Anti-Jamming Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

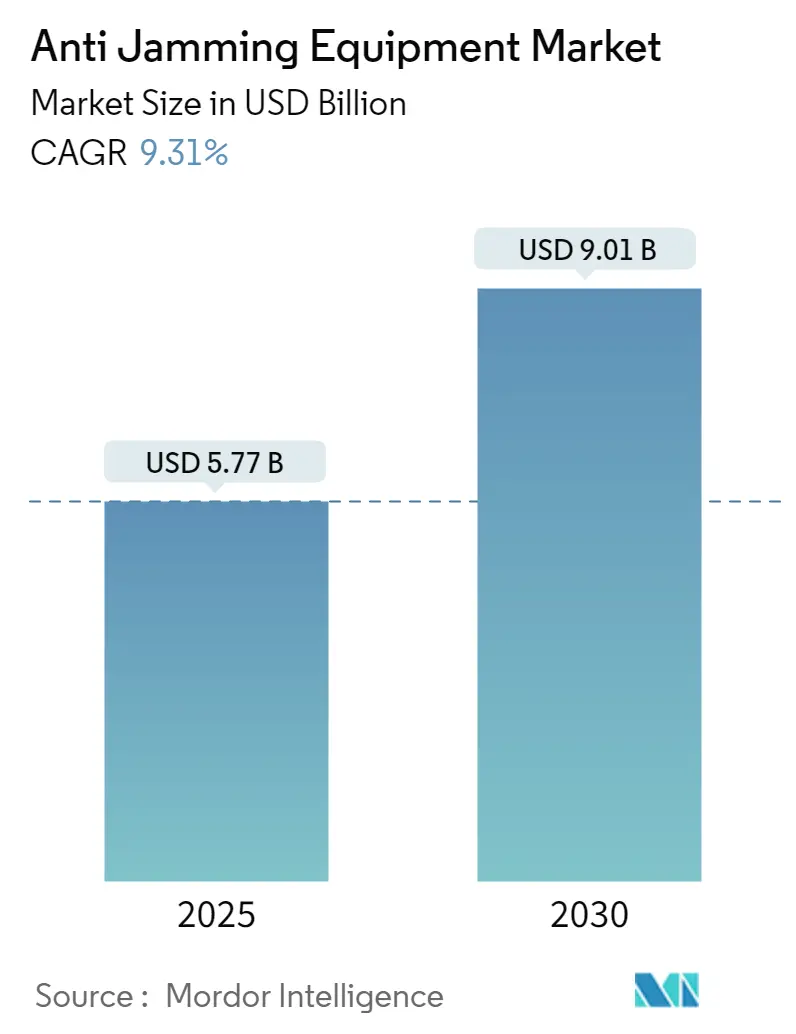

| Market Size (2025) | USD 5.77 Billion |

| Market Size (2030) | USD 9.01 Billion |

| Growth Rate (2025 - 2030) | 9.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Jamming Equipment Market Analysis by Mordor Intelligence

The Anti-Jamming Equipment Market size is estimated at USD 5.77 billion in 2025, and is expected to reach USD 9.01 billion by 2030, at a CAGR of 9.31% during the forecast period (2025-2030).

Growth stems from heightened demand for resilient positioning, navigation and timing (PNT) solutions as electronic warfare capabilities spread globally. Military modernization programs focus on closing GPS vulnerabilities highlighted during the Ukraine conflict, where frontline forces on both sides repeatedly disrupted satellite signals. Parallel investment in new low Earth orbit (LEO) constellations broadens the addressable base for next-generation anti-jamming receivers, while artificial intelligence-enabled digital beamforming enhances interference detection speed and accuracy. Regulatory mandates for dual-frequency, multi-constellation aviation receivers and e-navigation standards in maritime domains add a sizeable commercial retrofit opportunity. Export-control regimes create regional supply gaps that domestic vendors can fill, particularly in Asia-Pacific, where BeiDou, QZSS and NavIC constellations anchor sovereign PNT ambitions.

Key Report Takeaways

- By receiver type, Military and Government Grade units held 61.3% of the Anti-Jamming Equipment Market share in 2024, and Commercial/Transportation Grade units are forecast to grow at a 10.2% CAGR through 2030.

- By platform, Ground applications accounted for 33.7% share of the Anti-Jamming Equipment Market size in 2024 and Space-based terminals are advancing at an 11.9% CAGR through 2030.

- By anti-jamming technique, Beam Steering led with 28.4% revenue share in 2024, while Digital Beamforming registers the fastest 12.6% CAGR to 2030.

- By geography, North America commanded 38.6% share in 2024, whereas Asia-Pacific records a 12.7% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti-Jamming Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for GPS/GNSS in modernised C4ISR operations | 2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid fielding of unmanned and autonomous platforms needing assured-PNT | 2.1% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Mandates for resilient PNT in safety-critical civil sectors (aviation DFMC, maritime e-navigation) | 1.6% | Global, with early adoption in Europe & North America | Long term (≥ 4 years) |

| Proliferation of low-cost SDR-based jammers in grey-zone conflicts | 1.9% | Global, particularly in conflict-prone regions | Short term (≤ 2 years) |

| Adoption of authenticated GNSS (Galileo OSNMA, GPS M-code) opening retrofit cycle | 1.4% | Europe & North America initially, expanding globally | Medium term (2-4 years) |

| On-device AI/ML augmenting real-time interference detection and beamforming | 1.7% | Global, led by technology-advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Demand for GPS/GNSS in Modernised C4ISR Operations

Modern command, control, communications, computers, intelligence, surveillance and reconnaissance architectures depend on centimetric positioning and nanosecond-level timing. The U.S. Army’s Integrated Tactical Network now specifies 10 m accuracy under 40 dB jamming, driving a performance bar that commercial receivers cannot meet. [1]Andrew White, “Army Tests New GPS Resilience,” Army Technology, army-technology.comService branches also reference NATO STANAG 4751 to align anti-jamming receiver requirements across allied forces. Lessons from Ukraine show PNT degradation ripples through artillery fire control, ISR data fusion and datalink synchronization, prompting accelerated fielding of hardened receivers. Hybrid deployments that combine Starlink nodes with military-grade anti-jamming equipment kept Ukrainian units connected despite concerted RF attacks. Inter-service standardization and battlefield experience together cement sustained procurement momentum for premium anti-jamming solutions. [2]Patrick Tucker, “Starlink Aids Front-Line Connectivity,” Defense One, defenseone.com

Rapid Fielding of Unmanned and Autonomous Platforms Needing Assured-PNT

Autonomous aerial refuelers such as the U.S. Navy’s MQ-25 Stingray integrate sub-2 kg CRPA arrays that deliver 35 dB nulling, setting new SWaP-C benchmarks. Commercial drone manufacturers follow suit as regulators tighten beyond-visual-line-of-sight rules; FAA Remote ID proposals implicitly favor receivers that authenticate GPS and suppress spoofing FAA. Vendors like infiniDome claim 99.9% link availability under simulated denial, leveraging machine learning to predict jammer behaviors. Because unmanned vehicles cannot lean on human pilots for dead-reckoning, assured-PNT remains mission-critical, pushing Anti-Jamming Equipment Market adoption deeper into civil aerospace and robotics ecosystems. [3]Gidget Fuentes, “Navy’s MQ-25 Progresses on PNT,” Naval News, navalnews.com

Proliferation of Low-Cost SDR-Based Jammers in Grey-Zone Conflicts

Commodity SDR devices priced under USD 1,000 can now flood L1 and L2 bands across tens of kilometers, democratizing electronic attack capabilities. Field reports from Ukraine cite extensive adaptation of consumer hardware into tactical jammers, forcing defenders into a rapid innovation cycle. Agile interference that hops frequencies or mimics GPS waveforms degrades legacy null-steering antennas, so procurement offices pivot toward digital beamforming coupled with AI classifiers. This offense-defense escalation ensures recurring demand for upgradeable, software-defined anti-jamming architectures.

On-Device AI/ML Augmenting Real-Time Interference Detection and Beamforming

L3Harris embeds inference engines inside its latest CRPA arrays, achieving sub-10 ms threat characterization and instantaneous beam steering. Academic trials show neural classifiers isolating jammer signatures with 95% precision, cutting false-alarm rates and latency. Edge processors lower network traffic and power draw, making sophisticated countermeasures viable for size-constrained platforms. Civil vendors like NovAtel fold similar algorithms into OEM7 boards, highlighting a technology spillover that broadens addressable volume while sustaining defense-grade performance.

Restraints Impact Analysis Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High SWaP-C of multi-element CRPA for small platforms | -1.8% | Global, particularly affecting UAV and portable applications | Medium term (2-4 years) |

| Interoperability challenges with legacy navigation and comms stacks | -1.2% | Global, with higher impact in regions with aging infrastructure | Long term (≥ 4 years) |

| Export-control and ITAR restrictions limiting technology transfer | -1.4% | Global, with highest impact on international markets | Long term (≥ 4 years) |

| Escalating spectrum-congestion causing self-inflicted (friendly-fire) jamming | -0.9% | Primarily North America & Europe with dense RF environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High SWaP-C of Multi-Element CRPA for Small Platforms

Seven-element antennas often weigh 3-5 kg and draw 15-25 W, overshooting UAV payload budgets and soldier-carried radio limits GPS WORLD. Element spacing rules driven by physics hinder dramatic miniaturization, so vendors experiment with metamaterials and tightly coupled arrays. Cobham prototypes promise 50% footprint reduction but remain in low-rate production. The size-power penalty splits the Anti-Jamming Equipment Market into high-performance military models and cost-sensitive commercial variants, constraining cross-sector economies of scale. Until disruptive antenna topologies mature, SWaP-C will cap uptake on micro-UAVs and handheld devices.

Export-Control and ITAR Restrictions Limiting Technology Transfer

Controlled Reception Pattern Antenna algorithms fall under USML XI, demanding U.S. State Department licenses that can delay shipments for months. Comparable European dual-use controls further fracture the supply landscape. International customers often settle for downgraded performance or pursue indigenous development, trimming the total accessible revenue for leading U.S. suppliers. Classification of AI signal-processing software compounds barriers, as source code requires separate authorizations. Frameworks like AUKUS streamline small subsets of transfers but leave broader constraints intact, muting global diffusion of top-tier anti-jamming technology and tempering long-run Anti-Jamming Equipment Market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Receiver Type: Military Grade Maintains Margin Leadership

Military and Government Grade receivers commanded 61.3% revenue in 2024 on the back of 60 dB-plus jamming tolerance and -40 °C to +85 °C operating envelopes. Premium prices—10-20 times commercial units—underpin robust profitability, while the U.S. Common GPS Module program pools demand across services to offset NRE outlays. Commercial/Transportation Grade gear shows 10.2% CAGR as aviation DFMC mandates and maritime e-navigation projects activate large retrofit cycles. Competitive offerings fold M-code-derived firmware into automotive and industrial SKUs, accelerating civil adoption and narrowing the affordability gap.

Cost-sensitive sectors embrace multi-constellation chips that harness BeiDou and Galileo for diversity without the full CRPA burden. Suppliers leveraging shared silicon lines tap automotive scale to shave production costs, aiding diffusion into precision agriculture, construction and rail signaling. The ensuing volume uptick supports broader component supply chains, indirectly reinforcing military program sustainability and enlarging the overall Anti-Jamming Equipment Market.

By Anti-Jamming Technique: Digital Beamforming Overtakes Static Arrays

Beam Steering held 28.4% share in 2024 thanks to decades-old phased-array fielding on naval and airborne assets. Digital Beamforming now posts 12.6% CAGR as FPGA throughput doubles and software-defined radios collapse hardware complexity. AI-optimized weight vectors adapt on the fly to frequency-hopping interference, refreshing installed systems via firmware rather than new antenna panels. Nulling remains attractive for cost-constrained nodes, though susceptibility to agile threats limits long-term relevance.

Civilian Signal Processing and Adaptive Notch filtering fill size-restricted niches such as wearables and IoT trackers. Meanwhile, encrypted civil authentication—Galileo OSNMA and GPS M-code—emerges as a complementary line of defense that raises the spoofing bar without heavy antenna arrays. Vendors blend cryptographic checks with machine learning beamformers to deliver layered protection, underlining why software-centric solutions are redefining competitive differentiation across the Anti-Jamming Equipment Market.

By Platform: Ground Nodes Dominate While Space Terminals Accelerate

Ground vehicles and fixed stations represented 33.7% of 2024 revenue, driven by the U.S. Army’s USD 200 million MAPS buys and NATO base-station upgrades. Large-aperture CRPAs with 40-plus elements enable deep nulling against high-power truck-mounted jammers, making them the tactical network’s first line of defense. Supply chains benefit from less stringent weight constraints, favoring robust metallic housings and multi-board RF back-ends that boost mean time between failure.

Space-based terminals record 11.9% CAGR as proliferated LEO networks expose satellites to terrestrial interference. Constellation operators embed phased arrays that look both earthward and toward companion satellites, demanding radiation-hardened RFICs and thermal-managed power stages. Airborne fleets modernize more gradually, yet new tanker and ISR aircraft integrate miniaturized CRPAs within aerodynamic fairings to preserve drag metrics. Naval platforms battle multipath reflections off sea surfaces, spurring specialized adaptive algorithms tuned for dynamic vessel motion. Platform diversity thus continues broadening total available demand for the Anti-Jamming Equipment Market.

By Application: Navigation Commands Spend While Weapon Guidance Grows Fast

Navigation, Positioning and Timing absorbed 36.1% revenue in 2024 because every network node needs an anti-jamming front end to maintain absolute time and geographic reference. Precision-guided munitions raise bar further; modern PGMs require 3 m CEP and impose 40 dB jamming resilience, accelerating subsystem upgrades in artillery shells and glide bombs. Consequently, Targeting and Weapon Guidance expands at 10.8% CAGR through 2030, narrowing the historical gap with navigation.

Surveillance and Reconnaissance payloads rely on accurate geolocation to stitch multisensor intelligence, while Flight and Platform Control prioritizes ultra-low-latency resilience to avoid mission aborts. Command, Control and Communications segments demand nanosecond timing for crypto key rotation. Emerging medevac drones add life-critical urgency, spotlighting anti-jamming as a humanitarian enabler. Collectively these use cases amplify the Anti-Jamming Equipment Market size and diversify revenue beyond traditional defense silos.

By Frequency Band: Multi-Band Diversity Gains Ground

L1/L2 bands delivered 42.5% sales in 2024 courtesy of entrenched GPS heritage and wide receiver inventories. Jamming intensity pushes integrators to adopt tri-band or wider coverage solutions, lifting Multi-Band configurations to an 11.4% CAGR trajectory. Higher-power L5/E5 channels strengthen link budgets, while BeiDou’s B1-B3 lanes and Galileo’s E6 add redundancy. Tri-band antennas exploit overlapping polarizations to refine beam null placement, augmenting interference rejection without size growth.

Regulators such as RTCA specify DO-229 performance baselines that effectively institutionalize multi-frequency capability within civil aviation. As certified avionics trickle down into maritime and rail sectors, demand for wideband front-ends pushes RF filter and low-noise amplifier innovation, reinforcing upward momentum across the Anti-Jamming Equipment Market.

Geography Analysis

Anti-Jamming Equipment Market in North America

North America sized the Anti-Jamming Equipment Market at 38.6% share in 2024, underpinned by Pentagon outlays exceeding USD 1.7 billion for assured PNT through FY 2025. The U.S. Space Force funnels USD 500 million into the Resilient GPS initiative, while Canada directs Arctic sovereignty projects that require cold-tolerant CRPAs. A dense cluster of primes—RTX Corporation, L3Harris and Lockheed Martin—anchors R&D pipelines and vertically integrated production. Export Administration Regulations shield domestic IP yet limit foreign revenue channels, so suppliers chase multiyear sustainment contracts to solidify cash flows.

Asia-Pacific tallies the fastest 12.7% CAGR between 2025-2030 thanks to China’s BeiDou global rollout, Japan’s QZSS augmentation and India’s NavIC expansion. Indigenous receiver programs reduce exposure to ITAR constraints and spawn local champions. Chinese PLA procurement favors domestic CRPA vendors, while Korean Positioning System prototypes unlock fresh satellite terminal demand. Regional tensions in the South China Sea and the Taiwan Strait maintain defense budgets that prioritize electronic protection measures, accelerating the Anti-Jamming Equipment Market trajectory.

Europe progresses steadily, leveraging European Space Agency investments and EU Digital Compass policies that call for sovereign, secure connectivity. Thales, Safran and Rohde & Schwarz spearhead Galileo-compatible solutions targeting both defense and civil safety-of-life users. NATO interoperability mandates unify procurement specifications across member states, easing cross-border supply chain synergies. Middle East and Africa benefit from border security modernization and critical-infrastructure builds, though adoption rates hinge on license approvals. South America sees incremental uptake, with Brazil’s agriculture drones and Argentina’s border forces anchoring civil grade demand, reinforcing global diversification of the Anti-Jamming Equipment Market.

Competitive Landscape

Market concentration remains moderate; RTX Corporation, BAE Systems, L3Harris Technologies and Lockheed Martin collectively hold 45% share, leveraging decades of classified CRPA research and deep program management expertise. Long-term Indefinite-Delivery Indefinite-Quantity contracts insulate cash flows while iterative block upgrades keep incumbents entrenched. Emerging entrants focus on AI-driven software stacks that retrofit onto legacy antennas, carving out specialty niches.

Horizontal consolidation gathers pace; Safran’s acquisition of timing specialist Orolia fuses oscillators with anti-jamming antennas into turnkey resilient-PNT kits. Thales’ 2024 purchase of a metamaterial CRPA start-up trims size by 40%, positioning the group for lightweight UAV bids. Supply-chain verticalization intensifies as primes secure gallium nitride RF chip lines to curb export restrictions.

Commercial pressure mounts from automotive and telecom sectors that seek affordable jamming protection. Vendors like u-blox and Septentrio leverage mass-market GNSS chip volumes to cut cost, opening mid-tier civil channels. Meanwhile, infiniDome captures aviation retrofit orders after securing FAA certifications, proving regulatory compliance can unlock sizeable new pockets of the Anti-Jamming Equipment Market.

Anti-Jamming Equipment Industry Leaders

RTX Corporation

Chelton Limited

Novatel Inc. (Hexagon AB)

Mayflower Communications

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: L3Harris Technologies won a USD 587 million U.S. Navy contract for adaptive beamforming electronic-warfare suites.

- August 2024: RTX Corporation received a USD 77.2 million U.S. Air Force order for Miniaturized Airborne GPS Receivers featuring enhanced anti-jamming.

- July 2024: Thales Group closed a USD 45 million acquisition of a CRPA specialist, adding metamaterial technology to its lineup.

- June 2024: U.S. Space Force awarded USD 120 million across multiple vendors for Resilient GPS satellites embedding anti-spoofing payloads.

Global Anti-Jamming Equipment Market Report Scope

Anti-jamming equipment protects signal receivers from intervention and deliberate jamming. For instance, when a GPS signal reaches the earth's surface, it becomes weak and susceptive to being overcome by more powerful radio frequency (RF) energy. GPS anti-jamming handles power minimization to decrease the effect of interference and jamming so that the GPS receiver can continue to function correctly. The market's scope is limited to anti-jamming equipment offered by market vendors, which includes civilian and defense applications.

The anti-jamming equipment market is segmented by technology (nulling technique, civilian techniques, and beam steering techniques), end-user application (flight control, defense, surveillance and reconnaissance, navigation, position, timing, casualty evacuation, and other end-user applications), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, rest of Europe), Asia-Pacific (China, Japan, South Korea, rest of Asia-Pacific) and rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| Military and Government Grade |

| Commercial / Transportation Grade |

| Nulling |

| Beam Steering |

| Civilian (Signal Processing / Adaptive Notch) |

| Digital Beamforming |

| Adaptive Cryptographic Authentication |

| Airborne | Manned Aircraft |

| Unmanned Aerial Vehicles | |

| Ground | Armoured and Tactical Vehicles |

| Fixed and Portable Ground Stations | |

| Naval | |

| Space-Based and Satellite Terminals |

| Navigation, Positioning and Timing |

| Surveillance and Reconnaissance |

| Flight and Platform Control |

| Targeting and Weapon Guidance |

| Command, Control and Communications |

| Casualty Evacuation / MEDEVAC |

| L1/L2 |

| L5 / E5 |

| Multi-Band (Tri-Band +) |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Italy | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Middle East and Africa | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| South Africa |

| By Receiver Type | Military and Government Grade | |

| Commercial / Transportation Grade | ||

| By Anti-Jamming Technique | Nulling | |

| Beam Steering | ||

| Civilian (Signal Processing / Adaptive Notch) | ||

| Digital Beamforming | ||

| Adaptive Cryptographic Authentication | ||

| By Platform | Airborne | Manned Aircraft |

| Unmanned Aerial Vehicles | ||

| Ground | Armoured and Tactical Vehicles | |

| Fixed and Portable Ground Stations | ||

| Naval | ||

| Space-Based and Satellite Terminals | ||

| By Application | Navigation, Positioning and Timing | |

| Surveillance and Reconnaissance | ||

| Flight and Platform Control | ||

| Targeting and Weapon Guidance | ||

| Command, Control and Communications | ||

| Casualty Evacuation / MEDEVAC | ||

| By Frequency Band | L1/L2 | |

| L5 / E5 | ||

| Multi-Band (Tri-Band +) | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Italy | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Middle East and Africa | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| South Africa | ||

Key Questions Answered in the Report

What is the global value forecast for anti jamming equipment in 2030?

The segment is projected to reach USD 9.01 billion by 2030, reflecting a 9.31% CAGR over 2025-2030.

Which region is expanding the fastest in anti jamming solutions?

Asia-Pacific posts the highest 12.7% CAGR through 2030, buoyed by BeiDou, QZSS, and NavIC programs.

Why do autonomous platforms accelerate demand for anti-jamming receivers?

Unmanned vehicles cannot rely on human operators, so they require assured-PNT; AI-enabled CRPAs now deliver 35 dB nulling at sub-2 kg SWaP thresholds.

How large is the share held by Military and Government Grade receivers?

These hardened units captured 61.3% share in 2024 on the back of 60 dB+ jamming resistance.

What anti-jamming technique is growing the fastest?

Digital beamforming leads with a 12.6% CAGR, thanks to software-defined radios and machine-learning weight-vector optimization.

Which contractual program illustrates strong U.S. spending?

The U.S. Space Force’s Resilient GPS initiative commands USD 500 million to deploy hardened satellites that bolster interference resistance.

Page last updated on: