cancer deaths and raise national life expectancy by 10 months [1]OECD, “Tackling the Impact of Cancer on Health, the Economy and Society: Argentina,” OECD.ORG. Even after a decade of organized screening, 30% of new cases still present at late stages, underscoring a sizeable gap in diagnostic capacity that keeps hospitals and imaging centers upgrading equipment. Population aging will swell per-capita oncology spending by 70% between 2023 and 2050, reinforcing long-term demand for mammography systems. The concentration of both cancer incidence and medical infrastructure in Buenos Aires and Córdoba magnifies regional equipment needs.

Technological Advancements in Digital & 3-D Imaging

Ten-year clinical evidence shows DBT detects 20-65% more invasive tumors and trims false-positive recalls from 10.6% to 7.2% relative to 2-D studies[2]Radiological Society of North America, “Ten-Year Study Shows Tomosynthesis Improves Breast Cancer Detection,” RSNA.ORG. A dataset of 272,938 screenings reported a 5.3% cancer-detection rate for DBT versus 4.0% for digital mammography, while advanced-stage findings fell sharply. Private clinics in Buenos Aires and Mendoza quickly translated these gains into new procurement cycles, often bundling AI-assisted image-analysis software that lifts detection a further 20%. This technical edge compresses replacement timelines for analog units and establishes new performance baselines influencing both public tenders and private upgrades.

Expansion of National Breast-Cancer Screening Program

Argentina’s National Program for Control of Breast Cancer mandates biennial mammography for women aged 50-69, with public financing to remove cost barriers. Accreditation protocols, staff training, and minimum technical standards embedded in the program direct procurement criteria nationwide. A companion familial-risk initiative broadens eligibility and requires more imaging throughput, especially in provinces with few fixed facilities. Economic evaluations of telemammography show incremental cost-effectiveness ratios comfortably below WHO thresholds for Argentina, encouraging remote-reading networks that amplify equipment utility across vast rural regions. Provincial roll-outs prioritize areas where screening infrastructure was previously minimal.

Reimbursement for DBT Boosting Hospital Demand

The Compulsory Medical Plan now reimburses DBT, lowering financial hurdles to adoption. Private insurers followed suit, converting better diagnostic performance into higher service revenues for hospitals. Because DBT reduces callback rates, administrators also see operational savings that enhance return on investment. These combined incentives accelerate equipment refreshes in Buenos Aires and Córdoba, where competitive hospital markets value diagnostic precision and patient experience.

Roll-Out of Mobile Mammography Units in Rural Provinces

Mobile units are expanding screening coverage among women who rarely access fixed sites; studies show the highest reach in underserved, low-adherence groups. Portable flat-panel detectors matched to truck-based suites deliver higher image quality than earlier computed-radiography set-ups, making mobile services clinically comparable to stationary clinics. Provincial health departments increasingly allocate funds for these units as a fast, scalable answer to geographic disparities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-exposure concerns among patients | -1.3% | Urban, educated populations | Long term (≥ 4 years) |

| High upfront cost of 3-D systems for public hospitals | -2.2% | National public sector | Medium term (2-4 years) |

| Irregular reimbursement cycles in public healthcare | -1.8% | Nationwide public facilities | Short term (≤ 2 years) |

| Import restrictions and customs delays | -1.1% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of 3-D Systems for Public Hospitals

A DBT console can cost USD 85,000-275,000, a formidable outlay for facilities financed by provincial budgets that devote limited capital to high-tech upgrades. Public health spending equals only 2.19% of GDP, and roughly 17 million Argentines remain uninsured, forcing policymakers to prioritize essential services over advanced imaging. Urban-rural resource imbalances further tilt allocations toward Buenos Aires, leaving provincial hospitals dependent on refurbished equipment or donor programs for modernization. As a result, analog and first-generation digital machines persist in many public sites, sustaining a two-tier care environment.

Irregular Reimbursement Cycles in Public Healthcare

Payment delays vary across provinces, with some hospitals waiting months for compensation from Obras Sociales or provincial treasuries, hampering their ability to service loans or pay suppliers. Cash-flow gaps discourage equipment leasing and slow adoption of maintenance contracts, often forcing imaging centers to scale back operating hours or postpone preventive service, undermining screening targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Systems Drive Market Modernization

Digital platforms held 60.72% of Argentina mammography market share in 2025, reflecting decisive migration away from analog units. Hospitals and imaging centers underscore the clinical benefits of higher resolution and lower radiation, while software upgrades extend equipment life cycles. Analog machines remain common in smaller provincial hospitals but continue to lose ground as refurbished digital units become affordable during currency swings. The “Others” category—including contrast-enhanced mammography and breast-specific gamma imaging—records the fastest CAGR at 9.38%, suggesting experimentation beyond traditional x-ray modalities. Regulatory hurdles from ANMAT, such as Spanish-language labeling and certificate-of-free-sale requirements, raise entry barriers, favoring vendors with established local partners. Portable digital detectors, fitted into mobile vans serving remote provinces, demonstrate superior diagnostic yield compared with older computed-radiography plates, fostering a parallel mobile-screening market.

Locally refurbished digital systems satisfy budget constraints for many public hospitals, providing compliant image quality without the premium price of new imports. Currency devaluation amplifies this value proposition and sustains a domestic refurbishment ecosystem that refurbishes, certifies, and services units originally sourced from high-income markets.

By Technology: 3-D Tomosynthesis Reshapes Diagnostic Standards

Full-field digital mammography still commands 54.12% of Argentina mammography market size, but 3-D DBT is outpacing every other technology at a 9.68% CAGR thanks to its demonstrable jump in invasive cancer detection. Hospitals and private clinics cite reductions in false positives and callbacks as central to the upgrade business case. Reimbursement now includes DBT, which reinforces provider interest and accelerates replacement cycles. AI algorithms layered on DBT datasets raise detection sensitivity further, shortening reading times and offsetting Argentina’s radiologist shortage.

Phase-contrast and spectral mammography hold niche roles, particularly in evaluating dense breast tissue. Although current uptake is modest, their potential to visualize micro-calcifications without contrast may open incremental opportunities for vendors specializing in research hospitals and high-risk clinics. All vendors stress interoperability with PACS and cloud archives, ensuring seamless integration with national telemammography pilots that extend specialist readings to remote centers.

By End-User: Hospitals Dominate Amid Diagnostic-Center Growth

Hospitals controlled 65.05% of Argentina mammography market share in 2025 because they offer screening, biopsy, and oncology services under one roof. Yet diagnostic imaging centers are growing fastest at 9.87% CAGR, propelled by private investment and patient demand for shorter wait times. These centers operate lean cost structures and longer service hours, making them attractive to women balancing work and family obligations.

Mobile units and telemedicine platforms form the “Others” end-user segment and are vital for rural outreach. Studies confirm mobile vans do not cannibalize fixed-site volumes; instead they capture patients who would otherwise skip screening, lifting overall system throughput. Telemammography networks link these vans to specialists in metropolitan hospitals, overcoming workforce shortages and ensuring diagnostic consistency.

Geography Analysis

Buenos Aires province generates the largest share of mammography procedures and capital purchases, fueled by its dense population and concentration of public and private hospitals. Premier institutions such as the Breast Center Institute integrate genetic counseling and early-detection outreach, reinforcing demand for high-end 3-D systems. Despite resource depth, public-sector patients still face median treatment delays of 76 days versus 60 days in private facilities, reflecting systemic fragmentation.

Córdoba, Santa Fe, and Mendoza provinces form the second tier of demand. Provincial health authorities are investing in new public imaging suites, and private hospital chains deploy 3-D systems to differentiate services. Córdoba’s Society of Breast Pathology illustrates localized professional ecosystems that sustain equipment upgrades and training. Santa Fe’s industrial base enables employer-funded insurance schemes that boost private screening volumes, while Mendoza’s cross-border patient flows from Chile add incremental utilization.

Northern and Southern regions, characterized by vast rural areas and limited fixed infrastructure, rely heavily on mobile screening programs. Provincial governments partner with NGOs and private donors to finance vans equipped with portable digital detectors. Tele-reading centers in Buenos Aires provide off-site interpretation, which reduces staffing barriers and stabilizes diagnostic quality in sparsely populated provinces.

Competitive Landscape

Argentina’s mammography equipment market is moderately fragmented. Hologic, GE Healthcare, and Siemens Healthineers capture premium segments with 3-D DBT portfolios, AI toolkits, and multi-year service contracts. Hologic’s Genius 3-D platform, for instance, reports 20-65% higher invasive-cancer detection, a statistic that resonates with oncologists and payers [3]Hologic, “2023 Sustainability Report,” HOLOGIC.COM. Samsung Medison and Planmed compete on modular designs and lower price points aimed at mid-tier private clinics.

Currency volatility grants domestic refurbishers a comparative cost advantage. By sourcing pre-owned digital units from North America or Europe, upgrading detector panels, and providing local service, these firms deliver 30-40% savings relative to new imports. Public hospitals tend to favor such offerings because procurement cycles are delayed by reimbursement uncertainty and import licensing backlogs.

Service capabilities now rank alongside technology in purchasing criteria. Manufacturers offer uptime guarantees, remote diagnostics, and staff-training packages to mitigate operational disruptions from reimbursement delays. The Chamber of Medical Diagnostic Institutions (CA.DI.ME.) sets voluntary maintenance standards, and compliance often influences tender outcomes. White-space opportunities remain in mobile screening, where equipment vendors can bundle financing, vans, and tele-reading platforms into turnkey solutions for provincial health ministries.

Argentina Mammography Industry Leaders

Siemens AG

GE Healthcare

Fujifilm Holdings Corporation

Hologic Inc.

Planmed OY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Pro Mujer, Mamotest, and the Avon Foundation funded 40 free mammograms in Roque Sáenz Peña, Chaco, advancing rural screening capacity.

- May 2023: Johnson & Johnson Impact Ventures invested in Mamotest to scale telemammography operations across Argentina and Mexico.

Argentina Mammography Market Report Scope

Mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer.

Argentina's mammography market is segmented by product type (digital systems, analog systems, breast tomosynthesis, and other product types) and end-users (hospitals, specialty clinics, and diagnostic centers). The report offers the value (USD) for the above segments.

By Product Type

| Digital Mammography Systems |

| Analog Mammography Systems |

| Others |

By Technology

| 2-D Full-Field Digital Mammography (FFDM) |

| 3-D Digital Breast Tomosynthesis |

| Phase-Contrast & Spectral Mammography |

By End-User

| Hospitals |

| Diagnostic Imaging Centers |

| Others |

| By Product Type | Digital Mammography Systems |

| Analog Mammography Systems | |

| Others | |

| By Technology | 2-D Full-Field Digital Mammography (FFDM) |

| 3-D Digital Breast Tomosynthesis | |

| Phase-Contrast & Spectral Mammography | |

| By End-User | Hospitals |

| Diagnostic Imaging Centers | |

| Others |

Key Questions Answered in the Report

How big is the Argentina Mammography Market?

The Argentina Mammography Market size is expected to reach USD 27.17 million in 2026 and grow at a CAGR of 8.72% to reach USD 41.27 million by 2031.

Which product category leads current sales?

Digital mammography platforms hold 60.72% of 2025 sales value.

Who are the key players in Argentina Mammography Market?

Siemens AG, GE Healthcare, Fujifilm Holdings Corporation, Hologic Inc. and Planmed OY are the major companies operating in the Argentina Mammography Market.

Why are diagnostic imaging centers growing faster than hospitals?

Private investment, extended opening hours, and shorter wait times give imaging centers a 9.87% CAGR forecast.

Page last updated on: