Aloe Vera-Based Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

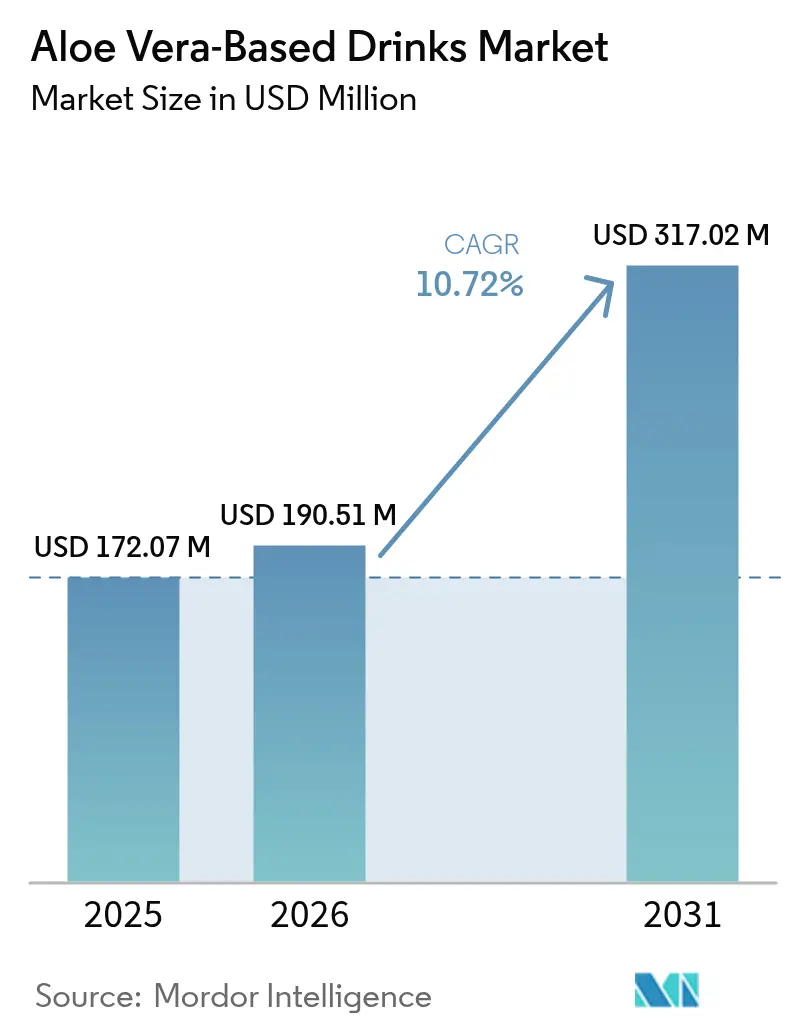

| Market Size (2026) | USD 190.51 Million |

| Market Size (2031) | USD 317.02 Million |

| Growth Rate (2026 - 2031) | 10.72% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aloe Vera-Based Drinks Market Analysis by Mordor Intelligence

Aloe Vera-based drinks market size in 2026 is estimated at USD 190.51 million, growing from 2025 value of USD 172.07 million with 2031 projections showing USD 317.02 million, growing at 10.72% CAGR over 2026-2031. Accelerated demand for functional beverages that enhance digestion and immunity drives this growth, while ready-to-drink formats eliminate preparation barriers and broaden mainstream appeal. Flavor engineering that softens aloe’s bitterness without compromising polysaccharide levels encourages repeat purchases, and organic certification enables brands to sustain price premiums in North America and Europe. The Asia-Pacific region keeps supply costs in check through extensive cultivation, whereas recent regulatory clarity in the European Union has opened a sizable new outlet for product launches. Competitive intensity remains moderate because raw-material volatility and strict quality standards deter rapid scale-up by newcomers.

Key Report Takeaways

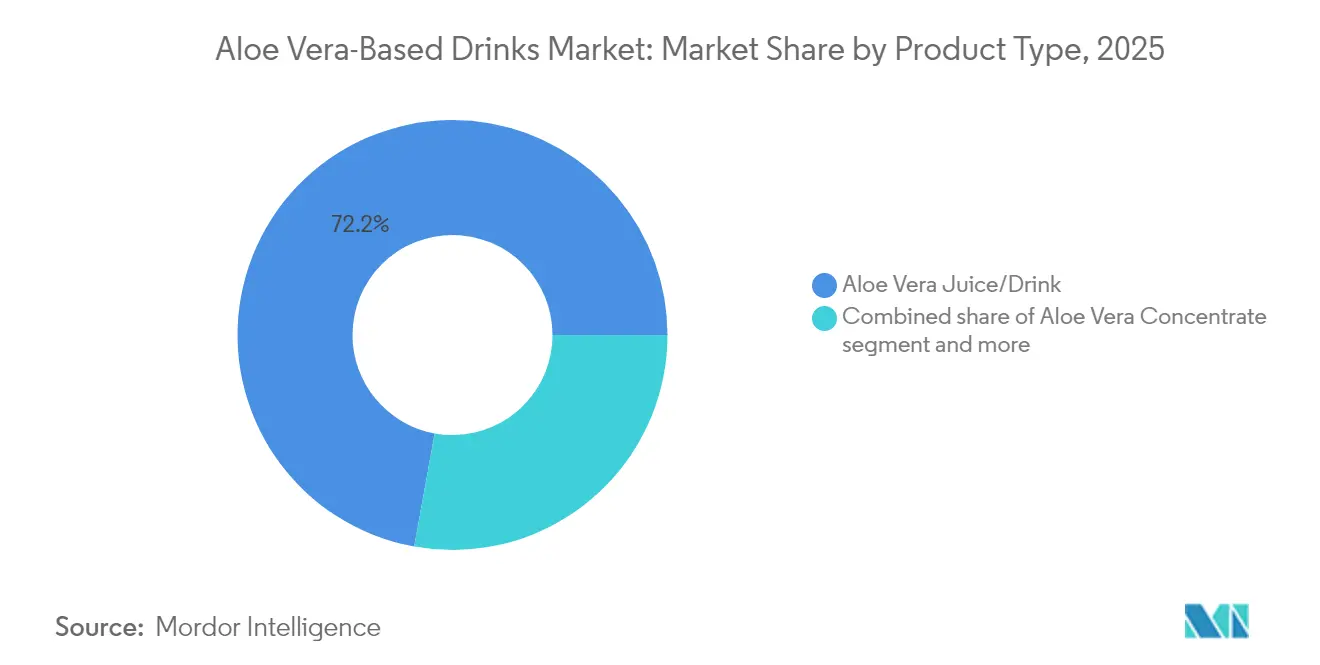

- By product type, Aloe Vera Juice/Drink led with 72.15% revenue share in 2025, while Aloe Vera Concentrate is expanding at 12.05% CAGR through 2031.

- By flavor, flavored variants captured 56.70% of the Aloe Vera-based drinks market share in 2025; the unflavored segment is forecast to grow at 11.58% CAGR.

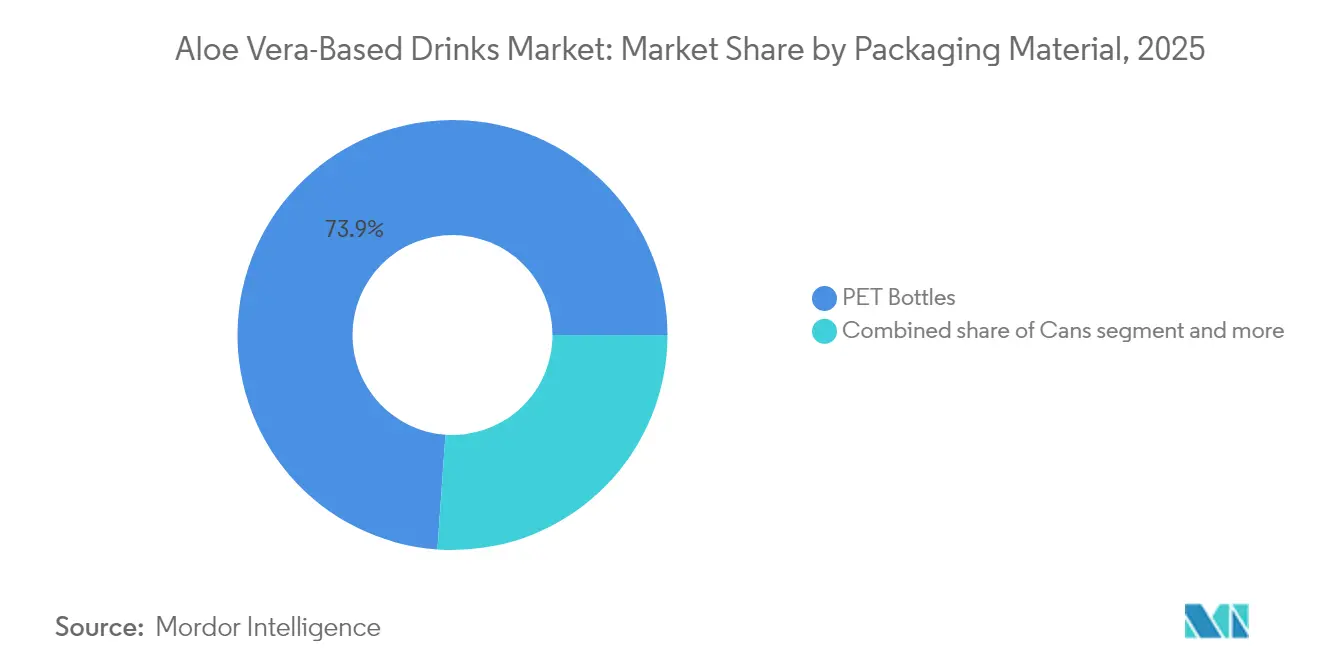

- By packaging, PET bottles accounted for 73.88% of the Aloe Vera-based drinks market size in 2025, whereas cans are projected to advance at a 11.39% CAGR.

- By channel, supermarkets and hypermarkets held a 41.05% share in 2025, and online retail is set to expand at a 12.62% CAGR to 2031.

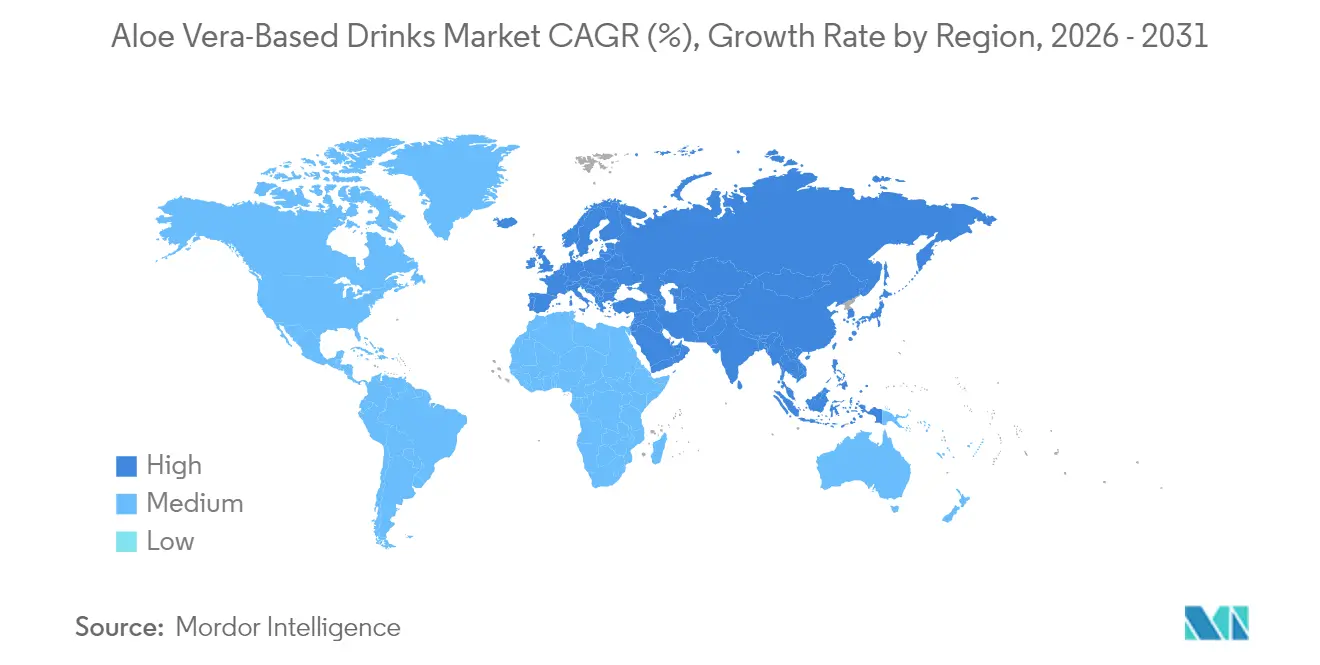

- By region, the Asia-Pacific region commanded 38.25% of the 2025 value; Europe is on track for the fastest growth, with a 12.37% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aloe Vera-Based Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Functional beverage preference | +2.1% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Digestive-health focus | +1.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| RTD format expansion | +1.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Flavor innovation | +1.3% | Global | Short term (≤ 2 years) |

| Premium and organic lines | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Low-calorie variants | +1.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Functional Beverages

Consumers are now allocating a greater portion of their beverage spending toward drinks that deliver measurable health benefits. Aloe’s acemannan content supports natural gut health claims, which resonate strongly with millennials and Gen Z shoppers. Supermarkets have responded by creating dedicated functional-drink sections, moving aloe from niche shelves into high-traffic aisles. The proliferation of adaptogens and probiotics in new blends deepens perceived wellness benefits and sustains price elasticity. These factors, together, underpin a structural rise in category shelf presence across developed retail markets.

Increasing Popularity of Natural Digestive-Health Products

Skepticism toward synthetic additives steers consumers toward botanicals with long medicinal histories. Aloe’s inner-leaf gel offers a recognizable solution, but standardizing acemannan levels remains an industry-wide hurdle. The International Aloe Science Council establishes voluntary benchmarks that enable premium brands to establish and maintain consumer trust. Regulatory frameworks such as 21 CFR Part 170 in the United States provide further guardrails for food-grade formulations[1]Source: U.S. Food and Drug Administration, “CFR Title 21, Parts 170–172,” fda.gov. Companies, therefore, stress inner-leaf extraction and low-aloin processes to meet both safety and efficacy expectations, according to The International Aloe Science Council.

Expansion of Ready-to-Drink (RTD) Formats

Single-serve PET bottles and aluminum cans let shoppers buy aloe drinks on impulse at gyms, transit hubs, and convenience stores. Large beverage groups are expanding their contract-packing capacity; a notable example is Suntory Oceania’s carbon-neutral plant in Queensland, which can fill more than 200 million liters annually, according to Krones AG[2]Source: Krones AG, “Carbon-Neutral Beverage Plant Reference,” krones.com. Smaller brands utilize such facilities to scale without incurring heavy capital investment, thereby ensuring a nationwide reach while focusing on ingredient sourcing and branding. RTD availability, therefore, broadens the Aloe Vera-based drinks market beyond core wellness aficionados.

Fruit and Herbal Flavor Innovations

Bitterness once limited the appeal of aloe, but blends with pineapple, mango, ginger, and turmeric now soften the taste while layering complementary health benefits. Balanced formulations must preserve enough aloe to sustain digestive-health claims, which forces close control of dilution ratios. Successful variants win mainstream listings where flavor drives repeat purchases. As retailers expand their functional-drink offerings, flavor diversity further distinguishes shelf propositions and mitigates the risk of commoditization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited functional-benefit awareness | -1.4% | Emerging markets, rural areas | Medium term (2-4 years) |

| Short shelf life | -1.6% | Regions lacking cold chain | Short term (≤ 2 years) |

| High production and input costs | -1.3% | North America, Europe | Long term (≥ 4 years) |

| Adulteration or quality inconsistency | -1.1% | Fragmented supply regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Awareness of Functional Benefits

Outside major urban centers, aloe remains better known as a topical cosmetic ingredient than as a drink. Educational campaigns are expensive, and health-claim regulations require robust clinical evidence, which smaller firms may struggle to fund. Certification logos are helpful, but their recognition remains low in developing regions. Over time, coordinated industry research could broaden understanding, although fragmentation among producers complicates joint outreach efforts.

Short Shelf Life for Minimally Processed Drinks

Fresh aloe gel loses its quality within hours of harvest, and minimally processed beverages last only one to two weeks when refrigerated. Regions without reliable cold-chain logistics, therefore, cannot stock raw-style formats. HTST pasteurization extends shelf life to several months while preserving more acemannan than UHT, but it incurs additional energy costs and may still compromise the fresh flavor. Concentrate, and powder alternatives unlock ambient shipping, but forfeit “raw” positioning, leaving marketers to balance reach and authenticity, according to the Engineers India Research Institute[3]Source: Engineers India Research Institute, “Project Report on Aloe Vera Cultivation and Processing,” eiriindia.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Efficiency Drives Concentrate Momentum

In 2025, juice and drink formats accounted for 72.15% of the Aloe Vera-based drinks market, underscoring shoppers' preference for grab-and-go convenience. Concentrates, although smaller, are advancing at a 12.05% CAGR because they ship lighter weight and co-pack close to the destination, which lowers unit logistics expenses. These savings are especially relevant for exporters in the Asia-Pacific who dilute and bottle nearer to North American and European consumers. Processing choices matter: hand-filleted gel maximizes polysaccharide retention, while whole-leaf grinding boosts yield but demands stricter aloin control. For concentrates, spray-drying and freeze-drying extend shelf stability to 24 months, although they require high energy, prompting interest in solar-drying pilots that reduce operating costs in tropical zones.

Commercial players also segment by usage occasion. Ready-to-drink bottles target hydration and digestion on the go, whereas concentrate sachets cater to smoothie bars and functional shot producers. The flexibility of concentrates supports private-label and food-service contracts, broadening revenue streams beyond retail shelves. Those dynamics position Aloe Vera-based concentrates to keep outpacing the overall Aloe Vera-based drinks market growth through the forecast horizon.

By Flavor Type: Transparency Spurs Unflavored Uptake

Flavored variants held 56.70% share in 2025, leveraging fruit and herb blends to offset aloe’s natural bitterness. Tropical pairings, such as pineapple and mango, convey freshness, while ginger or turmeric infusions layer on immune-boosting or anti-inflammatory cues. The critical constraint is dilution: excessive flavor bases can lower acemannan density below functional thresholds, so formulators fine-tune ratios to protect health claims. Retail buyers prioritize taste for repeat sales, making flavor leadership a pathway to prime shelf locations in broad-channel supermarkets.

Unflavored options, though historically niche, are gaining at 11.58% CAGR as clean-label consumers tolerate, and sometimes seek, the plant’s original taste. The segment benefits from e-commerce, where long-copy product pages explain purity credentials, and from specialty channels that allow sampling. Short ingredient lists, often just aloe gel, water, and ascorbic acid, strengthen trust. This minimalism is closely linked to organic certification, raising basket value but requiring dependable, high-grade supplies. As transparency expectations rise, the Aloe Vera-based drinks market will likely see converging flavor and purity propositions that widen consumer choice.

By Packaging Material: Sustainability Lifts Aluminum Cans

PET bottles still dominated 2025 volume at 73.88%, aided by established global recycling streams and clear visibility of product pulp. Yet environmental scrutiny has intensified, and bottle-to-bottle circularity remains below desired targets in several regions. Producers respond by lifting recycled-PET content, which raises costs by roughly 7% but helps meet retailer sustainability scorecards. Technical advances, such as light-blocking additives, now protect polysaccharides from UV degradation without resorting to opaque labels.

Aluminum cans are growing at an 11.39% CAGR, driven by recycling rates exceeding 90% in deposit-return markets like Germany and a solid consumer perception of can recyclability. Complete light exclusion further extends shelf life, a benefit for ambient logistics in hot climates. Design cues, such as matte finishes and pastel palettes, help reposition cans from a soft-drink heritage to a wellness territory. Cartons hold a smaller slice, but aseptic filling provides twelve-month stability that suits export consignments where port delays are common. Glass stays premium but faces freight-emission and breakage drawbacks that curb scale in the Aloe Vera-based drinks industry.

By Distribution Channel: Digital Platforms Expand Reach

Supermarkets and hypermarkets accounted for 41.05% of 2025 turnover, leveraging foot traffic and multi-tiered price promotions to spur trial. Listing fees, slotting allowances, and high margin requirements, however, weigh heavily on emerging brands. Convenience stores capitalize on the single-serve momentum among commuters, but route-to-market fragmentation limits their national coverage in many developing countries. Specialty health-food outlets nurture credibility and offer educational touchpoints, yet their narrow footprint caps volume potential.

Online retail, expanding at 12.62% CAGR, removes shelf-space constraints and supports subscription models that lock in monthly demand. Detailed product storytelling online addresses consumer doubts about taste and efficacy, fostering high repeat rates for trusted labels. Quick-commerce services further blur the line between digital and on-premise procurement by delivering chilled bottles within 30 minutes in major cities. Food-service and gym channels add incremental volume with attractive margins, though customized pack sizes and regulatory compliance for away-from-home consumption require extra operational attention. Together, these avenues ensure the Aloe Vera-based drinks market maintains diverse pathways to shoppers as habits evolve.

Geography Analysis

The Asia-Pacific region commanded 38.25% of the 2025 value, driven by the entrenched cultural acceptance of aloe in traditional remedies and its scalable cultivation bases in China, India, and South Korea. Rapid urbanization and the premiumization of RTD beverages provide brands with a receptive audience, while investments like Suntory’s carbon-neutral Queensland plant indicate confidence in continued demand for functional drinks. Challenges include fragmented farm structures and varying quality control regimes, which raise adulteration risks and complicate cross-border traceability. National initiatives in India to boost medicinal-plant acreage could expand supply, but high marketing costs and limited price supports still constrain farmer profitability.

Europe, freed from its prior food-use ban in late 2024, is now the fastest-growing region at a 12.37% CAGR. Germany, Spain, and Italy lead early adoption thanks to established organic food cultures, while the United Kingdom’s health-and-wellness retail ecosystem accelerates trial. EFSA oversight imposes strict aloin limits, raising compliance costs but assuring consumers of safety. Deposit-return schemes push aluminum-can recycling rates above 90%, aligning with sustainable packaging expectations that favor aloe drinks, positioned as eco-friendly. Supply remains tight as organic acreage lags demand, prompting closer sourcing ties between European fillers and growers in Mexico and Kenya.

North America presents a mature but still expanding opportunity anchored by high functional-beverage awareness and robust e-commerce penetration. U.S. organic food sales reached USD 63.8 billion in 2023 despite inflationary pressures. The USDA’s Organic Transition Initiative supports acreage growth, yet adoption momentum has been slower than hoped, leaving brands dependent on imported gel. Canada mirrors U.S. preferences but on a smaller scale and benefits from harmonized labeling rules that simplify cross-border distribution. Mexico, with arid regions suited to aloe cultivation, is a critical supplier, though producers must navigate certification audits to meet Northern buyers’ quality thresholds.

South America and the Middle East & Africa together account for a modest but rising share of the Aloe Vera-based drinks market. Brazil’s beverage majors have begun pilot aloe lines, but cold-chain constraints beyond big cities delay broad rollout. Argentina leverages proximity to cultivation zones, while Colombia explores solar-drying techniques that could give smallholders year-round income streams. In the Gulf Cooperation Council, affluent expatriate populations seek premium wellness drinks, yet extreme heat and logistical costs keep prices high. South Africa’s organized retail network provides a springboard for regional growth, although interrupted power supply occasionally disrupts refrigeration-dependent segments.

Regulatory Landscape

Aloe vera-based drinks are regulated primarily as foods, but enforcement tightens when labels imply disease treatment. In the United States, products positioned with therapeutic claims can be treated as unapproved new drugs under the Federal Food, Drug, and Cosmetic Act, while food-grade formulations must meet FDA requirements for ingredient safety and labeling, including guardrails used for food ingredients under 21 CFR Part 170.

In Europe, market access for aloe preparations shifted after the EU General Court annulled Commission Regulation (EU) 2021/468 on November 13, 2024 (in cases including Aloe Vera of Europe v Commission), which had restricted certain aloe leaf preparations containing hydroxyanthracene derivatives (HADs) under Regulation (EC) No 1925/2006. Even with that legal change, suppliers still face strict safety and quality expectations around aloin/HAD control and broader import compliance, including corporate due diligence and reporting obligations tied to supply-chain transparency such as the Corporate Sustainability Due Diligence Directive (CSDDD) and the Corporate Sustainability Reporting Directive (CSRD).

Competitive Landscape

The Aloe Vera-based drinks market remains moderately fragmented, with the five largest players setting quality and price benchmarks, yet collectively holding well under half of the global revenue. South Korea’s OKF leverages scale manufacturing and a broad certification portfolio to supply more than 180 countries. ALO Drink, headquartered in the United States, differentiates itself with fruit-forward recipes and transparent pulp visibility that appeal to mainstream grocery shoppers. Forever Living Products integrates beverages within a direct-selling ecosystem, sidestepping retail shelf fees and using distributor education to sustain high engagement. Lotte Chilsung Beverage enjoys domestic RTD strength and rapid product development cycles, while Herbalife offers aloe concentrates as rehydration adjuncts that seamlessly integrate into its nutrition programs.

Barriers to rapid market-share acquisition include raw-material price fluctuations, complex food-safety compliance requirements, and the technical challenge of balancing acemannan retention with shelf stability. Leading brands invest in HTST pasteurization and multi-stage filtration to maximize functional payloads without sacrificing taste. Certification and traceability now serve as competitive moats; OKF, for instance, highlights International Aloe Science Council seals to reassure buyers, and several North American start-ups utilize blockchain ledgers to log farm-to-bottle journeys. These systems add cost, yet they underpin premium positioning especially in online retail where ingredient provenance weighs heavily on purchase decisions.

Strategic partnerships shape expansion trajectories. Asian processors enter toll-packing agreements with European and U.S. brands to circumvent freight costs of finished beverages, while Western firms sign multiyear leaf supply contracts to lock in acemannan specifications. Product white spaces persist in low-calorie, monk-fruit-sweetened SKUs, and in functional blends that incorporate collagen or adaptogens. Consolidation remains plausible over the medium term as multinational beverage groups scout acquisitions to gain a foothold in the fast-growing Aloe Vera-based drinks industry.

Aloe Vera-Based Drinks Industry Leaders

ALO Drink (SPI West-Port)

Forever Living Products

Lotte Chilsung Beverage

Herbalife Nutrition

OKF Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory clarity in Europe following the November 2024 General Court decision that annulled Commission Regulation (EU) 2021/468 has reopened product-development and listing activity for compliant aloe drink formulations, while maintaining a premium on tight control of aloin/HAD content and supporting documentation. For brands and suppliers, this creates room to win listings by demonstrating inner-leaf sourcing, low-aloin processing, and third-party assurance, using frameworks and seals associated with bodies such as the International Aloe Science Council alongside mainstream food-safety certifications used by beverage co-packers.

Recent launches also point to more ingredient-forward positioning that matches functional-beverage shopping behavior. In February 2026, ALO Drink introduced not-from-concentrate, all-natural juice flavors (including 100% Passion Fruit and 100% Sugarcane formats) at Expo West, reinforcing demand for flavor innovation while keeping a clear aloe proposition. On the operations side, automation opportunities in peeling, filtration, and purification lines, including automated peeling and ultrafiltration steps used to remove aloin while protecting bioactives, can support scale-up and consistency, which is a differentiator in a category affected by quality variability and short shelf-life constraints.

Recent Industry Developments

- May 2026: Forever Living Products India introduced Aloe Herbal Infusion, a zero-calorie format positioned for hot or iced consumption. The launch extends aloe beyond RTD bottles into preparation-based wellness routines, adding new occasions for the brand without adding sugar or calories.

- March 2026: Forever Living Products India announced that its flagship Forever Aloe Vera Gel is now manufactured locally in India. Local production is intended to improve supply continuity and quality oversight while reducing lead times, supporting wider availability in a key Asia-Pacific market.

- April 2025: Grace Foods released price-marked packs for its Say Aloe drinks range in three flavors (Original, Strawberry, and Mango) in 500 ml bottles at GBP 1.15. The rollout targets high-velocity retail execution and affordability, helping drive trial and repeat purchase in mainstream channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers ready-to-drink beverages where aloe vera is a stated core ingredient, sold in mainstream and specialty channels, and counted at the value generated from selling these drinks to end buyers across major regions.

Scope exclusions: It excludes dietary supplement capsules, cosmetic-grade aloe inputs, and bulk aloe ingredients that are not sold as finished beverages.

Segmentation Overview

- By Product Type

- Aloe Vera Juice/Drink

- Aloe Vera Concentrate

- Others (Aloe vera Infused Water, Aloe Vera Mixed Juice, Aloe Vera Gel, and Others)

- By Flavor Type

- Flavored

- Unflavored/Natural

- By Packaging Material

- PET Bottles

- Cans

- Tetra-Pak and Cartons

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- South Africa

- United Arab Emirates

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the fact base that makes later assumptions easier to defend. We pull public information such as agriculture and crop statistics from sources like FAOSTAT, trade flows from UN Comtrade, and food safety guidance from agencies such as the US FDA and the European Commission.

To keep the model tied to what is actually sold, we also review product labeling rules, packaging and beverage-category notes from industry associations, and company filings and investor presentations for channel mix and geography cues. A paid subscription for company financials and news is used selectively to spot product launches and country expansion, and an import export shipment-level database is referenced when trade visibility adds clarity. These sources are not exhaustive, and many other public documents were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on checking what share of aloe-based SKUs truly qualify as aloe vera drinks, and how pricing and channel margins behave across regions. We spoke with brand and distribution-side respondents, along with packaging and ingredient-side experts, so the demand signals and supply constraints could be reconciled before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 40% |

| Mid tier: 53% | Functional/Unit leaders: 27% | EMEA: 34% |

| Smaller Players: 20% | Managers: 58% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build that uses beverage category sales direction, aloe-based drink penetration, and observed price bands to reconstruct value by region. The totals are then checked using selective bottom-up approximations, such as sampled SKU price points by pack type and an outlet-level volume sense from channel discussions, and the model is adjusted where the two views do not line up.

Inputs that matter in this market include the share of flavored versus natural products, packaging mix shifts across PET, cans, and cartons, online retail growth versus store-led sales, aloe raw material availability and quality compliance, and region-specific labeling or safety expectations that can limit launches. For forecasting, we use scenario analysis supported by a simple multivariate regression view, where growth is linked to functional beverage adoption, distribution expansion, and expected pricing movement, and then sanity-checked with what practitioners expect for new product velocity. When a sub-region has weak data, gaps are handled by using proxy indicators like import trends and comparable functional drink growth, followed by expert review before locking the final numbers.

Data Validation & Update Cycle

Outputs are validated through multiple checkpoints so that unusual jumps are explained before sign-off. We compare results against independent signals like trade direction, packaging format momentum, and channel feedback on pricing and repeat purchase, and then we re-check outliers at the country and region level.

A second analyst review is completed for assumption logic, and experts are re-contacted when new regulations, major launches, or supply shocks make earlier inputs stale. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is done so clients receive the latest updated view.

Mordor Intelligence's Aloe Vera Based Drinks Market Sizing Compared With Other Published Estimates

Published numbers for aloe vera based drinks can look far apart because the category boundary is interpreted differently, and the year used for the current market size is not always the same. Differences also come from how companies treat flavored blends, how they convert currencies, and whether their price assumptions reflect retail shelf prices or a closer-to-realized value.

Retail price checks across common pack sizes, plus channel feedback on online versus store-led mix, are the evidence points that keep Mordor Intelligence tied to a consistent finished-drinks scope, rather than letting adjacent aloe products inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 190.51 M (2026) | |

| Industry Publisher A | USD 131.67 M (2024) | Uses an earlier base year and may apply a narrower definition that misses newer aloe blend launches and recent channel expansion, which can depress the stated current value. |

| Global Publisher B | USD 146.80 M (2025) | Starts from a different base year and can rely on broad functional beverage growth assumptions, with limited clarity on whether value is tracked at retail or closer to realized pricing by channel. |

Taken together, the spread is largely explained by timing and by what gets counted as an aloe vera drink versus a broader aloe-related beverage set. By keeping the scope anchored to finished drinks and by using repeatable checks on pricing and channel mix, our estimate stays easier to trace back to clear variables and review steps.

Key Questions Answered in the Report

How large is the Aloe Vera-based drinks market projected to be by 2031?

It is forecast to reach USD 317.02 million by 2031, reflecting a 10.72% compound annual growth rate.

Which region currently leads global sales of aloe beverages?

Asia-Pacific holds the lead with 38.25% of 2025 revenue thanks to widespread cultivation and cultural familiarity with aloe.

What packaging format is growing fastest for aloe drinks?

Aluminum cans are advancing at 11.39% CAGR, driven by high recycling rates and light-blocking protection of active components.

Why are concentrates gaining traction among manufacturers?

Concentrated formats cut shipping weight and enable local dilution, trimming logistics costs by 15–20% compared with shipping ready-to-drink bottles.

What role does organic certification play in consumer choice?

Organic labels underpin premium pricing, especially in North America and Europe, and reassure buyers of low aloin levels and sustainable farm practices.

Page last updated on: