Blowers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.09 Billion |

| Market Size (2031) | USD 11.39 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

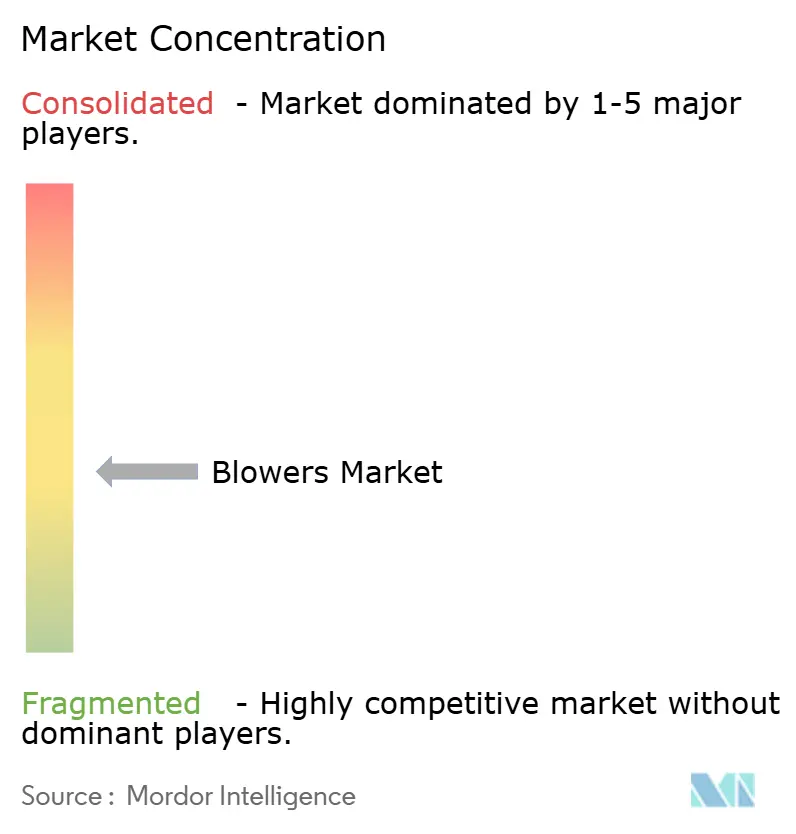

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blowers Market Analysis by Mordor Intelligence

The Blowers Market size is expected to grow from USD 8.69 billion in 2025 to USD 9.09 billion in 2026 and is forecast to reach USD 11.39 billion by 2031 at 4.62% CAGR over 2026-2031.

Growing wastewater-treatment capacity additions, tougher industrial emission standards, and the migration from oil-lubricated machines to magnetic-bearing designs, which cut energy use by 30%, are the primary drivers of growth. End users view energy as more than 40% of total wastewater-plant operating costs, making efficiency upgrades financially compelling. The Asia-Pacific region leads demand, driven by public infrastructure spending, while medium-pressure applications in the process industries register the fastest incremental volume growth. Consolidation among top suppliers is reshaping the competitive landscape as firms acquire technology specialists to expand their portfolios and reduce the lifecycle costs of air-handling systems.

Key Report Takeaways

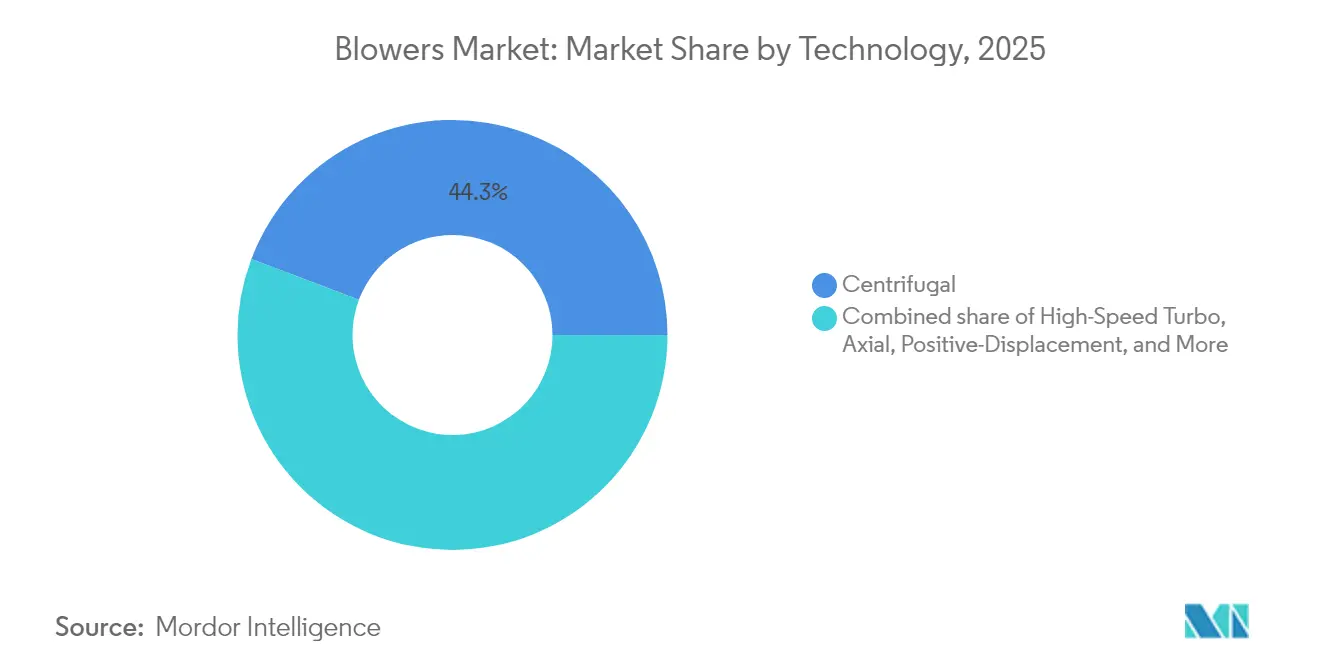

- By technology, centrifugal blowers held 44.25% of the blower market share in 2025, whereas high-speed turbo blowers are projected to expand at a 5.86% CAGR to 2031.

- By pressure range, low-pressure units captured 41.85% of the blower market size in 2025, while the medium-pressure segment is poised to grow at a 5.46% CAGR during the forecast period.

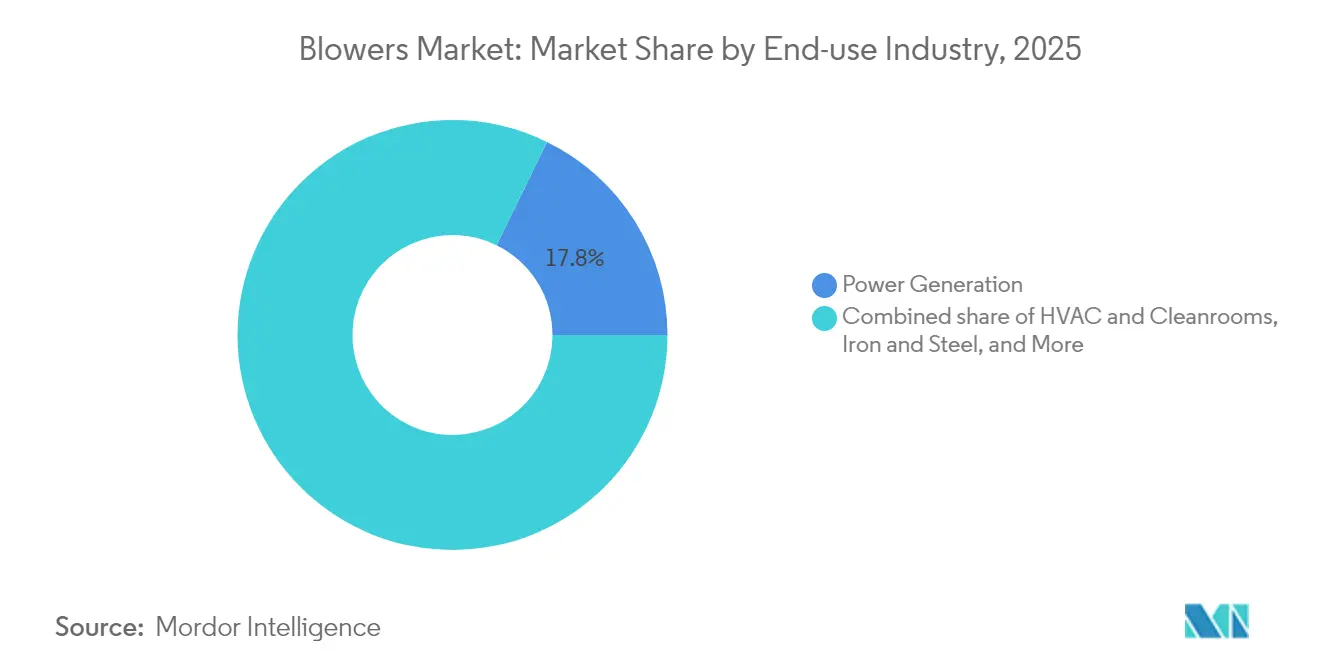

- By end-use industry, power generation accounted for an 17.75% revenue share of the blower market size in 2025; HVAC and cleanrooms are projected to advance at a 6.44% CAGR through 2031.

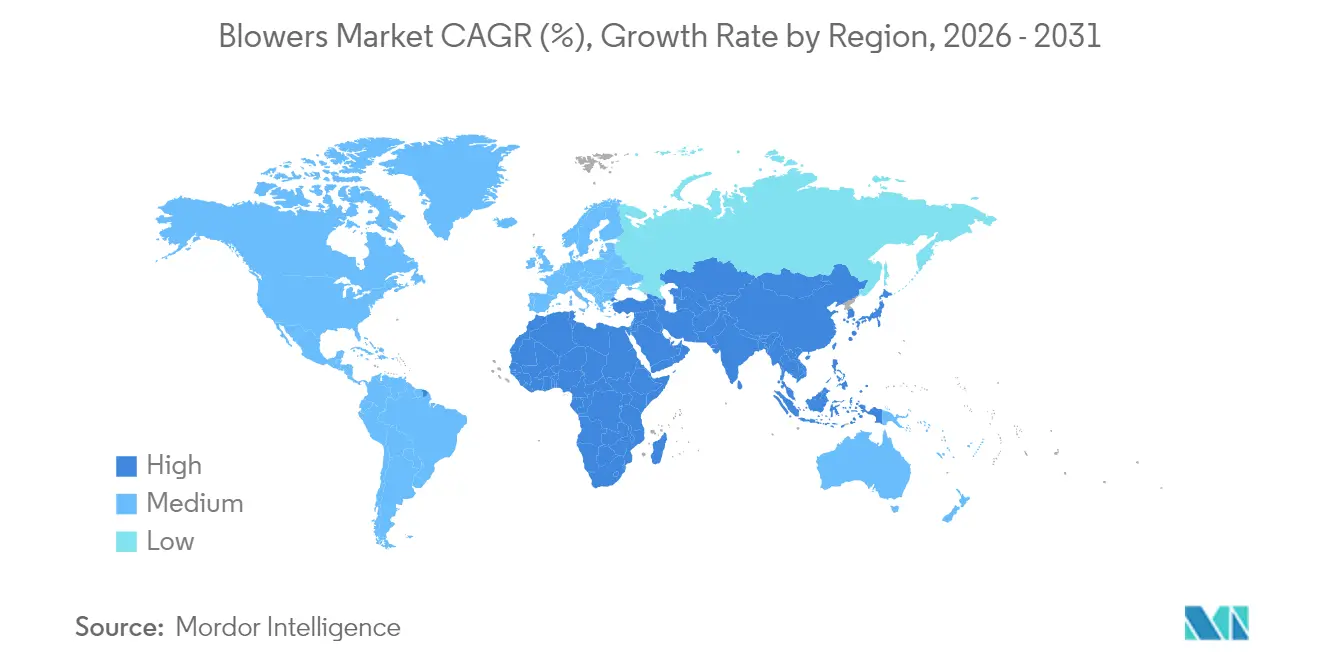

- By geography, the Asia-Pacific region commanded 43.10% of 2025 sales and is also the fastest-growing regional market, with a 5.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blowers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of wastewater-treatment infrastructure | +1.20% | Global, with APAC and MEA leading | Medium term (2-4 years) |

| Stricter industrial air-emission regulations | +0.80% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Power-generation additions in emerging economies | +0.90% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Industrial energy-efficiency retrofits | +0.70% | Global, with EU and North America early adoption | Short term (≤ 2 years) |

| Data-centre liquid-cooling demand for high-pressure blowers | +0.60% | North America, APAC, expanding to EU | Short term (≤ 2 years) |

| Farm-scale biogas digesters boosting regenerative blowers | +0.40% | EU, North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Wastewater-Treatment Infrastructure

Municipal and industrial wastewater facilities are increasing their aeration capacity, which typically accounts for 40-60% of a plant’s electricity budget, resulting in sustained demand for blowers.(1)Mark Hinckley, “Magnetic Bearings: An Attractive Force for Energy-efficiency,” blowervacuumbestpractices.com A retrofit at the Kansas Water Resource Recovery Facility cut annual energy costs by USD 35,000 after switching to high-speed integrally geared blowers. Asia-Pacific governments are coupling water-scarcity concerns with stricter discharge rules, spurring the uptake of centrifugal and magnetic-bearing turbo models that provide precise dissolved-oxygen control. Modular treatment packages help smaller municipalities standardize procurement, indirectly boosting the blower market by favoring brands with proven reliability. Vendors able to supply digital monitoring and predictive-maintenance software gain further advantage as utilities target whole-of-life operating savings.

Stricter Industrial Air-Emission Regulations

Tightening particulate and gas limits across chemical, power, and food-processing plants are pushing operators to acquire blowers that sustain constant flow under variable conditions.(2)Britt Burt & Brock Ramey, “U.S. Power Industry Outlook 2025,” turbomachinerymag.comThe United States plans 875 GW of new generating capacity between 2025-2029, each project integrating flue-gas treatment systems reliant on high-efficiency blowers. Europe’s revised Industrial Emissions Directive incorporates continuous emissions monitoring, a specification that favors magnetic-bearing turbo designs due to their oil-free reliability. Pharmaceutical producers and cleanrooms now require class 100 or better airflow, broadening the regulatory pull on the blower market. Overall, compliance costs steer procurement toward premium machines with verifiable energy and uptime metrics, enabling suppliers to secure higher margins despite price-sensitive sectors.

Power-Generation Additions in Emerging Economies

Rising electricity demand in the APAC and MEA regions underpins orders for forced-draft, induced-draft, and flue-gas desulfurization blowers that maintain combustion efficiency in natural-gas plants. The parallel rollout of utility-scale solar and wind power adds balancing requirements, driving demand for high-reliability machines that can cycle frequently without service downtime. Data centre proliferation creates a still-niche but fast-growing need for high-pressure liquid-cooling blowers capable of producing a stable output of 70+ kPa. Industrial gas-turbine packages likewise demand precision air-handling, often bundled with OEM maintenance agreements that lock in long-term parts revenue for blower vendors. In emerging markets, utilities prioritize low total cost of ownership, which reinforces the sales of magnetic-bearing systems, even where capital budgets remain constrained.

Industrial Energy-Efficiency Retrofits

Manufacturers worldwide target aggressive reductions in Scope 1 and Scope 2 emissions, translating into systematic upgrades of blower systems. The Victor Valley Wastewater Reclamation Authority reported an annual savings of 928,000 kWh and a cost reduction of USD 98,000 after replacing aging units with VFD-equipped alternatives. Energy-service companies now structure retrofit projects on performance-guarantee contracts, removing upfront capital expenditure barriers for plant operators. Variable-frequency drives, matched with smart control algorithms, enable facilities to trim airflow during low-load periods without compromising process stability, thereby reinforcing the demand for digitally enabled blower systems. High electricity tariffs and carbon pricing in the EU quicken payback periods, sharpening interest in magnetic-levitation solutions that cut operating expenditure by double-digit percentages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel & copper price volatility | -0.50% | Global, with manufacturing-heavy regions most affected | Short term (≤ 2 years) |

| High energy consumption and noise versus alternative tech | -0.30% | Global, with stricter regulations in EU and North America | Medium term (2-4 years) |

| Magnetic-levitation turbo blowers cannibalising legacy units | -0.40% | North America & EU early adoption, expanding globally | Medium term (2-4 years) |

| Rare-earth magnet supply-chain exposure | -0.20% | Global, with China-dependent supply chains most vulnerable | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel & Copper Price Volatility

Commodity swings create budget uncertainty for end users and margin pressure for manufacturers, especially given steel’s weight in centrifugal-blower housings and copper’s role in motor windings. Producers respond by dual-sourcing metals and carrying higher inventories, which raises working-capital needs. Projects in cost-sensitive sectors often defer purchase orders until price signals stabilize, temporarily damping blower market demand. EPC contractors now insert price-escalation clauses into contracts, transferring part of the raw-material risk back to clients. Although hedging instruments offer partial relief, sustained volatility could delay large wastewater plant tenders scheduled for 2026-2027.

Magnetic-Levitation Turbo Blowers Cannibalising Legacy Units

Magnetic bearings reduce energy use by 30% and maintenance costs by 95%, enabling paybacks of two to three years that motivate rapid replacement of legacy systems. The resulting substitution erodes aftermarket revenue from the installed base for conventional-technology suppliers. Manufacturers without magnetic expertise face accelerated obsolescence unless they license or acquire suitable platforms. The upgrading trend is most intense in wastewater and high-duty industrial processes where uptime is critical. Over the medium term, the shift may cap unit-shipment growth in traditional positive-displacement segments even as overall blower market revenue rises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Centrifugal Dominance Faces Turbo Disruption

The blower market size for centrifugal technology accounts for a 44.25% share in 2025, reflecting decades of proven reliability in municipal wastewater and general industrial applications. High-speed turbo designs, however, are projected to register a 5.86% CAGR through 2031, as buyers prioritize lifetime energy savings. Centrifugal models still appeal where lower upfront cost and simpler maintenance outweigh efficiency benefits, especially in developing regions with limited technical skill availability. Suppliers position hybrid portfolios that combine in-house centrifugal lines with acquired magnetic-bearing offerings to defend their market share. Turbo machines are increasingly integrating condition-monitoring sensors, providing operators with real-time data that further enhances their perceived value. Positive-displacement roots blowers retain relevance in flow-constant applications, such as the pneumatic conveying of bulk solids, although their share is declining. Axial machines occupy a niche in high-volume, low-pressure cooling towers, while regenerative units are growing in farm-scale biogas digesters, where moisture-tolerant airflows are crucial.

Second-generation turbo blowers operate at rotational speeds exceeding 40,000 rpm, supported by advanced micro-mesh filters that enhance bearing life in dusty environments. Several manufacturers now bundle software that automatically tunes impeller pitch to maintain efficiency across fluctuating loads, a key differentiator in variable-torque wastewater aeration. As magnet supply risks persist, a subset of operators signals interest in hybrid ceramic-bearing technology, although these prototypes remain unproven at an industrial scale. Overall, centrifugal equipment is expected to keep numerical leadership but cede incremental revenue gains to turbo units in high-value segments.

By Pressure Range: Medium-Pressure Applications Drive Growth

Low-pressure machines, operating below 15 kPa, secured 41.85% of the blower market share in 2025, primarily driven by municipal aeration basins and HVAC distribution. Medium-pressure equipment (15-70 kPa) is expanding at a 5.46% CAGR, as chemical plants, cement kilns, and material-handling lines modernize with tighter process controls. The increasing demand for precise pressure regulation in specialty chemicals is driving the need for pneumatic transport systems, which centrifugal and turbo models effectively deliver. High-pressure variants above 70 kPa address niche combustion air and gas compression duties, with order intake tied to oil refinery turnarounds and gas turbine installations. Process intensification trends, such as higher throughput reactors, necessitate variable-speed drives that enable rapid pressure adjustments without wasting energy. Solution providers differentiate through integrated medium-voltage drives like SINAMICS PERFECT HARMONY GH180, which ensures stable output across a 10:1 speed range.

Emerging markets favor standardized medium-pressure skid packages, allowing faster greenfield plant startups while mitigating skill shortages. To tap into that need, several OEMs have relocated their final assembly closer to APAC, thereby cutting logistics costs and import duties. Aftermarket service revenues also tend to favor medium-pressure applications, as industrial users often sign multi-year performance agreements that cover instrumentation calibration and impeller rebalancing.

By End-use Industry: HVAC & Cleanrooms Emerge as Growth Leader

Power generation accounted for 17.75% of the global blower market size in 2025. Base-load fossil plants, combined-cycle gas units, and biomass boilers rely on induced-draft and flue-gas desulfurization blowers to regulate combustion and control emissions. However, HVAC and cleanroom installations are projected to grow at a 6.44% CAGR to 2031 as the semiconductor and biologics industries build dozens of ultra-clean fabs. These facilities require laminar airflow that maintains ISO 14644 Class 1-5 particulate thresholds, often necessitating redundancy and magnetic-bearing designs to prevent oil contamination. Food and beverage processors incorporate hygienic stainless-steel blowers to comply with stricter sanitation codes, while the construction and cement segments utilize medium-pressure machines for material blending and dust mitigation.

Oil and gas applications face mixed fortunes: upstream gas gathering stations still specify regenerative blowers for vapor recovery, but downstream refineries defer non-critical capex amid energy transition uncertainty. Meanwhile, mining and metals expand cautiously alongside base-metal demand for electric-vehicle batteries, generating steady but unspectacular blower volumes. Across industries, the pivot toward digital maintenance dashboards that integrate vibration analytics is uniform, highlighting that ancillary software now influences purchase choice as much as mechanical design.

Geography Analysis

The Asia-Pacific region underpinned USD 3.75 billion worth of blower sales in 2025, accounting for 43.10% of the global value. China’s “Zero Discharge” mandates accelerate municipal wastewater upgrades, while India’s Jal Jeevan Mission funds new treatment plants that collectively boost the adoption of centrifugal and turbo blowers. ASEAN electronics hubs in Vietnam and Malaysia are installing cleanroom-grade HVAC blowers to support the fast-rising chip-assembly exports. The region’s 5.02% CAGR outlook reflects both greenfield infrastructure and retrofits aimed at lowering energy intensity.

North America follows with mature but lucrative replacement demand. Utilities retrofit aged aeration equipment with VFD-linked turbo blowers to comply with state energy-efficiency incentives. The build-out of data centres across the United States generates high-pressure liquid-cooling orders, providing suppliers with margin-rich project opportunities. Federal emission-reduction targets are accelerating the early adoption of magnetic-bearing technologies in petrochemical clusters along the Gulf Coast. Canada’s expanding biogas programs enhance sales of moisture-resistant regenerative units for anaerobic digesters.

Europe sustains premium pricing on the back of the Industrial Emissions Directive, encouraging facilities to buy oil-free machines that guarantee class-zero air purity. Germany’s chemical and pharmaceutical complexes are investing in variable-speed centrifugal blowers to reduce energy bills amid rising carbon charges. The region’s advanced aftermarket environment favors subscription-based maintenance services, expanding recurring revenue streams. South America and the Middle East & Africa collectively contributed less than 10% of the 2025 volume, but signal upside linked to desalination plants and mining projects. Currency and political risks temper short-term adoption; however, international financiers’ focus on water security in the MEA supports long-term growth in the blower market.

Competitive Landscape

The blower market exhibits moderate fragmentation, with the top five vendors controlling an estimated 35-40% of global revenue, leaving sizable room for regional specialists. Ingersoll Rand spent more than USD 300 million on acquisitions between 2024-2025, adding wastewater and air-treatment expertise to its industrial portfolio. Atlas Copco’s 2025 acquisition of Korean compressor maker Kyungwon Machinery expands its Asia-Pacific manufacturing footprint and reduces lead times for regional buyers. Such inorganic moves demonstrate that scale and technological depth are critical to defending a share in energy-efficient magnetic-bearing segments.

Technology integration stands out as the competitive frontier. Market leaders bundle IoT nodes that stream vibration, temperature, and bearing data to cloud dashboards, enabling predictive maintenance and remote troubleshooting. Start-ups targeting the blower industry leverage proprietary bearing materials or advanced aerodynamics to achieve sub-0.1 kW/m³/min efficiency metrics, pressuring incumbents to accelerate R&D. Price rivalry remains intense in low-pressure municipal tenders, but differentiation through life-cycle cost modeling enables premium brands to secure supply agreements despite higher upfront prices.

Regional dynamics add complexity. Chinese domestic suppliers are growing rapidly in mid-tier municipal projects, yet they struggle to enter export-controlled semiconductor cleanrooms that require ISO-certified, oil-free air. European firms capitalize on stringent environmental regulations to sell high-end magnetic-levitation units, while North American OEMs focus on aftermarket contracts that secure parts and service revenue. Raw-material cost volatility squeezes smaller producers, who lack purchasing leverage, catalyzing further consolidation over the forecast horizon.

Blowers Industry Leaders

Continental Blower LLC

CG Power and Industrial Solutions Limited

DongKun Industrial Co. Ltd

Howden Group Ltd

Loren Cook Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Atlas Copco announced the pending acquisition of Kyungwon Machinery Industry Co. Ltd. for about 465 MSEK (USD 43 million) to enhance its Industrial Air Division's reach in Asia-Pacific.

- February 2025: Ingersoll Rand acquired SSI Aeration, a wastewater treatment specialist with USD 30 million in revenue, thereby boosting its municipal solutions portfolio.

- October 2024: Ingersoll Rand acquired Air Power Systems (APSCO), Blutek, and UT Pumps for a combined total of USD 135 million, adding compressed air and specialty pump technologies to its portfolio.

- February 2024: Ingersoll Rand finalized the acquisition of Friulair S.r.l. for USD 146 million, expanding its air treatment solutions, particularly in the food and beverage and pharmaceutical sectors.

Global Blowers Market Report Scope

Blowers are mechanical devices that move gas or air in a certain direction, at a certain speed, and at a certain angle to maximize the rate of heat transfer and the efficiency of the process.These are used to heat, cool, ventilate, and move the air that industrial processes require.These systems typically consist of a fan, an electric motor, a drive system, ducts or pipes, flow control devices, and air conditioning equipment, such as filters and cooling coils.

The blower market is segmented by type, deployment, and geography. By type, the market is segmented into centrifugal and axial, and by deployment, the market is segmented into industrial and commercial. The report also covers the market size and forecasts for the blower market across major regions. For each segment, the market sizing and forecasts have been done based on revenue capacity in USD billions.

| Centrifugal |

| Axial |

| Positive-Displacement (Roots) |

| High-Speed Turbo |

| Regenerative |

| Low (Below 15 kPa) |

| Medium (15 to 70 kPa) |

| High (Above 70 kPa) |

| Power Generation |

| Oil and Gas |

| Iron and Steel |

| Chemical and Petrochemical |

| Mining and Metals |

| Construction and Cement |

| Food and Beverage |

| Waste-Water Treatment |

| HVAC & Cleanrooms |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Centrifugal | |

| Axial | ||

| Positive-Displacement (Roots) | ||

| High-Speed Turbo | ||

| Regenerative | ||

| By Pressure Range | Low (Below 15 kPa) | |

| Medium (15 to 70 kPa) | ||

| High (Above 70 kPa) | ||

| By End-use Industry | Power Generation | |

| Oil and Gas | ||

| Iron and Steel | ||

| Chemical and Petrochemical | ||

| Mining and Metals | ||

| Construction and Cement | ||

| Food and Beverage | ||

| Waste-Water Treatment | ||

| HVAC & Cleanrooms | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the global blower market size in 2026?

The blower market size reached USD 9.09 billion in 2026.

How fast is the blower market expected to grow?

Between 2026 and 2031, the blower market is projected to post a 4.62% CAGR.

Which region leads the blower market?

Asia-Pacific held 43.10% of global revenue in 2025 and is also the fastest-growing region at 5.02% CAGR through 2031.

What technology segment is growing the quickest?

High-speed turbo blowers are forecast to expand at 5.86% CAGR, the fastest among all technology segments.

Why are magnetic-bearing blowers gaining popularity?

Magnetic-bearing units lower energy consumption by 30% and cut maintenance costs by 95%, yielding paybacks in under three years.

Which end-use industry will grow most rapidly?

HVAC and cleanroom applications are expected to advance at 6.44% CAGR through 2031, outpacing all other industries.

Page last updated on: