Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

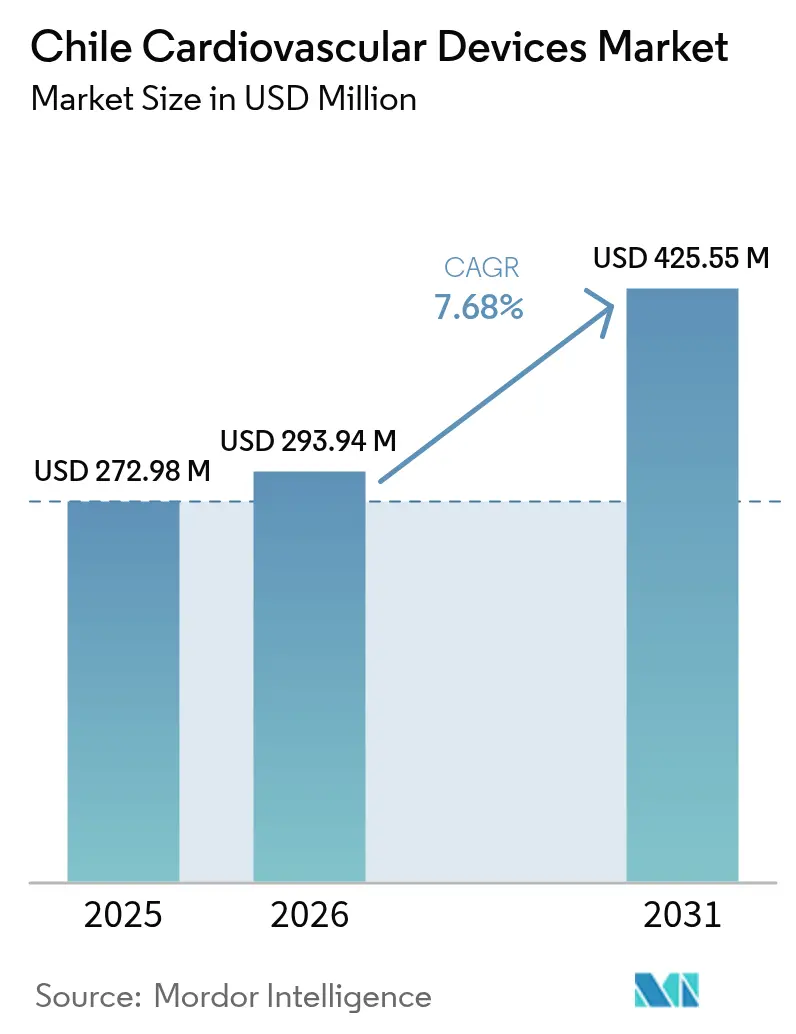

| Base Year Market Size (2025) | USD 272.98 Million |

| Market Size (2026) | USD 293.94 Million |

| Market Size (2031) | USD 425.55 Million |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

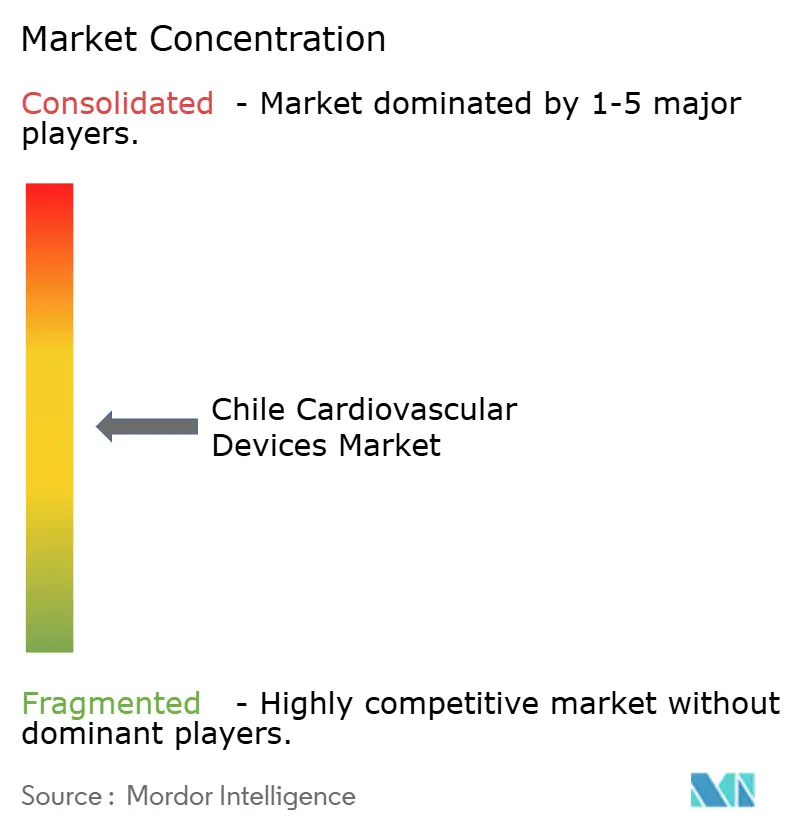

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Cardiovascular Devices Market Analysis by Mordor Intelligence

The Chile cardiovascular devices market size was valued at USD 272.98 million in 2025 and estimated to grow from USD 293.94 million in 2026 to reach USD 425.55 million by 2031, at a CAGR of 7.68% during the forecast period (2026-2031). Its expansion reflects the government-led National Cardiovascular Health Program, which channels higher budgets toward device procurement in public hospitals while simultaneously supporting telemedicine rollouts that shorten diagnostic times for acute coronary events. Uptake is strongest for therapeutic and surgical devices as FONASA hospitals upgrade catheterization labs, yet diagnostic and monitoring innovations are gaining momentum because remote regions such as Patagonia now transmit more than 50,000 ECGs each month over the national tele-cardiology grid. Mandatory ISAPRE coverage for cardiac implants, introduced in 2023, has removed out-of-pocket barriers for roughly 15% of the population, accelerating elective pacemaker and CRT procedures in private clinics. Multinational suppliers face an uneven reimbursement landscape and currency volatility, prompting partnerships with local networks like RedSalud to stabilise distribution and after-sales support.

Key Report Takeaways

- By device type, therapeutic and surgical devices led with 68.73% revenue share in 2025; diagnostic and monitoring devices are projected to expand at an 8.63% CAGR through 2031.

- By application, coronary artery disease captured 47.12% share of the Chile cardiovascular devices market size in 2025; structural heart disease treatments are advancing at an 8.42% CAGR through 2031.

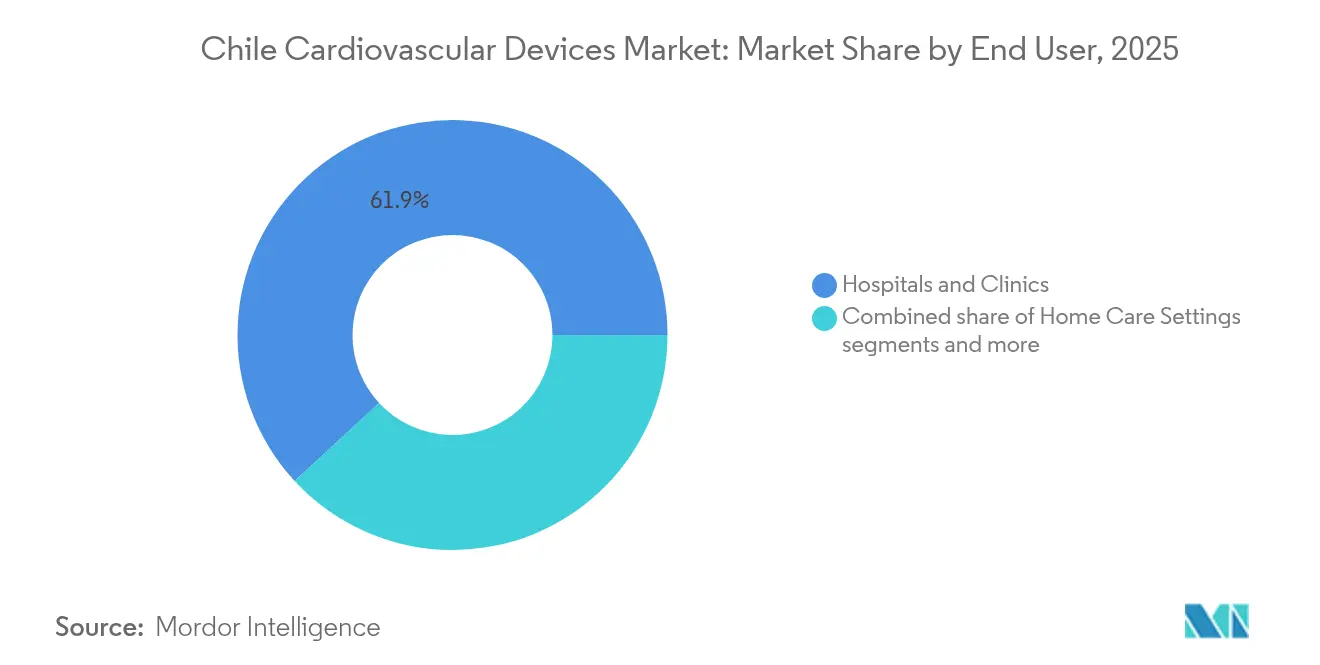

- By end user, hospitals and clinics held 61.88% of the Chile cardiovascular devices market share in 2025, while home care settings and remote monitoring platforms are projected to grow at a 8.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government’s National Cardiovascular Health Program expanding device procurement in public hospitals | +1.1% | National, higher impact in public hospitals | Medium term (2–4 years) |

| Rising prevalence of ischemic heart disease linked to dietary transitions in urban Chile | +0.9% | Urban regions (Santiago, Valparaíso, Concepción) | Long term (≥ 4 years) |

| Mandatory Private Health Insurance (ISAPRE) coverage expansion for cardiac implants effective 2023 | +0.8% | Private sector beneficiaries nationwide; strongest in major urban centers | Short to medium term (≤ 3 years) |

| Growth of local interventional cardiology centers accredited for TAVI procedures | +0.7% | Accredited tertiary centers in Santiago and leading regional hubs | Medium term (2–4 years) |

| Increasing medical tourism from neighboring Pacific Rim countries for cardiac surgery in Santiago | +0.5% | Metropolitan Santiago; select high-complexity private hospitals | Medium term (2–4 years) |

| Tele‑cardiology adoption in remote Patagonia fueling demand for connected monitoring devices | +0.4% | Southern and remote regions (Patagonia, Aysén, Magallanes); rural networks | Short to medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Ischemic Heart Disease Linked to Dietary Transitions in Urban Chile

Food-environment studies in Santiago show that low-income boroughs with limited access to fresh produce register higher ischemic heart-disease rates than wealthier districts, a disparity persisting despite the front-of-pack labelling law. Consequently, coronary interventions remain the largest application within the Chile cardiovascular devices market, pushing hospitals to increase inventories of drug-eluting stents and balloon catheters. Wearable blood-pressure cuffs and portable ECG recorders are also proliferating as community clinics deploy them for primary-prevention campaigns. Device makers leverage these urban programmes to pilot AI-powered analytics that flag arrhythmogenic patterns before symptom onset, broadening preventive care.

Mandatory Private Health Insurance (ISAPRE) Coverage Expansion for Cardiac Implants Effective 2023

ISAPRE beneficiaries now receive reimbursement for pacemakers, CRT devices and implantable defibrillators, lifting procedure volumes in private hospitals by double-digit percentages during 2024[1]Source: Bupa, “Annual Report 2023,” bupa.com . Suppliers initially recorded stronger sales but must navigate a Supreme Court ruling that caps premium adjustments using risk-factor tables, a shift that could compress margins on high-end implants. Nevertheless, the policy continues to draw patients from public waitlists into private suites, underpinning forecast growth in the Chile cardiovascular devices market during the next two years.

Growth of Local Interventional Cardiology Centers Accredited for TAVI Procedures

Hospitals accredited for transcatheter valve work have expanded beyond Santiago, with Valparaíso facilities now performing TAVI under multidisciplinary heart teams. The milestone first robotic-assisted TMVR procedure in March 2025 showcases Chilean competence in structural-heart innovation. Such credentials attract device trials and medical tourists, enabling centres to negotiate favourable consignment terms with multinationals. These hubs also require high-resolution imaging systems and dedicated ICU monitoring, spurring cross-category equipment purchases.

Government’s National Cardiovascular Health Program Expanding Device Procurement in Public Hospitals

Public hospitals that serve 80% of Chileans through FONASA have received ring-fenced allocations for cath-lab upgrades, imaging consoles and device replenishment. Procurements align with the HEARTS Pharmacy rollout that standardises blood-pressure checks and improves hypertension adherence, thereby broadening the installed base for ambulatory monitors. The plan’s staged implementation across 187 communes shields spending from election cycles, giving vendors multi-year visibility. As a result, the Chile cardiovascular devices market now sees higher volumes of therapeutic stents and implantable rhythm devices entering public tenders. Digital platforms linked to FOFAR medicine stockpiles further sustain demand for point-of-care monitors that integrate with pharmacy data feeds

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Reimbursement for Next-Generation Bioabsorbable Stents by FONASA | -0.7% | National, with higher impact in public hospitals | Medium term (2-4 years) |

| Peso Volatility Driving Up Import Costs for High-End Implantables | -0.5% | National, with higher impact on premium device segments | Short term (≤ 2 years) |

| Fragmented Public Tender Cycles Causing Procurement Delays Beyond 12 Months | -0.4% | National public healthcare system | Medium term (2-4 years) |

| Shortage of Trained Electrophysiologists Outside Santiago Limiting Device Utilization | -0.3% | All regions except Metropolitan Santiago | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Next-Generation Bioabsorbable Stents by FONASA

While GES guarantees cover acute myocardial-infarction treatment, hospital budgets rarely stretch to the price premium on absorbable scaffolds, constraining penetration to private payers. The resulting supply imbalance limits scale efficiencies, keeping per-unit costs high and delaying broader uptake across the Chile cardiovascular devices market. Clinicians advocate for cost-effectiveness reviews, yet funding cycles suggest only gradual policy relaxation over the next four years.

Peso Volatility Driving Up Import Costs for High-End Implantables

Device invoices are largely denominated in USD or EUR, exposing hospitals to exchange swings that can widen tender budgets by double digits within months. Some facilities postpone orders for CRT and ICD systems, while distributors hedge currency movements at added cost. The squeeze is most acute for niche devices such as ventricular assist pumps, which lack domestic substitutes. Consequently, premium-segment growth within the Chile cardiovascular devices market decelerates whenever the peso weakens sharply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Innovations Reshape Care Delivery

Chile cardiovascular devices market leadership by therapeutic and surgical equipment remains intact, yet diagnostics are closing the gap as tele-cardiology matures. In value terms, diagnostic and monitoring devices will outpace the broader market at an 8.63% CAGR through 2031, leveraging the national network that analyses more than 50,000 ECGs monthly. Portable recorders and AI-enabled wearables feed real-time data to cardiology hubs, reducing STEMI mortality from 12% to 8.6% since 2024.

Therapeutic and surgical systems accounted for 68.73% of the Chile cardiovascular devices market size in 2025, underscoring enduring demand for drug-eluting stents and rhythm-management implants. Uptake is amplified by ISAPRE reimbursement, especially for CRT-P devices that restore ventricular synchrony in heart-failure cohorts. Robotic TMVR cases in Santiago now demonstrate feasibility for fully percutaneous mitral repair, widening indications and seeding demand for advanced valve prostheses. Nevertheless, currency swings elevate import costs, prompting hospitals to consolidate purchases under multi-year tenders tied to peso hedges.

By Application: Structural Heart Interventions Gain Momentum

Coronary artery disease retained 47.12% of the Chile cardiovascular devices market share in 2025 on the back of persistent ischemic burden in urban centres. Public-hospital stent volumes climbed after GES enhancements guaranteed quicker door-to-balloon times, yet private clinics still perform most elective PCI work.

Structural-heart procedures are the fastest-growing application, with an 8.42% CAGR outlook to 2031, driven by ageing demographics and improved screening that flags valve degeneration earlier. The 2025 first-in-human robotic TMVR success eliminated severe regurgitation in non-surgical candidates and signals a step-change in minimally invasive therapy options. Chile’s participation in multinational TMVR studies positions local investigators to access investigational devices ahead of formal approvals, giving Santiago centres a regional edge.

By End User: Home Care Settings Disrupt Traditional Models

Hospitals and clinics still controlled 61.88% of the Chile cardiovascular devices market size in 2025, reflecting entrenched referral patterns and complex procedure capabilities. New rural clinics funded under the Universal Primary Healthcare Coverage and Resilience plan are adding tele-ICU bays, further anchoring institutional demand.

Yet home care and remote monitoring represent the system’s fastest-expanding frontier at a 8.98% CAGR. Adoption of the Mi Salud-APS app shows that 64.6% of enrolled patients actively transmit vitals, freeing hospital capacity and enabling earlier intervention for rhythm anomalies. Smart textiles and subcutaneous biosensors now feed cloud dashboards, prompting AI algorithms to flag decompensation in heart-failure patients well before symptoms escalate. Vendors that bundle devices with data analytics services are capturing annuity streams that dampen revenue cyclicality.

Geography Analysis

Santiago’s Metropolitan Region commands the bulk of device revenue, hosting Chile’s densest cluster of cath labs and nearly all electrophysiology fellowships. Hospital Clínico Universidad Católica anchors innovation, having executed Latin America’s first robotic-assisted TMVR in March 2025, and its procurement cycles often serve as bellwethers for the Chile cardiovascular devices market. Local distributors maintain just-in-time inventories in the capital, ensuring same-day access to stents and pacing leads.

Valparaíso and Bío Bío regions form the secondary axis for growth. Their regional hospitals receive priority HEARTS Pharmacy deployments that integrate pharmacists into longitudinal hypertension care, stimulating orders for ambulatory BP monitors and single-use catheters. Tele-ICU links between these centres and Santiago offset specialist shortages and expand surgical backlogs for structural-heart cases.

Remote Patagonia illustrates tele-medicine’s transformative role: cold-chain drones deliver electrodes while satellite broadband uploads ECGs from clinics near Punta Arenas. Portable defibrillators ruggedised for sub-zero field use are now standard kit for ambulance crews, and RedSalud’s February 2025 tele-cardiology platform routes device diagnostics to Santiago-based electrophysiologists in seconds. By contrast, mining hubs in Antofagasta demand occupational-screening ECG trailers to mitigate arrhythmia risks linked to particulate exposure, sustaining niche volumes for high-capacity Holter systems.

Regulatory Landscape

Chile regulates cardiovascular devices through the health authority Instituto de Salud Publica (ISP) and the Ministry of Health (MINSAL), under the Codigo Sanitario framework and implementing decrees. A key 2026 anchor is Exempt Decree No. 25 (published March 2026), which expanded the mandatory sanitary control regime by adding 39 categories of medical devices and IVDs under Article 111 of the Health Code. The added list includes high-risk cardiovascular products such as pacemakers, defibrillators, heart valves, stents, and cardiovascular catheters.

For products not yet in the mandatory registration list, or when registration is not required, importation can use a Customs Destination Certificate (CDA) processed through the GICONA 2.0 electronic platform. For registered devices, import and post-market control follow ISP requirements. For drug-device combinations used in cardiology, the pathway depends on the primary mode of action: device-led combinations are handled under medical device provisions (for example, Decree No. 825), while integrated products governed as pharmaceuticals follow Decree No. 3, making early classification decisions a practical step for market access planning.

Value Chain Analysis

The value chain is import-centric. Multinational manufacturers supply finished cardiovascular devices into Chile through local authorized representatives and distributors that manage ISP-facing compliance, customs clearance, warehousing, and hospital support. Regulatory changes in 2026 affect upstream documentation and importer readiness, as Exempt Decree No. 25 expanded mandatory sanitary control to additional high-risk cardiovascular categories and increases the need for technical file preparation, quality-system evidence, and local technovigilance workflows to keep supply continuity.

Downstream demand is driven by public and private purchasing channels. Public volumes flow through FONASA-linked hospitals and procurement mechanisms such as CENABAST tenders, with coverage frameworks, including GES for priority conditions, shaping utilization across coronary and acute care pathways. Private clinics serving ISAPRE beneficiaries contribute materially to implantable rhythm management and elective interventions, while provider networks and hospital groups act as consolidators that can negotiate consignment, training, and service-level commitments from global OEMs and their Chilean distribution partners.

Competitive Landscape

Abbott, Boston Scientific and Edwards Lifesciences anchor the premium segment with full-line portfolios and service engineers stationed in the capital. Market entry barriers include the need for local studies; therefore, multinationals fund fellowship programmes that familiarise surgeons with their platforms.

AI integration has become the new battleground. GE HealthCare’s cloud-linked sensors automate ward surveillance, while start-ups such as Capstan Medical leverage robotic precision to shorten valve-deployment times[2]Source: Capstan Medical, “Robotic-Assisted TMVR First-in-Human,” citoday.com .

Partnership strategies dominate: RedSalud grants suppliers exclusivity in return for volume rebates across its 55-facility network, whereas public-sector bids reward local assembly value-addition, nudging global firms toward contract manufacturing in Santiago. Competitive intensity remains moderate; however, impending policy shifts around ISAPRE solvency could rearrange private-sector purchasing power and spark consolidation among distributors.

Chile Cardiovascular Devices Industry Leaders

Boston Scientific Corporation

Phillips Healthcare

Medtronic PLC

Siemens Healthineers AG

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The March 2026 publication of Exempt Decree No. 25, which brought additional high-risk cardiovascular categories (including pacemakers, defibrillators, heart valves, stents, and cardiovascular catheters) into mandatory sanitary control with defined compliance timelines, creates a window for structured market-access programs. Companies that arrange early ISP submissions, local importer authorization, and post-market surveillance capabilities during the transition can improve continuity in tender eligibility and reduce authorization gaps for implantable and interventional portfolios.

Remote diagnostics and connected monitoring are a practical whitespace area. Chile already transmits more than 50,000 ECGs per month through the national tele-cardiology grid, and the Mi Salud-APS model indicates high patient participation in vital-sign transmission. This operating base supports opportunities for interoperable remote cardiac monitors, AI-assisted triage software, and service-layer offerings that bundle devices with data workflows for public networks and private provider groups. A second, evidence-backed avenue is clinical capability expansion in structural heart, where Chilean centers have demonstrated advanced procedures such as the first robotic-assisted TMVR in March 2025, reinforcing demand for compatible imaging, cath-lab infrastructure, and specialized disposables tied to valve and transcatheter programs.

Recent Industry Developments

- June 2026: Boston Scientific launched the OPAL HDx Faraview mapping system in Chile and reported first clinical procedures at Hospital Clinico Regional Dr. Guillermo Grant Benavente in the Bio Bio region. The introduction expands local access to advanced EP mapping capabilities outside Santiago and supports adoption of higher-complexity ablation workflows that drive recurring catheter and mapping consumable demand.

- March 2025: Hospital Clinico Universidad Catolica performed Latin Americas first robotic-assisted TMVR, eliminating severe mitral regurgitation in two high-risk patients. The milestone strengthens Chilean structural heart credentials and increases requirements for complementary imaging, valve technologies, and peri-procedural monitoring systems at tertiary centers.

- February 2025: RedSalud launched a nationwide tele-cardiology program that enables remote pacemaker interrogation and ICD parameter adjustment. The rollout increases utilization of connected cardiac rhythm management ecosystems and reinforces the need for secure data connectivity, service support, and device fleets compatible with remote follow-up.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Chile cardiovascular devices market covers medical devices used to diagnose, monitor, and treat heart and blood vessel conditions. Coverage includes use in hospitals, clinics, and home care settings, and the market is measured in revenue terms in USD.

Scope exclusions: we exclude pharmaceuticals, purely software-only tools, and routine hospital services that are not sold as cardiovascular device products.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia & Conduction Disorders

- Heart Failure & Cardiomyopathy

- Structural & Congenital Heart Defects

- Peripheral Vascular Disease

- By End User

- Hospitals & Clinics

- Home Care Settings

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand environment in Chile, and then checking where device purchasing typically appears in public data. We reference sources such as Chile's Ministry of Health publications, the National Institute of Statistics (INE) for population and aging trends, OECD health indicators, and World Bank macro series to set realistic baselines for care access and spending.

On the supply and availability side, we review Chilean customs trade statistics where relevant, along with publications from medical and cardiology societies, peer-reviewed clinical journals for procedure trends, and public procurement notices. We also use company filings, investor presentations, and reputable press to confirm product mix changes and pricing direction, and we use a paid subscription for company financials plus a patent database to cross-check innovation and portfolio shifts. These desk sources are illustrative only, and many other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary discussions are used to pressure-test assumptions that are hard to see in public data, especially for procedure mix, replacement cycles, and channel markups. We spoke with manufacturers and distributors, hospital procurement staff, cath lab and OR stakeholders, and clinical specialists so the demand signals and the supply view could be reconciled. Since this is a single-country market, coverage was balanced across major urban care settings and secondary centers to reflect how adoption and pricing can vary inside Chile.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 35% | |

| Smaller Players: 14% | Managers: 53% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up blend. The top-down side is anchored on a treated-patient and procedure demand pool across key cardiovascular interventions and diagnostics, which is then translated into device revenue using adoption and pricing assumptions. To keep the totals grounded, we add selective bottom-up checks using supplier and distributor revenue patterns, sample average selling price (ASP) by device category, and volume sanity checks from channel feedback.

Model inputs that move the results in practical ways include cardiology procedure volumes, such as interventional cases and rhythm management implant activity, penetration of newer therapies like transcatheter valve approaches, device replacement and follow-up utilization in monitoring, public versus private hospital mix, and observed ASP movement by imported versus locally distributed products. Where a direct volume signal is weak, we use proxy indicators such as cath lab capacity expansion, utilization comments from interviews, and import value direction, then narrow the range through expert re-checks.

For forecasting, scenario analysis is used so the model reflects how reimbursement focus, hospital capex cycles, and adoption speed of higher-value devices affect the next years. Assumptions are not carried forward mechanically. Instead, they are updated based on what respondents expect for pricing, tender behavior, and procedure growth before the final curve is locked.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, then reviewed for variances that do not fit what the care pathway would imply. When an estimate sits outside a reasonable band, we re-check the driver chain, revisit the pricing logic, and re-contact sources if the variance remains difficult to explain.

Before sign-off, the model goes through a multi-step analyst review so key assumptions, conversions, and category totals are consistent and traceable. Reports are refreshed annually, and interim updates are made when material events occur, such as policy shifts, major tender outcomes, or sharp currency moves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Chile Cardiovascular Devices Market Size Compared With Other Published Estimates

Published values for Chile cardiovascular devices often do not match because each study draws the market boundary differently and applies its own timing for prices, currency conversion, and adoption rates. In our work, we keep the estimate explainable from the demand side, then use real-world pricing and channel feedback to keep it realistic.

A common gap driver is how quickly ASPs are refreshed and which exchange-rate timing is used when imported devices dominate the basket. The model is also shaped by whether procedure growth is treated as steady or accelerated after capacity additions. By updating pricing inputs and FX timing closer to the base year and re-validating the implied volumes with channel checks, Mordor Intelligence reduces drift that can happen when older price points and one-time assumptions are carried forward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 272.98 M (2025) | |

| Global Consultancy A | USD 240.00 M (2024) | Uses a different base year and appears to apply broader averaging on pricing and growth, which can understate recent ASP increases and the impact of newer, higher-value therapies. |

| Industry Publisher B | USD 152.30 M (2025) | Likely applies a narrower product basket or more conservative inclusion for premium implantables, and the higher growth rate suggests aggressive adoption assumptions that can shift the starting-year total downward. |

The spread is mainly explained by timing and scope choices, followed by how pricing and adoption are refreshed year to year. By linking the market to procedure-led demand, updating ASP and FX assumptions to the base year, and then re-checking the totals with channel feedback, the final number stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the Chile cardiovascular devices market?

The Chile cardiovascular devices market size is USD 293.94 million in 2026 and is expected to reach USD 425.55 million by 2031 at a 7.68% CAGR

Which device category is expanding the fastest?

Diagnostic and monitoring devices show the quickest growth, projected to log an 8.63% CAGR through 2031 as tele-cardiology services proliferate.

Why are structural-heart interventions gaining momentum in Chile?

Robotic TMVR success and wider accreditation for TAVI centres are enabling minimally invasive procedures for ageing patients, driving an 8.42% CAGR in the structural-heart segment.

How does telemedicine influence device demand in remote areas?

Monthly analysis of more than 50,000 ECGs and widespread use of the Mi Salud-APS app create sustained demand for connected monitors that transmit real-time data to urban specialists.

Page last updated on: