Aircraft Fuel Tanks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 1.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

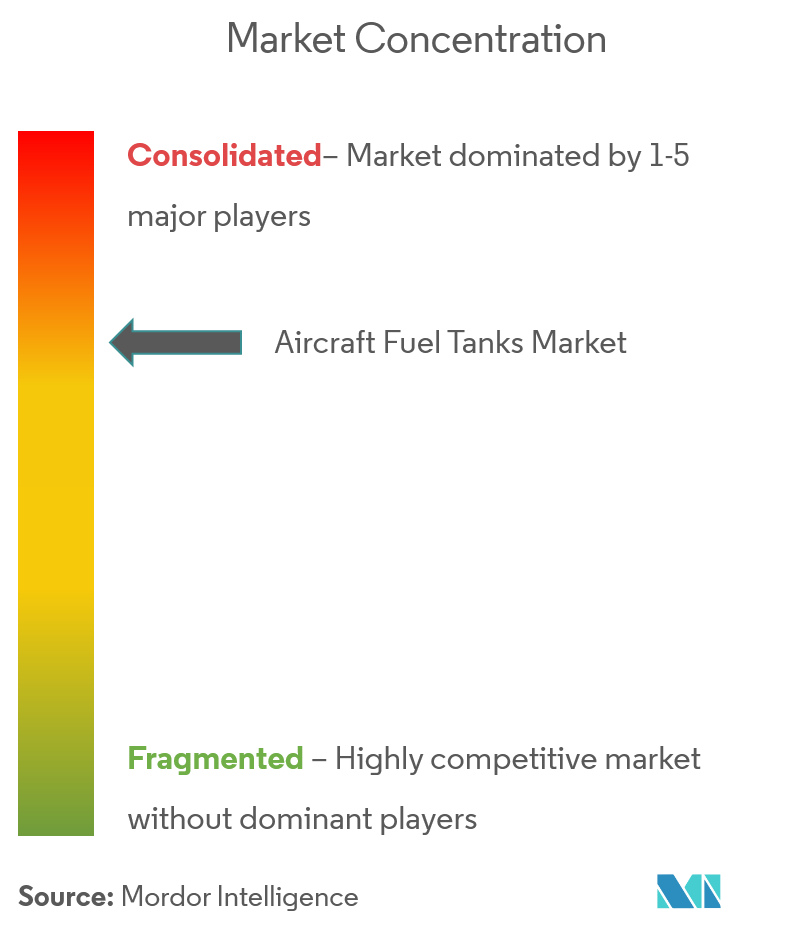

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Fuel Tanks Market Analysis by Mordor Intelligence

The aircraft fuel tanks market size is expected to grow from USD 0.97 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.06 billion by 2031 at 1.49% CAGR over 2026-2031. The modest topline masks latent disruption as OEMs balance incremental upgrades to kerosene-based systems with sizeable R&D outlays for hydrogen storage. Robust replacement demand—underpinned by Boeing’s projection for nearly 44,000 new deliveries through 2043—anchors baseline production volumes, even as cryogenic concepts mature for mid-2030s entry-into-service. Parallel defense recapitalization initiatives, such as the US KC-Y bridge tanker and the Next Generation Air-refueling System, inject premium revenue streams into a market historically led by commercial programs. Composite material penetration keeps margins attractive; carbon-fiber solutions account for 41.34% of 2024 material revenues, reflecting the unrelenting OEM focus on weight reduction.

Key Report Takeaways

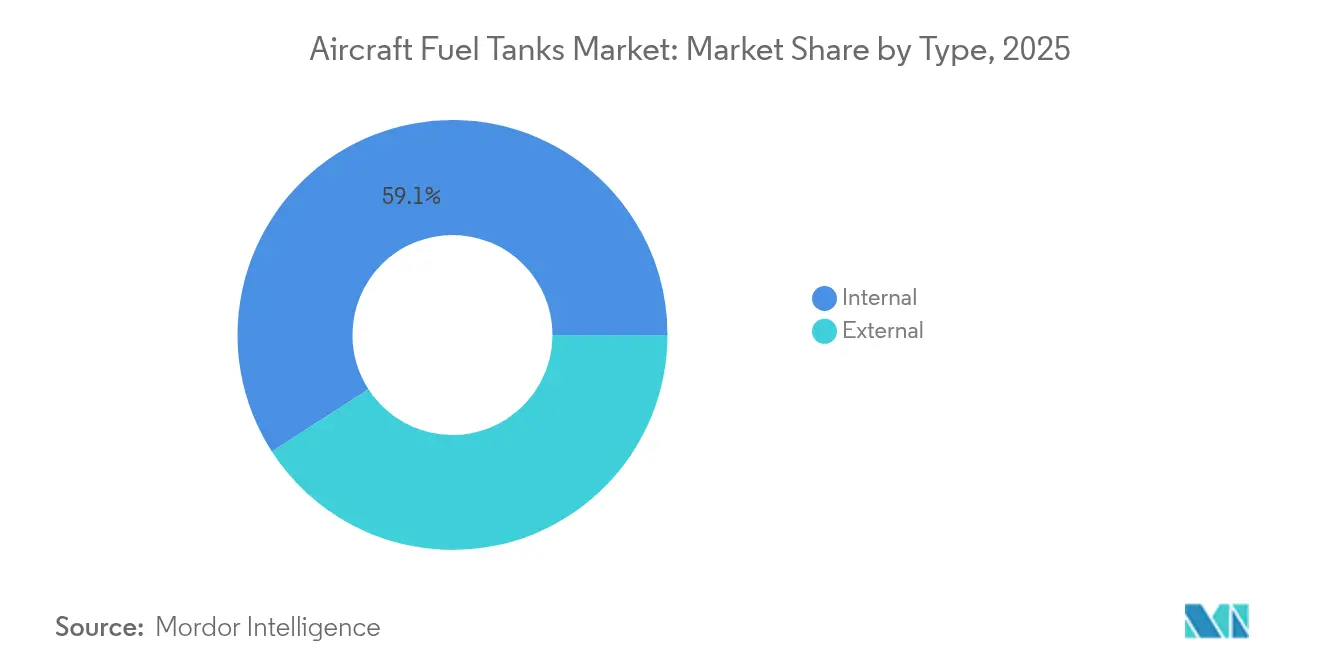

- By type, internal tanks controlled 59.12% of the aircraft fuel tanks market share in 2025, while external and conformal designs posted the fastest 3.9% CAGR to 2031.

- By material, carbon-fiber composites led with 40.95% revenue in 2025; hybrid cryogenic materials are set to expand at a 5.28% CAGR through 2031, outpacing legacy metallics.

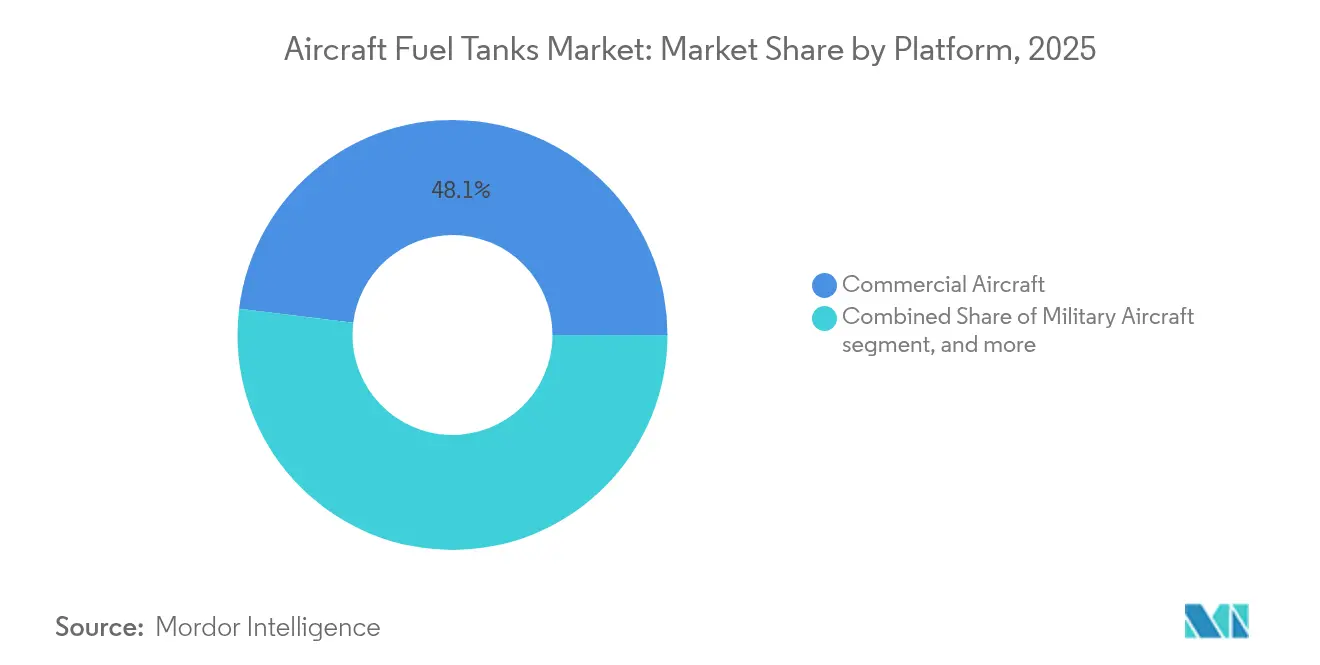

- By platform, commercial aircraft programs held 48.05% of the aircraft fuel tank market size 2025, yet military aircraft recorded the strongest 3.22% CAGR to 2031.

- By end use, OEM channels captured 67.55% of 2025 revenue; the aftermarket enjoys a 4.55% CAGR on the back of auxiliary-range retrofit kits.

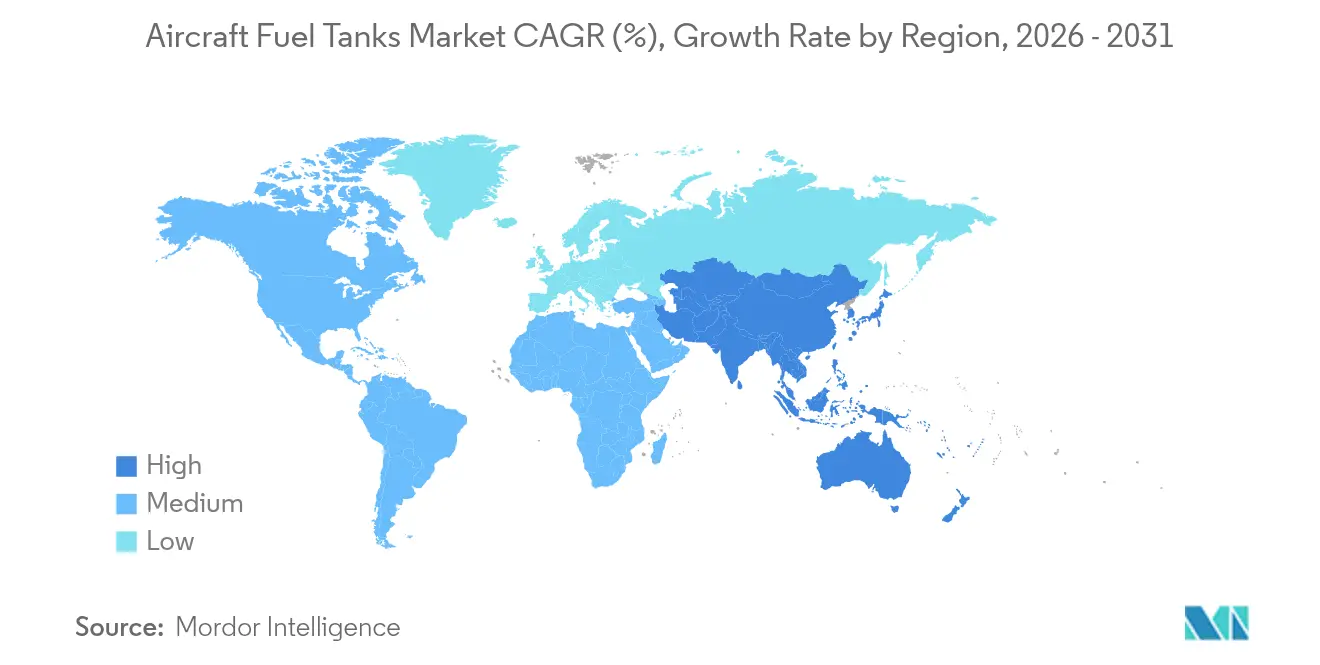

- By geography, North America retained leadership with a 35.05% share in 2025, whereas Asia-Pacific is the fastest-growing region, with a 5.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Fuel Tanks Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial aircraft production up-cycle | +0.8% | Global; focus on North America and Europe | Medium term (2-4 years) |

| Defense fleet modernization programs | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Adoption of lightweight CFRP and hybrid tanks | +0.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising retrofit demand for auxiliary/long-range kits | +0.3% | Global; strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Mandatory inert-gas inerting systems | +0.2% | Global | Medium term (2-4 years) |

| Emergence of cryogenic LH₂ tanks for zero-emission aircraft | +0.1% | Europe and North America first movers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercial Aircraft Production Up-Cycle

Airlines are replacing older narrow-bodies with high-utilization single-aisle jets, sustaining baseline fuel-tank demand even during macroeconomic uncertainty. The Airbus A321XLR’s 12,900-liter rear-center tank extends range to 4,700 nm, proving that creative fuel storage unlocks new, thinner routes.[1]Airbus, “A321XLR Receives Type Certificate,” easa.europa.eu Record backlog visibility—often exceeding 10 years—allows tank suppliers to forward-plan capacity. OEMs now target 90-day cabin-to-wing modification cycles, down from 120 days on early programs, broadening line-fit throughput. Sustained single-aisle mix shifts favor technologies that ease center-of-gravity management as airlines standardize high-density seating. While supply-chain fragility tempers near-term output, the driver’s net positive effect remains sizable over the medium term.

Defense Fleet Modernization Programs

Three-phase tanker recapitalization in the United States involves completing KC-46A deliveries by 2029, procuring 140-160 KC-Y units, and fielding the stealth NGAS platform around 2040. The KC-46A alone has transferred over 200 million lb of fuel in global operations, highlighting the mission-critical role of advanced tank technology. Asia-Pacific outlays, accounting for 42% of global arms imports, widen the addressable military fleet base. Europe’s eight-unit Multinational MRTT Fleet provides a cooperative model that other regions may replicate for cost-effective aerial refueling capacity.[2]European Defence Agency, “Multinational MRTT Fleet,” eda.europa.eu Premium pricing of stealth-compatible tanks offsets the narrower unit volumes typical of defense programs, ensuring a robust revenue contribution through the long term.

Adoption of Lightweight CFRP and Hybrid Tanks

Carbon-fiber reinforced polymer has trimmed tank weight by up to 33% in NASA demonstrators, improving aircraft fuel burn by double-digit percentages. The European Space Agency validated linerless CFRP cryotanks, opening the door to 2-ton upper-stage mass savings with direct crossover potential for large transports. Automated Fiber Placement (AFP) adds real-time closed-loop control, slashing scrap rates and paving the way for certifiable Type V hydrogen vessels. Netherlands-led hydrogen-tank consortia seek 2025 flight validation, accelerating cross-industry learning curves.[3]CompositesWorld, “Type V Hydrogen Tank Manufacturing,” compositesworld.com Despite certification hurdles, composite-heavy architectures underpin most new-build civil programs, establishing a growth platform for hybrid cryogenic tanks.

Rising Retrofit Demand for Auxiliary/Long-Range Kits

Range-extension kits let airlines open marginal city pairs without ordering new airframes. ALOFT AeroArchitects’ B737NG solution adds up to 50% extra range through modular belly or lower-lobe tanks, maintaining the original cabin configuration. The modular design reduces labor hours and downtime, which is critical for carriers, averaging 12-hour daily utilization. Headwind-prone North Atlantic routes benefit from the flexibility to tanker extra fuel when seasonal winds peak. Retrofit demand surfaces strongly among regional operators that cannot justify wide-bodies but still need transcontinental reach. Consequently, despite its smaller revenue base, the aftermarket registers the steepest CAGR among all end-use channels.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aerospace raw-material prices and supply chain risk | -0.4% | Global; most acute in North America and Europe | Short term (≤ 2 years) |

| Stringent certification and fire-safety testing requirements | -0.3% | Global | Medium term (2-4 years) |

| High R&D and tooling CAPEX for composite tanks | -0.2% | Developed markets | Long term (≥ 4 years) |

| Sub-100-seat electric aircraft reducing future tank demand | -0.1% | Early uptake in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Aerospace Raw-Material Prices and Supply Chain Risk

Titanium sponge sourcing remains exposed, with the United States importing over 90% from geopolitically sensitive suppliers. Russia’s conflict with Ukraine and China’s capacity build-up undermine price stability, driving a 6.8% global titanium CAGR through 2027. Counterfeit alloy incidents have prompted intensified incoming inspection protocols at Airbus and Boeing lines, heightening cost and schedule pressure. Backlogs now embed longer lead times for forgings and castings, forcing OEMs to dual-source critical tank components. Diversification campaigns and near-shoring initiatives require multi-year capital commitments, diluting margin upside for first-tier suppliers.

Stringent Certification and Fire-Safety Testing Requirements

The FAA’s Fuel Tank Flammability Reduction rule caps fleet-average exposure at 3% of operating time, obligating costly inert-gas or ignition-mitigation retrofits.[4]Federal Aviation Administration, “Fuel Tank Flammability Reduction Rule,” ecfr.gov EASA’s special-conditions process for the A321XLR entailed more than 400 joint meetings and 900 flight-test hours, demonstrating the resource intensity for novel configurations. Hydrogen aircraft add fresh hazards that require entirely new regulatory frameworks per the FAA’s December 2024 hydrogen roadmap. Qualification regimens involve pressure cycling to 3.5 psi, 25-hour vibration sweeps, and 50-ft drop tests. Over the next decade, cumulative compliance costs for mandated inerting systems could exceed USD 35.7 billion across in-service fleets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: External Tanks Drive Innovation

External tanks record the fastest 3.9% CAGR as militaries prioritize drop-tanks, conformal systems, and buddy-pod refuelers that can be jettisoned or detached when tactical needs shift. Internal systems still dominate 59.12% of 2025 revenue, underscoring their space-efficiency and center-of-gravity advantages in commercial service. Eaton’s 1,360-gal jettisonable units showcase compliance with JP-4, JP-5, and JP-8 while offering structural provisions for supersonic carriage. The emergence of conformable shapes supports blended-wing-body demonstrators that lack traditional wing boxes. Advancements in self-sealing technology protect against incendiary rounds, while integrated fuel-quantity gauging achieves sub-0.25% accuracy through digital probes.

Growth pivots to emerging hybrid fighter missions demanding stealth and ferry range, compelling designers to blend internal bays with low-observable external pods. Bladder-based auxiliary kits reinforce aftermarket momentum, letting airlines field range-extension packages without structural re-certification. Active-health-monitoring sensors feed prognostic algorithms that schedule maintenance windows before leaks propagate. Thus, even as the aircraft fuel tank market size remains, internal systems and external tank innovation deliver a disproportionate share of incremental revenue.

By Material: Hybrid Technologies Lead Innovation

Carbon-fiber composites captured 40.95% of 2025 revenue, driven by weight savings of 15-35 kg per short-haul aircraft, translating into multi-million-dollar lifetime fuel burn reductions. Hybrid cryogenic structures clock a 5.28% CAGR as hydrogen roadmaps crystallize around mid-2030s entry-into-service. Linerless Type V tanks promise 40% additional weight savings but face micro-crack propagation issues under high-cycle pressure loads. Metallic alloys such as aluminum-lithium retain relevance where proven fracture toughness is paramount, especially in wing integral tanks for wide-bodies. Polymer-based bladders continue to service retrofit demand thanks to installation speed and lower capital requirements.

Automated Fiber Placement couples ultrasonic welding to create liquid-tight seams, a prerequisite for cryogenic LH₂. Hybrid configurations mesh titanium liners with carbon overwraps, allowing linerless concepts to mature. Embedded fiber-optic sensors track strain and temperature in real time, enabling predictive maintenance business models. Consequently, while composites dominate value today, the aircraft fuel tanks market share of hybrid and smart-material solutions will continue to climb.

By Platform: Military Modernization Accelerates

Commercial single-aisle jets commanded 48.05% of 2025 revenues, but a 3.22% CAGR on the defense side edges military programs to the growth forefront. KC-46A, KC-Y, and NGAS platforms underpin a pipeline of over 300 tanker units through 2040. Fighter upgrades involving conformal or buddy-store refuelers further inflate unit values despite lower annual volumes. The aircraft fuel tanks market size attributed to general and business aviation remains stable as long-range variants of popular models adopt tailored auxiliary solutions.

Asia-Pacific rearmament budgets pivot toward Indigenous manufacturing, generating local demand for tank subsystems in India, Japan, and South Korea. Commercial long-haul programs stay subdued, yet auxiliary packages that raise payload range on A330-200s and B767-300ERs soften the impact. JetZero’s blended-wing-body concept, backed by RTX, introduces new fuselage-integrated fuel bay architectures to reset design rules. Cumulatively, military and next-generation civil demonstrators reposition the platform mix toward higher-value configurations over the forecast window.

By End Use: Aftermarket Retrofit Momentum

OEM line-fit remained the revenue cornerstone at 67.55% in 2025, anchored by entrenched supply agreements and complex certification dossiers. Nevertheless, the aftermarket is forecast to outpace all channels with a 4.55% CAGR as operators opt for incremental range over capital-intensive fleet growth. Auxiliary kit providers benefit from modular designs that slot into lower-deck holds without disturbing passenger layouts. MRO hubs in Malaysia and Morocco gain traction as Eaton and Safran co-locate repair stations near high-growth fleets.

FAA inerting mandates spur retrofit of nitrogen-generation or ignition-mitigation systems across 3,000-plus US-registered transports. Blended-fuel compatibility checks, required as SAF ratios rise, drive further inspection and component swap-outs. Digital fuel-quantity upgrades leveraging silicon-on-sapphire sensors create a new recurring revenue layer. Hence, even though OEM channels will continue to dominate absolute dollars, aftermarket solutions remain the chief growth engine in the aircraft fuel tanks market.

Geography Analysis

North America led with 35.05% of 2025 revenue on the back of Boeing’s high-volume B737 and B787 lines, plus the US Air Force’s tanker recapitalization roadmap. The KC-46A program, despite schedule slips, validates advanced inert-ing and boom-refueling tanks capable of 1,200 gallons-per-minute offload rates. Washington’s policy focuses on reshoring titanium and aluminum value chains and aims to defuse geopolitical risk from Russia and China. The Biden administration’s 2025 Inflation Reduction Act credits hydrogen-aircraft demonstrators, catalyzing early LH2 tank R&D funding

Asia-Pacific posts the highest 5.07% CAGR as China seeks to double its commercial fleet by 2043, demanding more than 8,000 single-aisle aircraft that will ship with integral carbon-fiber tanks. COMAC C919 deliveries reached 10 aircraft by end-2024, stimulating home-grown subsystem ecosystems. India’s 8.3% annual passenger growth underpins high-seat-count narrow-body orders, while its Make-in-India scheme lures fuel-system joint ventures such as Safran-HAL for LEAP engine parts. Defense spending, accounting for 42% of global imports, demands multirole tankers and conformal solutions on revamped fighter fleets.

Europe’s share edges forward on steady Airbus output and collaborative defense projects like the eight-unit MRTT fleet delivered out of the Netherlands. EASA’s RefuelEU mandate requires 2% SAF blending in 2025, scaling to 70% by 2050, compelling tank upgrade paths for fuel-property variability. Regional R&D clusters in Sweden and France invest heavily in cryogenic demonstrators, exemplified by GKN’s 5,000 m² expansion in Trollhättan that integrates AFP cells and digital twins. Brexit-driven customs frictions dampen UK suppliers’ competitiveness, yet targeted investments by Spirit AeroSystems shore up critical-structure capacity. Overall, geographical demand shifts make Asia-Pacific the volume growth leader while North America remains the technology bellwether.

Competitive Landscape

The aircraft fuel tanks market is moderately consolidated: the top five suppliers together command a major share of revenue, underpinned by multi-decade sole-source positions with Airbus and Boeing. Boeing’s USD 8.3 billion purchase of Spirit AeroSystems internalizes wing-box and center-tank know-how, protecting supply continuity after repeated quality lapses. Parker Hannifin’s sale of its composites and fuel containment arm to SK Capital narrows its aerospace span but unlocks cash for motion-control acquisitions.

Suppliers differentiate through material science and digital manufacturing. Lockheed Martin’s plant-wide digital thread slashes non-recurring expense by linking tank design, AFP lay-up, and nondestructive inspection on a single MES backbone. GKN Aerospace partners in projects such as ICEFlight, targeting 500-kW cryogenic powertrains that rely on linerless CFRP tanks capable of minus 253 °C operations.

Regulatory compliance favors incumbents with extensive design-assurance experience. FAA SFAR-88 requires continuous inspection criteria, raising barriers for new entrants lacking DER-level expertise. Yet white-space potential in LH₂ storage opens footholds for agile composites specialists willing to shoulder early-stage certification risk. Consequently, while legacy players remain dominant, the move to hydrogen is poised to reshuffle the supplier hierarchy over the next decade.

Aircraft Fuel Tanks Industry Leaders

Safran SA

Eaton Corporation plc

Robertson Fuel Systems LLC

Meggitt PLC (Parker-Hannifin Corporation)

GKN Aerospace (Melrose plc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Airbus started researching higher MRTT output to satisfy rising aerial-refueler demand.

- May 2025: GKN Aerospace joined the Airbus-led ICEFlight to validate cryogenic electric architectures using LH₂ tanks.

- February 2025: Safran Aircraft Engines and HAL inked a pact on LEAP forged parts under the Make-in-India initiative.

- December 2024: The FAA issued a hydrogen-aircraft safety roadmap covering the tank fire/explosion hazards.

Global Aircraft Fuel Tanks Market Report Scope

Aircraft fuel tanks are a major component of aircraft fuel systems. The market is segmented by type, application, and region.

The report also provides market size and forecast in value (USD million) for the major countries across all the regions.

| Internal (Integral, Bladder, Self-sealing) |

| External (Drop, Conformal, Buddy-Pods) |

| Metallic Alloys (Al-Li, Ti) |

| Carbon-Fiber Composites |

| Polymer/Elastomer Bladders |

| Hybrid and Next-Gen Cryogenic |

| Commercial Aircraft |

| Military Aircraft |

| General Aviation Aircraft and Business Jets |

| OEM |

| Aftermarket/Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Internal (Integral, Bladder, Self-sealing) | ||

| External (Drop, Conformal, Buddy-Pods) | |||

| By Material | Metallic Alloys (Al-Li, Ti) | ||

| Carbon-Fiber Composites | |||

| Polymer/Elastomer Bladders | |||

| Hybrid and Next-Gen Cryogenic | |||

| By Platform | Commercial Aircraft | ||

| Military Aircraft | |||

| General Aviation Aircraft and Business Jets | |||

| By End Use | OEM | ||

| Aftermarket/Retrofit | |||

| By Region | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aircraft fuel tanks market?

The market is valued at USD 0.98 billion in 2026 and is forecasted to reach USD 1.06 billion by 2031.

Which segment of the aircraft fuel tanks market grows the fastest?

External and conformal tanks lead with a 3.9% CAGR through 2031 as militaries expand aerial-refueling flexibility.

Why are composites important in aircraft fuel tanks?

Carbon-fiber tanks cut structural weight by up to 33%, lowering airline fuel bills and enabling longer ranges.

How big is the aftermarket opportunity for fuel tank retrofits?

The aftermarket achieved a 4.55% CAGR, fueled by auxiliary-range kits that can extend single-aisle reach by up to 50%.

Which region leads growth in aircraft fuel tanks?

Asia-Pacific posted the highest 5.07% CAGR, driven by China’s and India’s rapidly expanding fleets and defense budgets.

Will hydrogen aircraft eliminate the need for conventional fuel tanks?

No; they will require larger cryogenic tanks, creating a new materials and certification frontier rather than shrinking demand.

Page last updated on: