Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

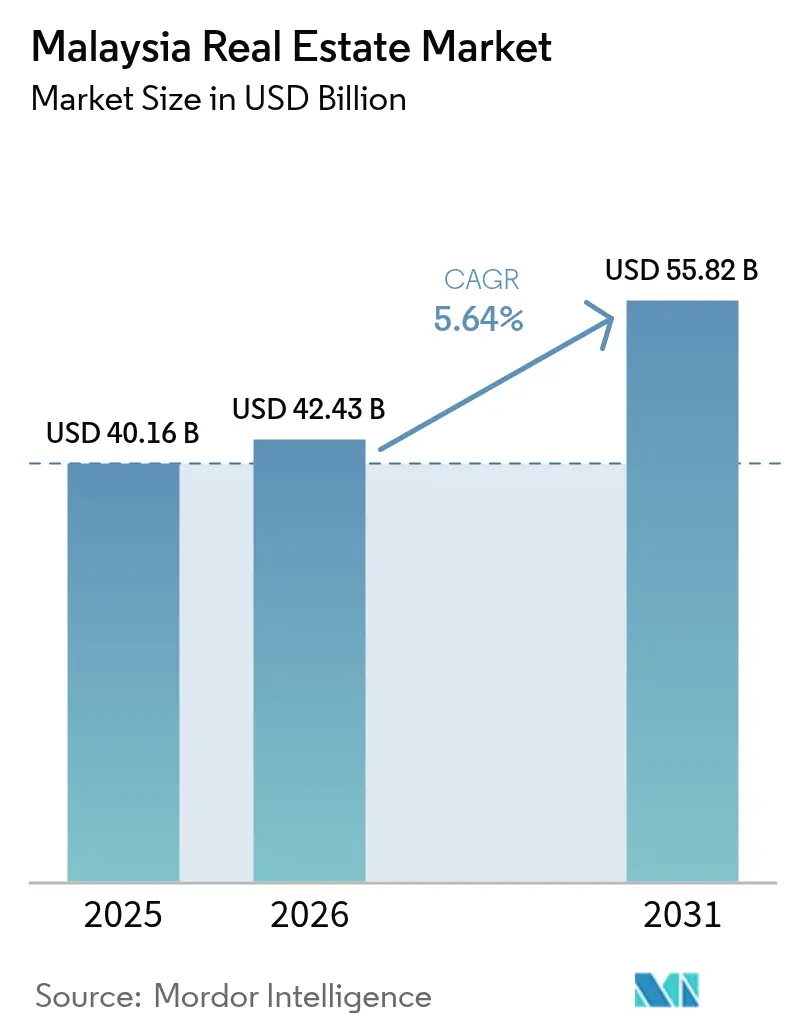

| Base Year Market Size (2025) | USD 40.16 Billion |

| Market Size (2026) | USD 42.43 Billion |

| Market Size (2031) | USD 55.82 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Real Estate Market Analysis by Mordor Intelligence

The Malaysia real estate market size was valued at USD 40.16 billion in 2025 and estimated to grow from USD 42.43 billion in 2026 to reach USD 55.82 billion by 2031, at a CAGR of 5.64% during the forecast period (2026-2031). Sustained government spending on rail, highway, and port infrastructure is redirecting housing and commercial demand toward newly connected corridors. Semiconductor capital expenditure, led by a USD 7 billion Intel plant, is translating into steady absorption of industrial parks and high-spec logistics hubs. Residential sentiment shows signs of revival after pandemic-era softness, supported by policy incentives for first-time buyers and the ongoing shift toward larger landed homes. At the same time, foreign direct investment in AI data centers and renewable-energy projects is broadening commercial asset demand. Developers with early land positions near transit nodes, port hinterlands, and cross-border gateways are best placed to ride the next growth wave of the Malaysia real estate market.

Key Report Takeaways

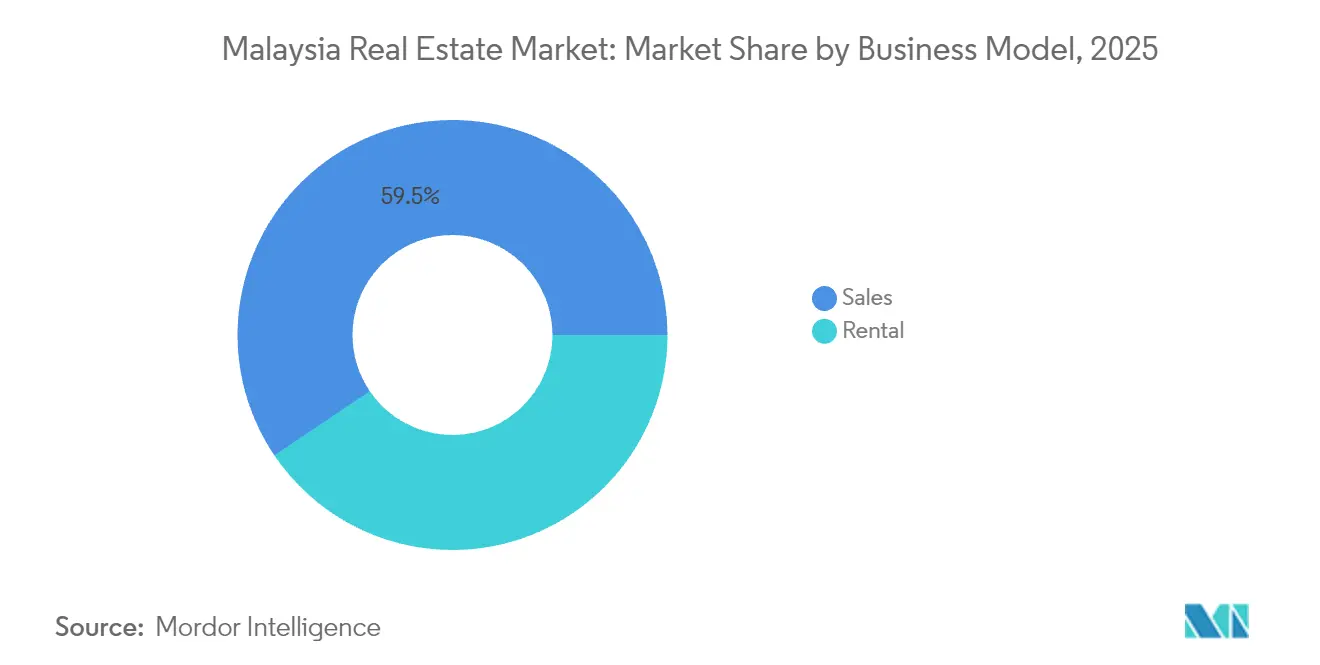

- By business model, sales properties held 59.45% of the Malaysia real estate market share in 2025; rental assets are forecast to expand at a 6.32% CAGR through 2031.

- By property type, residential dominated with a 61.35% share in 2025, while commercial stock is projected to rise at a 6.47% CAGR to 2031.

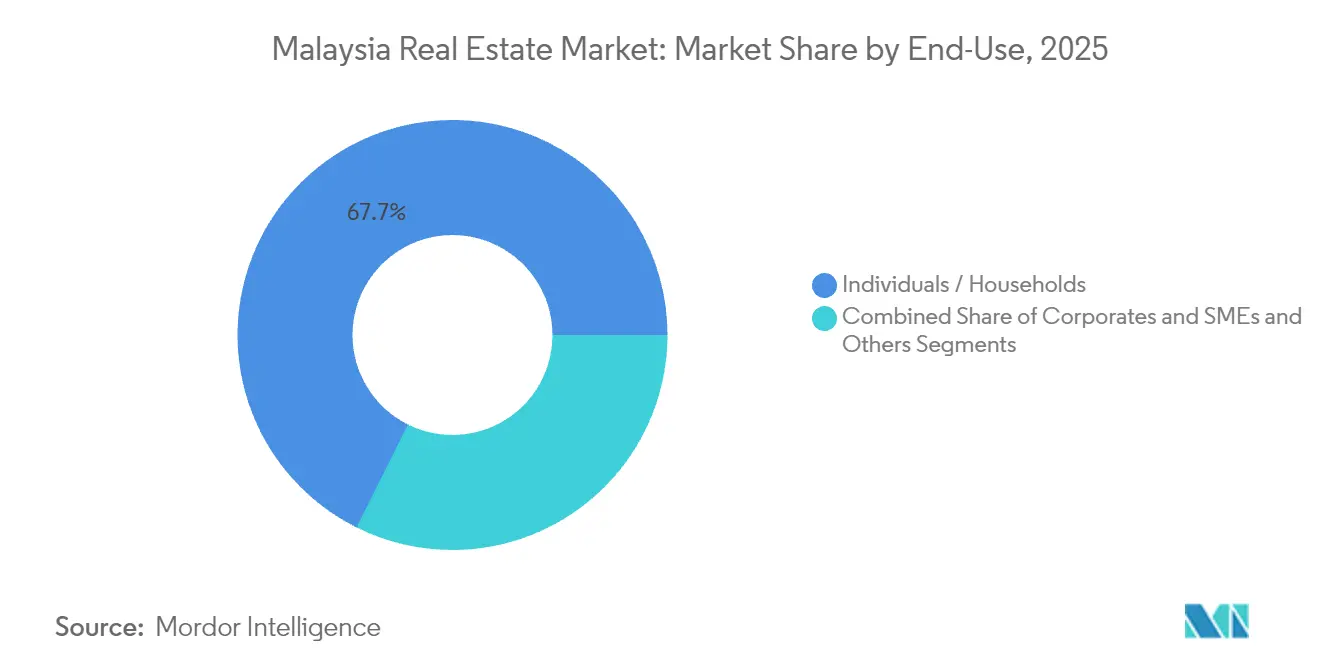

- By end-user, individual households accounted for 67.65% of demand in 2025; corporate and SME users show the highest projected CAGR at 6.62% to 2031.

- By key cities, Kuala Lumpur captured 44.90% revenue share in 2025, whereas Johor Bahru is advancing at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure investments (MRT/LRT, highways, cross-border links) | +1.5% | Klang Valley, Johor-Singapore corridor | Long term (≥ 4 years) |

| Urban growth in Klang Valley, Penang, Johor | +1.2% | Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| Industrial and logistics expansion (E&E, nearshoring) | +1.0% | Selangor, Penang, Johor | Medium term (2-4 years) |

| Foreign ownership avenues and REIT market | +0.8% | National, focus on KL & Johor | Short term (≤ 2 years) |

| Sustainable, transit-oriented, smart projects | +0.7% | Major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure investments opening new property corridors

Infrastructure development is driving significant changes in Malaysia's property market. With a budget of USD 11.16 billion, the MRT3 Circle Line is set to add 51 kilometers and 31 stations, establishing an orbital route around Kuala Lumpur. In tandem with this rail expansion, Westports is investing USD 8.8 billion to boost Port Klang's capacity to 27 million TEUs, spurring a surge in warehouse demand along the Klang logistics belt. Meanwhile, the Pan Borneo Highway and East Coast Rail Link are enhancing connectivity along the east-west axis, reaching into secondary states. This has led to proactive landbank acquisitions, anticipating a rise in valuations. Developers, seizing the opportunity, are strategically planning township launches near interchange hubs slated to open from 2027. This newfound accessibility is poised to drive capital appreciation in Malaysia's real estate market, especially in the suburbs now gaining prominence.

Urban growth in Klang Valley, Penang, and Johor sustaining residential demand

Urbanization is driving significant changes in Malaysia's real estate market, particularly in Klang Valley, Penang, and Johor. As urbanization intensifies, economic activities are increasingly aligning with mass-transit corridors in Klang Valley, Penang, and Johor. The MRT2 line, linking satellite townships to Kuala Lumpur’s primary job zones, has notably elevated property values in Bandar Sri Damansara and Kepong due to reduced commute times. In Penang, Batu Kawan township introduced 704 landed units priced at USD 209,000 each, capitalizing on the influx of new semiconductor factories. Johor's landscape is shaped by the Johor-Singapore Special Economic Zone, with projects like the USD 582 million Bukit Chagar, designed for cross-border commuters. This trend underscores a growing preference for developments that seamlessly integrate residential, retail, and logistics components. Real estate agents highlight that properties within a 500-meter radius of transit stations can command resale premiums of up to 30%. Such trends indicate a pronounced shift towards transit-oriented housing as the dominant investment focus in Malaysia's real estate landscape[1]Y. Tan, “Bandar Sri Damansara Prices Lifted by MRT2,” edgemalaysia.com.

Industrial and logistics expansion supporting land absorption

Malaysia's industrial and logistics sectors are witnessing significant growth, driven by substantial investments and policy support. In 2024, Malaysia approved fresh investments totaling USD 56.6 billion. The electronics and electrical sector attracted USD 10.4 billion, reinforcing Malaysia's position as the sixth-largest semiconductor exporter globally. Intel's USD 7 billion assembly plant in Penang and GlobalFoundries' newly announced hub are boosting pre-leasing activity for high-spec factories designed for clean-room operations. Knight Frank reports steady demand for units between 20,000 and 50,000 sq ft in Selangor and Johor, as suppliers diversify away from China. Additionally, CapitaLand Malaysia Trust's USD 6 million investment in Nusajaya Tech Park, fully leased to optics and medical tenants, highlights institutional interest in stable industrial yields. The New Industrial Master Plan 2030, which emphasizes advanced manufacturing, provides a strong policy framework supporting Malaysia's real estate market.

Foreign investment avenues enhancing market participation

The revamped Malaysia My Second Home program now offers Silver, Gold, and Platinum tiers tied to deposit requirements and property purchase minimums ranging from USD 133,000 to USD 444,000. It secured 1,902 approvals in 2024, supporting high-rise absorption in Kuala Lumpur and coastal Penang. Visa holders may withdraw 50% of deposits for property buys after one year, channeling capital directly into sales completions. Meanwhile, Microsoft’s USD 2.2 billion and Google’s USD 2 billion data-center commitments have spurred site aggregation for hyperscale campuses near fiber routes in Johor and Selangor. The combined effect is deeper foreign participation across residential and specialized commercial segments of the Malaysia real estate market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oversupply and unsold inventory in high-rise submarkets | -1.1% | Kuala Lumpur, Selangor high-rise clusters | Short term (≤ 2 years) |

| Household income constraints and selective lending | -0.8% | Nationwide, first-time buyers | Medium term (2-4 years) |

| Policy shifts creating investor uncertainty | -0.6% | National, premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oversupply challenges in high-rise segments

The high-rise segment in Malaysia's real estate market is grappling with significant oversupply challenges. As of Q3 2023, unsold inventory in Malaysia's real estate market stood at 25,311 units, valued at USD 3.87 billion. Notably, Kuala Lumpur accounted for 3,111 units, representing 19.07% of the total overhang. The issue arises from a pricing mismatch: developers have primarily focused on units priced above USD 111,000, while actual demand is concentrated in the USD 67,000 to USD 111,000 range. Adding to the problem, banks have restricted end-financing for speculative projects, leading to slower sales and higher marketing expenses. In response to changing post-pandemic preferences, some firms are shifting back to landed formats, launching 3,127 units in Q1 2024. However, until the clearance rate improves, the oversupply is expected to continue weighing on capital gains in Malaysia's real estate market.

Household income constraints moderating absorption

The Malaysian real estate market faces challenges stemming from economic and financial factors. Household debt stands at 81.9% of GDP, limiting affordability in major cities. The central bank, aiming to alleviate payment stress, has kept policy rates steady at 3.0%. However, lenders are exercising caution, leading to loan approval ratios dipping below pre-COVID figures. The 2025 budget has set aside guarantees for 20,000 mortgages, but in Klang Valley and Penang, wage growth is falling behind asset inflation. Maybank reports a 10.4% growth in its mortgage portfolio, and digital approvals via Home2u indicate a hidden demand. Yet, many buyers find themselves stretching their debt-service ratios just to secure properties. In the Malaysian real estate market, purchasing power is poised to trail behind price appreciation in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rental Momentum Amid Sales Dominance

Sales properties controlled 59.45% of the Malaysia real estate market in 2025, mirroring the nation’s home-ownership ethos. Transaction volume hit 311,211 units worth USD 36.21 billion that year, validating the segment’s scale. Supported by fixed-rate mortgages and stamp-duty waivers for first homes, primary launches continue to record robust bookings. Developers such as Sime Darby Property have sold over 2,700 units valued at USD 578 million since 2023 through digital booking systems.

Rental stock, although smaller, is charting a 6.32% CAGR to 2031, the fastest rate in the Malaysia real estate market. Younger professionals favor flexibility and are clustering around MRT and LRT stations where transit-linked apartments allow car-free living. Coworking operators located in these nodes estimate that reduced commute times save tenants 7,000 hours annually. Johor’s proximity to Singapore further propels rental yields, with serviced apartments like Gen Rise (GDV USD 125 million) aimed at cross-border workers achieving pre-leasing success.

By Property Type: Residential Scale, Commercial Upswing

Residential holdings delivered 61.35% of Malaysia's real estate market share in 2025 on the back of sustained appetite for terrace houses and condominiums. Eco World’s USD 1.56 billion Eco Horizon in Batu Kawan exemplifies township scale, offering over 2,000 homes that align with industrial job growth nearby. Landed products in Gamuda Cove’s Palma Sands, priced from USD 101 million GDV, achieved full bookings on release day, reaffirming end-user focus on space and community amenities.

Commercial assets are forecast to post a 6.47% CAGR to 2031, helped by semiconductor supply-chain investments that require clean-room factories and logistics warehouses. CapitaLand Malaysia Trust’s USD 6 million factory buy in Nusajaya Tech Park signals steady institutional entry into light-industrial strata. Office demand is tilting toward ESG-certified towers with floorplates capable of hosting hybrid work configurations. Retail landlords are repositioning malls with omnichannel tenants to capture rising e-commerce logistics synergies in the Malaysia real estate market.

By End-User: Household Bulk, Corporate Acceleration

Individual households absorbed 67.65% of total transactions in 2025, reflecting cultural emphasis on property as a family asset. Government initiatives, including the Step-Up Financing Scheme and mortgage guarantees, aim to widen first-time buyer access. Digital banks have reduced loan approval times, though debt-service ratios remain stretched in Klang Valley.

Corporate and SME users exhibit a 6.62% CAGR outlook through 2031, driven by robust FDI inflows totaling USD 16 billion in Q1 2024. Microsoft’s USD 2.2 billion AI infrastructure and Google’s USD 2 billion data-center plans are spurring demand for edge-ready campuses in Johor and Selangor. SMEs leverage Maybank’s under-10-minute digital financing to secure shophouses and micro warehouses, preserving agility amid supply-chain uncertainties. Institutional investors and REITs account for a growing “other” category that channels pension capital into stabilized logistics and retail portfolios within the Malaysia real estate market.

Geography Analysis

As of 2025, Kuala Lumpur accounts for 44.90% of Malaysia's real estate transactions. This is driven by its strong employment base, key retail areas, and improved transportation links connecting suburban areas to the central business district (CBD). In the Golden Triangle, average condominium prices have stabilized as new projects focus on co-living spaces and green-certified designs aimed at younger buyers. Developers are managing supply by staggering project completions to match demand. Unsold units, priced above USD 111,000, are attracting foreign buyers, particularly under the MM2H program.

Johor Bahru is the fastest-growing metropolitan area, with a projected growth rate of 6.78% CAGR until 2031. It is expected to account for nearly 19.60% of Malaysia's real estate market share in the coming years. Industrial growth is driving this expansion, with UEM Sunrise developing a renewable-energy park and Gamuda investing USD 94 million in Port Dickson land for potential data centers. These developments are encouraging white-collar migration and increasing residential demand. The Rapid Transit System, expected to connect Johor Bahru to Singapore by 2026, will reduce commuting times to Woodlands to under 15 minutes. Developers are focusing on mixed-use projects near transit stations to attract early buyers seeking rental income opportunities.

Outside these key areas, Penang benefits from its semiconductor industry and tourism appeal, maintaining strong demand for landed homes in areas like Batu Kawan. Sabah, Sarawak, and Pahang are seeing growth due to new east-west highways, which improve logistics for plantation and renewable-energy investors. Port Klang's USD 8.8 billion terminal expansion is driving logistics and warehouse development along the coastal Selangor region. These regional developments are diversifying opportunities and expanding Malaysia's real estate market.

Regulatory Landscape

Malaysia's real estate market is governed by a mix of federal and state rules covering developer licensing, buyer protection, construction compliance, and foreign participation. In 2026, the Ministry of Housing and Local Government (KPKT) advanced the Madani Housing Reform agenda, upgrading HIMS and the TEDUH system. By May 2026, the government reported 1,615 housing projects restored since December 2022, pointing to tighter monitoring and stronger intervention capabilities for project delivery and remediation.

In 2026, the policy direction also moved toward a data-driven housing framework, with the National Housing Policy 2026-2035 nearing finalization and using local income data to map and set affordable home prices. At the same time, the proposed Real Property Development Bill, intended to replace the Housing Development (Control and Licensing) Act 1966, Act 118, was positioned to broaden oversight beyond residential projects to include commercial developments. Existing buyer safeguards, including KPKT requirements for Housing Development Accounts (HDA) and strengthened audit mechanisms, continue to influence developers' cashflow governance and compliance obligations.

Value Chain Analysis

Malaysia's real estate value chain spans land origination and planning approvals, financing, construction delivery, sales and leasing, and post-handover operations such as property management, facilities management, valuations, and transaction platforms. Developers and their contractor ecosystem sit at the center of execution, while government-linked programs and regulators shape build methods and compliance.

Construction activity is a key upstream driver of supply. The construction sector recorded total work done of RM158.8 billion in 2024, followed by RM132.2 billion for the first three quarters of 2025 (RM45.4 billion in Q3 2025), which supports contractor utilization, labor demand, and materials throughput. On the build and inputs side, CIDB frameworks and mandates influence cost, productivity, and supplier qualification, including Industrialised Building System (IBS) requirements, such as a minimum 70 IBS Score referenced in government circulars for applicable projects, and Certification of Construction Product and Material (CCPM) under the CIDB Act 520 (Amendment) 2011. Supplier readiness is also being supported through initiatives such as CIDB's Strategic Ecosystem Vendor Development Program for the IBS cluster, launched in October 2024, and the Malaysia Public Works Strategic Collaboration Programme 2025 launched in February 2025 by the Ministry of Works/CIDB/JKR, aimed at more standardized, technology-enabled delivery for large public and private developments.

Competitive Landscape

Competition in Malaysia's real estate market is moderately fragmented, with no single developer holding more than a 10% nationwide share. Leading players use a combination of large landbanks, effective township development, and digital sales channels to sustain growth. In 2024, Sime Darby Property reported USD 756 million in revenue and USD 135 million in operating profit, balancing the launch of landed properties with industrial park projects in Elmina Business Park.

Developers are diversifying their portfolios by focusing on logistics and data-center assets. Gamuda acquired 389 acres in Port Dickson for USD 94 million, with plans for up to USD 3.6 billion in digital-infrastructure gross development value (GDV), enabling entry into hyperscale colocation. CapitaLand Malaysia Trust's acquisition in Johor marks its entry into industrial strata, reflecting growing institutional interest in stabilised, automation-ready warehouses.

Technology is playing a key role in improving sales processes. PropertyGuru, following EQT's USD 1.1 billion acquisition, is enhancing its AI-powered valuation and matching tools, serving over 31 million regional users. Developers are incorporating virtual tours, live-chat mortgage services, and blockchain booking systems to create smoother customer experiences. Sustainability is also becoming a priority, with Bursa Malaysia's ESG framework encouraging disclosures on embodied carbon, water reuse, and waste management. These efforts are improving service quality and increasing transparency in Malaysia's real estate market.

Malaysia Real Estate Industry Leaders

Sime Darby Property Berhad

SP Setia Berhad

Sunway Berhad (Property Division)

Eco World Development Group Berhad

IOI Properties Group Berhad

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is concentrated where policy, infrastructure, and corporate capex translate into site aggregation and specialized asset requirements. The National Housing Policy 2026-2035 uses local income mapping from the 2024 Household Income and Basic Amenities Survey to recalibrate affordability benchmarks, which gives developers room to adjust product design, pricing ladders, and location strategies around locally defined affordability.

Data center build-outs are a core commercial and industrial driver, with the second phase cited as a driver of annual construction activity alongside major transport packages such as the Penang LRT civil and systems packages supporting transit-oriented residential and mixed-use redevelopment. In parallel, NAPIC-reported unsold completed residential units of 32,801 as of Q1 2026 (worth RM16.37 billion) keep the competitive focus on differentiated formats, including green-certified buildings, transit-linked products, and smart-enabled homes near industrial parks in Johor-Singapore SEZ and on plans such as Malaysia Vision Valley 2.0 in Negeri Sembilan.

Recent Industry Developments

- July 2026: Sime Darby Property announced a proposed acquisition of Wisma UNIRAZAK, indicating an expansion of urban redevelopment exposure in Kuala Lumpur. The deal broadens the urban redevelopment pipeline and keeps activity tied to Kuala Lumpur's commercial real estate cycle in focus.

- January 2025: Gamuda Bhd bought 389 acres in Springhill Industrial Park, Port Dickson, for about USD 94.3 million. The land acquisition supports the group's capacity to pursue large-scale digital infrastructure projects and strengthens its industrial real estate portfolio.

- June 2024: Eco World opened the first phase of its Eco Horizon township in Batu Kawan, Penang, releasing 704 landed homes within a broader master plan. The launch added near-term residential supply near a semiconductor-linked growth area and reinforced the township model tied to industrial employment nodes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Malaysia real estate market is sized as the yearly value of property sales and leasing activity across residential and commercial real estate within Malaysia, expressed in current USD and aligned to observed pricing and demand indicators.

Scope exclusions: This sizing excludes construction contracting revenues and infrastructure project spending unless they directly flow into property sale values or rental income.

Segmentation Overview

- By Business Model

- Sales

- Rental

Data Validation & Update Cycle

We validate outputs by comparing model results with independent signals, including published transaction value summaries, lending direction, and consistency between price trends and absorption or occupancy. If the variance looks unusual, assumptions are reviewed in steps, and follow-up calls are triggered to clarify whether the issue is timing, scope, or a one-off event.

Before sign-off, an analyst review pass checks currency conversion timing, year alignment, and segment share logic so the totals reconcile cleanly. Reports are refreshed annually, and interim updates are made when material events occur, such as changes to lending rules, tax treatment, or foreign ownership policy. Right before delivery, a fresh scan is completed so clients receive the latest updated view.

Mordor Intelligence's Malaysia Analysis of Real Estate Market Size Versus Other Published Estimates

Published market values for Malaysia real estate can vary a lot because the underlying measurement is not always the same, and the inclusion of rentals, resale activity, and commercial leasing is handled differently. The spread also increases when different base years are chosen, or when currency timing and inflation assumptions are not aligned to the same period.

A frequent gap driver is that some figures lean toward an asset value style construct, while others focus on yearly monetized activity (sales plus rentals) that can be checked against transactions and credit signals. Another driver is how price and rent progression is projected, since extending a trend line without checking occupancy, take-up, and rate sensitivity can move the value sharply. Here, the sales and leasing activity lens is tied back to transaction values and lending conditions, a concrete modeling difference that explains why the 2025 total sits where it does for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 40.16 B (2025) | |

| Industry Research Publisher A | USD 84.90 B (2024) | This estimate appears to use a broader valuation pool for the country, which can resemble a stock or asset value view and can overstate annual sales and rental activity when compared on a like-for-like year basis. |

| Press Release Digest B | USD 22.15 B (2024) | This figure likely reflects a narrower captured value pool and a more conservative progression of prices and rents, which can undercount commercial leasing strength and city-level activity shifts. |

Taken together, the differences mostly come from what is being counted and how pricing and leasing are treated, rather than simple arithmetic. By linking the total to observable activity signals and then pressure testing assumptions through interviews, the final number remains transparent and easier to refresh each year.

Key Questions Answered in the Report

How large is the Malaysia real estate market in 2026?

The Malaysia real estate market size is USD 42.43 billion in 2026.

What is the forecast growth rate for Malaysia real estate through 2031?

The market is projected to rise at a 5.64% CAGR, reaching USD 55.82 billion by 2031.

Which city is growing fastest within Malaysia real estate?

Johor Bahru is expanding at a 6.78% CAGR due to strong cross-border and industrial catalysts.

Why are industrial properties in high demand?

Electronics and semiconductor investments, including Intel’s USD 7 billion plant, are absorbing land and warehouse supply.

What policy supports foreign buyers?

The revised Malaysia My Second Home program offers three tiers that allow visa holders to channel deposits into property purchases.

How is sustainability influencing new projects?

Bursa Malaysia’s ESG mandates and buyer preference for green, transit-linked homes are steering developers toward low-carbon, smart-home designs.

Page last updated on: