Air Starter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 435.69 Million |

| Market Size (2031) | USD 547.83 Million |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

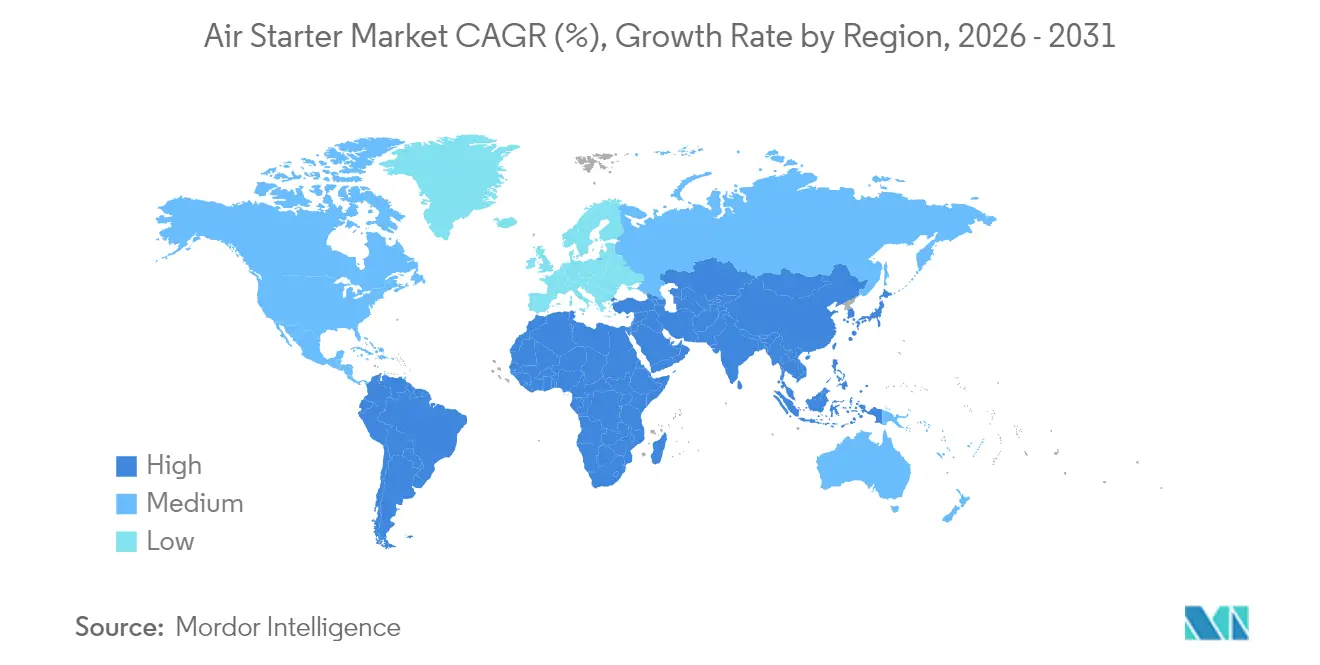

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Starter Market Analysis by Mordor Intelligence

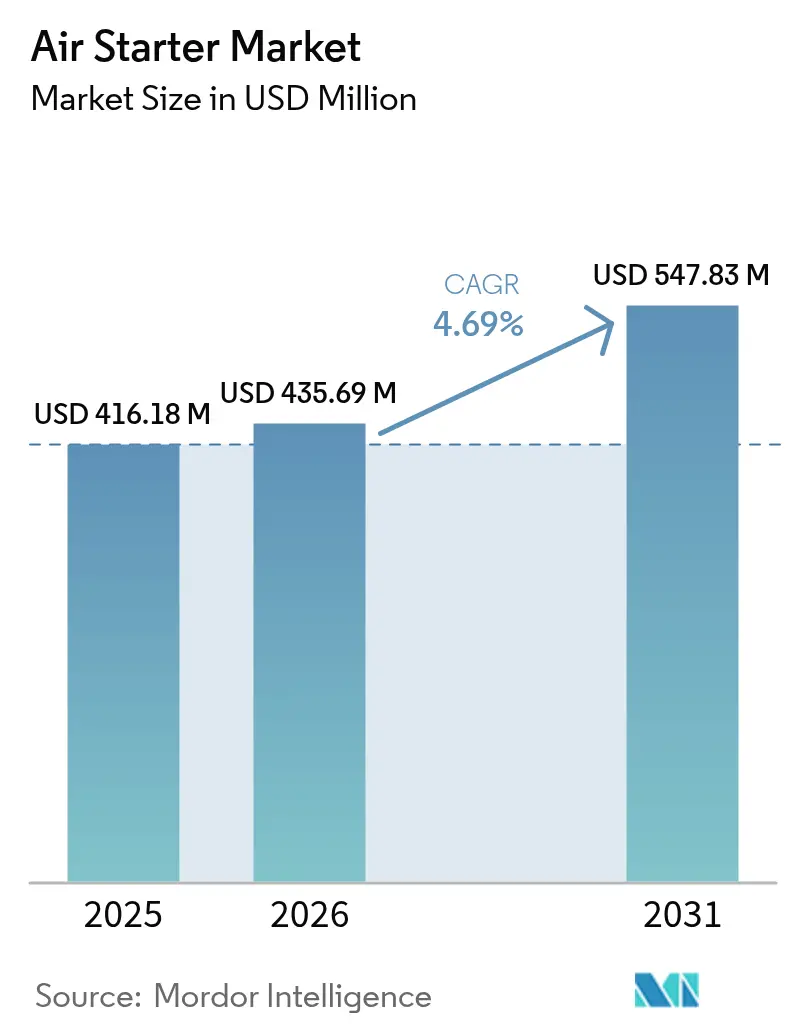

The Air Starter Market size was valued at USD 416.18 million in 2025 and estimated to grow from USD 435.69 million in 2026 to reach USD 547.83 million by 2031, at a CAGR of 4.69% during the forecast period (2026-2031).

Solid demand comes from hazardous-zone industries where pneumatic starters remain the safest ignition option, chiefly in oil and gas, LNG shipping, mining, and emerging hydrogen-ready power plants. OEMs emphasize ATEX- and IECEx-certified models to remove ignition risks, while fleet operators in LNG and dual-fuel shipping allocate larger capital budgets for starter upgrades. Mining contractors are scaling autonomous and electric fleets, which favor low-maintenance vane or hybrid systems. Retrofit programs for brownfield oil assets further expand installed bases, and service providers enhance aftermarket platforms that integrate hardware with predictive analytics to minimize downtime.

Key Report Takeaways

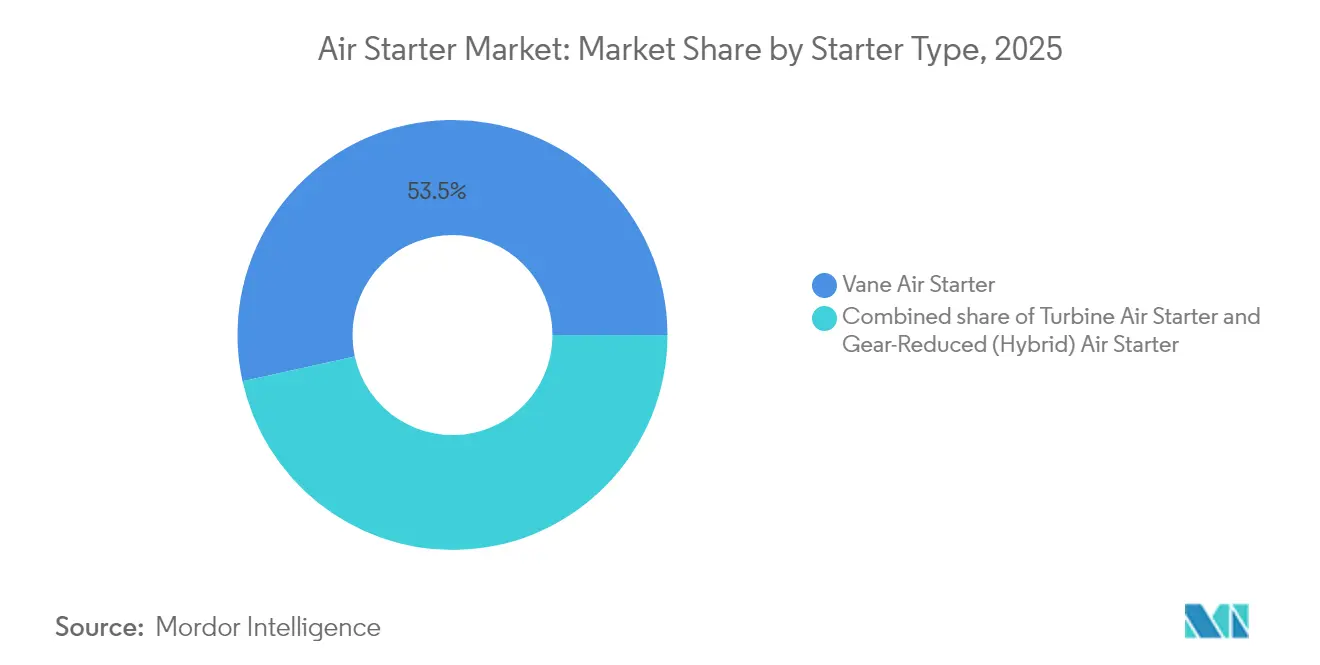

- By starter type, vane systems led with a 53.45% revenue share in 2025; gear-reduced hybrid units are forecast to expand at a 6.58% CAGR through 2031.

- By engine capacity, units with a capacity of up to 100 HP accounted for an 85.05% share of the air starter market size in 2025, whereas the 100-300 HP class is projected to grow at a 4.98% CAGR through 2031.

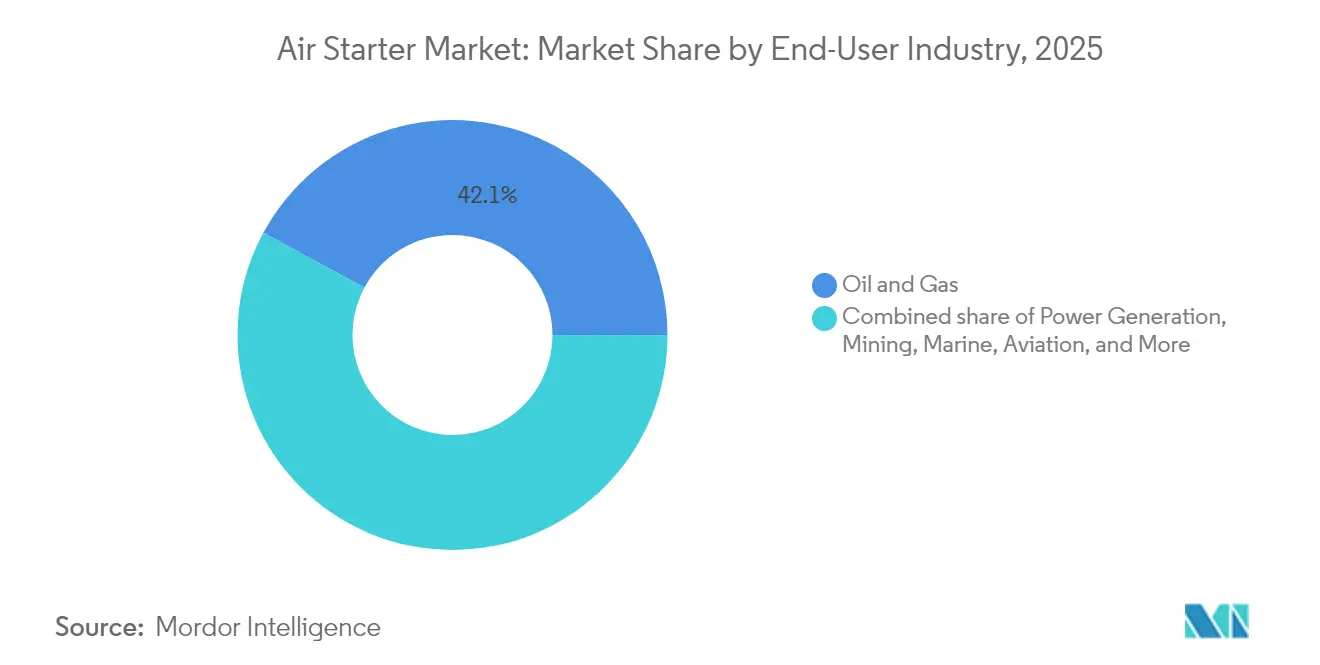

- By end-user industry, the oil and gas sector held 42.12% of the air starter market share in 2025 and is projected to advance at a 5.17% CAGR through 2031.

- By geography, North America commanded 39.45% of revenue in 2025, while Asia-Pacific is poised for the quickest expansion at a 6.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Starter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement of electric starters in hazardous zones | 0.80% | Global oil & gas, chemicals | Medium term (2–4 years) |

| LNG carrier fleet growth requiring ATEX starters | 0.60% | Global maritime, Asia-Pacific shipyards | Long term (≥4 years) |

| Brownfield life-extension retrofits | 0.70% | North America, Middle East, North Sea | Medium term (2–4 years) |

| Mining capex rebound | 0.50% | APAC, South America, Africa | Short term (≤2 years) |

| Hydrogen-ready gas turbine uptake | 0.40% | Europe, North America, Australia | Long term (≥4 years) |

| Autonomous haul trucks | 0.30% | Global mining regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising replacement of electric starters with pneumatic starters in hazardous zones

Industrial operators are standardizing ATEX- and IECEx-certified pneumatic solutions to mitigate ignition risks in Class I, Division 1 areas.[1]ABB Group, “IECEx Certification for Explosion Protection,” abb.com Insurers are increasingly flagging non-certified electric units, which accelerates retrofit cycles across refineries, grain silos, and chemical plants. The safety-driven transition prioritizes operational continuity over upfront cost, especially in upstream drilling and gas compressio,n where unscheduled outages carry hefty penalties. Resulting demand is buoyed by turnkey retrofit kits that minimize downtime and align with tightening regional safety audits.

Growth of LNG carrier fleet requiring ATEX-rated turbine starters

Global LNG shipping backlogs support persistent orders for explosion-proof turbine starters, a must for dual-fuel propulsion and cargo handling in volatile atmospheres.[2]The Maritime Executive, “Maersk Boosts Dual-Fuel Fleet Investment,” maritime-executive.com Danish, Korean, and Chinese yards embed these systems at the design stage, while owners increase budgets—Maersk raised its annual vessel capex to USD 10–11 billion—to future-proof their fleets for synthetic and bio-LNG operations. Floating production, storage, and offloading units echo this trend, emphasizing compact, corrosion-resistant designs to minimize offshore maintenance.

IOCs’ brownfield life-extension programs boosting retrofit demand

Roughly 70% of global oil now flows from mature fields, prompting life-extension schemes that replace aging electric starters with maintenance-light vane models.[3]Baker Hughes, “Mature Assets Solutions,” bakerhughes.com Operators gain quicker returns than greenfield projects and cut unplanned trips, a key priority for offshore platforms with aging electrical infrastructure. Service integrators bundle retrofits with remote monitoring to streamline post-installation support and reinforce compliance credentials.

Recovery in mining equipment capex post-2024 commodity super-cycle

Higher copper and lithium prices lifted order books for autonomous and electrified rigs; Epiroc logged a 17% Q1 2025 order jump.[4]Epiroc AB, “Q1 2025 Interim Report,” epiroc.com Underground hard-rock sites prize pneumatic starters for their dust tolerance, vibration resistance, and long uptime, which is critical, as even minute-long failures can erode profits exceeding USD 100,000 per hour. Integration of IoT sensors feeds predictive algorithms that align maintenance with scheduled stoppages, driving equipment reliability mandates across APAC and Latin America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric-drive frac pumps deleting start cycles | -0.60% | North America shale basins | Short term (≤2 years) |

| OEM consolidation trimming multi-vendor specs | -0.40% | Global industrial hubs | Medium term (2–4 years) |

| Legacy air leaks inflating ownership costs | -0.30% | Global factories | Long term (≥4 years) |

| Dry-lube vane material scarcity | -0.20% | Global supply chains | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Shift toward electric-drive frac pumps eliminating start-stop duty cycles

North American shale operators are transitioning to grid-powered or gas-turbine-generated electric frac spreads, which curbs the frequent engine restarts that historically drove air starter use. ProPetro’s three-year ExxonMobil deal exemplifies the shift, with dual-fuel or electric units already accounting for 65% of its fleet. Continuous pump operation reshapes starter demand patterns, forcing suppliers to diversify beyond legacy diesel applications.

OEM consolidation reducing multi-vendor starter specifications

Large industrial equipment builders are streamlining supply chains, locking in single-source agreements that narrow procurement rosters and squeeze smaller pneumatic specialists. Standardized platforms narrow customization margins and shift bargaining power toward integrators that can bundle starters with ancillary systems, thereby reducing the addressable volumes for niche vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Starter Type: Vane Systems Lead Despite Hybrid Innovation

Vane starters dominated the air starter market with a 53.45% share in 2025, reflecting a long track record of field reliability and straightforward servicing protocols. Oil and gas operators value these traits for remote sites where tooling and power may be constrained. Turbine models serve marine and aerospace equipment needing rapid spin-up. Hybrid gear-reduced designs are accelerating at a 6.58% CAGR, combining pneumatic drive with mechanical reduction to boost torque density for autonomous machinery and hydrogen-ready turbines. Additive manufacturing is now unlocking lightweight superalloy rotors that enhance thermal tolerance in extreme-duty turbine variants, positioning hybrids as a future growth driver in the broader air starter market.

Ongoing R&D focuses on sealing improvements, dry-lube coatings, and tighter tolerances achievable through metal additive processes. These innovations aim to widen maintenance intervals, a key selling point for unmanned mines or unmanned offshore installations. Progressive standards bodies are also updating certification schemes to streamline cross-acceptance between ATEX and regional codes, potentially lowering homologation costs for hybrid entrants.

By Engine Capacity: Small Engines Dominate Market Share

Units with a capacity of up to 100 HP captured 85.05% of the 2025 sales due to their sheer volume in compressors, gensets, and mobile machinery. Smaller displacement installations benefit from compact vane architectures that keep parts counts low and overhaul times short. The 100–300 HP tier is expanding at the fastest rate, with a 4.98% CAGR, as mid-sized mines and marine auxiliaries upgrade to larger, more efficient engines that require robust starters capable of delivering higher torque without proportionate increases in weight or air consumption. Sensor integration is spreading quickly across all capacity bands, enabling real-time tracking of temperature, rotation speed, and pressure to anticipate wear conditions and schedule just-in-time service.

Designers in the >300 HP class experiment with modular dual-starter packages for mission-critical gas turbines, providing redundancy that satisfies stringent availability contracts in peaking power plants. While volumes here are modest, ASPs are substantially higher, giving suppliers a profitable niche alongside mass-market small-engine applications within the broader air starter market.

By End-User Industry: Oil and Gas Sector Drives Growth

Holding 42.12% of 2025 revenue, oil and gas remains the anchor customer thanks to brownfield retrofits, LNG expansion, and midstream compressor upgrades. The segment also shows the quickest pace through 2031, at a 5.17% CAGR, because safety mandates and remote operations favor pneumatic over electric starters. Power generation follows where hydrogen-ready turbines need enhanced torque profiles. Mining demand is reviving with the rollouts of autonomous fleets, highlighting the robustness of starters in dusty, high-vibration environments. Marine applications—including LNG carriers and offshore support vessels—require ATEX-certified turbine models, which underpin a distinct, compliance-driven revenue stream within the air starter market.

Geography Analysis

North America led the way in 2025, accounting for 39.45% of revenue, driven by shale gas, offshore Gulf assets, and a robust pipeline of petrochemical upgrades. Harsh winters and desert heat test equipment to extremes, validating pneumatic resilience over a wide temperature range. The region’s aftermarket ecosystem is mature, offering rapid turnaround on rebuilds and certified spares, which reinforces loyalty to established brands.

The Asia-Pacific region is the growth pacesetter, with a 6.72% CAGR projected to 2031. China’s industrial hubs and India’s grid expansion fuel demand, while Korean and Chinese shipyards pack LNG carriers with turbine starters destined for export routes. Rising H2 pilot projects in Japan and Australia further diversify orders toward high-torque designs suited for blended fuels. Local component suppliers are stepping up to shorten lead times, although ATEX compliance still favors European and U.S. firms in securing premium contracts.

Europe maintains a balanced outlook as legacy industries adapt to meet stringent worker safety directives. Hydrogen clusters in Germany and the Nordics create pockets of specialized demand for certified high-torque systems. The Middle East leverages brownfield gas infrastructure spending, and Africa’s copper and gold corridors drive mining-centric sales, both contributing to a steady flow of projects that keep regional service depots active within the global air starter market.

Competitive Landscape

The field is moderately fragmented. Ingersoll Rand leads with a global service reach and 14 acquisitions in 2024 that deepened its air treatment and pump offerings, including a USD 146 million deal for Friulair. Competitors such as TDI, Gali, and Hilliard focus on niche turbine or vane specialties, while Epiroc and Caterpillar integrate proprietary starters into mining fleets. Technology battles now revolve around predictive analytics, additive manufacturing, and ultra-low-maintenance hybrid designs.

Strategic plays include vertical integration—pairing starters with compressors, dryers, and remote dashboards—to lock in customers across the entire equipment lifecycle. Certification leadership also matters; suppliers with harmonized ATEX, IECEx, and regional stamps win critical orders in high-risk zones. However, price competition exists for commoditized vane models, with value shifting toward total cost of ownership and uptime guarantees, thereby insulating premium suppliers from low-cost entrants.

Air Starter Industry Leaders

Ingersoll Rand plc

Tech Development Inc. (TDI)

Gali International

Austart

IPU Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ingersoll Rand acquired G & D Chillers and Advanced Gas Technologies for USD 27 million to expand its air treatment and on-site gas generation portfolios.

- February 2025: Ingersoll Rand acquired SSI Aeration, strengthening water-treatment markets with membrane diffusers that dovetail with compressed-air systems.

- February 2025: Ingersoll Rand reported 2024 revenue of USD 7.235 billion, a 5% increase, driven by industrial technologies.

- January 2025: Safran, Turbotech, and Air Liquide validated liquid-hydrogen turboshaft demonstrators, spotlighting starter requirements for cryogenic fuel ecosystems.

Global Air Starter Market Report Scope

The air starter market report includes:

| Vane Air Starter |

| Turbine Air Starter |

| Gear-Reduced (Hybrid) Air Starter |

| Up to 100 HP |

| 100 to 300 HP |

| Above 300 HP |

| Oil and Gas |

| Power Generation |

| Mining |

| Marine (LNG, FPSO, Naval) |

| Aviation |

| Transportation (Heavy-Duty Trucks, Rail) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Starter Type | Vane Air Starter | |

| Turbine Air Starter | ||

| Gear-Reduced (Hybrid) Air Starter | ||

| By Horsepower Rating | Up to 100 HP | |

| 100 to 300 HP | ||

| Above 300 HP | ||

| By End-User Industry | Oil and Gas | |

| Power Generation | ||

| Mining | ||

| Marine (LNG, FPSO, Naval) | ||

| Aviation | ||

| Transportation (Heavy-Duty Trucks, Rail) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the air starter market?

The Air Starter Market size was USD 435.69 million in 2026 and is forecast to climb to USD547.83 million by 2031.

Which segment is growing fastest within the air starter market?

Gear-reduced hybrid air starters post the highest growth, advancing at a 6.58% CAGR through 2031.

Why are pneumatic starters preferred in LNG carriers?

ATEX-rated pneumatic turbine starters eliminate ignition sources in explosive cargo environments, meeting safety codes for dual-fuel propulsion.

How will electric-drive frac pumps affect air starter demand?

Continuous electric pumps reduce start-stop cycles, curbing short-term pneumatic starter requirements in North American shale operations.

Which region will lead air starter market growth up to 2031?

Asia-Pacific is projected to record the fastest regional CAGR at 6.72%, driven by industrial expansion, LNG infrastructure and shipbuilding backlogs.

What role does predictive maintenance play in the air starter industry?

Sensors and analytics platforms forecast service needs, decreasing downtime and strengthening the aftermarket’s share in long-term revenue.

Page last updated on: