Ajinomoto Build-Up Film (ABF) Substrate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 17.65% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ajinomoto Build-Up Film (ABF) Substrate Market Analysis by Mordor Intelligence

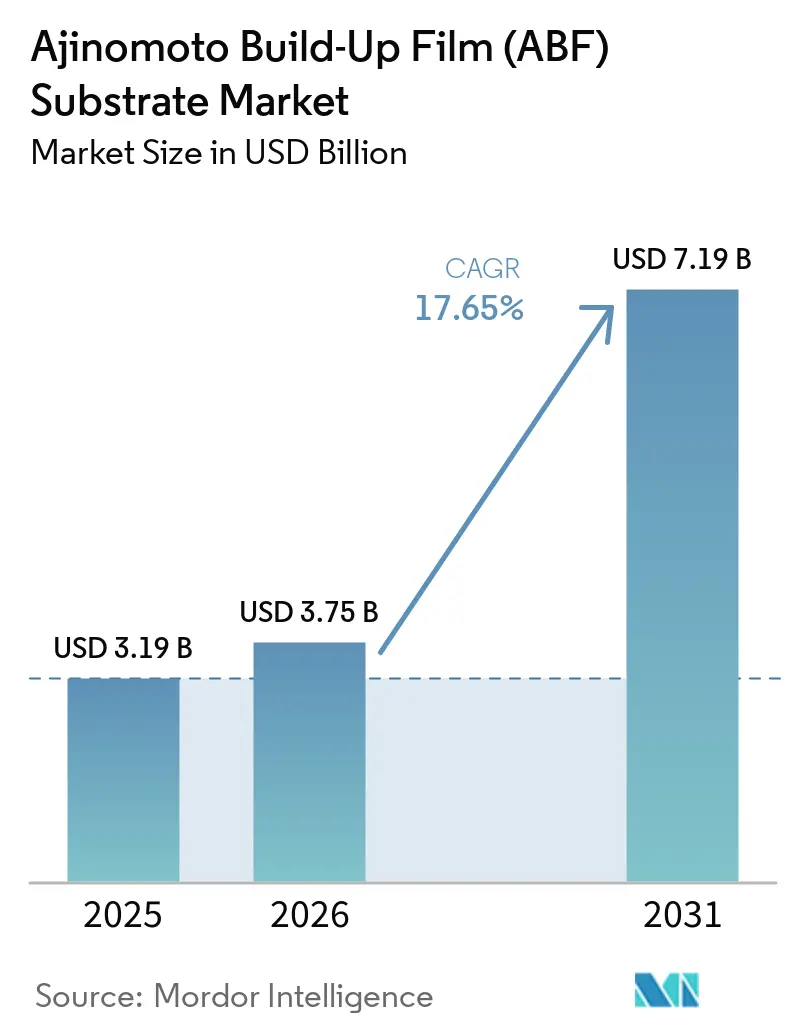

The Ajinomoto Build-Up Film substrate market size is projected to expand from USD 3.19 billion in 2025 and USD 3.75 billion in 2026 to USD 7.19 billion by 2031, registering a 17.65% CAGR between 2026 and 2031. Surging demand for larger, higher-layer-count substrates in artificial intelligence (AI) servers, coupled with multi-billion-dollar capacity expansions in Taiwan and Japan, is stretching the existing supply base. Flip-chip ball grid array (FC-BGA) remains the workhorse package as it routes more than 10,000 signals at thermal design powers exceeding 300 W, while early pilot runs of glass-core substrates have started but will not reach volume until after 2027. Hyperscalers are moving first, locking long-term supply agreements ahead of the 18-to-24-month qualification cycle, and are simultaneously funding North American and European build-outs to de-risk a supply chain still concentrated in East Asia. Incumbents with mature yield learning curves are reinforcing their lead by integrating sub-10 µm lithography, automated in-line inspection and feed-forward lithography to cut defect escape rates.

Key Report Takeaways

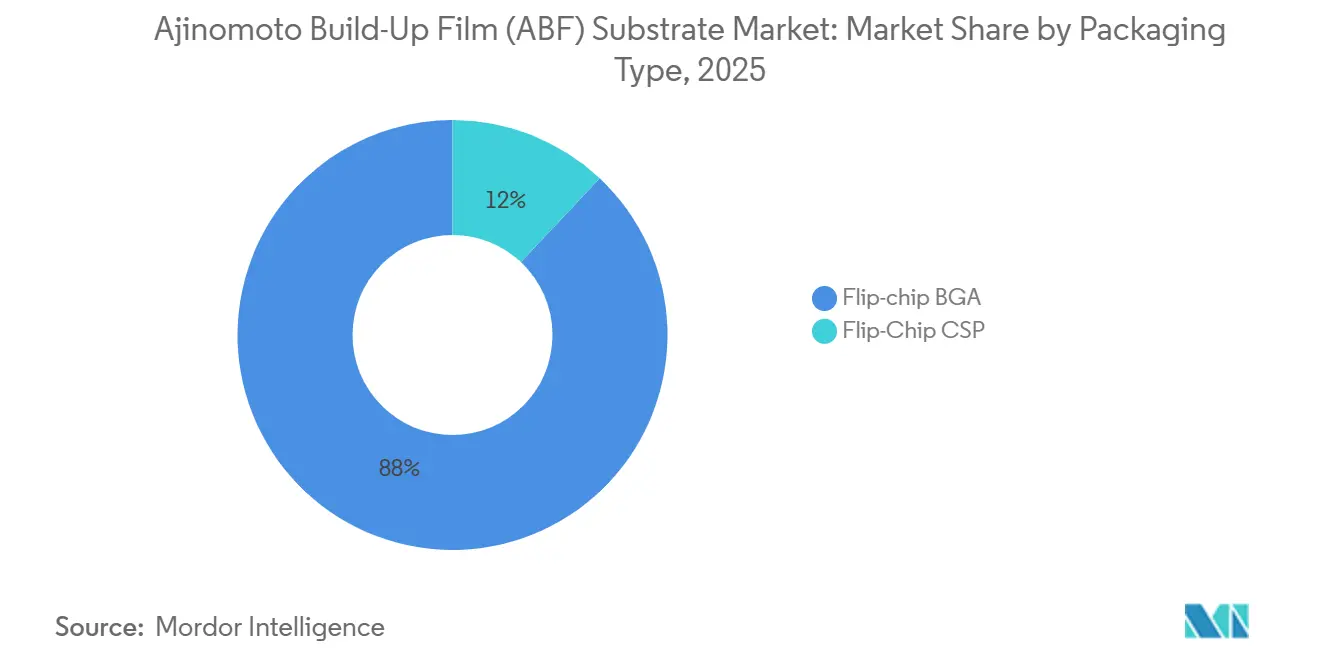

- By package type, flip-chip ball grid array led with an 88% revenue share in 2025, while the same segment is forecast to post an 18.05% CAGR through 2031.

- By application, AI GPUs commanded 47% of the 2025 value, whereas AI accelerators are projected to advance at an 18.15% CAGR over 2026-2031.

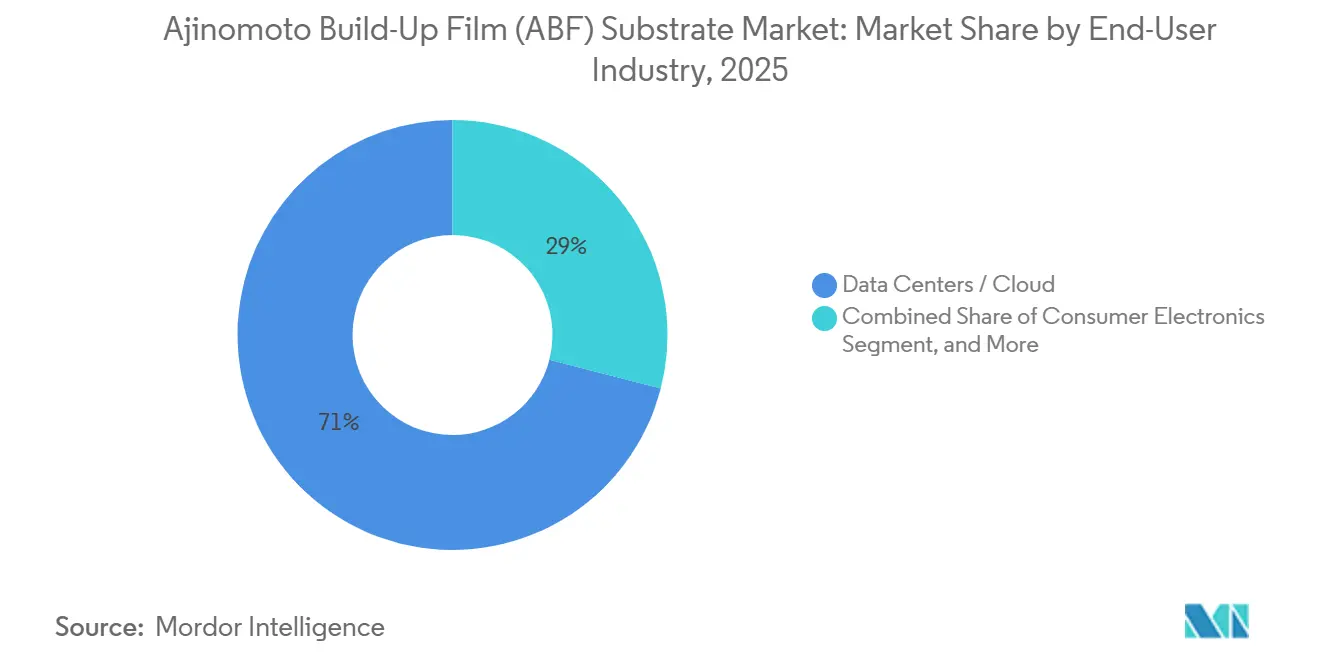

- By end-user industry, data centers and cloud infrastructure accounted for 71% of demand in 2025, yet automotive electronics is expected to record the fastest growth, with a 18.18% CAGR to 2031.

- By geography, Asia-Pacific held a 58% share in 2025, while North America is set to grow the quickest with an 18.65% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ajinomoto Build-Up Film (ABF) Substrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of ABF Substrates in AI GPU Packages | +5.0% | Global, Asia-Pacific and North America data-center hubs | Short term (≤ 2 years) |

| Shift Toward Chiplet Architectures Requiring Large-Area Substrates | +3.6% | Global, led by North America and Asia-Pacific hyperscalers | Medium term (2-4 years) |

| Capacity Expansion of Leading Substrate Makers in Taiwan and Japan | +3.3% | Asia-Pacific core, spillover to Southeast Asia | Medium term (2-4 years) |

| Advanced Lithography Integration for Sub-10 µm Lines and Spaces | +2.0% | Taiwan, Japan, South Korea | Long term (≥ 4 years) |

| Strategic Long-Term Supply Agreements With Hyperscalers | +1.7% | North America and Asia-Pacific cloud regions | Medium term (2-4 years) |

| Localization Incentives Under CHIPS and Similar Acts | +1.1% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of ABF Substrates In AI GPU Packages

Next-generation AI GPUs such as NVIDIA H200 and AMD MI300 require 12-to-20 build-up layers, sub-15 µm lines and spaces, and coefficient of thermal expansion (CTE) matching within 2 ppm / °C to mitigate warpage, pushing Ajinomoto Build-Up Film substrate market demand to record highs. Ibiden earmarked JPY 500 billion (USD 3.3 billion) for two Japanese fabs that will begin sequential ramp in fiscal 2027, explicitly aimed at these GPUs.[1]Ibiden Co. Ltd., “Notice Regarding Capital Investment for High-Performance IC Package Substrates,” ibiden.com Multi-chiplet layouts double the substrate area per package, and Ajinomoto, which controls over 95% of the ABF dielectric film supply, has announced a 50% capacity increase by 2030 to keep pace. With qualification lead times longer than a year, supply stays tight through at least 2027, granting early movers pricing power.

Shift Toward Chiplet Architectures Requiring Large-Area Substrates

Disaggregated compute tiles in AMD Bergamo or Intel Meteor Lake significantly increase substrate real estate by 40-60%, creating a need for routing densities of 2,000 nets/mm² and up to 24 layers. This increase in design complexity has driven manufacturers like Nan Ya Printed Circuit Board to develop 24-plus-layer substrates that aim to achieve sub-15 µm geometries by 2026. However, as multiple high-value dice are integrated onto a single laminate, the economic risk associated with a single killer defect rises substantially. To mitigate this risk, suppliers are adopting advanced technologies such as feed-forward adaptive lithography and high-speed optical inspection systems. These measures are designed to detect and address issues like particles or residue early in the production process, specifically before the lamination stage, ensuring higher yields and improved reliability.

Capacity Expansion Of Leading Substrate Makers In Taiwan And Japan

Unimicron, Nan Ya PCB, Ibiden, and Shinko have collectively pledged investments exceeding USD 10 billion during the period from 2025 to 2026, aiming to increase their production capacity by 50-80% by fiscal 2028. Kinsus, as part of this expansion effort, is allocating USD 744 million specifically to expand its Flip-Chip Ball Grid Array (FC-BGA) production lines. Despite these significant investments, Kinsus management anticipates that the market will remain undersupplied of FC-BGA products through early 2027. These brownfield projects are strategically positioned within Taiwan's well-established outsourced semiconductor assembly and test (OSAT) corridor. This location offers advantages such as reduced freight costs and shorter qualification times. However, it also heightens geopolitical risks in the region, which could pose challenges to the supply chain and overall market stability.

Advanced Lithography Integration For Sub-10 µm Lines And Spaces

Maskless lithography and vacuum-etch stacks are increasingly adopted as wet-etch processes struggle to achieve sub-10 µm resolution due to issues such as undercutting. To address these challenges, Ibiden has allocated a portion of its JPY 500 billion (USD 3.3 billion) investment program to the development and deployment of advanced steppers. Meanwhile, Kyocera is advancing its efforts by commercializing a ceramic-core substrate with 75 µm vias, designed to mitigate warpage issues commonly encountered in ultra-large packages. The initial adopters of these technologies are AI GPUs, followed closely by server CPUs, as these segments demand cutting-edge solutions. However, cost-sensitive sectors such as consumer electronics and automotive devices are expected to adopt these advancements at a slower pace, likely not until after 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity and Long Equipment Lead Times | -2.2% | Global, especially North America and Europe | Medium term (2-4 years) |

| Process Yield Challenges Above 10 Build-Up Layers | -1.6% | Asia-Pacific advanced facilities | Short term (≤ 2 years) |

| Short-Term Oversupply Risk From Aggressive Capacity Adds | -1.0% | Asia-Pacific core commodity lines | Short term (≤ 2 years) |

| Emergence of Alternative Glass and RDL-First Technologies | -0.8% | North America and Asia-Pacific R&D hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity And Long Equipment Lead Times

Greenfield fabs require investments ranging from USD 800 million to USD 1.2 billion and face a 12-18 month wait to procure essential equipment, such as laser drillers or vacuum laminators. These high costs and extended timelines effectively exclude smaller entrants from competing in the market. A case in point is Amkor’s Arizona plant, where construction commenced in late 2025. Despite receiving USD 407 million in CHIPS funding, the facility only began generating revenue in the first half of 2028, highlighting the lengthy lead times associated with such projects.[2]Amkor Technology Inc., “Q1 2026 Earnings,” amkor.com Additionally, tool vendors, which operate as oligopolies, tend to prioritize their established customers. This practice creates high cost and supply chain challenges for new market entrants, further solidifying the barriers to entry in this space.

Process Yield Challenges Above 10 Build-Up Layers

Each additional layer in the manufacturing process increases the risk of defect escape by 2-3%, and even a single short circuit or open connection can render a multi-chiplet module, valued at thousands of dollars, completely unusable. Unimicron’s reported yield gap relative to Ibiden on 16-layer boards led to the loss of NVIDIA design wins in 2024, underscoring the critical importance of maintaining high production standards. To address these challenges, suppliers are now employing external metrology techniques and off-tool alignment methods to effectively manage warpage issues. However, despite these advancements, the learning curves for optimizing these processes still span 12-18 months, reflecting the complexity and precision required in this domain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Type: Flip-Chip BGA Underpins Performance Computing

The Ajinomoto Build-Up Film market size for FC-BGA accounted for 88% in 2025 and is expected to grow at a 18.05% CAGR alongside the overall segment. FC-BGA enables direct solder bump interconnects that minimize inductance and support >10,000 signals, indispensable for AI accelerators and server CPUs. Ibiden’s Kawama and Ohno plants are fully dedicated to FC-BGA lines aimed at AI servers. Automotive-qualified versions passed AEC-Q100 in 2025, positioning Samsung Electro-Mechanics to capture rising zonal ECU demand.

FC-CSP held the remaining share, primarily catering to mobiles and wearables, where physical height constraints take precedence over raw bandwidth capabilities. The growth in FC-CSP volume is limited as semiconductor capital investments increasingly shift focus toward data centers, which demand higher performance and bandwidth. However, FC-CSP continues to play a significant role in supporting edge AI SOCs with TDPs under 20 W. Suppliers in this segment capitalize on well-established, mature 15-20 µm design rules, enabling them to maintain a competitive edge in cost efficiency while addressing the specific needs of these applications.

By Application: AI Accelerators Speed Past Legacy Compute

The Ajinomoto Build-Up Film (ABF) market share for AI GPUs was recorded at 47% in 2025, reflecting its dominance in this segment. However, even more significant growth is anticipated for custom tensor, neural, and inference chips, which demonstrated a robust compound annual growth rate (CAGR) of 18.15%. These chips, including Google’s TPU v5, AWS Trainium, and Meta’s in-house silicon, utilize substrates designed with advanced power-delivery networks and more than 15,000 vias. To capitalize on this trend, Zhen Ding has committed CNY 40 billion (USD 5.6 billion) to shift 70% of its revenue focus toward such accelerators by 2028, underscoring the strategic importance of this market.

While server CPUs remain a critical component of the market, they are now considered a mature segment, experiencing single-digit growth rates as hyperscalers extend their hardware refresh cycles. On the other hand, networking integrated circuits (ICs) are experiencing increased demand as AI fabric infrastructure expands. This is particularly evident in the case of 1.6 Tb Ethernet switch application-specific integrated circuits (ASICs) from companies like Broadcom and Marvell, which require precise controlled-impedance routing. Substrates used in this segment typically feature 8-12 layers, representing a moderate increase compared to AI GPUs. Despite this, they remain heavily reliant on ABF materials, underscoring their importance in the supply chain.

By End-User Industry: Automotive Emerges As Fastest Riser

Ajinomoto Build-Up Film substrate market size for data centers accounted for 71% of total demand in 2025. This growth is driven by hyperscaler capital expenditures, which are directly channeled into high-layer substrates. These investments often involve multi-year agreements, providing suppliers with a buffer against cyclical market fluctuations. Automotive applications, while representing only 7% of the market in 2025, are experiencing the fastest growth with a compound annual growth rate (CAGR) of 18.18%. This surge is attributed to the increasing adoption of Level 2+ and Level 3 autonomous driving systems, which require compute platforms capable of delivering over 1000 TOPS while operating in extreme temperature ranges of −40 °C to 125 °C. Samsung’s 10,000-bump FC-BGA, qualified in 2025, is specifically designed to meet these stringent requirements.

In addition to data centers and automotive applications, the telecom sector is also driving demand for Ajinomoto Build-Up Film substrates, particularly with the ongoing rollout of 5G standalone networks. These advancements are driving the need for more sophisticated substrates to support the high-performance requirements of modern telecom infrastructure. Meanwhile, the consumer electronics segment is witnessing a slowdown due to lengthening device refresh cycles, which has tempered its contribution to the overall market growth. Despite this, the combined demand from the data center, automotive, and telecom sectors continues to underscore the importance of Ajinomoto Build-Up Film substrates in enabling next-generation technologies across industries.

Geography Analysis

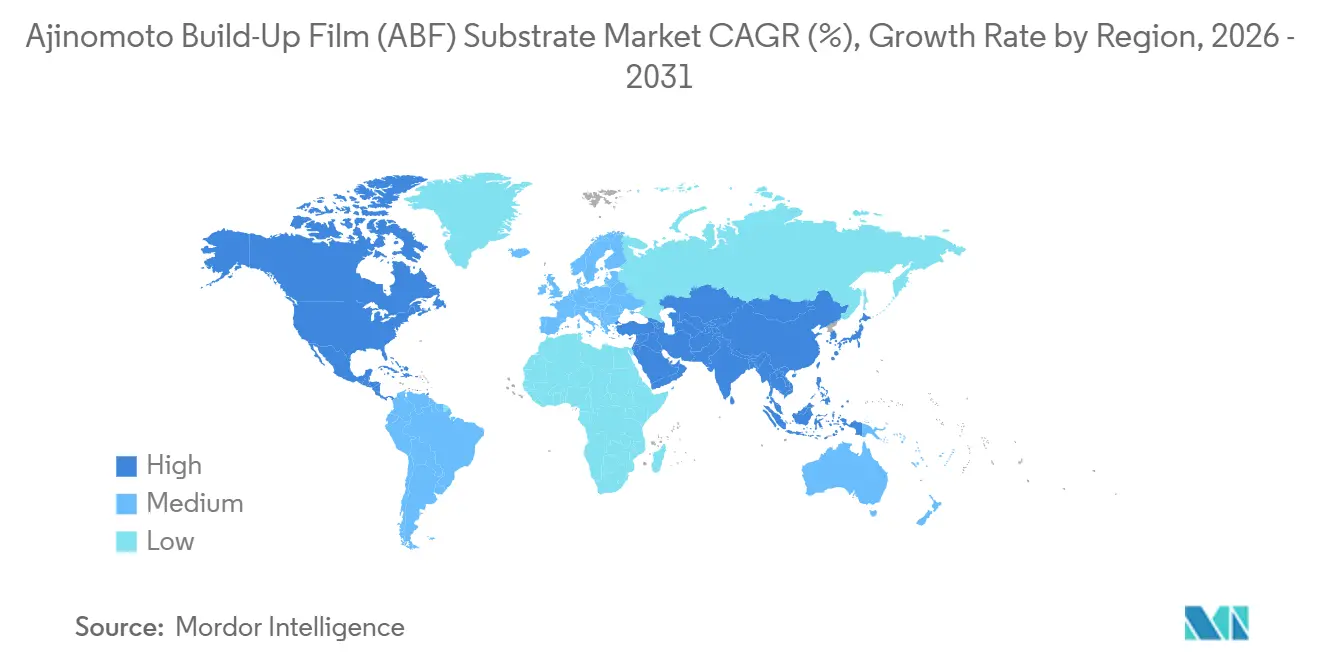

Asia-Pacific is expected to dominate the market, accounting for 58% of the 2025 value. Taiwan’s Unimicron, Nan Ya PCB, and Kinsus are strategically clustered around TSMC CoWoS lines, driving regional growth.[3]Kinsus Interconnect Technology, “2026 Investor Day,” kinsus.com Despite Kinsus’ USD 744 million expansion efforts, the near-term supply gap persists, leaving the region vulnerable to disruptions. Any geopolitical tensions or natural disasters, such as earthquakes, could potentially erase 6-12 months of supply. Japan is also a key player in the region, with Ibiden and Shinko investing a combined JPY 560 billion (USD 3.75 billion) to maintain high-layer technology expertise locally. Meanwhile, South Korea’s Samsung Electro-Mechanics and LG Innotek are channeling investments into Vietnam to leverage lower labor costs, although they continue to act as technology gatekeepers.

North America, although starting from a smaller base, is projected to experience the fastest growth with a compound annual growth rate (CAGR) of 18.65%. The CHIPS Act has provided significant grants, including USD 407 million to Amkor and USD 75 million to Absolics, signaling strong governmental support for the sector. However, the long payback period for greenfield projects remains a challenge. Companies like TTM Technologies are poised to benefit once domestic substrate lines achieve qualification. Additionally, hyperscalers are increasingly incorporating North American suppliers into their dual-sourcing strategies, further boosting the region’s potential for growth.

Europe maintains a niche position in the market, led by AT&S’s EUR 500 million (USD 540 million) competence center in Austria. The region benefits from the demand for high-quality standards such as ISO 26262 and IATF 16949, particularly from automotive OEMs and industrial automation players. These stringent requirements help shield local suppliers from competition with low-cost Asian manufacturers. Elsewhere, Vietnam is emerging as a significant assembly hub, driven by investments from companies like Samsung and Meiko. In contrast, South America and the Middle East currently hold negligible positions in the market, with limited activity in these regions.

Competitive Landscape

The market structure remains oligopolistic, with Ibiden, Unimicron, and Nan Ya PCB collectively controlling approximately 60% of AI-grade capacity. These companies are securing their positions by integrating multi-year take-or-pay agreements into their capital expenditure schedules, ensuring dominance before alternative technologies like glass-core or ceramic substrates gain significant traction. Notable investments include Samsung Electro-Mechanics’ KRW 1.8 trillion (approximately USD 1.35 billion) facility in Vietnam, AT&S’s advanced triple cleanroom in Austria, and Shennan Circuits’ CNY 6 billion (USD 0.84 billion) domestic expansion, all of which highlight the capital-intensive nature of this field.

Technical differentiation in the market is primarily driven by achieving high yields on substrates with more than 16 layers. Ibiden leads the industry with external optical metrology, enabling yields exceeding 90% on 20-layer boards. Unimicron, while slightly behind, has recently achieved NVIDIA qualification after implementing adaptive-shot lithography. Additionally, Onto Innovation’s inspection stack is becoming a standard tool integrated into brownfield expansions, raising the technological benchmark for new entrants and reinforcing the competitive edge of established players.

Emerging disruptors, particularly Chinese companies, are leveraging state support to scale their operations and compete in the market. Shennan Circuits aims to produce 200 million FC-BGA units annually, while Zhen Ding is targeting a 70% AI revenue mix by 2028.[4]Shennan Circuits Co. Ltd., “2025 Annual Report,” sz-sc.com Meanwhile, Kyocera is taking a different approach by bypassing the organic core race and introducing a 75 µm-via ceramic solution, which is well-suited for 2.5D interposers larger than 100 mm. Despite these advancements, the lengthy qualification processes and the significant capital expenditure required suggest that market concentration is likely to persist through 2031.

Ajinomoto Build-Up Film (ABF) Substrate Industry Leaders

Ibiden Co., Ltd.

Unimicron Technology Corp.

Nan Ya Printed Circuit Board Corporation

Shinko Electric Industries Co., Ltd.

AT&S Austria Technologies & Systemtechnik AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kyocera commercialized a multilayer ceramic-core substrate with 75 µm vias, marketed for AI accelerators and large 2.5D interposers.

- April 2026: Meiko Electronics set up a Vietnam subsidiary, budgeting JPY 50 billion (approximately USD 0.33 billion) for an FC-BGA plant focused on AI servers.

- February 2026: Ibiden approved a JPY 500 billion (USD 3.35 billion) program expanding Kawama and Ohno for high-layer AI substrates, with a sequential ramp from fiscal 2027.

- November 2025: Samsung Electro-Mechanics shipped pilot glass-core substrates and committed KRW 1.8 trillion (approximately USD 1.35 billion) to Vietnam for full utilization by H2 2026.

Global Ajinomoto Build-Up Film (ABF) Substrate Market Report Scope

The Ajinomoto Build-Up Film (ABF) Substrate Market refers to the global industry focused on the production, supply, and integration of ABF-based semiconductor substrates used in high-performance integrated circuit (IC) packaging. ABF substrates are advanced organic build-up films that enable fine-line circuitry, high layer counts, and superior electrical performance, making them essential for supporting high-speed, high-density chips used in modern computing applications.

The Ajinomoto Build-Up Film Substrate Market Report is Segmented by Package Type (Flip-chip BGA, and Flip-chip CSP), Application (AI GPUs, CPUs, AI Accelerators, and Networking ICs), End-user Industry (Data Centers, Consumer Electronics, Automotive, and Telecom), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). Market Forecasts are Provided in Terms of Value (USD).

| Flip-chip BGA |

| Flip-chip CSP |

| AI GPUs |

| CPUs (Server and Desktop) |

| AI Accelerators (TPUs, NPUs, Custom ASICs) |

| Networking / Data Center ICs |

| Data Centers / Cloud |

| Consumer Electronics |

| Automotive (ADAS, Autonomous Compute) |

| Telecom and Networking |

| North America |

| Europe |

| Asia-Pacific |

| Rest of the World |

| By Package Type | Flip-chip BGA |

| Flip-chip CSP | |

| By Application | AI GPUs |

| CPUs (Server and Desktop) | |

| AI Accelerators (TPUs, NPUs, Custom ASICs) | |

| Networking / Data Center ICs | |

| By End-user Industry | Data Centers / Cloud |

| Consumer Electronics | |

| Automotive (ADAS, Autonomous Compute) | |

| Telecom and Networking | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Key Questions Answered in the Report

What is the current Ajinomoto Build-Up Film substrate market size?

The Ajinomoto Build-Up Film substrate market size reached USD 3.19 billion in 2025 and is estimated at USD 3.75 billion in 2026.

Which package type leads demand?

Flip-chip ball grid array holds the dominant share, accounting for 88% of 2025 revenue due to its ability to accommodate >10,000 I/O pads for AI and server chips.

Why is North America the fastest-growing region?

CHIPS Act funding and hyperscaler dual-sourcing strategies are driving an 18.65% regional CAGR between 2026-2031 despite higher labor and permitting costs.

How are suppliers addressing high-layer yield loss?

Incumbents deploy external optical inspection, adaptive-shot lithography and tighter ABF handling to push yields above 90% on 16-plus-layer boards.

Are glass-core substrates a near-term threat to ABF?

Commercial glass cores will not ship in volume until after 2027, making them complementary rather than an immediate replacement for ABF.

Which end-user segment will grow fastest?

Automotive advanced driver-assistance systems and autonomous compute units are forecast to expand at an 18.18% CAGR through 2031 as vehicles adopt centralized zonal architectures.

Page last updated on: