Global Anxiety Disorders And Depression Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.8 Billion |

| Market Size (2031) | USD 30.49 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Anxiety Disorders And Depression Treatment Market Analysis by Mordor Intelligence

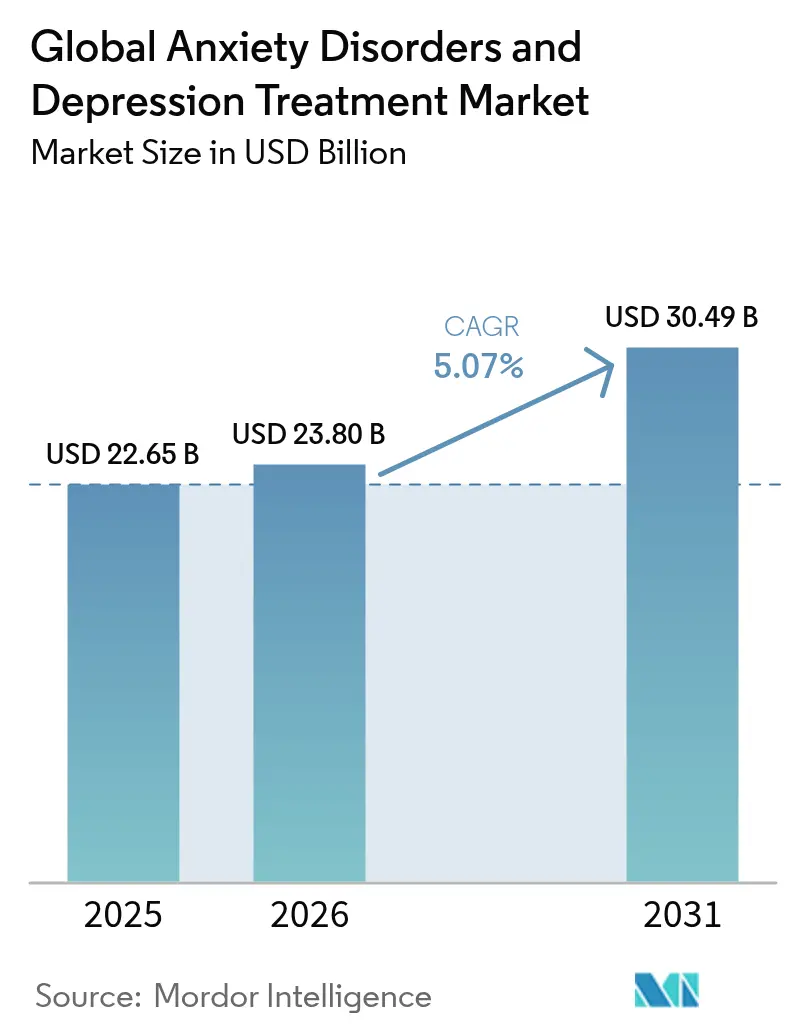

The Anxiety disorder and depression treatment market size is expected to grow from USD 22.65 billion in 2025 to USD 23.8 billion in 2026 and is forecast to reach USD 30.49 billion by 2031 at 5.07% CAGR over 2026-2031. Growth is propelled by accelerating mental-health awareness, recent U.S. FDA rules that open over-the-counter (OTC)[1]Source: U.S. Food and Drug Administration, “Nonprescription Drug Product Additional Condition for Nonprescription Use,” fda.gov pathways for select SSRIs, and landmark approvals covering digital therapeutics and psychedelic-assisted therapies. AI-driven adherence platforms, rising adoption among younger demographics, and geriatric demand for safer formulations further support volume expansion. Meanwhile, rapid-acting NMDA antagonists and neuroplastogens challenge the dominance of monoamine-based drugs, while value-based pricing and mental-health parity rules reshape revenue models in key markets.

Report Key Takeways

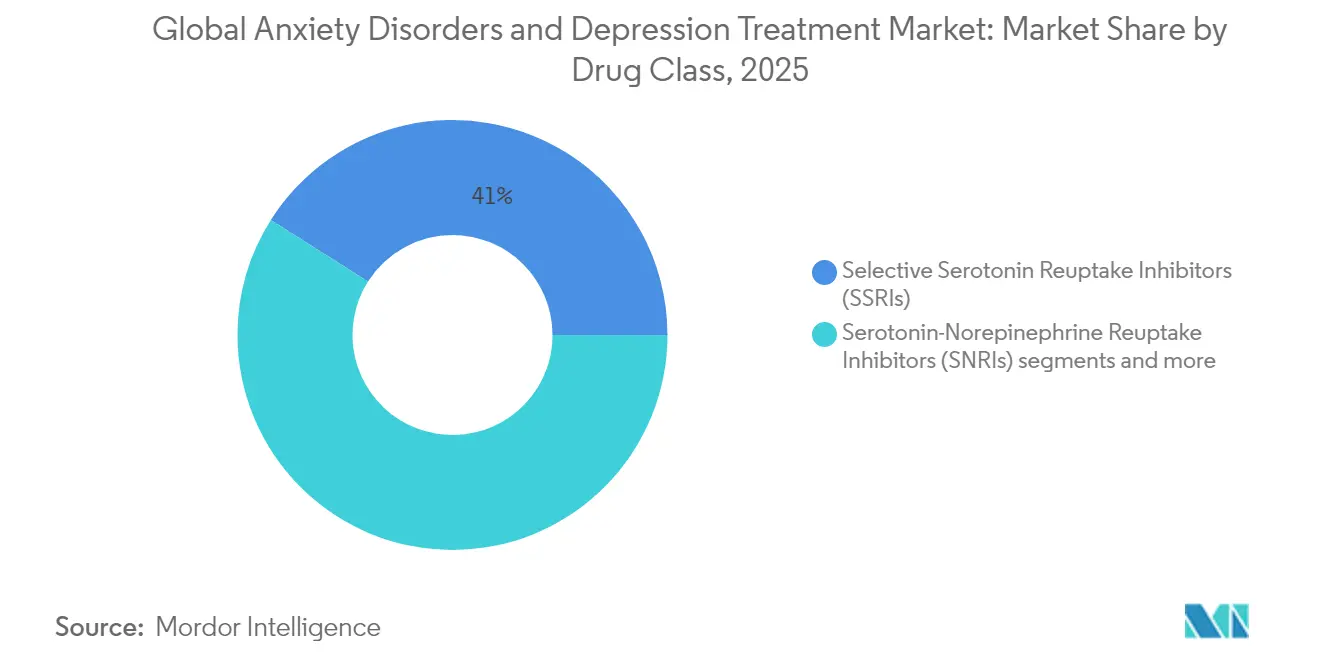

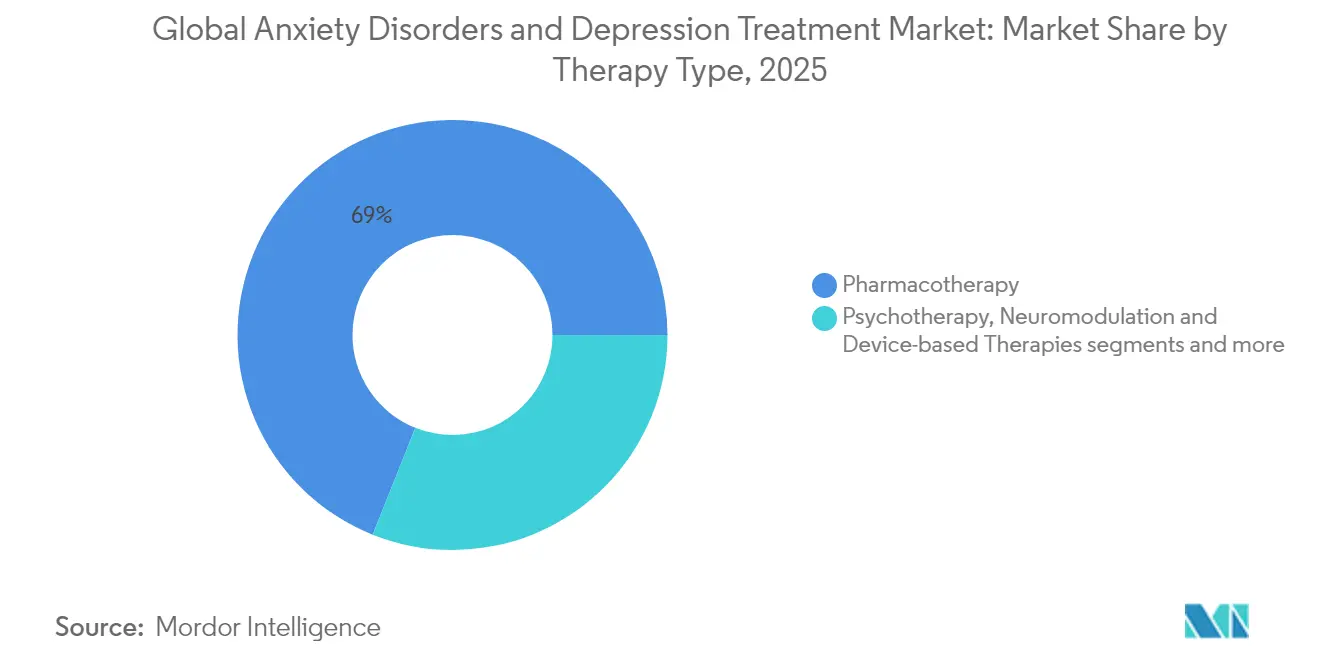

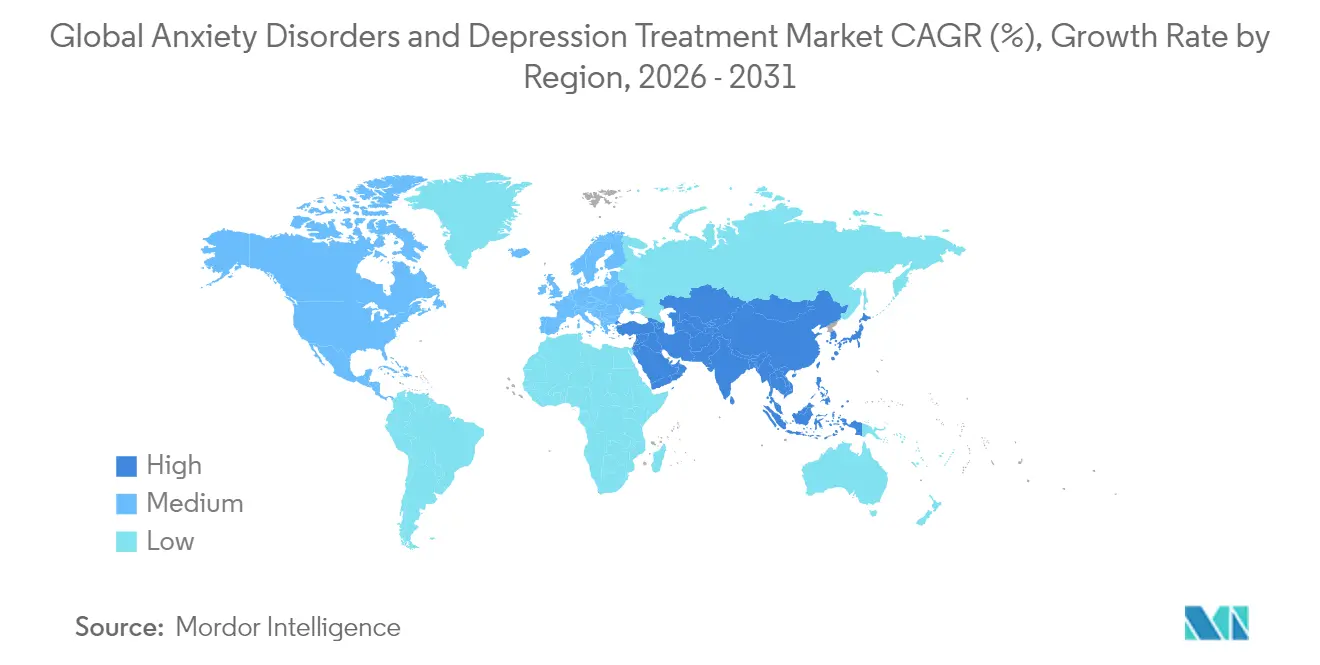

- By drug class, selective serotonin reuptake inhibitors led with 41.02% of the Anxiety disorder and depression treatment market share in 2025; atypical antipsychotics are forecast to advance at a 6.74% CAGR through 2031.By indication, major depressive disorder accounted for 38.22% of the Anxiety disorder and depression treatment market size in 2025, while PTSD treatments post the highest 6.89% CAGR to 2031.By therapy type, pharmacotherapy captured 68.95% revenue in 2025; digital therapeutics record the fastest 6.14% CAGR out to 2031.By end user, hospitals & clinics controlled 51.88% revenue in 2025; homecare settings grow quickest at 6.93% CAGR through 2031.By region, North America commanded 37.20% revenue in 2025; Asia-Pacific is projected to rise at an 7.76% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anxiety Disorders And Depression Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of anxiety & depression | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growing geriatric population prone to mental disorders | +0.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Pipeline approvals of novel antidepressant & anxiolytic agents | +1.0% | North America & EU primary, APAC secondary | Short term (≤ 2 years) |

| Increased awareness & stigma reduction toward mental health | +0.7% | Global, accelerated in APAC markets | Medium term (2-4 years) |

| OTC switch momentum for selected SSRIs | +0.5% | North America & EU focus | Short term (≤ 2 years) |

| AI-enabled digital therapeutics boosting adherence | +0.6% | North America & EU primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Anxiety & Depression

A post-pandemic surge in mental-health diagnoses increases demand, with depressive disorders representing 37.2% and anxiety 21.5% of mental-health DALYs in Asian nations. Younger adults adopt digital-first interventions, pushing firms to offer rapid-onset and personalized options. Payers are shifting to value-based reimbursement frameworks that emphasize measurable outcome improvement, compelling manufacturers to prove durability and speed of response beyond today’s SSRIs.

Growing Geriatric Population Prone to Mental Disorders

Ageing societies give rise to late-onset mood disorders and polypharmacy risks, intensifying need for drugs with cleaner interaction profiles. Gepirone’s approval as the first oral selective 5-HT1A agonist highlights opportunities in elderly-friendly mechanisms. Digital monitoring tools are gaining traction for early detection of cognitive decline, reinforcing care-at-home models and stimulating hardware-software ecosystems around established pills.

Pipeline Approvals of Novel Antidepressant & Anxiolytic Agents

Regulators display an openness to non-traditional mechanisms, awarding breakthrough status to psilocybin analogs and clearing the first prescription digital therapeutic for depression. AbbVie’s USD 1.95 billion pact with Gilgamesh underscores venture capital flowing into neuroplastogens that bypass classical psychoactive pathways[2]Source: AbbVie Press Office, “AbbVie and Gilgamesh Announce Collaboration on Next-Generation Therapies,” abbvie.com .

Increased Awareness & Stigma Reduction Toward Mental Health

Public campaigns, workplace programs, and social-media influencers are normalizing help-seeking, especially across Asia-Pacific where stigma had historically depressed engagement. This cultural shift accelerates OTC interest in low-dose SSRIs and drives uptake of discreet delivery forms. Providers now frame antidepressants as proactive wellness aids, broadening the addressable base beyond clinical populations.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expirations & generic erosion of blockbusters | -0.9% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Adverse effects limiting long-term adherence | -0.6% | Global, particularly in elderly populations | Medium term (2-4 years) |

| Psychedelic-assisted therapy siphoning demand | -0.4% | North America & EU primary | Medium term (2-4 years) |

| Value-based pricing & parity laws squeezing margins | -0.7% | North America & EU focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expirations & Generic Erosion of Blockbusters

Exclusivity cliffs remain sharp, with generics seizing as much as 90% of prescriptions inside a year of expiry. Branded players seek defense through reformulations and license deals such as Axsome’s settlement on Auvelity, yet economics favor cheaper substitutes unless brands deliver clear differentiation.

Value-Based Pricing & Parity Laws Squeezing Margins

The U.S. Mental Health Parity and Addiction Equity Act forces equivalent coverage, shifting cost risk to manufacturers in outcomes-based contracts. Firms now must supply real-world evidence platforms that track symptom-score improvements to justify premium price tags over generic SSRIs.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: SSRIs Hold Ground While Novel Pathways Accelerate

SSRIs controlled 41.02% revenue in 2025, underpinning the Anxiety disorder and depression treatment market with extensive safety records. Atypical antipsychotics, however, climb at a 6.74% CAGR as adjunctive options in major depression. Expansion stems from lumateperone’s broader label prospects and brexpiprazole’s PTSD nod. Meanwhile, 5-HT1A agonists, glutamate modulators, and psychedelics populate the “others” bucket that investors view as white-space categories capable of altering first-line prescribing.

Competition intensifies as agents that avoid weight gain, sexual dysfunction, or sedation draw preference among working-age users. Manufacturers respond with precision-dose kits and co-packaged digital-support apps that track adherence in real time and flag side-effect profiles for clinician review. Benzodiazepine utilization contracts as payers restrict long-term scripts, opening space for non-sedating anxiolytics and GABA-positive allosteric modulators with safer abuse profiles.

Note: Segment shares of all individual segments available upon report purchase

By Indication: Depression Still Dominates but PTSD Surges

Major depressive disorder generated 38.22% of 2025 revenue, reinforcing the Anxiety disorder and depression treatment market. PTSD, however, expands fastest at 6.89% CAGR, aided by FDA’s first approval of brexpiprazole plus sertraline and renewed interest in MDMA-assisted therapy despite Lykos’s recent setback.

Growing recognition of trauma across civilian life and veterans’ health policies widen the patient pool. Expanded diagnostic criteria for generalized anxiety disorder and social anxiety also unlock incremental volume, while obsessive-compulsive disorder remains underserved, thereby attracting pipeline focus on glutamatergic compounds and nasal sprays that promise rapid relief.

By Therapy Type: Digital Pairings Shift the Standard of Care

Pharmacotherapy still makes up 68.95% of 2025 spend, yet software-based adjuncts claim mindshare and regulatory legitimacy. Rejoyn’s 2024 FDA greenlight as the first Rx digital therapeutic positions app-pill bundles as future baseline care.

Digital tools extend dose-titration analytics, deliver cognitive training, and generate real-world evidence that secures payer acceptance. Device-driven neuromodulation—rTMS, tDCS, and implanted vagus stimulators—gains traction for refractory patients, while psychotherapy maintains steady relevance via hybrid telehealth models.

Note: Segment shares of all individual segments available upon report purchase

By End User: Homecare Rises on Telehealth Adoption

Hospitals and clinics delivered 51.88% sales in 2025, although home settings are growing quickest at 6.93% CAGR. Telepsychiatry, remote vital-sign monitoring, and AI-generated adherence nudges underpin decentralized regimens. Employers embed mental-health benefits to moderate productivity loss, broadening scripts beyond clinical encounters and adding another distribution node for pharmaceutical partners.

Geography Analysis

North America retained leadership with 37.20% revenue in 2025, underpinned by robust insurance coverage, rapid uptake of new modalities, and favorable FDA policies. Breakthrough designations for psilocybin analogs and the OTC switch pathway illustrate regulatory flexibility that accelerates launch cycles. U.S. parity laws expand access but compress margins, compelling firms to defend value through outcomes contracts.Asia-Pacific is set to be the growth engine with an 7.76% CAGR out to 2031. China’s NMPA approval of Ruoxinlin, a triple monoamine reuptake inhibitor, exemplifies regulatory modernization. Urbanization, social-media campaigns, and employer-led wellness programs reduce stigma, while price-sensitive segments favor generics. Japan, South Korea, and Australia spearhead digital-therapeutic adoption, whereas India’s large underserved population drives volume for low-cost SSRIs.Europe posts steady mid-single-digit gains as EMA’s revised antidepressant guideline promotes personalized endpoints and cross-border trial efficiencies. Universal coverage across Germany, France, and the Nordics sustains demand for innovative products once cost-utility criteria are satisfied. South America and the Middle East & Africa remain nascent but promising as telehealth infrastructure spreads and government stigma-reduction campaigns take hold.

Competitive Landscape

The Anxiety disorder and depression treatment market features moderate concentration. Big Pharma—Eli Lilly, Pfizer, Johnson & Johnson—leverages broad portfolios, but biotech challengers capture headlines with rapid-acting or psychedelic approaches. J&J’s USD 14.6 billion buyout of Intra-Cellular Therapies secures lumateperone, signaling a readiness to pay premium for novel MoAs. AbbVie’s multi-deal spree with Gilgamesh and Gedeon Richter underscores the race to own neuroplastogen and bipolar-focused assets.

Strategic collaborations pair pharma scale with digital-health agility; Otsuka’s alliance with Click Therapeutics fast-tracked Rejoyn, creating a template for combined pill-app submissions. Manufacturers also target treatment-resistant niches, coupling ketamine or dextromethorphan with SSRIs to accelerate onset. Generic houses consolidate to hold volume share as branded patents lapse, while API shortages and inflationary pressure push contract prices upward, benefitting integrated suppliers.

Marketing strategies pivot to patient-reported outcome storytelling and hybrid care pathways that highlight reduced total-cost-of-care versus simple symptom relief. Investment in real-world data platforms expands as payers demand longitudinal evidence of functional improvement.

Global Anxiety Disorders And Depression Treatment Industry Leaders

Pfizer Inc,

GlaxoSmithKline

Merck & Co. Inc

Eli Lily & Co

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Johnson & Johnson closed its USD 14.6 billion purchase of Intra-Cellular Therapies, adding lumateperone to its pipeline for adjunctive MDD treatment.

- May 2025: Supernus Pharmaceuticals moved to acquire Sage Therapeutics for up to USD 795 million, boosting its CNS franchise.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the global Anxiety Disorders and Depression Treatment market as the annual value of prescription medicines, device-based neuromodulation systems, and professionally delivered psychotherapies that are approved or reimbursed for major depressive disorder and the five most common anxiety disorders.

Scope Exclusion: Over-the-counter botanicals, wellness apps that never involve a clinician, and non-regulated self-help products are outside the frame.

Segmentation Overview

- By Drug Class (Value)

- Selective Serotonin Reuptake Inhibitors (SSRIs)

- Serotonin–Norepinephrine Reuptake Inhibitors (SNRIs)

- Tricyclic Antidepressants (TCAs)

- Monoamine Oxidase Inhibitors (MAOIs)

- Atypical Antipsychotics

- Benzodiazepines

- Others

- By Indication (Value)

- Major Depressive Disorder

- Generalized Anxiety Disorder

- Panic Disorder

- Social Anxiety Disorder

- Obsessive-Compulsive Disorder

- Others

- By Therapy Type (Value)

- Pharmacotherapy

- Psychotherapy (e.g., CBT)

- Neuromodulation & Device-based Therapies

- Digital Therapeutics

- By End User (Value)

- Hospitals & Clinics

- Specialty Mental-Health Centers

- Homecare Settings

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed psychiatrists, hospital pharmacy buyers, and payers across North America, Europe, and key Asia-Pacific nations. These discussions clarified country-level prescribing shares for SSRIs versus neuromodulation, real-world adherence, and upcoming formulary shifts, letting us verify desk estimates and adjust underlying assumptions.

Desk Research

We began with public datasets such as WHO mental-health prevalence tables, OECD Health Statistics on pharmaceutical expenditure, and FDA as well as EMA drug-approval libraries, which anchor treated-patient pools and patent timelines. Trade associations, for example, the International Federation of Pharmaceutical Manufacturers, and peer-reviewed journals supplied typical treatment durations and relapse rates. Company 10-Ks, quarterly calls, and clinical-trial registries rounded out launch schedules and pricing clues. Subscription resources, including D&B Hoovers for company revenue splits and Dow Jones Factiva for real-time headline checks, helped validate commercial uptake. The sources cited above illustrate our desk work; many additional outlets inform the model.

Market-Sizing & Forecasting

We build a top-down prevalence-to-treated-cohort model that starts with anxiety and depression incidence, applies diagnosis and treatment rates, and then layers average annual therapy cost. Supplier roll-ups and channel checks serve as selective bottom-up cross-tests. Inputs include: (1) WHO prevalence outlook, (2) branded versus generic share drift after patent cliffs, (3) median course length in weeks, (4) device installation counts for transcranial magnetic stimulation, (5) mental-health spend per capita, and (6) reimbursement expansion under new parity laws. A multivariate regression projects each driver through 2030; scenario analysis gauges upside from psychedelic approvals. Data gaps, such as private-clinic volumes, are filled with anchored ratios agreed upon during expert calls.

Data Validation & Update Cycle

Outputs undergo variance checks against historic sales, regional prescription audits, and independent prevalence surveys. Senior analysts review anomalies before sign-off. Reports refresh once a year, and interim updates trigger when material events, such as major approvals or guideline changes, surface; a final sweep occurs just before client delivery.

Why Mordor's Anxiety Disorders And Depression Treatment Baseline Remains Highly Credible

Published estimates often differ because firms choose unequal product baskets, base years, and refresh cadences.

Key gap drivers in this arena stem from whether therapies like cognitive behavioral therapy sessions or neuromodulation devices are included, the way average selling prices are inflated or discounted, and the speed at which generic erosion is modeled across regions. Mordor's approach combines prevalence math with selective supplier roll-ups and is re-benchmarked annually, which narrows drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.65 B (2025) | Mordor Intelligence | - |

| USD 20.51 B (2024) | Global Consultancy A | Omits device-based therapies and uses static ASPs |

| USD 12.89 B (2024) | Trade Journal B | Counts anxiety drugs only and relies on reported sales of top 10 firms |

| USD 10.89 B (2020) | Regional Consultancy C | Historic base year rolled forward with fixed CAGR, no primary validation |

These comparisons show that figures swing when scope narrows or aging assumptions go unchallenged. By triangulating treated-cohort math with on-ground interviews, Mordor delivers a balanced, transparent baseline that decision-makers can retrace and replicate.

Key Questions Answered in the Report

What is the current size of the Anxiety disorder and depression treatment market?

It reached USD 23.8 billion in 2026 and is projected to climb to USD 30.49 billion by 2031 at a 5.07% CAGR.

Which drug class generates the highest revenue?

SSRIs lead with 41.02% revenue in 2025, although atypical antipsychotics are the fastest-growing segment at 6.74% CAGR.

Why are digital therapeutics important for this market?

FDA clearance of Rejoyn validates software-based adjuncts that improve adherence and outcomes, fueling a 6.14% CAGR for digital solutions.

Which is the fastest growing region in Global Anxiety Disorders and Depression Treatment Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region will grow fastest?

Asia-Pacific is expected to expand at an 7.76% CAGR due to regulatory modernization, stigma reduction, and rising healthcare access.

How are parity laws affecting manufacturers?

U.S. parity requirements shift reimbursement to value-based contracts, pressuring margins unless firms provide real-world outcome data.