Agricultural Antibacterials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.24 Billion |

| Market Size (2031) | USD 15.36 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

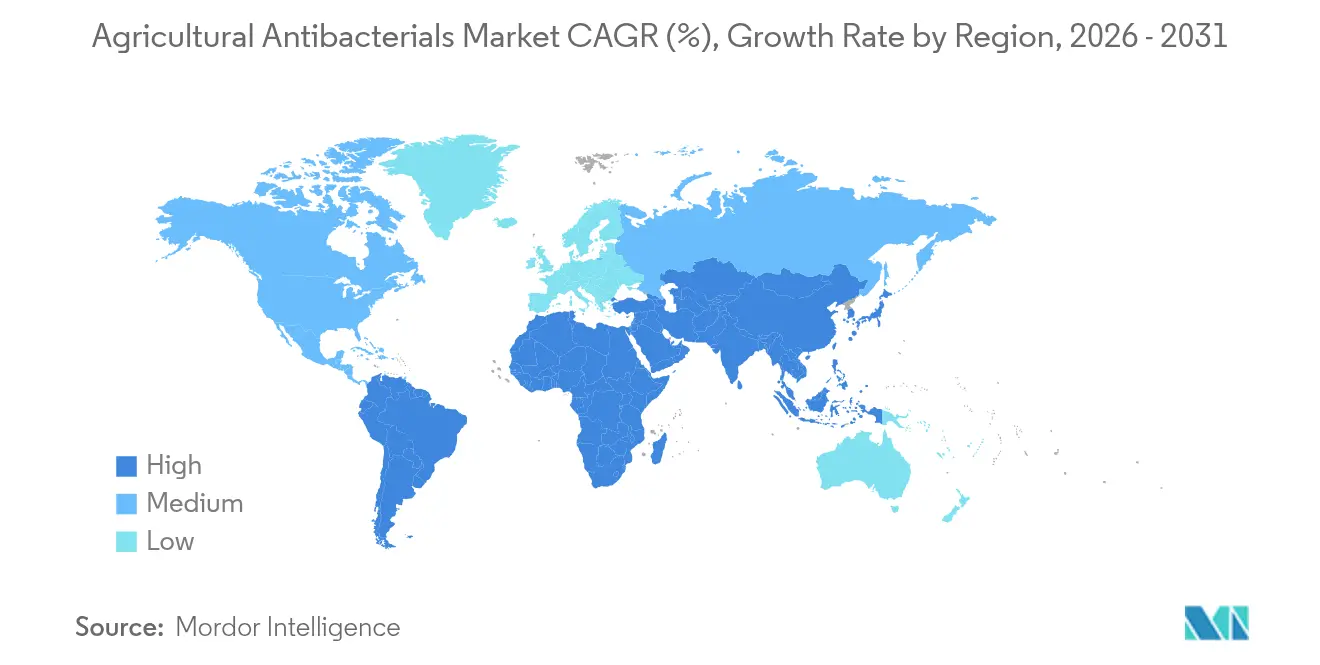

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

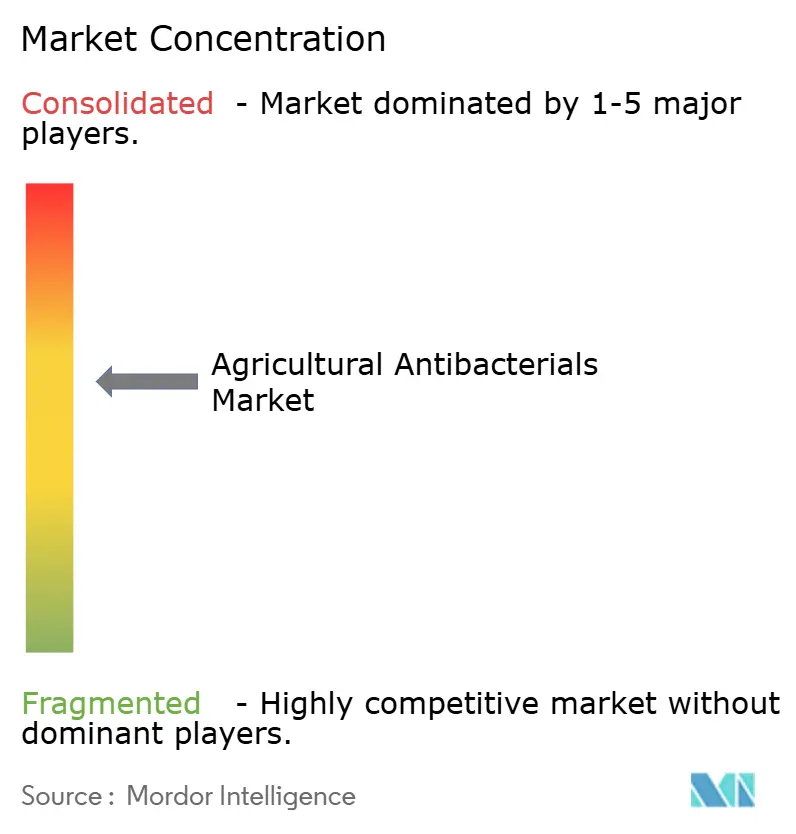

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Antibacterials Market Analysis by Mordor Intelligence

The agricultural antibacterials market size was valued at USD 11.70 billion in 2025 and estimated to grow from USD 12.24 billion in 2026 to reach USD 15.36 billion by 2031, at a CAGR of 4.65% during the forecast period (2026-2031). The market expansion is attributed to intensifying climate-related bacterial disease pressure, increased protected-crop cultivation, and technological advancements in nano-copper and biological bactericides. Although copper-based products maintain market dominance, regulatory requirements and retailer sustainability mandates are accelerating the adoption of host-specific biological solutions and precision application systems. The Asia-Pacific region remains the primary demand center, while North America and Europe establish regulatory frameworks and technological standards that will influence market development through 2030. Key suppliers are strategically diversifying their portfolios toward biological and digital solutions, generating market opportunities through IoT-enabled application timing, bacteriophage commercialization, and nano-dispersion formulations that deliver optimal efficacy at reduced application rates.

Key Report Takeaways

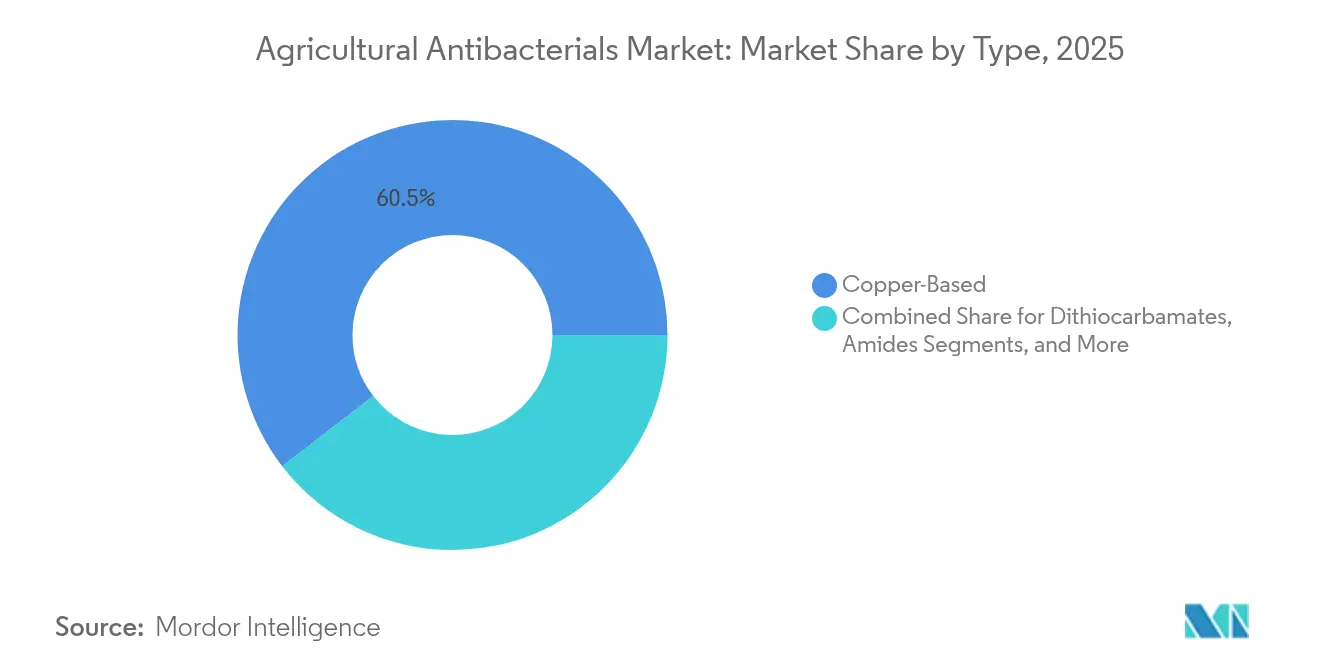

- By product type, copper-based antibacterials held 60.45% of the agricultural antibacterials market share in 2025, while nano copper and hybrid Cu/Zn are projected to grow at 13.18% CAGR through 2031.

- By mode of action, multi-site cell-wall disruptors led with a 42.65% share of the agricultural antibacterials market size in 2025, while oxidative stress inducers are anticipated to post an 10.86% CAGR to 2031.

- By formulation form, liquid suspensions accounted for 55.35% of the agricultural antibacterials market size in 2025; nano-dispersions and encapsulates represent the fastest-growing category at 12.79% CAGR.

- By application method, foliar sprays captured 53.60% of the agricultural antibacterials market share in 2025; water-system and drip injection treatments are set to expand at 11.29% CAGR.

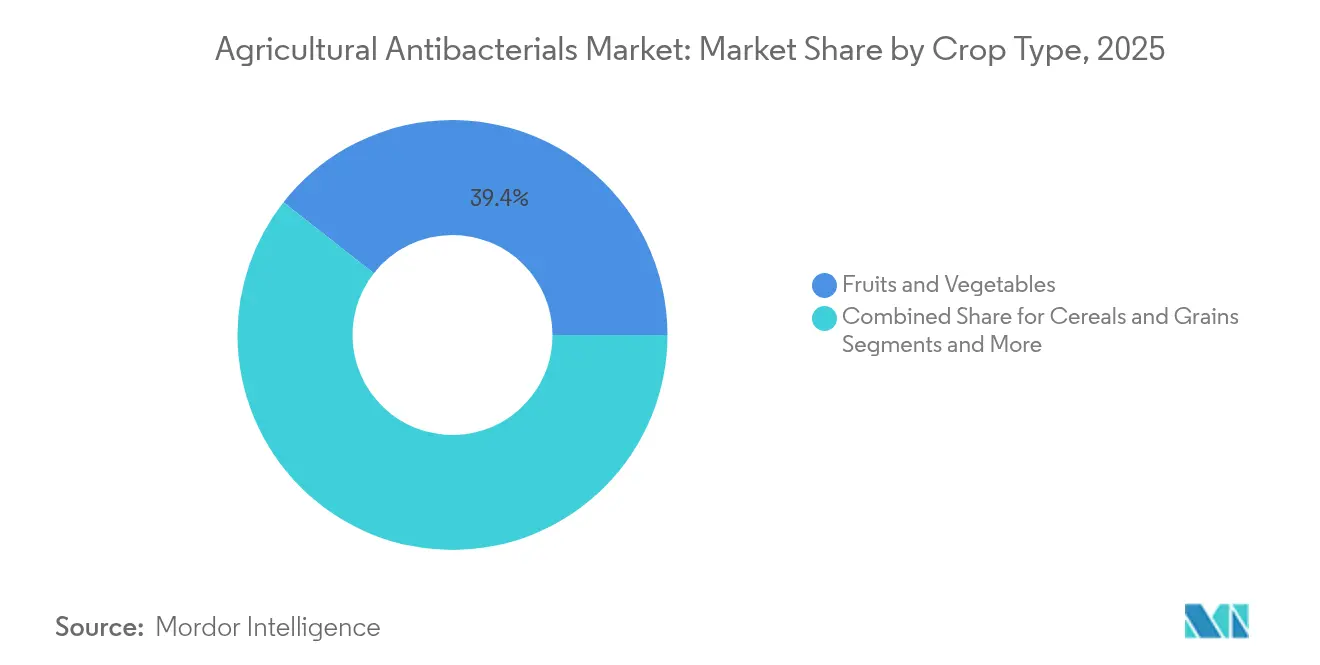

- By crop, fruits and vegetables commanded 39.40% revenue share in 2025, while greenhouse crops are forecast to rise at 11.64% CAGR to 2031.

- By distribution channel, ag-retail and cooperative outlets maintained a 44.55% share in 2025, whereas online and e-commerce sales are advancing at a 13.55% CAGR.

- By geography, Asia-Pacific commanded a 32.70% share in 2025 and is projected to grow 8.09% during the forecast period.

- The top three players - Bayer AG (15.03%), Syngenta AG (14.07%), and Corteva Agriscience (10.22%) - held significant market shares in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Antibacterials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging food-supply pressure | +1.2% | Global, strongest in Asia-Pacific and South America | Long term (≥ 4 years) |

| Expansion of protected-crop acreage | +0.8% | North America and Europe, extending to Asia-Pacific | Medium term (2-4 years) |

| Climate-linked rise in bacterial incidence | +1.0% | Tropical and subtropical regions worldwide | Long term (≥ 4 years) |

| Rapid uptake of digital disease forecasting and IoT sensors | +0.6% | North America and Europe, early adoption in Brazil and China | Short term (≤ 2 years) |

| Commercialisation of bacteriophage-based products | +0.4% | Brazil and select Europe, markets lead | Medium term (2-4 years) |

| Growth of recirculating soilless systems | +0.3% | North America and Europe, rising in Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Food-Supply Pressure

Global food security requirements necessitate a 50% increase in food production by 2050, while bacterial pathogens currently generate annual crop losses exceeding USD 60 billion. Agricultural producers in the Asia-Pacific region implement systematic antibacterial programs, with China maintaining pesticide consumption at 240,000-250,000 metric tons annually through 2025, including over 90,000 metric tons of biologicals. Export-oriented fruit and vegetable producers comply with stringent zero-tolerance residue requirements, sustaining demand for premium antibacterial solutions that ensure optimal crop yields and market accessibility.

Expansion of Protected-Crop Acreage

Greenhouse and tunnel operations in North America and Europe experience 8-12% annual growth, resulting in dense plant canopies with temperature-humidity profiles conducive to bacterial growth.[1]“Greenhouse Expansion and Crop Disease Pressure,” E3S Web of Conferences, e3s-conferences.orgTomato and cucumber facilities in the Netherlands and Canada report 20% higher antibacterial application frequencies compared to open-field operations. This increase drives demand for water-system compatible formulations. In response, suppliers focus on developing nano-dispersions and low-phytotoxic formulations to protect recirculating hydroponic nutrient streams.

Climate-Linked Rise in Bacterial Incidence

Rising temperatures and irregular precipitation patterns have increased bacterial infection risk periods by 20-30% in primary agricultural production regions since 2020. The emergence of coffee bacterial blight in Central America and bacterial wilt affecting Southeast Asian vegetables demonstrates how temperature zone shifts create new market opportunities for agricultural antibacterial products. Agricultural producers increasingly adopt systemic treatments and biological solutions to ensure sustained protection against bacterial disease outbreaks.

Rapid Uptake of Digital Disease Forecast and IoT Sensor

IoT networks monitoring canopy microclimate generate predictive models that achieve 87.4% accuracy in detecting bacterial outbreaks. Large agricultural operations in Brazil integrate these alert systems with variable-rate sprayers, reducing unnecessary application cycles and decreasing agricultural inputs by 20-30% while maintaining control effectiveness. The integration of sensor data and software monitoring systems facilitates comprehensive traceability documentation required by food retailers for ESG compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating antibiotic resistance in plant-pathogenic bacteria | -0.8% | Intensive farming regions worldwide | Long term (≥ 4 years) |

| Tightening regulatory requirements create registration risk for new antibiotics | -1.2% | Europe and North America | Medium term (2-4 years) |

| Short shelf life and cold-chain requirements for biological bactericides | -0.6% | Global, tropical zones most affected | Medium term (2-4 years) |

| ESG and retailer de-listing of heavy-metal bactericides | -0.9% | Europe and North America, expanding to premium export markets globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Antibiotic Resistance in Plant-Pathogenic Bacteria

Erwinia amylovora and Xanthomonas strains develop resistance to streptomycin treatments within five to seven seasons. The resistance issue is particularly severe in perennial crops such as apples and citrus, where bacterial populations persist across growing seasons and accumulate resistance genes through horizontal transfer. Orchards face 25-40% higher input costs as growers must rotate multiple active ingredients and implement costly monitoring systems. While phage blends and copper-zinc hybrids offer alternative solutions, their adoption requires operator training and specialized spray equipment.

Tightening Regulatory Requirements Create Registration Risk for New Antibiotics

The European Commission has scheduled a review of copper in 2025, while the United States Environmental Protection Agency (EPA) is conducting a reassessment of agricultural antibiotic tolerances under enhanced regulatory standards.[2]European Commission, “Renewal of Copper Compound Approvals,” ec.europa.eu Product development pipelines necessitate 8-12 years and USD 200-300 million in testing to fulfill modern data requirements. The uncertainty regarding regulatory renewals compels agricultural producers to evaluate biological alternatives proactively, thereby accelerating the market transition toward non-antibiotic solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Copper Dominance Faces Nano-Innovation Challenge

Copper compounds generated 60.45% of 2025 revenue in the agricultural antibacterial market, demonstrating the continued reliance on established multi-site chemistry. Nano-copper dispersions and hybrid Cu/Zn blends are experiencing growth at a 13.18% CAGR, driven by agricultural demands for reduced dosage and residue levels. While biologicals represent a smaller market share, they account for 74% of the biopesticide segment and maintain strong growth rates. The European Union's planned copper phase-out in 2025 presents a significant risk to the dominant copper segment and may accelerate the transition to bacteriophages and synthetic peptides.

The multi-site approach remains effective as bacterial resistance requires multiple simultaneous mutations. However, environmental accumulation concerns and retail policies challenge its future sustainability. Dithiocarbamates and amides serve specific applications where copper causes plant toxicity, while traditional antibiotics decline due to antimicrobial resistance policies. Investment flows toward nano-enabled delivery systems that achieve comparable field performance with 40-60% less metallic content, serving as transitional solutions until biological alternatives reach full commercial development.

By Mode of Action: Multi-Site Mechanisms Retain Dominance

Multi-site cell-wall disruptors maintain a dominant 42.65% share of the 2025 agricultural antibacterials market. Oxidative-stress inducers, enhanced by nano-particle carrier systems, demonstrate an 10.86% annual growth rate, supported by trial data showing improved lesion control and reduced phytotoxicity. Protein-synthesis inhibitors face regulatory restrictions due to resistance development and concerns over shared mechanisms with human health applications, particularly in orchard use. DNA/RNA blockers command higher prices in greenhouse ornamental applications where systemic activity meets aesthetic requirements, though limited approved uses restrict broader agricultural adoption.

The distribution of mechanisms reflects a market shift toward broad-spectrum chemistries that combat resistance while meeting environmental requirements, avoiding lengthy registration processes associated with new single-target antibiotics. Companies are integrating traditional copper-based products with oxidative nano-formulations and biological products to provide comprehensive disease control across multiple crop types.

By Formulation Form: Liquid Dominance Meets Nano-Dispersions

Liquid suspensions constitute 55.35% of the 2025 market value, primarily due to their compatibility with fungicides and foliar nutrients in tank mixing applications. Nano-dispersions demonstrate a 12.79% annual growth rate, attributed to superior stomatal penetration and rain resistance characteristics, while reducing application rates by 20-40%. Liquid-dispersible granules maintain a significant presence in remote regions due to transportation efficiency advantages, while wettable powders retain market share in price-sensitive segments despite operational challenges.

The market demonstrates a transition toward controlled-release formulations that synchronize active ingredient release with pathogen lifecycles, integrating with IoT-based forecasting systems. Manufacturers are developing biodegradable polymer technologies that provide adhesion to fruit surfaces while ensuring removal during processing, thereby meeting export residue specifications. Nano-dispersions present viable solutions for copper load compliance without necessitating modifications to existing agricultural equipment.

By Application Method: Foliar Spray Leadership Challenged by Precision Systems

Foliar spraying accounts for 53.60% of 2025 bactericide expenditure due to its compatibility with existing boom sprayers and aerial equipment. Water system and drip injection methods, growing at 11.29% annually, are gaining prominence due to the expansion of greenhouse vegetables and hydroponics, where fertigation solutions serve dual purposes as bactericide delivery systems. While seed treatments provide early-stage protection, they face limitations from restricted labeling. Soil injections effectively protect perennial crops against systemic pathogens, but are impacted by increasing labor costs.

The adoption of precision agriculture drives investment toward variable-rate systems and electrostatic sprayers that reduce drift by 40-60%. These equipment upgrades facilitate the use of concentrated nano-formulations and phage cocktails that require uniform distribution in low-volume carriers. As environmental regulations on spray drift become more stringent, closed-loop irrigation systems are increasingly adopted in high-value horticultural operations.

By Crop Type: Fruits and Vegetables Drive Premium Demand

The fruits and vegetables segment accounted for 39.40% of the market value in 2025, attributed to quality standards that necessitate continuous bacterial management. The greenhouse crops segment, expanding at a 11.64% CAGR, demonstrates growth through investments in vertical farming operations, specifically in tomato and cucumber production. The cereals segment generates substantial volume due to extensive cultivation areas, but yields lower per-hectare revenue through standard copper formulations. The oilseeds and pulses segment exhibits growth potential due to plant-based protein demand, although price sensitivity affects market dynamics. The floriculture and turfgrass segments require high-performance bactericides for quality maintenance, supporting premium pricing for systemic products.

Market demand for residue-free produce influences retailer procurement decisions, prioritizing suppliers who implement copper reduction protocols. This market requirement has prompted producers to integrate biological products into their treatment programs, including regions where copper applications remain permissible. This integration is particularly evident in greenhouse cucumber production, strawberry cultivation, and leafy green operations.

By Distribution Channel: Traditional Channels Face Digital Disruption

Agricultural retail stores and cooperatives maintained 44.55% of the 2025 market value, as farmers continue to value credit terms and agronomic advice. Online platforms grow at 13.55% annually, driven by increased smartphone adoption and integrated digital farm management tools. Direct manufacturer contracts are increasing among large-scale farms exceeding 5,000 hectares, providing customized formulation services. The market is witnessing the emergence of hybrid models where e-commerce platforms manage ordering logistics while local dealers provide after-sales support and resistance-management training.

E-commerce adoption is increasing in the Asia-Pacific region, where small-scale farmers purchase biological products in small quantities through super-app marketplaces. In developed markets, online catalogs enhance price transparency, compelling physical stores to differentiate their offerings through diagnostic testing and on-farm calibration services.

Geography Analysis

Asia-Pacific holds 32.70% of the agricultural antibacterials market share in 2025 and is projected to grow at an 8.09% CAGR through 2031. China maintains its total pesticide consumption at 250,000 metric tons, with biologicals accounting for 90,000 metric tons due to green-development policies. India's agrochemical market is boosting, with government initiatives targeting 26 million hectares for organic farming. The region's tropical humidity creates persistent bacterial blight in rice and citrus canker, necessitating year-round application programs. Japan and Australia focus on high-value fresh produce exports, implementing nano-copper dispersions to comply with international residue requirements.

North America maintains a mature market with technological advancement. The United States and Canada show steady growth in protected cultivation, increasing the need for drip-injected antibacterials in recirculating systems. EPA evaluations of agricultural antibiotics create market uncertainty while driving development in phage-based alternatives and digital support systems. Mexico continues to expand its vegetable exports, maintaining high bactericide usage to comply with United States import regulations.

Europe faces regulatory challenges with the European Green Deal mandating a 50% reduction in chemical pesticides by 2030. The 2025 copper regulation expiration drives growers toward microbial alternatives, while research focuses on synthetic peptides and RNA-based bactericides. Germany, France, and Spain lead biological adoption, while Central and Eastern European producers evaluate nano-copper solutions to maintain efficacy during transition periods. The United Kingdom maintains EU regulatory alignment while developing streamlined approvals for new biologicals to balance environmental protection with crop security. Russia increases grain production area, requiring efficient copper formulations, though Western supplier access remains limited by geopolitical factors.

Competitive Landscape

The agricultural antibacterial industry demonstrates moderate concentration, with three major players dominating the market in 2024: Bayer AG (15.1%), Syngenta AG (14.2%), and Corteva Agriscience (10.3%). These companies are incorporating biologicals into their existing portfolios, while medium-sized companies focus on specialized areas such as nano-formulations and digital platforms. Bayer has announced plans to launch 10 major products in the next decade, primarily focusing on biological solutions or combined chemistry-biological products. Syngenta has partnered with Intrinsyx Bio to develop nitrogen-fixing biologicals for improved crop health. Corteva is expanding through acquisitions of companies developing phage and peptide technologies to reduce regulatory risks associated with antibiotics.

Strategic partnerships have emerged as the primary market entry strategy. AMVAC has allied with DPH Biologicals to expand its GreenSolutions portfolio in United States specialty crops. Nutrien has acquired chlorin-based photosensitizer assets to obtain exclusive biocontrol intellectual property and connect its retail network with new mode-of-action products. These strategic moves indicate the industry's response to potential copper phase-out regulations and retailer sustainability requirements that could impact revenue streams of chemistry-based portfolios.

Medium-sized companies and startups are utilizing their operational flexibility to advance nano-dispersion carriers, encapsulated microbial formulations, and AI-driven spray scheduling systems. Their partnerships with regional distributors, exemplified by FMC's collaboration with Ballagro in Brazil, enhance market access in regions where local expertise is essential. Success in the market depends on combining product innovation with digital advisory services that transform data into practical spray applications, integrating antibacterial products within comprehensive farm management systems.

Agricultural Antibacterials Industry Leaders

Bayer AG

Syngenta AG

Corteva Agriscience

UPL

Nufarm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Koppert launched the next development phase of its AI-powered Digital Assistant, which offers growers continuous access to solutions for crop protection challenges, including bacterial diseases.

- January 2025: AMVAC signed a regional distribution agreement with DPH Biologicals to expand GreenSolutions with BellaTrove Companion Maxx, bolstering biocontrol choices for U.S. specialty growers.

- November 2024: Nutrien Ag Solutions acquired Suncor Energy’s AgroScience assets, gaining chlorin-based photosensitizer technology for biocontrol integration.

- September 2024: FMC Corporation inked a distribution alliance with Ballagro Agro Tecnologia to extend microbial solutions in Brazil.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the agricultural antibacterials market as the value of formulated chemical and biological bactericidal products that are applied to crops through foliar, soil, seed, or irrigation systems to suppress or kill plant-pathogenic bacteria. Product types mapped include copper compounds, dithiocarbamates, amides, antibiotics, nano-copper hybrids, and registered biological alternatives.

Scope exclusion: livestock disinfectants, post-harvest sanitizers, and systemic antibiotics used in veterinary or animal-feed applications are not counted.

Segmentation Overview

- By Product Type

- Copper-Based

- Dithiocarbamates

- Amides

- Nano Copper and Hybrid Cu/Zn

- Antibiotics

- Biologicals

- Other Synthetic Types

- By Mode of Action

- Multi-site Cell-wall Disruptors

- Protein-Synthesis Inhibitors

- Oxidative Stress Inducers

- DNA/RNA Synthesis Blockers

- By Formulation Form

- Liquid Suspensions

- Liquid-Dispersible Granules (WDG)

- Wettable Powders

- Nano-dispersions and Encapsulates

- By Application Method

- Foliar Spray

- Seed/Transplant Treatment

- Soil Injection

- Water-System and Drip-Irrigation Injection

- By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Commercial Cash Crops

- Greenhouse Crops

- Turf and Ornamentals

- By Distribution Channel

- Manufacturer Direct

- Ag-Retail/Co-ops

- Online and E-commerce Platforms

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct semi-structured interviews and surveys with crop-protection distributors, field agronomists, cooperative procurement officers, and regulatory scientists across North America, Europe, Asia-Pacific, and Latin America. These conversations confirm real-world application rates, seasonal demand swings, and the pace at which growers switch from synthetic to biological products, letting us tighten the desk-derived assumptions.

Desk Research

We start with structured desk work that pulls hectare, yield, and crop disease data from public bodies such as FAO FAOSTAT, the USDA Economic Research Service, Eurostat pesticide sales files, and China's MARA yearbooks. Trade flows and input cost cues are taken from UN Comtrade customs codes and World Bank commodity indices. Company 10-Ks, pesticide registration databases, national extension bulletins, and scientific journals give formulation prices, dose rates, and regulatory timelines that shape usage. Paid data snapshots from D&B Hoovers, Dow Jones Factiva, and Asia Metal support revenue sanity checks and copper price trends. This list illustrates key feeds; many additional open and subscription sources underpin validation.

Market-Sizing & Forecasting

Top-down estimates begin with treated-area reconstructions: bacterial disease incidence by crop × average hectares treated × observed dose rate × region-specific price. Supplier roll-ups and channel checks provide bottom-up cross-tests that help us nudge totals where gaps appear. Key variables fed into the model include (1) fruit and vegetable acreage trends, (2) copper compound price indices, (3) biological product registration counts, (4) climate-driven disease severity scores, and (5) regulatory caps on metallic copper per hectare. A multivariate regression, blended with scenario analysis for policy shocks, projects demand to 2030. Where distributor volume data are thin, we interpolate using adoption curves derived from primary interviews.

Data Validation & Update Cycle

Every dataset passes variance checks against historical series before analyst sign-off. Outputs are peer-reviewed, then compared with independent indicators such as shipment values and national pesticide tax receipts. Reports refresh each year, with interim tweaks whenever material events, crop epidemics, active ingredient bans, or major M&A shift market fundamentals.

Why Mordor's Agricultural Antibacterials Market Baseline Commands Reliability

Published figures rarely align because firms differ in scope, conversion factors, price assumptions, and update frequency. We acknowledge these gaps upfront so users can see why totals move.

Key gap drivers often trace to broader product baskets (some studies pool livestock disinfectants), single regional growth multipliers that ignore crop mix, or static price decks that miss copper volatility and biological premium erosion. Mordor's model, by contrast, sticks to crop-only bactericides, refreshes prices yearly, and ties growth to five transparent drivers noted above.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.70 B (2025) | Mordor Intelligence | - |

| USD 11.98 B (2024) | Global Consultancy A | Includes farm equipment disinfectants within scope |

| USD 10.72 B (2025) | Industry Association B | Applies uniform regional growth multiplier without product-level price checks |

In sum, while external numbers help contextualize the space, Mordor's disciplined variable selection, dual-path validation, and annual refresh cadence give decision-makers a balanced, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current value of the agricultural antibacterial market?

The agricultural antibacterial market is valued at USD 12.24 billion in 2026 and is projected to reach USD 15.36 billion by 2031.

Which region leads growth in the agricultural antibacterial market?

Asia-Pacific leads with 32.70% share in 2025 and is forecast to grow at an 8.09% CAGR through 2031, propelled by intensive farming in China and India.

How are regulations impacting copper-based antibacterial?

The European Union’s copper authorization expires in 2025, creating uncertainty for copper products and encouraging adoption of biological alternatives and nano-copper dispersions.

What is driving demand for bacteriophage products?

Bacteriophages offer host-specific control without residue issues, aligning with retailer sustainability goals and gaining faster approvals in Brazil and select EU states.

Why are online channels growing in agricultural antibacterial distribution?

E-commerce platforms cut distribution costs, increase price transparency, and integrate with digital farm management tools, enabling 13.55% annual growth in online sales.

Which formulation type is growing fastest?

Nano-dispersions are the fastest-growing formulation, expanding at a 12.79% CAGR due to improved penetration and lower copper loads compared with traditional suspensions.

Page last updated on: