Aircraft Altimeter And Pitot Tube Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

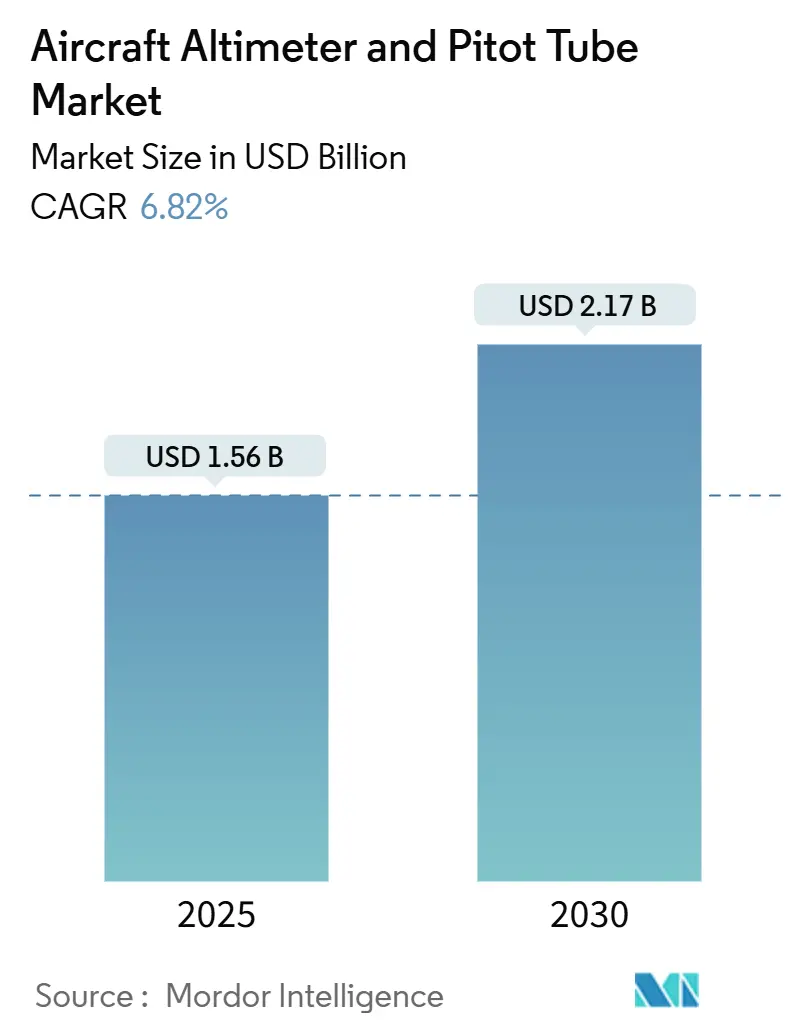

| Market Size (2025) | USD 1.56 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 6.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Altimeter And Pitot Tube Market Analysis by Mordor Intelligence

The aircraft altimeter and pitot tube market size is USD 1.56 billion in 2025 and is projected to reach USD 2.17 billion by 2030, translating into a 6.82% CAGR over the forecast period. This healthy growth profile reflects the accelerated replacement of legacy air-data instruments with MEMS-based solid-state solutions, the wave of ADS-B Out compliance activity across fixed-wing fleets, and the rapid installation of digital cockpits in new-build and retrofitted aircraft. Operators pursuing fuel-burn reductions adopt climate-resilient flight-level optimization algorithms that require millibar-level static-pressure accuracy, creating incremental demand for higher-resolution sensors. Meanwhile, the shifting from discrete altimeter and pitot hardware toward multifunction air-data modules pushes suppliers to bundle sensing, processing, and self-diagnostic capability inside a single enclosure, reducing wiring weight and easing installation. Competitive intensity rises as disruptive MEMS suppliers undercut traditional quartz-based systems, while incumbents defend share through proven certification pipelines and long-term OEM contracts.

Key Report Takeaways

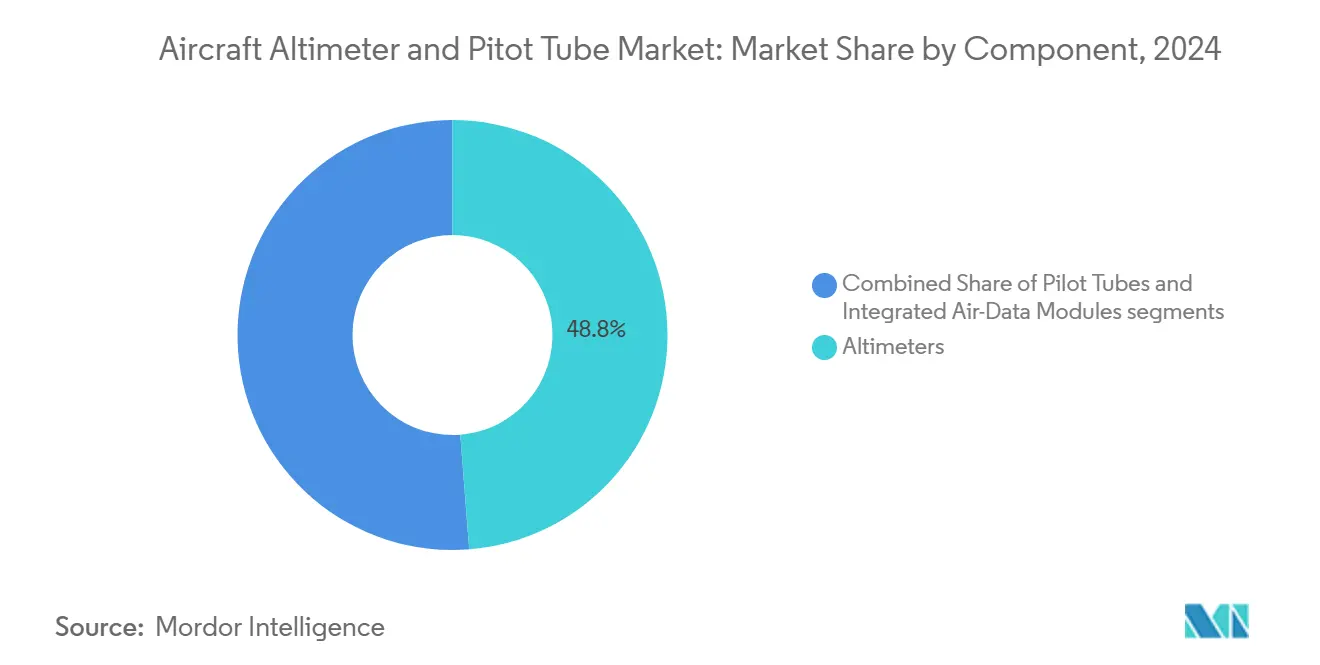

- By component, altimeters held 48.76% of the aircraft altimeter and pitot tube market share in 2024; integrated air-data modules are advancing at a 7.14% CAGR through 2030.

- By platform, commercial aviation led with 58.42% revenue share in 2024, while general aviation is projected to expand at a 7.45% CAGR to 2030.

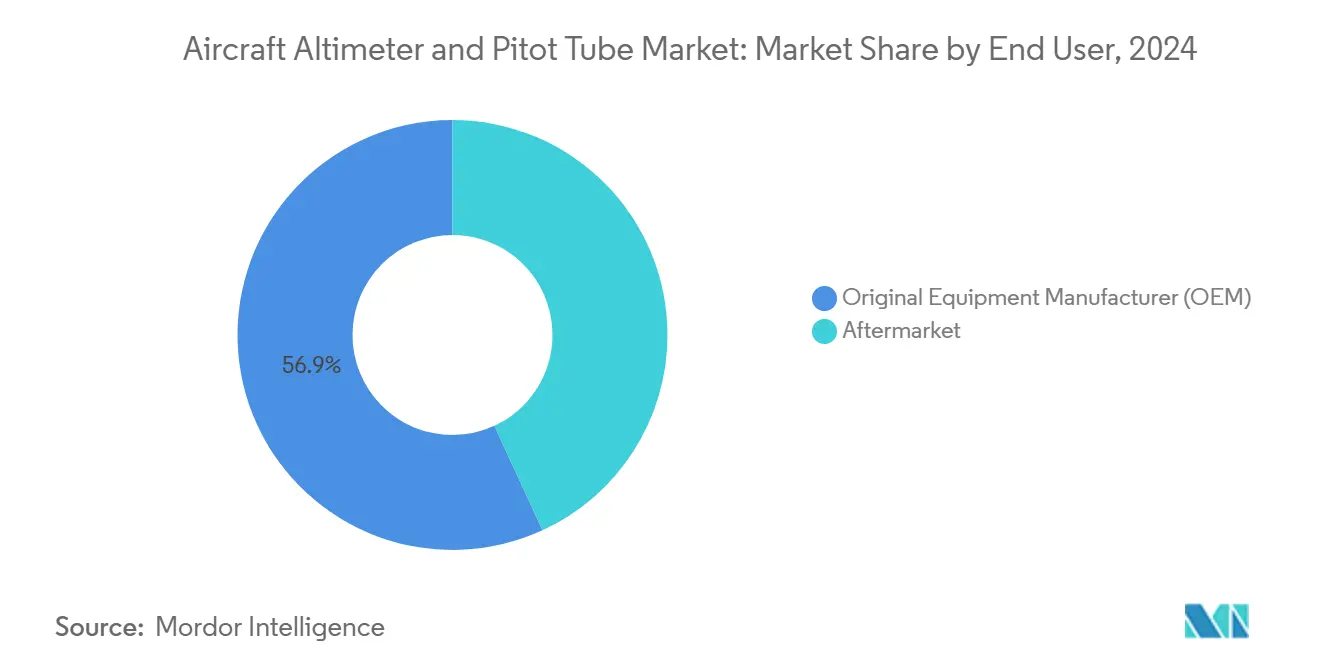

- By end user, the OEM segment commanded 56.87% of the aircraft altimeter and pitot tube market size in 2024; the aftermarket is forecasted to grow at a 7.56% CAGR between 2025 and 2030.

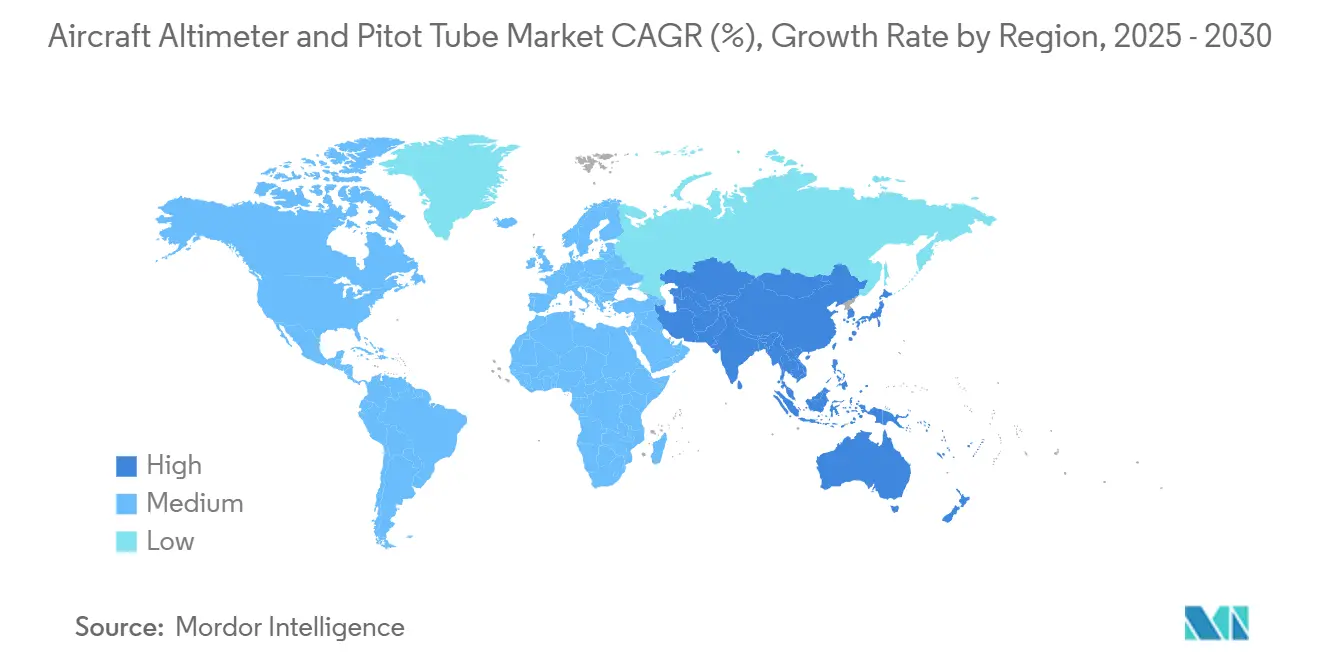

- By geography, North America accounted for a 33.76% share of the aircraft altimeter and pitot tube market size in 2024, whereas Asia-Pacific is set to post the fastest 7.95% CAGR through 2030.

Global Aircraft Altimeter And Pitot Tube Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated fleet renewal of narrowbody aircraft | +1.2% | Global, concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing emphasis on compliance with ADS-B Out retrofit mandates | +1.8% | Global, priority in North America, Europe and Asia-Pacific | Short term (≤ 2 years) |

| Rising adoption of digital cockpits in next-generation regional jets | +0.9% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Integration of MEMS-based solid-state pressure sensing technologies | +1.1% | Global, R&D leadership in North America and Europe | Long term (≥ 4 years) |

| Advancements in climate-resilient flight-level optimization algorithms | +0.7% | Global, focus on high-traffic corridors | Long term (≥ 4 years) |

| Growing demand for high-accuracy flight instrumentation in commercial aviation | +0.9% | Global, emphasis on Asia-Pacific fleet expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Fleet Renewal of Narrowbody Aircraft

Fleet modernization programs speed up as carriers retire fuel-inefficient units and induct new 737, A320, and C919 families outfitted with advanced avionics. Boeing forecasts the Chinese fleet doubling to 9,740 aircraft by 2043, and three-quarters of these deliveries are single-aisle models that require integrated air-data modules for ADS-B and autothrottle functions. New-build demand is complemented by retrofit work on in-service A320ceo and B737 NG units undergoing glass-cockpit upgrades that mandate millibar-level altitude accuracy. Airlines chasing 1-2 % block-fuel savings now rely on altitude-optimized climb profiles and reduced vertical-separation minima, which hinge on pressure-sensing precision. Suppliers capable of delivering low-drift MEMS transducers bundled with DO-178C-qualified software win line-fit positions and secure lucrative consumables revenue through the life cycle. The result is an apparent pull-through effect that cements the aircraft altimeter and pitot tube market as a beneficiary of narrowbody replacement cycles.

Increasing Emphasis on Compliance with ADS-B Out Retrofit Mandates

ADS-B mandates lock in an equipment baseline that drives recurring sales of certified altitude encoders and Mode S transponders. As of January 2025, 169,116 US civil aircraft were equipped with ADS-B Out capability, up 11% from a year earlier.[1]Federal Aviation Administration, “Current Equipage Levels,” faa.gov Variations in Canadian, Mexican, and European implementation timelines prolong the retrofit window, while post-installation maintenance creates annuity revenue streams for sensor calibration and periodic inspection. In small-turbine and piston categories, operators often discover legacy static-pressure systems cannot meet barometric accuracy thresholds once fused with ADS-B, prompting wholesale replacement with modern air-data computers. The regulatory clock, therefore, acts as a catalyst for both initial hardware upgrades and future-proofing investments that sustain the aircraft altimeter and pitot tube market well beyond the retrofit deadline.

Rising Adoption of Digital Cockpits in Next-Generation Regional Jets

Embraer E-Jets E2 and ATR 72-600 fleets migrate toward integrated flight decks where synthetic-vision systems, terrain-awareness modules, and envelope-protection algorithms rely on low-latency pressure measurements. Garmin’s G5000 Prime exemplifies the shift to all-digital instrument panels that collapse multiple conventional gauges into touchscreen displays.[2]Curtiss-Wright Corporation, “Honeywell And Curtiss-Wright Develop Cockpit Voice Recorders To Help Boeing Airbus Meet New 25-Hour Safety Mandate,” curtisswright.com Digitalization broadens the value proposition for altimeter and pitot suppliers, integrating data buses, built-in test equipment, and ARINC-429/664 interfaces inside their probes. Regional carriers seek cockpit commonality with mainline narrowbodies to lower pilot-transition costs, further standardizing demand for high-precision pressure systems. Therefore, the market benefits from hardware volume and the software and data-integration layers surrounding each sensor.

Integration of MEMS-Based Solid-State Pressure Sensing Technologies

MEMS devices reduce moving parts, cut power draw, and enable form factors small enough to embed inside wing-leading-edge probes. Collins Aerospace’s SmartProbe pairs MEMS transducers with on-board processors to generate compensated airspeed, Mach, and angle-of-attack outputs that drop directly onto the avionics bus. Because calibration coefficients are stored on-chip, maintenance crews can swap units without aircraft-level recalibration, lowering life-cycle cost for operators. Certification hurdles remain significant because DO-178C Level-A software drives processing logic and fault-monitoring routines, but incumbents wield this barrier to sustain margins. Over the long term, MEMS sensors tilt the cost-performance curve, and their expanding use underpins a sizable share of new revenue for the aircraft altimeter and pitot tube market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended supply chain lead times for aerospace-grade quartz components | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Increased litigation risks due to pitot probe icing susceptibility | -0.6% | Global, regulatory focus in North America and Europe | Medium term (2-4 years) |

| Cost pressure from emerging low cost solid-state sensor alternatives | -0.9% | Global, competitive pressure in Asia-Pacific | Long term (≥ 4 years) |

| Delays in certification processes tied to DO-178C Level-A software requirements | -0.7% | Global, bottlenecks in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Supply Chain Lead Times for Aerospace-Grade Quartz Components

Aerospace-grade quartz remains indispensable for legacy barometric capsules in many commercial transport altimeters. Temperature-vacuum annealing, multi-week stabilization, and tight piezo-electric testing protocols lengthen lead times to 40-60 weeks, straining OEM production horizons. Semiconductor fabs prioritize higher-volume consumer parts at near-full capacity, leaving aerospace purchase orders competing for thin manufacturing windows. Line-fit programs secure allocation through multi-year supply agreements, but independent MRO shops face “aircraft-on-ground” events when parts are unavailable.

Increased Litigation Risks Due to Pitot-Probe Icing Susceptibility

The Air France 447 verdict sharpened legal scrutiny on pitot-probe performance in high-altitude ice-crystal environments. Subsequent FAA and EASA directives mandate dual-heater redundancy and post-flight blockage checks on A330, A340, and B787 fleets, raising retrofit and warranty costs. Manufacturers now integrate acoustic reflectometry to detect partial obstructions in real time, but this adds electronics that must survive lightning-induced transients. Carriers operating in tropical storm tracks allocate extra maintenance man-hours for probe inspection, indirectly elevating the total cost of ownership. Insurance premiums for widebody operators have ticked up, transferring a portion of liability pressure down the value chain to sensor suppliers. The cumulative legal and compliance outlays erode margins and clip 0.6 percentage points from forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integrated Modules Reshape the Value Chain

Altimeters accounted for 48.76% of the aircraft altimeter and pitot tube market share in 2024, reflecting their non-negotiable role in altitude readout redundancy for IFR operations. However, integrated air-data modules already capture a 7.14% CAGR tailwind, pointing to system-on-probe architectures that blend pitot, static, and temperature sensing with digital compensation. These integrated packages reduce wiring by up to 20 lb on a narrowbody and free valuable panel real estate, streamlining final assembly and maintenance. Tier-one avionics suppliers leverage proprietary compensation algorithms to deliver ±10 ft altitude accuracy across –70 °C to +85 °C, surpassing traditional mechanical bellows. Therefore, the aircraft altimeter and pitot tube market shifts from discrete components toward multifunction units that embed certification-grade software and health monitoring.

Technological miniaturization underpins this transition, as MEMS pressure dies shrink to sub-3 mm footprints while achieving 0.01% full-scale linearity. Collins Aerospace’s SmartProbe consolidates differential and total pressure measurement inside a wing-leading-edge mount, eliminating remote lines susceptible to freezing. Meanwhile, Honeywell’s connected-maintenance architecture pushes vibration and temperature data into predictive analytics engines, flagging sensor drift before it breaches minimum-equipment-list thresholds. As aftermarket players chase retrofit prospects, they confront intellectual-property walls created by custom checksum protocols that lock integrated probes to their native air-data computers. These high-switching-cost dynamics underpin sustained margin premiums and reinforce the leadership positions of incumbent suppliers within the aircraft altimeter and pitot tube market.

By Platform: General Aviation Accelerates the Upgrade Cycle

Commercial aviation retained 58.42% of the aircraft altimeter and pitot tube market in 2024 because of fleet-scale ADS-B compliance and a continuing parade of A320neo and B737 MAX deliveries. Single-aisle airframes alone consume more than 80,000 pitot probes annually when factoring in spare-part provisioning, cementing the segment’s revenue primacy. Yet the spotlight increasingly tilts toward general aviation, forecasted to log a 7.45% CAGR as business jet owners retrofit for FANS 1/A and RNP 0.3 operations. Synthetic-vision primary flight displays demand instantaneous air-data refresh at 60 Hz, compelling Gulfstream G500 and Dassault Falcon 10X operators to adopt solid-state pitot-static systems that speak Ethernet-AVB natively.

Rotorcraft also contributes to offshore transport and search-and-rescue (SAR) missions requiring accurate low-speed airspeed for auto-hover. Leonardo AW139 retrofits illustrate how modular probes withstand salt-spray corrosion while feeding redundant avionics lanes. Military fleets remain a steady buyer, anchored by US Army helicopter and USAF tanker modernization programs that favor multi-mission air-data configurations. However, protracted budget cycles temper annual spending volatility, yielding a flatter demand curve than civil counterparts. The cumulative effect sees platform diversification buffering cyclical swings and reinforcing the aggregate resilience of the aircraft altimeter and pitot tube market.

By End User: Aftermarket Captures Growing Wallet Share

OEM linefit installations still represent 56.87% of revenue, as every airframe exits the factory equipped with dual or triple independent pressure channels. Linefit dominance furnishes suppliers with lifetime incumbency, given that avionics common-type certification discourages mid-life sensor swaps. Nevertheless, the aftermarket posts the superior 7.56% CAGR as aging fleets cross the 12-year maintenance threshold that triggers altimeter overhaul or outright replacement. ADS-B retrofits provide an immediate uplift, but the sustained wave comes from heavy checks when operators harmonize cockpit layouts with newer siblings.

The aircraft altimeter and pitot tube industry capitalizes on Asia-Pacific’s burgeoning MRO sector, where Airbus pegs maintenance demand at USD 51 billion by 2043, doubling from 2024.[3]Airbus S.A.S., “Asia-Pacific’s aircraft services market to double over next 20 years,” aircraft.airbus.com Line maintenance providers stock rotable integrated probes to minimize aircraft-on-ground time, and predictive-health analytics platforms generate replacement alerts that funnel predictable parts demand to authorized distributors. Independent repair stations, meanwhile, negotiate Parts Manufacturer Approval (PMA) licenses for simple pitot-tube designs, injecting competitive price tension that ultimately widens the customer base. Consequently, aftermarket momentum supplies an expanding revenue flank that shores up growth for the overall aircraft altimeter and pitot tube market.

Geography Analysis

North America commanded 33.76% of the aircraft altimeter and pitot tube market size in 2024 due to its concentration of OEM final-assembly lines, mature MRO infrastructure, and early adoption of ADS-B Out requirements. The FAA’s leadership role in defining DO-178C and DO-254 guidelines gives regional suppliers a regulatory early-mover advantage. Defense spending exceeding USD 840 billion in 2025 sustains procurement of KC-46A tankers and UH-60V upgrades, each embedding redundant solid-state air-data channels. Coupled with a general aviation fleet of 211,000 active aircraft, the regional customer mix secures a broad aftermarket funnel and cements steady cash flows for instrument vendors.[4]Federal Aviation Administration, “Current Equipage Levels,” faa.gov

Asia-Pacific is the fastest-growing geography, registering a 7.95% CAGR as China and India continue multi-decade fleet expansions. Airbus projects the region’s aviation-services market to balloon to USD 129 billion by 2043, with maintenance services soaring from USD 19 billion to USD 51 billion. Domestic OEMs like COMAC turn to indigenous sensor suppliers to localize the supply chain, but certification hurdles leave room for Western incumbents to capture premium niches. Rapid airport construction across Indonesia, Vietnam, and the Philippines adds more than 4,000 daily narrowbody departures within five years, pumping recurring demand for spares and overhauls.

Europe maintains a balanced demand curve built on Airbus final-assembly lines in France and Germany and a robust biz-jet refurbishment ecosystem in Switzerland. Stricter EASA icing-tolerance tests accelerate the retirement of non-heated pitot probes, stimulating immediate replacement orders. Sustainability regulations such as “Fit for 55” incentivize airlines to exploit flight-level optimization algorithms, indirectly nudging carriers toward next-generation pressure sensors that feed the required data granularity. The Middle East and Africa trail in absolute volume yet show high growth pockets tied to Gulf carrier fleet additions and sub-Saharan regional jet adoption. Their harsh operating environments—desert sand, salt spray, and tropical thunderstorms—drive a premium on ruggedized integrated probes, opening high-margin niche opportunities within the aircraft altimeter and pitot tube market.

Competitive Landscape

The aircraft altimeter and pitot tube market sits in the mid-concentration band, with the top five suppliers controlling more than 50% combined share. Honeywell International, Inc., Collins Aerospace (RTX Corporation), and Garmin Ltd. anchor the field through deep certification track records and entrenched OEM positions. Honeywell’s USD 103 million radar-altimeter contract with the US Army reaffirms its military clout, while Collins Aerospace leverages SmartProbe intellectual property to lock in long-term agreements on A220 and E2 programs. Garmin extends its reach from general aviation into light jet platforms, bundling probes with integrated flight decks to capture end-to-end avionics revenue.

Mergers and acquisitions remain a strategic lever; TransDigm’s USD 27 million acquisition of Astronautics’ flight-instrument lines adds attitude and heading indicators that cross-sell with pitot-static packages. After launching compact mission computers with embedded flight-test data-visualization software, Curtiss-Wright signals ambitions to couple sensors with analytics. The competitive narrative now revolves around full-stack offerings encompassing hardware, software, and digital services, an integrated approach that raises switching costs and shields margins.

Entrants focusing on low-cost MEMS chips face formidable certification and brand-trust barriers, but their disruptive pricing injects new dynamics in cost-sensitive helicopter and trainer markets. Incumbents pre-empt erosion by releasing “value lines” that retain essential DO-160G compliance while trimming non-critical features. The strategic outcome is a balanced market where technological differentiation, software pedigree, and service ecosystems remain decisive while price competition plays an increasingly visible, yet contained, role.

Aircraft Altimeter And Pitot Tube Industry Leaders

Honeywell International Inc.

Garmin Ltd.

Thales Group

Meggitt Ltd. (Parker-Hannifin Corporation)

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: The US Army, through the Defense Logistics Agency, awarded Honeywell International, Inc. a USD 103 million contract to supply its Next-Generation APN-209 Radar Altimeter (Next Gen APN-209) system across various Army aircraft platforms.

- February 2022: Collins Aerospace established a long-term agreement with Hainan Airlines to supply Air Data Sensors, including Pitot and Total Air Temperature sensors, for its 500-aircraft fleet, which comprises A320, A330, and B737NG models.

Global Aircraft Altimeter And Pitot Tube Market Report Scope

| Altimeters |

| Pitot Tubes |

| Integrated Air-Data Modules |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Military Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Altimeters | ||

| Pitot Tubes | |||

| Integrated Air-Data Modules | |||

| By Platform | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Military Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aircraft altimeter and pitot tube market?

The aircraft altimeter and pitot tube market stands at USD 1.56 billion in 2025 and is projected to reach USD 2.17 billion by 2030.

How fast is demand expected to grow through 2030?

The market is forecasted to register a 6.82% CAGR.

Which component category is expanding the quickest?

The Integrated air-data modules segment is expected to grow at 7.14% CAGR.

Why is Asia-Pacific attracting attention from suppliers?

Fleet expansion in China and India drives a 7.95% CAGR for regional demand.

What is the main regulatory driver for retrofit activity?

Global ADS-B Out mandates requiring certified altitude-encoder accuracy.

Page last updated on: