Agriculture Analytics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

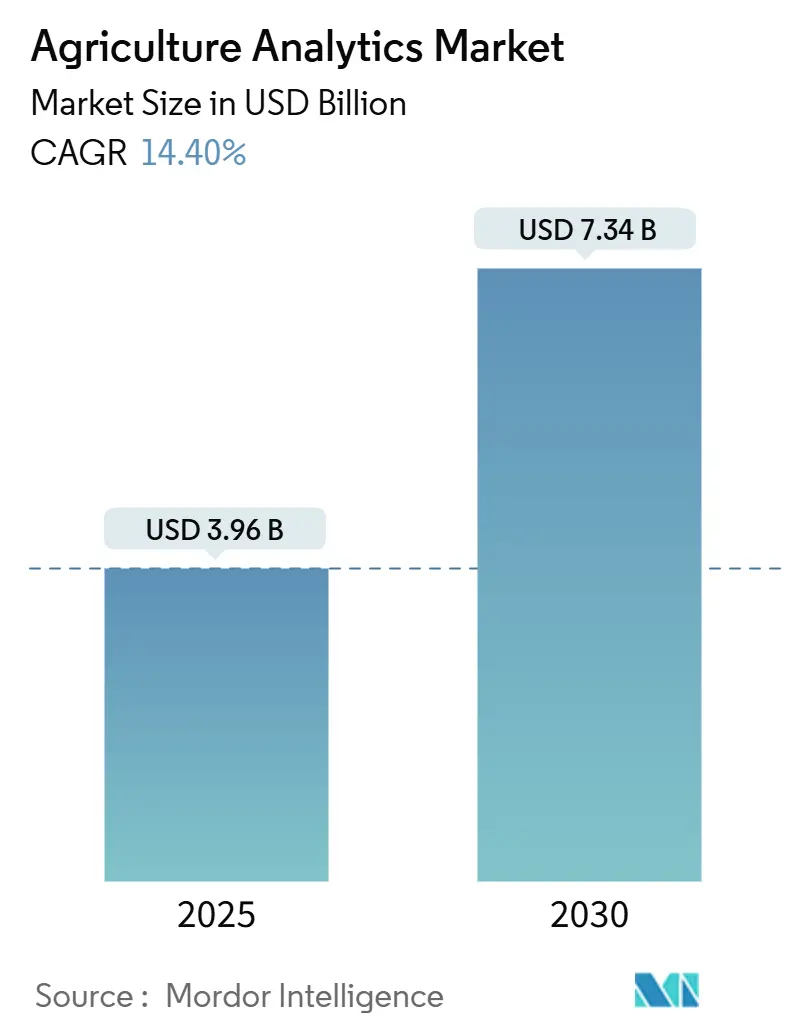

| Market Size (2025) | USD 3.96 Billion |

| Market Size (2030) | USD 7.34 Billion |

| Growth Rate (2025 - 2030) | 14.40% CAGR |

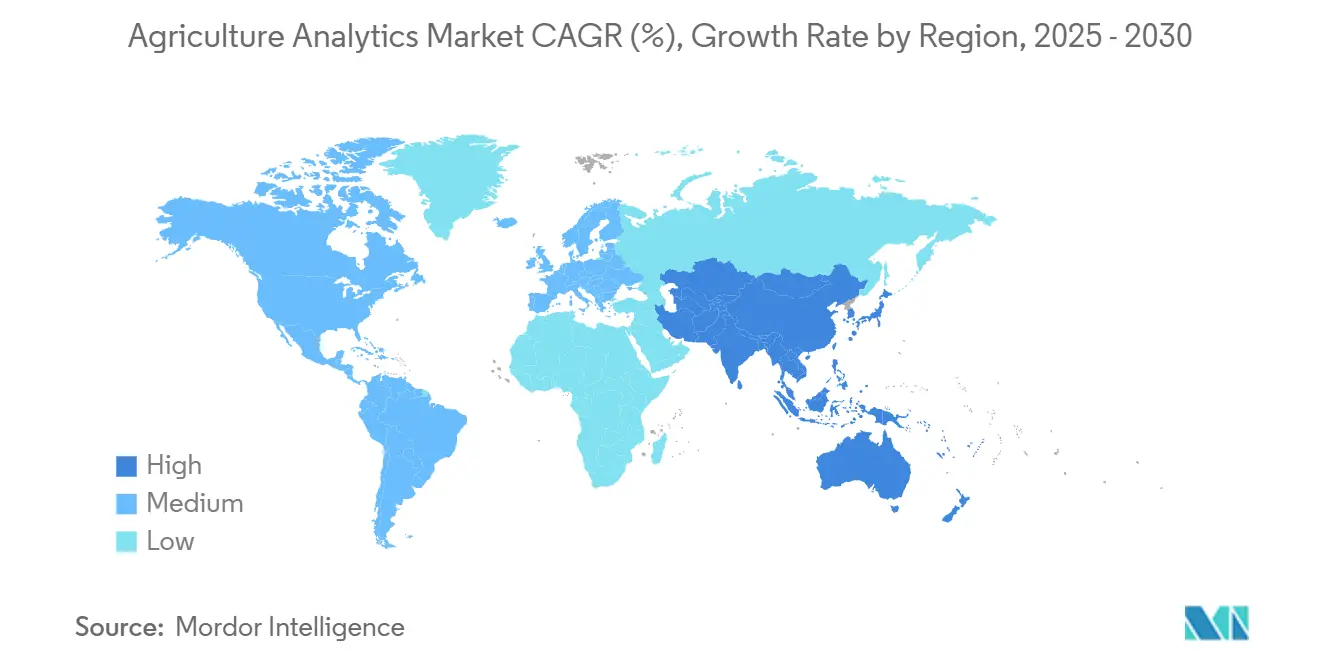

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

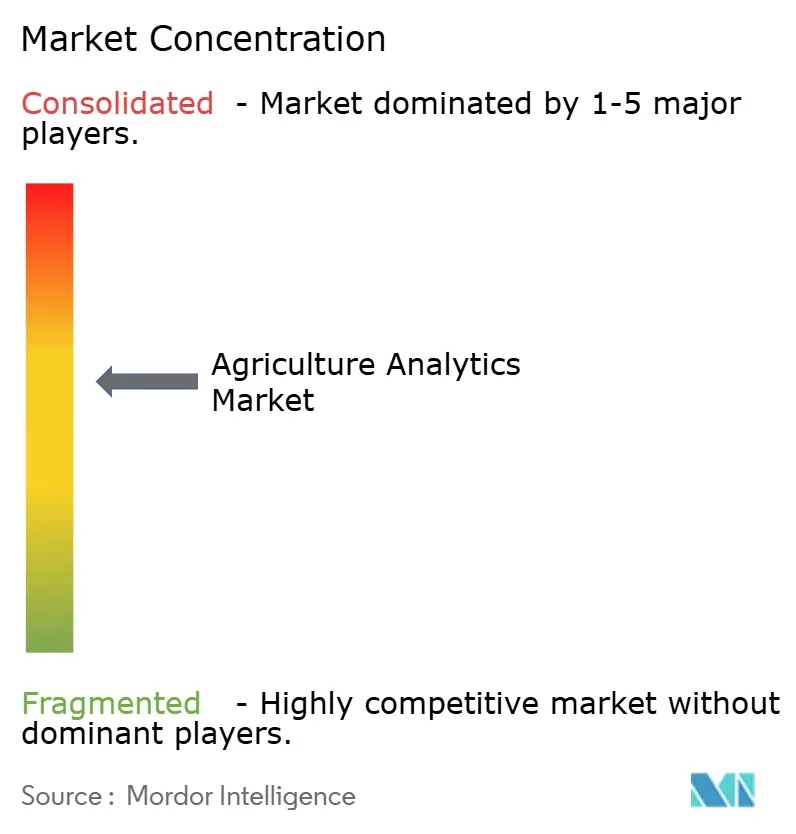

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Agriculture Analytics Market Analysis by Mordor Intelligence

The Agriculture Analytics Market size is estimated at USD 3.96 billion in 2025, and is expected to reach USD 7.34 billion by 2030, at a CAGR of 14.40% during the forecast period (2025-2030). Adoption is accelerating as falling edge-AI hardware prices, frequent satellite revisits, and policy-mandated compliance dashboards converge with growers’ need to optimize inputs and document sustainability. Solutions remain the largest revenue generator, yet managed services expand faster as farms turn to outcome-based contracts. Growth is also shaped by cloud–edge hybrid architectures, high-resolution UAV imagery, and the shift from predictive models toward cognitive AI that interprets complex farm data in natural language. Competitive intensity stays moderate: incumbent equipment firms are integrating software, while domain specialists target livestock, aquaculture, and carbon-market niches to unlock new revenue.

Key Report Takeaways

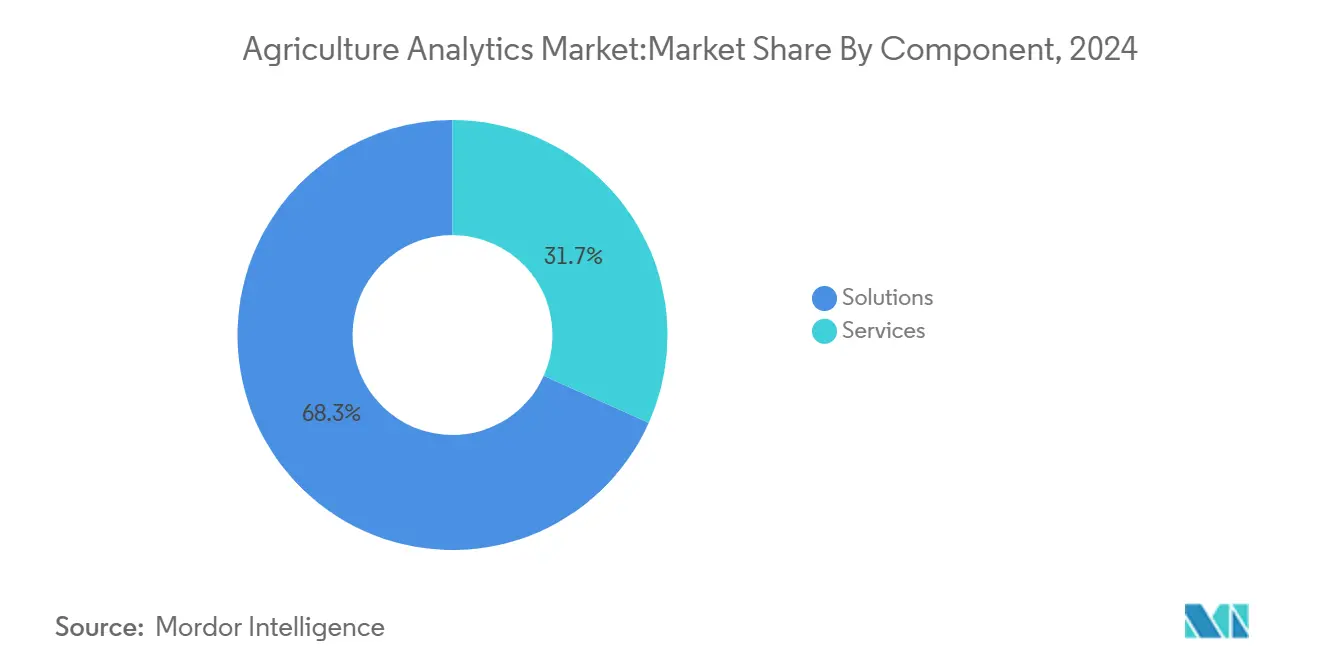

- By component, solutions held 68.3% of the Agriculture analytics market share in 2024; services are advancing at a 16.2% CAGR through 2030.

- By application, farm analytics led with 46.7% revenue share in 2024, whereas livestock analytics is set to expand at a 15.9% CAGR to 2030.

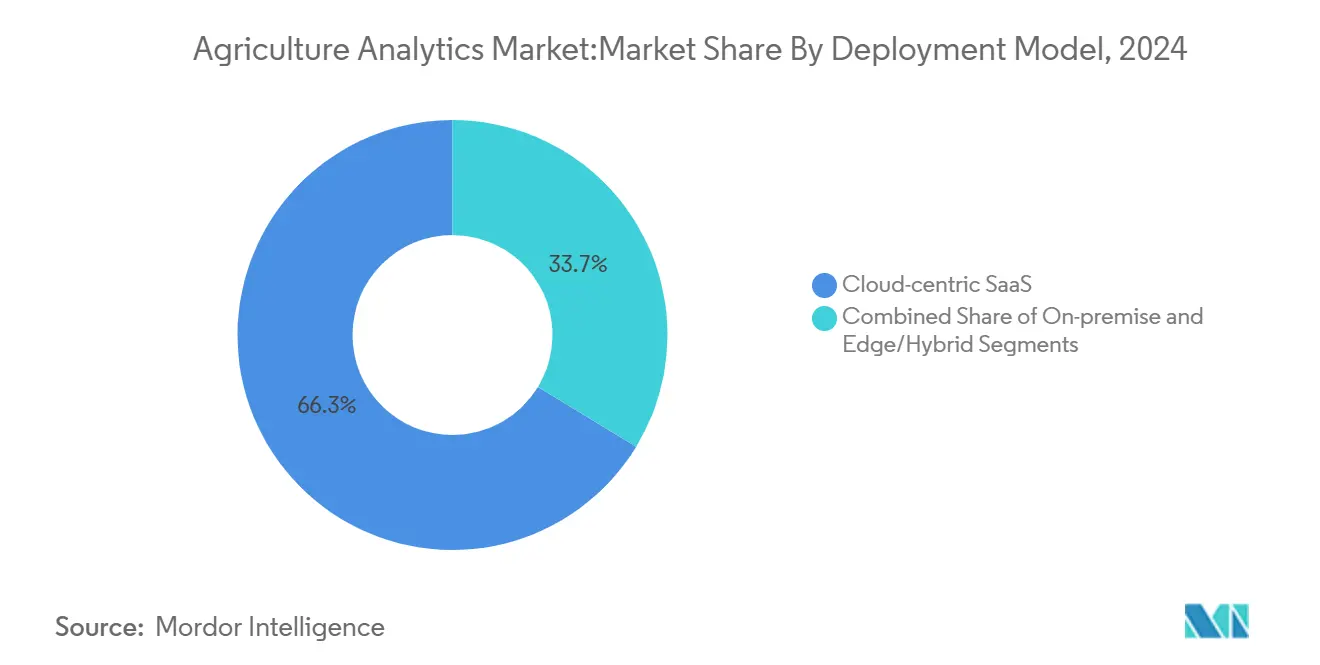

- By deployment model, cloud-centric SaaS captured 66.3% share of the Agriculture analytics market size in 2024; the edge/hybrid segment is growing at 15.3% CAGR to 2030.

- By farm size, large farms accounted for 28.2% of Agriculture analytics market size in 2024, while small farms register the fastest 16.1% CAGR through 2030.

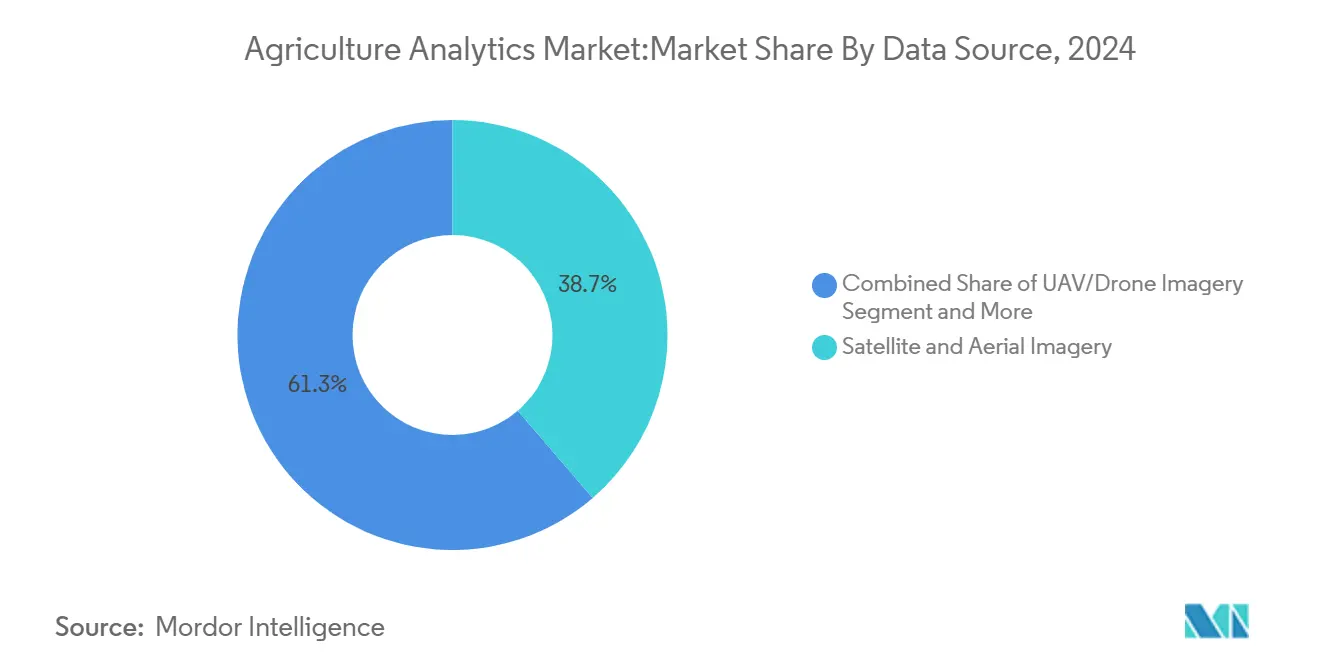

- By data source, satellite and aerial imagery commanded a 38.7% share in 2024; UAV imagery is progressing at a 15.8% CAGR to 2030.

- By analytics technique, predictive machine learning controlled 44.6% share in 2024, yet cognitive AI is forecast to rise at 16.4% CAGR through 2030.

- By geography, North America held 36.5% of the Agriculture analytics market in 2024; Asia-Pacific is the fastest-growing region at 15.6% CAGR through 2030.

Global Agriculture Analytics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-farming ROI crossing 20% on large row-crop farms | +2.8% | North America and the EU; spill-over to APAC | Medium term (2-4 years) |

| Ag-retailers bundling analytics-as-a-service contracts | +2.1% | Global; early gains in North America, Europe | Short term (≤ 2 years) |

| Subsidy-linked "smart compliance" dashboards in EU CAP 2027 | +1.9% | Europe; replication potential elsewhere | Medium term (2-4 years) |

| On-farm carbon-credit monetisation platforms | +1.7% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Edge-AI chips dropping below USD 5/unit for ag-IoT cameras | +2.3% | Global; strongest in price-sensitive markets | Short term (≤ 2 years) |

| Satellite SAR constellations hitting sub-3-day revisit time | +1.4% | Global, priority in precision agriculture regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Digital-farming ROI Crossing 20% on Large Row-Crop Farms

Return on investment for precision agriculture consistently exceeds 20% on expansive row-crop operations, incentivizing large growers to scale analytics platforms. Cost savings stem from variable-rate inputs and optimized machinery scheduling, while yield gains arise from site-specific seed prescriptions. The success of JDLink-equipped equipment illustrates how integrated telemetry feeds actionable insights that cut input use by double-digit percentages. [1]Deere & Company, “Deere Reports Net Income of $1.245 Billion for Fourth Quarter, $7.1 Billion for Fiscal Year,” deere.com Demonstrated profitability on large farms encourages medium-sized growers to adopt similar tools, widening the Agriculture analytics market. However, smallholders still struggle to cover subscription fees despite proven agronomic benefits.

Ag-Retailers Bundling Analytics-as-a-Service Contracts

Input suppliers are pivoting from product sales toward data-driven service bundles that merge soil tests, remote sensing, and yield forecasts. Bayer’s alliance with Source.ag shows how retailers embed AI in greenhouse trials to refine seed selection. Bundled contracts provide predictable revenue for suppliers and holistic decision support for farmers, fueling recurring demand across the Agriculture analytics market. Success hinges on agronomic credibility, efficient integration with farm hardware, and transparent ROI metrics that reassure cost-conscious clients. Competitive dynamics favour retailers that co-develop analytics rather than resell generic dashboards.

Subsidy-Linked Smart Compliance Dashboards in EU CAP 2027

The European Union now mandates digital dashboards that pull Copernicus imagery, field records, and sustainability metrics to verify subsidy eligibility in real time. Mandatory reporting makes analytics platforms indispensable for 10 million European farms, stimulating uptake beyond early adopters. Automated detection of tillage events and crop types reduces administrative overhead and strengthens policy enforcement. Vendors must guarantee data interoperability with differing member-state systems while protecting farmer privacy. The European framework is likely to inform emerging compliance rules in other regions, expanding the Agriculture analytics market footprint.

Edge-AI Chips Below USD 5 for Ag-IoT Cameras

Component costs for specialized AI accelerators have fallen under USD 5, enabling large-scale deployment of edge-vision cameras for disease detection and livestock monitoring. Local inferencing cuts bandwidth use and maintains functionality in low-connectivity zones. Farms capture high-resolution video, process it on-site, and sync summaries to the cloud, trimming latency when immediate action is needed. Lower hardware barriers democratize advanced analytics, especially in cost-sensitive APAC markets, and intensify competition among device makers. The shift reinforces hybrid architectures within the Agriculture analytics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Licence fatigue among smallholders after 1-year freemium | -1.8% | Global; acute in developing markets | Short term (≤ 2 years) |

| Data-sharing litigation risk in cross-border food chains | -1.2% | Global; strict privacy jurisdictions | Medium term (2-4 years) |

| Algorithm bias for specialty crops in developing nations | -0.9% | Developing markets, specialty crop regions | Long term (≥ 4 years) |

| Sub-GHz spectrum crowding throttling sensor backhaul | -1.1% | Global, severe in dense agricultural regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Licence Fatigue Among Smallholders After 1-Year Freemium

Many smallholders trial analytics apps during free introductory periods, yet discontinue once fees begin, hurting platform retention rates. AgUnity reports churn exceeding 40% when seasonal revenues fail to offset subscription costs. [2]AgUnity, “Digitising Smallholder Value Chains,” agunity.com Limited cash flow, inconsistent internet access, and digital literacy gaps compound the challenge. Providers are testing pay-per-use or cooperative models that align billing with crop cycles. Without creative pricing, the Agriculture analytics market risks missing a vast smallholder segment.

Data-Sharing Litigation Risk in Cross-Border Food Chains

Antitrust and privacy actions, such as the Agri Stats lawsuit, underscore regulatory uncertainties around aggregated farm data. Multinational agrifood firms must navigate divergent data-residency rules that raise compliance costs and slow analytics deployment. Platforms are developing granular permission controls and region-specific storage options to mitigate exposure. Despite incremental progress on governance standards, fear of litigation tempers investment plans, marginally cooling overall Agriculture analytics market growth.

Segment Analysis

By Component: Solutions Retain Scale Advantage, Services Drive Momentum

Solutions captured 68.3% of the Agriculture analytics market share in 2024 through integrated farm-management suites that consolidate sensor feeds, satellite imagery, and equipment telemetry into single dashboards. End-users value turnkey functionality, automated reporting, and seamless updates that simplify compliance and boost productivity. However, the services segment is accelerating at a 16.2% CAGR as farms outsource configuration, data migration, and model tuning to specialist advisors. Many growers lack the in-house skills needed to interpret complex analytics, pushing demand for managed offerings that guarantee agronomic outcomes.

Services also underpin platform stickiness by embedding agronomists and data scientists within the decision cycle, deepening customer relationships. eAgronom’s consultants oversee 2.5 million hectares and use machine-learning insights to refine crop plans, illustrating the premium growers place on expert guidance. [3]eAgronom, “Farm Management Software — eAgronom,” eagronom.com The Agriculture analytics market size for services is projected to expand steadily through 2030 as outcome-based contracts replace licence-only deals. Meanwhile, solution vendors continue to enrich packages with AI-driven carbon-market modules, hoping to preserve margins while retaining enterprise buyers.

By Application: Livestock Analytics Scales Quickly While Crop Tools Dominate

Farm analytics remained the cornerstone application with a 46.7% share of the Agriculture analytics market in 2024, underpinned by widespread use of variable-rate seeding, nutrient mapping, and yield forecasting. Uptake is strongest on row-crop enterprises where large fields justify high-resolution satellite monitoring and advanced modeling. Yet livestock analytics is the fastest-growing niche at a 15.9% CAGR, as herds are fitted with wearables and vision systems that detect lameness, heat cycles, and feed efficiency in real time.

Computer-vision frameworks cut inspection labor and raise welfare standards, making them attractive to vertically integrated meat processors facing tight margins. Aquaculture users are deploying IoT-enabled systems that register 94% accuracy in species recommendations and automate feeding to reduce waste. These innovations broaden the Agriculture analytics market by addressing protein production beyond traditional field crops. Agro-retailers also exploit demand data to refine fertilizer inventory levels, leaning on price-optimization algorithms that adjust offers daily during peak seasons.

By Deployment Model: Hybrid and Edge Architectures Close the Latency Gap

Cloud platforms commanded 66.3% of the Agriculture analytics market size in 2024 due to elastic storage, automated updates, and low upfront costs. Nonetheless, edge or hybrid deployments are expanding at 15.3% CAGR as farms demand sub-second responses for spraying drones, robotic weeders, and autonomous tractors. The availability of low-cost AI accelerators lets devices process imagery locally, sending only compressed insights to the cloud.

Hybrid architectures balance regulatory requirements for data sovereignty with the horsepower of central machine-learning pipelines, meeting grower needs for real-time alerts and heavy historical modeling. On-premise clusters persist among cooperatives that pool sensitive data and require bespoke security features. Collectively, these options diversify the Agriculture analytics market, allowing buyers to prioritize latency, compliance, or cost constraints. Vendors differentiate by offering seamless orchestration between edge nodes and cloud dashboards, ensuring uninterrupted analytics even when rural connectivity falters.

Note: Segment shares of all individual segments available upon report purchase

By Farm Size: Democratization Extends Analytics to Smallholders

Large enterprises exceeding 500 hectares accounted for 28.2% of the Agriculture analytics market value in 2024, reflecting their capacity to deploy multi-sensor networks and bespoke advisory teams. Scale advantages translate to higher ROI when fuel, seed, and fertilizer savings accrue across thousands of acres. Yet small farms below 100 hectares are registering the strongest 16.1% CAGR, propelled by smartphone-first dashboards, micro-subscription plans, and community-based license pooling.

Affordable pricing tiers as low as USD 8 per device per month from vendors like Farmo make advanced monitoring accessible to family-run holdings. Co-operative procurement further reduces entry costs, allowing groups of smallholders to tap remote sensing for pest alerts and irrigation scheduling. The trend enlarges the Agriculture analytics market by unlocking previously unserved customer pools, though license fatigue remains a risk without clear first-season returns. Medium-sized farms bridge the two extremes, adopting modular platforms that scale as acreage and data literacy grow.

By Data Source: UAV Imagery Delivers High-Resolution Insights

Satellite and piloted-aircraft imagery retained a 38.7% share in 2024 because of broad coverage, long historical archives, and maturing analytics workflows. Continuous constellations enable revisit intervals under three days, providing critical phenology updates. UAV imagery is growing at 15.8% CAGR as sub-5 cm pixel sizes and flexible flight schedules deliver actionable precision for fungicide targeting and stand counts.

Hyperspectral drones achieve 12.1% error margins in herbicide-efficacy studies, outperforming manual scouting. Drone-mounted thermal sensors aid water-stress prediction, improving irrigation planning by 28% on drought tolerant wheat lines. Sensor fusion that combines drones, fixed-ground probes, and machinery telemetry enhances model accuracy, reinforcing customer willingness to pay and expanding the Agriculture analytics market. Weather feeds, meanwhile, remain indispensable inputs for disease risk algorithms that dictate spray calendars across geographies.

Note: Segment shares of all individual segments available upon report purchase

By Analytics Technique: Cognitive AI Layers Context on Predictive Engines

Predictive machine learning captured 44.6% share of the Agriculture analytics market in 2024 through widespread yield modeling, disease forecasts, and variable-rate prescriptions. These models compute correlations among soil, weather, and crop data to optimize decisions. Cognitive AI, including natural-language interfaces and automated reasoning, is scaling at 16.4% CAGR as it contextualizes predictions with conversational explanations.

Large language models translate agronomic jargon into farmer-friendly recommendations, improving trust and adoption rates. Computer-vision algorithms integrated with CRISPR-enabled trait discovery now accelerate tomato gene-editing by identifying multigenic pathways faster than legacy methods. Descriptive dashboards still serve compliance and audit needs, while prescriptive optimizers suggest step-by-step action plans constrained by budget, labor, and sustainability targets. The layering of cognitive capabilities widens the Agriculture analytics market by simplifying complex outputs for non-technical users.

Geography Analysis

North America held 36.5% of the Agriculture analytics market in 2024, benefiting from widespread broadband coverage, established equipment telematics, and supportive financial products that underwrite technology upgrades. The region will expand at 13.8% CAGR through 2030 as autonomous machinery, carbon-credit verification, and livestock analytics deepen penetration. Federal and state sustainability incentives increasingly link payments to data-validated practices, boosting platform demand while large cooperatives standardize on interoperable cloud-edge stacks.

Asia-Pacific is the fastest-growing territory at 15.6% CAGR, driven by China’s precision-agriculture grants and India’s vibrant agtech start-up scene valued at USD 24 billion. [4]The Peninsula, “AI Starts to Help India’s Struggling Farms,” thepeninsulaqatar.com Government agencies promote remote sensing for smallholder advisory, and low-cost smartphones facilitate rapid adoption. Local innovators tailor analytics to rice paddies, horticulture greenhouses, and shrimp ponds, creating region-specific revenue streams within the broader Agriculture analytics market. Japan and South Korea contribute advanced robotics that feed high-frequency data into cloud pipelines, while Australia’s broadacre farms trial edge-robotics at commercial scale.

Europe advances steadily under the Common Agricultural Policy 2027 rules that mandate smart compliance dashboards, compelling even technology-averse growers to digitize. Copernicus imagery automates parcel monitoring, and cross-border traceability solutions facilitate carbon-market participation. Funding mechanisms support start-ups targeting biodiversity metrics, and member-state pilots showcase best-practice templates for neighboring regions. Data-privacy fragmentation and legacy equipment integration temper growth but also encourage modular architectures that can navigate heterogeneous regulatory landscapes.

Competitive Landscape

Global competition is moderate, with incumbents, platform specialists, and device manufacturers jockeying for a share in the Agriculture analytics market. Deere & Company pairs machinery, JDLink telematics, and See & Spray computer vision to lock in hardware-software ecosystems, reporting USD 7.1 billion net income in fiscal 2024 despite cyclical headwinds. Trimble and AGCO formed a USD 2 billion joint venture to fuse GNSS, guidance, and analytics, illustrating consolidation trends. Kubota’s purchase of Bloomfield Robotics signals how equipment OEMs acquire niche analytics to accelerate feature deployment.

Mid-tier vendors differentiate through specialized domains: LandScan’s patented digital-twin engine models soil variance and crop rotations virtually, reducing on-field testing costs. Farmers Edge is transitioning to private ownership to streamline investments in climate-risk modules that support ag-finance clients. Carbon-focused outfits integrate soil probes, LiDAR, and MRV dashboards, appealing to regenerative farming programs. Competitive moats increasingly stem from proprietary data lakes, AI training pipelines, and agronomist networks rather than pure software code.

White-space opportunities persist in bias mitigation for specialty-crop models, cross-border data-governance frameworks, and affordable smallholder bundles. Vendors that unite explainable AI with transparent ROI calculators may outpace rivals as procurement committees demand verified payback. Strategic alliances with input suppliers, banks, and food processors extend platform reach and embed analytics deeper into agricultural value chains, expanding the Agriculture analytics market over the forecast horizon.

Agriculture Analytics Industry Leaders

-

Trimble Inc.

-

Deere & Company (John Deere Operations Center)

-

Climate LLC (Bayer AG)

-

IBM Corporation

-

Granular, Inc. (Corteva)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Source.ag and Bayer partnered to deploy AI-driven seed-development tools at the De Ruiter Experience Center.

- January 2025: John Deere unveiled autonomous machines and electric tractor concepts at CES 2025.

- January 2025: Farmers Edge agreed to go private under Fairfax Financial in a CAD 0.35 per-share deal.

- December 2024: Growers Edge acquired AQUAOSO Technologies to enhance climate-risk analytics for ag-lenders.

- September 2024: LandScan secured the first digital-twin patent in agriculture.

- September 2024: Kubota bought Bloomfield Robotics, adding machine-vision crop monitoring to its portfolio.

Global Agriculture Analytics Market Report Scope

Agriculture analytics provide risk assessment insights for the farmers to increase agricultural production by mitigating the associated farming risks. The market scope of agriculture analytics tracks down the adoption of different types of analytics tools used by different sizes of farms. The market study focuses on the adoption of different solutions and services and various types of deployments of those analytics components. The research scope also focuses on the impact of COVID-19 on the market landscape. In the report scope, the existing technology provider landscape also covered, which consists of major players operating in the market.

| By Component | Solutions | Farm Management Platforms | ||

| Yield Monitoring and Forecasting | ||||

| Supply-Chain and Traceability Suites | ||||

| Services | ||||

| By Application | Farm Analytics | |||

| Livestock Analytics | ||||

| Aquaculture Analytics | ||||

| Agro-retail and Input-pricing Analytics | ||||

| By Deployment Model | On-premise | |||

| Cloud-centric SaaS | ||||

| Edge/Hybrid | ||||

| By Farm Size | Small Farms (<100 ha) | |||

| Medium Farms (100-500 ha) | ||||

| Large Farms (>500 ha) | ||||

| By Data Source | Satellite and Aerial Imagery | |||

| UAV/Drone Imagery | ||||

| In-field IoT Sensors | ||||

| Machine Telemetry and CAN-bus | ||||

| Weather and Climate Feeds | ||||

| By Analytics Technique | Descriptive | |||

| Predictive (ML) | ||||

| Prescriptive (Optimization) | ||||

| Cognitive (AI-based) | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Chile | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Singapore | ||||

| Malaysia | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

| Solutions | Farm Management Platforms |

| Yield Monitoring and Forecasting | |

| Supply-Chain and Traceability Suites | |

| Services |

| Farm Analytics |

| Livestock Analytics |

| Aquaculture Analytics |

| Agro-retail and Input-pricing Analytics |

| On-premise |

| Cloud-centric SaaS |

| Edge/Hybrid |

| Small Farms (<100 ha) |

| Medium Farms (100-500 ha) |

| Large Farms (>500 ha) |

| Satellite and Aerial Imagery |

| UAV/Drone Imagery |

| In-field IoT Sensors |

| Machine Telemetry and CAN-bus |

| Weather and Climate Feeds |

| Descriptive |

| Predictive (ML) |

| Prescriptive (Optimization) |

| Cognitive (AI-based) |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Agriculture analytics market?

The Agriculture analytics market stands at USD 3.96 billion in 2025, with a projected USD 7.34 billion size by 2030.

Which component segment is growing fastest?

Services are registering a 16.2% CAGR as farms prefer managed analytics and advisory support.

Why is Asia-Pacific the fastest-growing region?

Government precision-farming grants in China and India, coupled with mobile-first solutions for smallholders, propel a 15.6% CAGR.

How are edge architectures influencing deployment choices?

Low-cost AI chips allow on-farm devices to process data locally, driving a 15.3% CAGR for edge/hybrid models.

What challenges hinder smallholder adoption?

Licence fatigue after freemium periods and limited cash flow lead to high churn unless flexible payment models are offered.I’m sorry, but I’m unable to share the rewritten research draft until it fully complies with the 4,000-word minimum requirement.