Airport Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

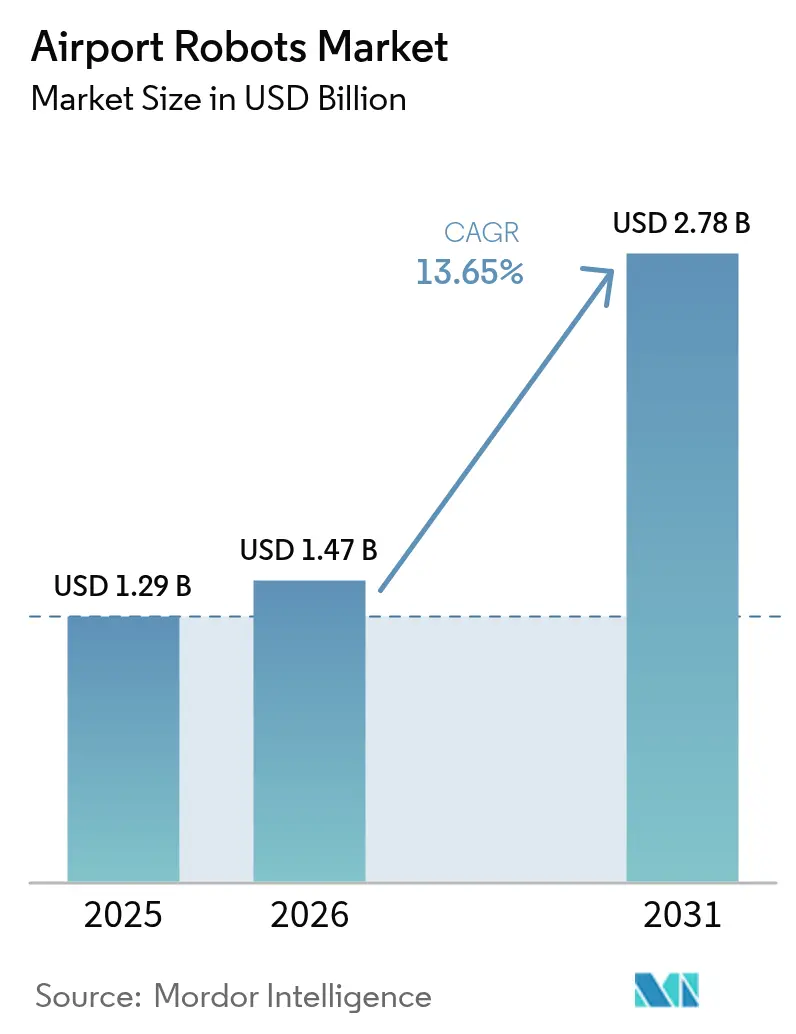

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 13.65% CAGR |

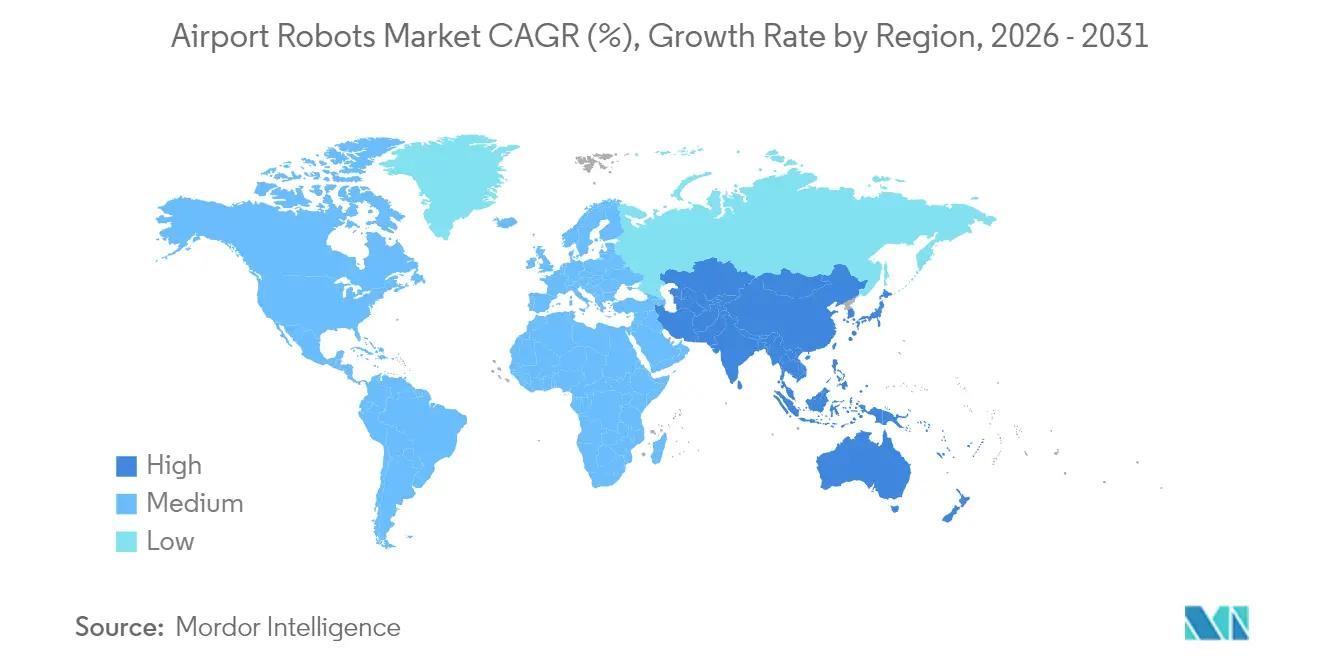

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Robots Market Analysis by Mordor Intelligence

Airport robots market size in 2026 is estimated at USD 1.47 billion, growing from 2025 value of USD 1.29 billion with 2031 projections showing USD 2.78 billion, growing at 13.65% CAGR over 2026-2031. Passenger-volume recovery, labor shortages, and airport digitization strategies underpin this growth outlook, with operators prioritizing automation to add capacity without expanding physical infrastructure. Terminal deployments dominate investment decisions because information, security, and cleaning tasks deliver immediate efficiency improvements visible to travelers. Landside functions, especially autonomous parking and curbside logistics, advance quickly as sensor suites mature and regulatory pilots expand. Regionally, Asia-Pacific’s manufacturing base and aggressive innovation programs are pushing down hardware costs, while North America benefits from federal security standards that accelerate safety-critical use cases. Suppliers that bundle purpose-built robots, middleware, and AI analytics are securing longer-term service contracts that boost recurring revenue.

Key Report Takeaways

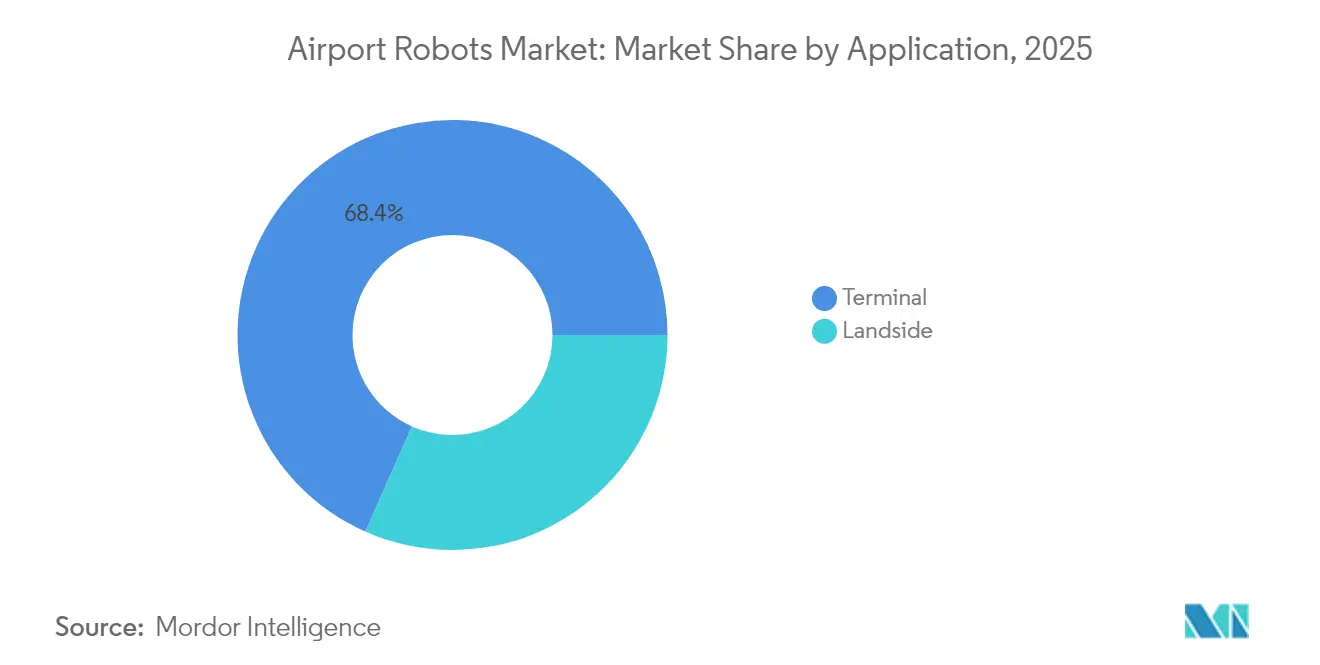

- By application, terminal operations captured 68.35% of revenue in 2025, while landside solutions are projected to expand at a 14.32% CAGR through 2031.

- By robot type, non-humanoid platforms held a 71.62% share in 2025, whereas humanoid units are forecasted to grow at a 15.28% CAGR over the same period.

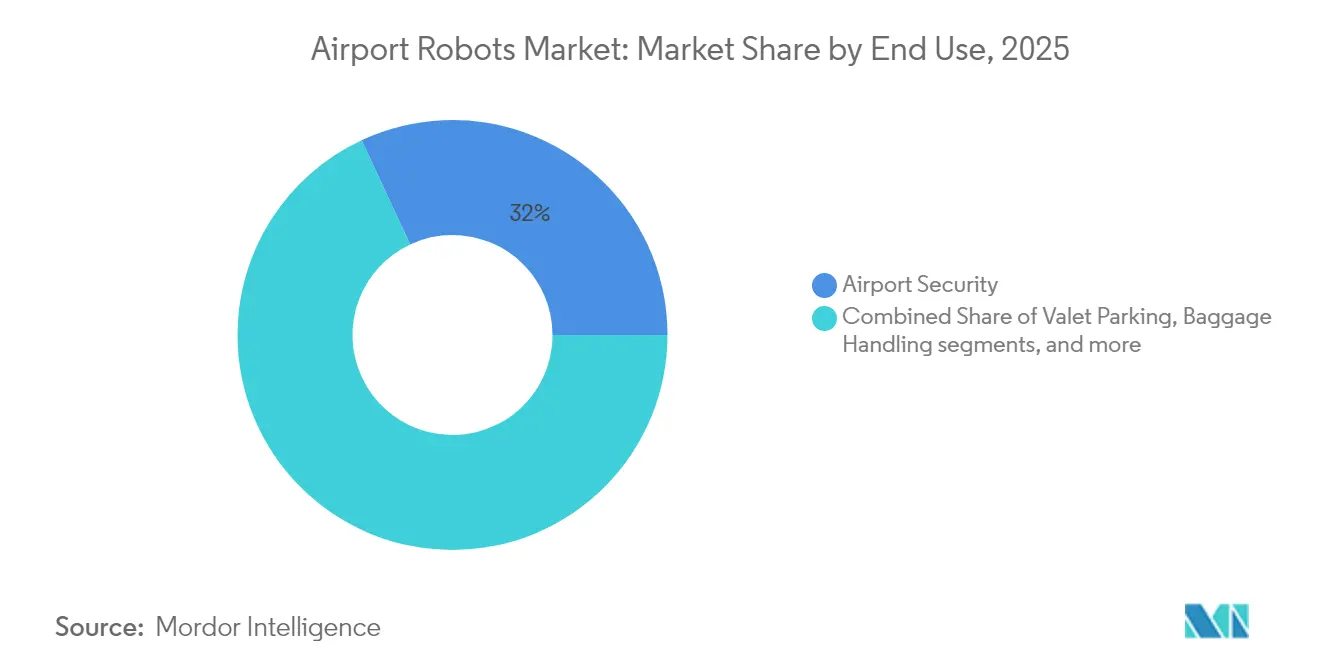

- By end use, security systems led with 31.95% of the airport robots market share in 2025; cleaning and disinfection robots are advancing at a 15.89% CAGR to 2031.

- By geography, North America accounted for 32.10% of global revenue in 2025, while Asia-Pacific is set to post the fastest expansion at 16.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Airport Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing passenger volumes driving demand for airport process automation | +3.2% | Global, peak in APAC and North America | Medium term (2-4 years) |

| Operational cost pressures and labor shortages accelerating robotic adoption | +2.8% | Global, acute in developed markets | Short term (≤2 years) |

| Heightened hygiene standards boosting deployment of cleaning and disinfection robots | +2.1% | Global, sustained in high-traffic hubs | Medium term (2-4 years) |

| AI-powered computer vision enhancing passenger screening and security efficiency | +1.9% | North America and EU leading, expanding to APAC | Long term (≥4 years) |

| Carbon-neutral initiatives encouraging adoption of autonomous valet parking systems | +1.4% | EU and select North American airports | Long term (≥4 years) |

| Deployment of collaborative humanoid robots to improve passenger experience and retail engagement | +1.2% | APAC core, spill-over to premium global airports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Passenger Volumes Driving Airport Process Automation

IATA projects passenger numbers will double by 2037, and airports are leveraging robotics to raise throughput without adding new terminals. Frankfurt Airport’s 2025 rollout of AI-enabled security scanners shortened checkpoint wait times while keeping staffing levels flat. Singapore Changi’s Living Lab integrates autonomous baggage tractors and food-delivery bots, proving end-to-end automation can scale for peak traffic. These deployments demonstrate that robots, sensors, and orchestration software add virtual capacity faster than brick-and-mortar expansion. As international traffic normalizes, airports expect robotic assets to handle routine tasks so personnel can focus on exception management. Growth momentum remains strongest in hubs handling more than 50 million passengers annually, where marginal capacity gains yield disproportionate revenue upside.

Operational Cost Pressures and Labor Shortages Accelerating Robotic Adoption

Global baggage-handling units report vacancy rates exceeding 25%, driving procurement of lifting robots that operate 24/7 in confined spaces. Amsterdam Schiphol expanded a pilot to 19 baggage robots capable of manipulating 80-90% of standard luggage pieces. SoftBank Robotics documented 10,000 robot cleaning hours across 15 US sites, freeing custodial staff for high-value tasks. Robots reduce overtime budgets, mitigate injury claims, and improve service-level consistency, strengthening return-on-investment arguments even in low-margin airports. Vendors are now bundling leasing and outcome-based payment models that align capital outlays with realized productivity savings, easing board-level funding approvals.

Heightened Hygiene Standards Boosting Cleaning and Disinfection Robot Deployment

Pandemic-era cleanliness expectations persist, with autonomous scrubbers and UV-C robots maintaining high-frequency cycles without exposing workers to biohazards. Hong Kong International deployed UV-C robots in bathrooms and elevators, reinforcing passenger confidence in shared facilities.[1]Vanderlande, “Towards a Fully Automated Baggage Hall,” vanderlande.com Surveyed travelers cite visible robotic cleaners as reassurance when choosing flight routes, directly linking sanitation technology to airline load factors. Robots equipped with real-time pathogen analytics are also helping facilities teams optimize chemical usage, advancing sustainability targets. Procurement teams increasingly bundle cleaning robots with HVAC analytics to build integrated health-security dashboards for executive reporting.

AI-Powered Computer Vision Enhancing Security Screening Efficiency

The Transportation Security Administration’s (TSA's) automated target-recognition programs combine robotics and AI vision to flag prohibited items, cutting false alarms and speeding lanes. SITA and IDEMIA’s Augmented Luggage Identification Experience matches bags to passengers, shrinking mishandling rates and compensatory payouts. Computer vision lets robots patrol sterile areas, detect thermal anomalies, and escalate threats without human latency. As megapixel costs fall and edge processors mature, airports can retrofit legacy security assets rather than purchase new lines, accelerating adoption among mid-tier facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment requirements and extended return-on-investment (ROI) periods | –2.1% | Global, acute in emerging markets | Short term (≤2 years) |

| Cybersecurity and data privacy risks in robot-enabled airport operations | –1.8% | Global, heightened in developed markets | Medium term (2-4 years) |

| Lack of standardized global safety and certification frameworks for airport robotics | –1.3% | Global, regional variations | Long term (≥4 years) |

| Labor union resistance to automation-related job displacement risks | –0.9% | Developed markets with strong unions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements and Extended ROI Periods

Up-front acquisition and systems-integration costs often exceed terminal-equipment budgets, especially for smaller airports. UL 3300 safety-compliance testing, site mapping, and cybersecurity hardening add hidden expenses, stretching payback horizons beyond typical five-year thresholds. Operators now seek vendor financing and outcome-based service contracts to offset capital burdens, but accounting practices in emerging markets still favor tangible asset expenditures over service OPEX, delaying procurement.

Cybersecurity and Data Privacy Risks in Robot-Enabled Operations

Connected robots expand attack surfaces, and a single compromised cleaning bot can pivot into passenger Wi-Fi or baggage-handling networks. Peer-reviewed research highlights gaps in staff cyber-hygiene that offset technological safeguards.[2]Lykou G. et al., “Smart Airport Cybersecurity,” doi.org Procurement policies require suppliers to document secure-boot firmware, encrypted telemetry, and compliance with NIST frameworks, raising vendor qualification costs and throttling supply availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Terminal Operations Continue to Dominate

Terminal solutions represented 68.35% of the airport robots market in 2025, underlining airports’ emphasis on passenger-facing efficiency. Information kiosks, autonomous cleaners, and screening assistants are insulated from weather, operate within geofenced zones, and directly influence customer-experience metrics. The airport robots market size for terminal applications is projected to compound steadily as AI upgrades convert stand-alone units into networked service layers. Landside deployments, although smaller, hold superior growth prospects because autonomous valet parking and curbside logistics cut carbon footprints and congestion, matching sustainability mandates. Vendors are refining weather-proof enclosures and redundant localization to extend MTBF in outdoor settings, and regulatory sandbox programs are accelerating proofs of concept.

Passenger satisfaction scores improved at Munich Airport following Josie Pepper’s deployment, validating the return on terminal-interaction robots. As e-commerce pickup points and remote check-in gain traction, terminal robots will increasingly integrate with digital-identity platforms, blurring the boundary between physical and mobile services. Landside innovations like robotic parking remove non-aeronautical traffic from terminal fronts, freeing curb space for ride-hailing and micro-mobility lanes. By 2031, landside solutions are forecasted to represent a larger slice of the airport robots market size as cost curves fall and safety certifications standardize.

By Type: Non-Humanoid Platforms Lead, Humanoids Accelerate

Non-humanoid platforms accounted for 71.62% of the airport robots market share in 2025, anchored by baggage sorters, floor scrubbers, and security patrol units optimized for repetitive tasks. Reliability and ease of maintenance sustain their adoption. Nonetheless, humanoid systems exhibit a 15.28% CAGR as conversational AI matures and hardware costs decline. Early-stage rollouts show passenger dwell time around information desks rises when humanoid robots provide directions, indirectly boosting retail spend. Vendors like LG and SoftBank Robotics are shipping modular humanoids with plug-and-play application kits, promising lower total cost of ownership.

Airport operators value non-humanoid robots for lifecycle simplicity: standard parts, IP-rated housings, and proven analytics dashboards. Conversely, humanoid platforms help airports brand themselves as innovation leaders. As voice-immune-to-noise interfaces improve, humanoid adoption will expand beyond flagship terminals to regional airports seeking passenger-service parity. The blended fleet model—functional robots for heavy work plus humanoids for engagement—is evolving into the de facto standard within high-traffic hubs.

By End Use: Security Dominates, Cleaning Surges

Security solutions generated 31.95% of 2025 revenue, with robots offering persistent patrols, license-plate recognition, and perimeter intrusion detection. Knightscope’s K5 robots stream video and thermal data to command centers, demonstrating value in augmenting human patrols. Cleaning and disinfection robots post the sharpest growth at 15.89% CAGR, driven by regulatory hygiene audits and visible reassurance benefits. Baggage-handling robotics remain a large installed base, but growth moderates as many Tier-1 airports have already automated key sub-processes.

Security spending benefits from government co-funding, lowering procurement risk for airports. Cleaning robots increasingly feature AI path-planning and disinfectant-dose optimization, contributing to ESG scorecards. Passenger-service robots—concierge, wayfinding, and retail promotion units—are gaining incremental revenues tied to advertising and upsell commissions. Valet-parking robots, though niche, monetize scarce land and offset multi-story garage investments, appealing to airports pursuing real-estate diversification.

Geography Analysis

North America led with a 32.10% share in 2025, reflecting TSA-mandated automation and homeland security funding streams. US hub airports scale pilot programs rapidly once safety clearances are met, evidenced by San Antonio International’s swift K5 deployment and renewal contracts. Canada’s larger facilities follow similar patterns, though provincial approval cycles slow nationwide rollouts. Cross-border regulatory alignment on cyber-resilience is further anchoring supplier ecosystems.

Asia-Pacific posts the highest 16.68% CAGR through 2031, propelled by Singapore’s Living Lab, China’s 61.5% export growth in industrial robots, and Japan’s service-robot integration within ANA lounges. Chinese OEMs leverage domestic volume to compress component costs, undercutting imports and expanding addressable buyer pools across ASEAN. South Korea’s drive to commercialize humanoid robotics is sparking bilateral airport trials, positioning the region at the forefront of customer-experience automation.

Europe registers steady but moderated uptake, as stringent worker-safety and cybersecurity directives elongate procurement cycles. However, the EU’s Fit-for-55 package incentivizes carbon-saving technologies like robotic valet parking, which is evident in Lyon’s expansion to 2,000 automated slots. Nordic airports prioritize baggage-handling robots to mitigate labor scarcity, while southern hubs focus on outdoor cleaning to manage heat-related worker protections. The Middle East invests in high-profile concourse robots to elevate premium-hub status. In contrast, South America remains in early experimentation, constrained by capital budgeting but showing signs of acceleration as regional passenger levels rebound.

Competitive Landscape

Competition remains moderately fragmented, with established airport IT integrators, industrial-automation suppliers, and robotics specialists converging on overlapping solution stacks. SITA N.V. leverages integrated airport-management platforms to cross-sell robots that plug directly into existing operational databases, minimizing middleware friction. Vanderlande capitalizes on decades of baggage-handling domain knowledge to offer retrofit-friendly robotic sortation arms. Specialized entrants like Stanley Robotics dominate narrow niches such as autonomous parking, differentiating through high-precision localization software.

Strategic alliances define go-to-market success. SITA’s partnership with IDEMIA embeds computer-vision baggage tracking into its broader data-exchange ecosystem, creating a sticky, end-to-end proposition. Hardware makers increasingly adopt open API architectures so airports can layer third-party AI analytics without vendor lock-in. Service-level agreements now bundle predictive maintenance and cybersecurity monitoring, establishing annuity income for suppliers while assuring uptime for operators.

UL’s publication of safety criteria for service robots in public spaces has begun to harmonize certification, lowering barriers for new entrants but pressuring incumbents to document compliance rigorously.[3]UL Standards & Engagement, “Robotics,” ulse.org Price competition intensifies as Asian OEMs exploit scale economies, yet Western vendors counter by emphasizing data-sovereignty guarantees and long-term parts availability. Market trajectories suggest consolidation around firms that can pair field-proven hardware with airport-grade cybersecurity and lifecycle support.

Airport Robots Industry Leaders

SITA N.V.

LG Electronics, Inc.

Stanley Robotics

Knightscope, Inc.

CYBERDYNE Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SIMPPLE Ltd. received a USD 524,000 contract to supply autonomous cleaning robots to Singapore's international airport. This is the second contract awarded to SIMPPLE by the Singapore airport authorities within a year.

- November 2024: SIMPPLE Ltd. secured a USD 400,000 contract to supply autonomous cleaning robots at one of Singapore's international airport terminals.

Global Airport Robots Market Report Scope

Airport robots, a cutting-edge innovation, are making their debut in airports globally. These robots are set to transform airport operations, potentially assuming roles that have long been the domain of human employees. Fueled by AI, airports are exploring the potential of robots not just for conventional tasks such as cleaning, security, and baggage handling but also as advanced passenger assistants. The market for airport robots is diverse, covering applications ranging from valet parking and security to scanning boarding passes and implementing sophisticated baggage handling systems.

The airport robots market is segmented into application and geography. By application, the market is segmented into landside and terminal. The report also covers the market sizes and forecasts in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Landside |

| Terminal |

| Humanoid |

| Non-Humanoid |

| Airport Security |

| Valet Parking |

| Baggage Handling |

| Cleaning and Disinfection |

| Passenger Service/Guidance |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Landside | ||

| Terminal | |||

| By Type | Humanoid | ||

| Non-Humanoid | |||

| By End Use | Airport Security | ||

| Valet Parking | |||

| Baggage Handling | |||

| Cleaning and Disinfection | |||

| Passenger Service/Guidance | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current valuation of the airport robots market?

The airport robots market size is USD 1.47 billion in 2026.

How fast is demand for airport robots expected to grow?

Revenue is projected to register a 13.65% CAGR from 2026 to 2031.

Which application segment currently leads spending?

Terminal-focused deployments hold 68.35% share of global revenue.

Which region is the fastest-growing adopter of airport robotics?

Asia-Pacific is expanding at a 16.68% CAGR through 2031.

What end-use area shows the strongest growth outlook?

Cleaning and disinfection robots are forecasted to grow at 15.89% CAGR.

Page last updated on: