Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

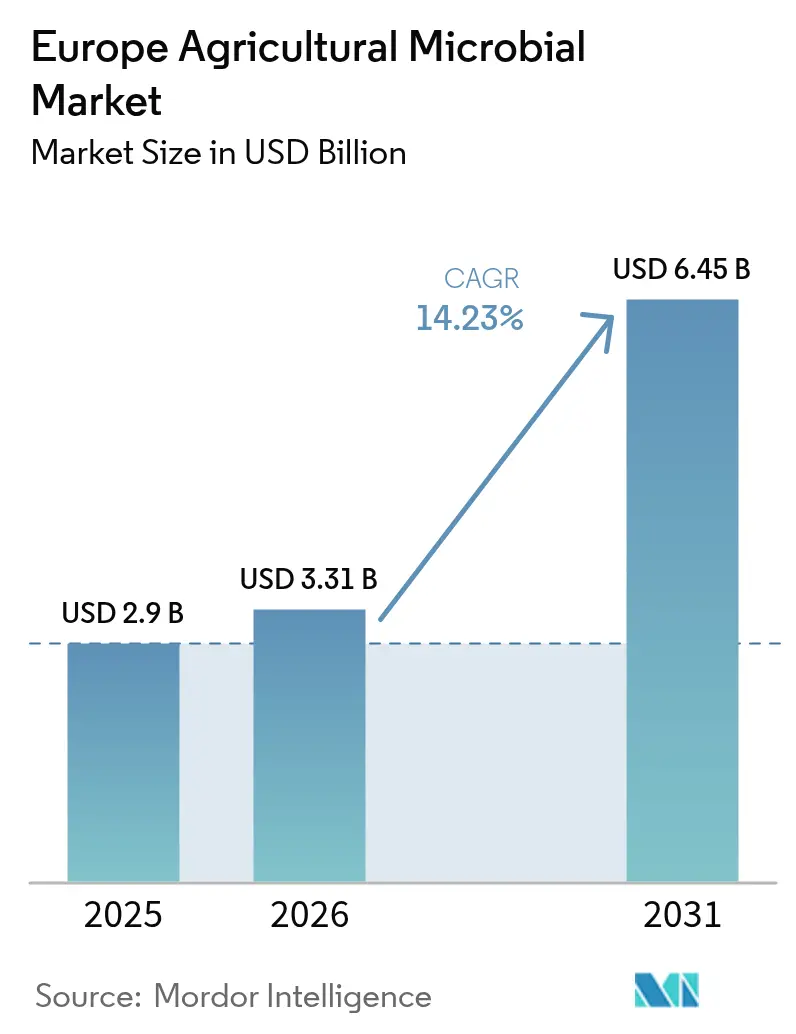

| Base Year Market Size (2025) | USD 2.90 Billion |

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 6.45 Billion |

| Growth Rate (2026 - 2031) | 14.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Agricultural Microbial Market Analysis by Mordor Intelligence

The Europe agricultural microbial market size was valued at USD 2.90 billion in 2025 and estimated to grow from USD 3.31 billion in 2026 to reach USD 6.45 billion by 2031, at a CAGR of 14.23% during the forecast period (2026-2031). Structural demand is shifting toward biological inputs as the European Union’s Farm-to-Fork mandate halves chemical pesticide use, and carbon-credit programs reward nitrogen-fixing inoculants. The Europe agricultural microbial market benefits from retailer zero-residue specifications that raise switching incentives, precision-application technologies that improve field consistency, and post-Brexit regulatory divergence that accelerates product launches in the United Kingdom. Competitive strategies center on vertical integration and AI-guided strain selection to raise efficacy, while white-space opportunities lie in Eastern European cold-chain logistics and liquid formulations that simplify on-farm handling. Headline risks include lengthy Europe Union registrations, high upfront costs for smallholders, and fragmented extension services that slow knowledge transfer.

Key Report Takeaways

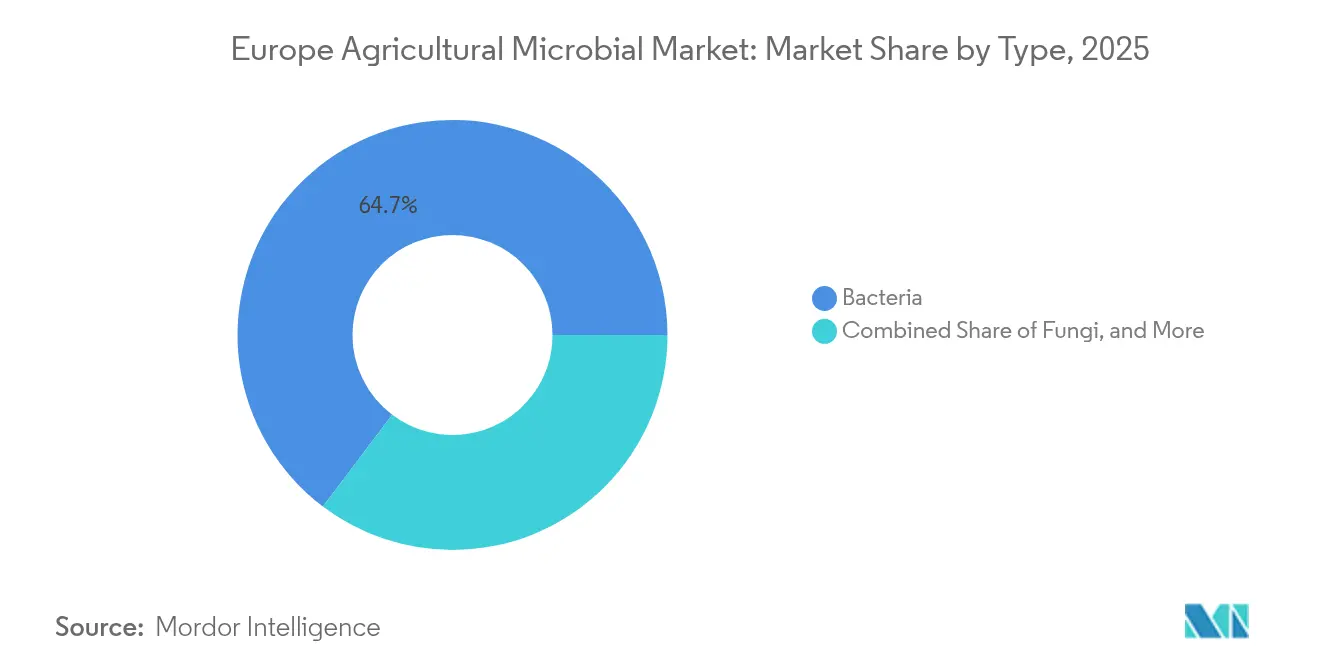

- By type, bacteria held 64.70% of the Europe agricultural microbial market size in 2025, while fungi microorganisms are forecast to expand at a 15.12% CAGR to 2031.

- By application, fruits and vegetables led with 36.50% revenue share in 2025, while pulses and oilseeds are projected to grow at a 14.67% CAGR through 2031.

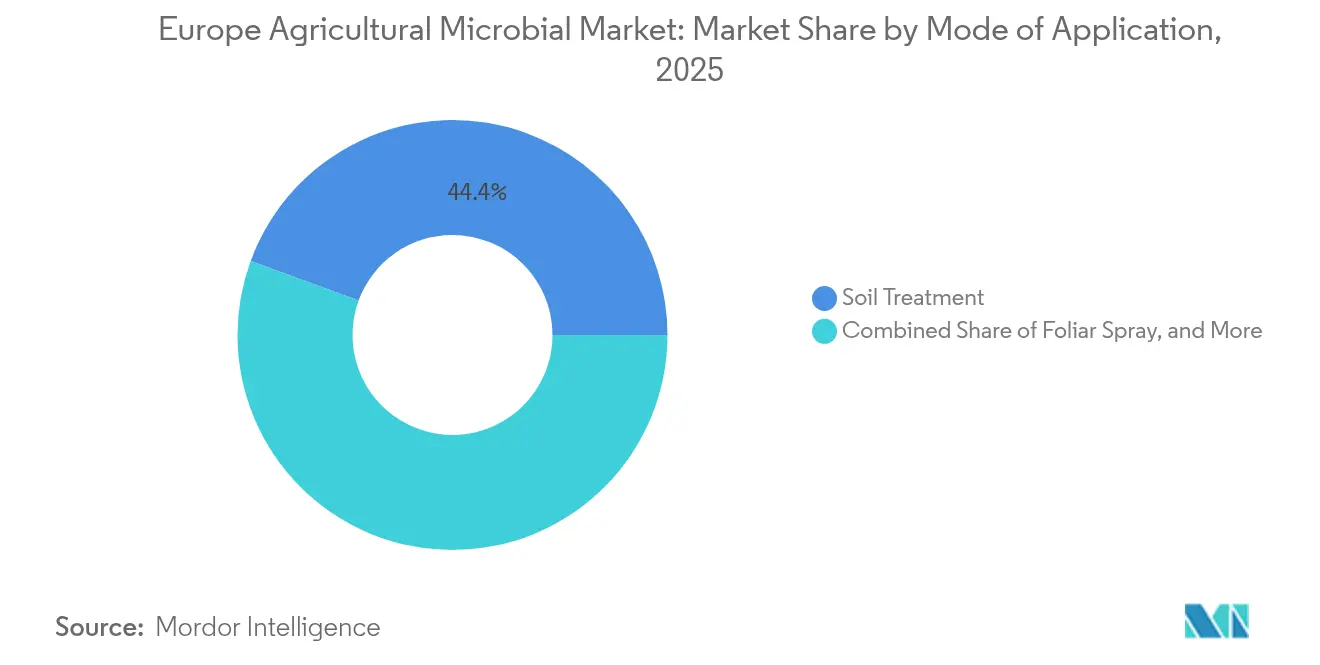

- By mode of application, soil treatment accounted for 44.40% of the Europe agricultural microbial market size in 2025, whereas foliar spray adoption is projected to rise at a 14.32% CAGR to 2031.

- By geography, France is projected to account for 20.85% of the Europe agricultural microbial market in 2025, while Poland is projected to grow at an approximate 17.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Agricultural Microbial Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of organic and regenerative farming | +3.2% | Germany, France, Spain, Italy, spillover to the rest of Europe | Medium term (2-4 years) |

| European Union Farm-to-Fork pesticide-reduction mandates | +4.1% | Pan-European, strongest in Germany, France, Spain, Italy | Short term (≤ 2 years) |

| Consumer demand for residue-free produce | +2.8% | Germany, France, the United Kingdom, and Spain | Medium term (2-4 years) |

| Expansion of European Union carbon-credit schemes rewarding bio-fertilizer use | +1.5% | France, Germany, Netherlands, gradual European Union-wide rollout | Long term (≥ 4 years) |

| AI-guided microbiome formulations boosting field efficacy | +1.9% | United Kingdom, Germany, France, diffusion to Southern Europe | Medium term (2-4 years) |

| Post-Brexit United Kingdom fast-track pathway for biological registrations | +1.0% | United Kingdom, indirect European Union influence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Organic and Regenerative Farming

Certified organic farmland across the European Union reached 15.9 million hectares in 2024, representing 10.2% of the total utilized agricultural area. France, Spain, and Italy collectively manage over 7 million hectares under organic protocols. Regenerative agriculture, which emphasizes soil health metrics beyond organic certification, is expanding even faster as carbon credit programs and retailer sustainability scorecards reward practices such as cover cropping, reduced tillage, and microbial inoculant use. The trend is most pronounced in Germany and France, where large-scale arable farms possess the agronomic expertise and equipment to integrate microbials into precision-seeding workflows, yet smaller Mediterranean holdings in Spain and Italy are catching up as cooperative extension services disseminate application protocols tailored to high-value horticultural crops.

European Union Farm-to-Fork Pesticide-Reduction Mandates

The European Commission's Farm-to-Fork strategy, adopted in 2020 and reinforced through 2024 legislative updates, mandates a 50% reduction in chemical pesticide use and risk by 2030, creating a regulatory void that biological alternatives must fill [1]Source: European Commission, “Farm to Fork Strategy,” food.ec.europa.eu . Member states are translating this target into national action plans. For instance, France has committed to phasing out glyphosate and neonicotinoids ahead of the Europe Union-wide deadline, while Germany has introduced stricter buffer zones around water bodies that effectively ban many conventional sprays. These restrictions are accelerating the adoption of microbes in two ways. First, they remove chemical competitors from the market, forcing growers to trial bacterial and fungal biocontrols for diseases such as botrytis and powdery mildew. The regulatory influence of the European Union's Sustainable Use of Pesticides Directive further reinforces this shift by requiring integrated pest management plans that prioritize non-chemical methods, embedding microbials into the compliance framework rather than treating them as optional add-ons.

Consumer Demand for Residue-Free Produce

Premium retail chains across Germany, France, and the United Kingdom have instituted zero-residue certification programs that test finished produce for any detectable pesticide traces, a standard more stringent than organic certification, which permits certain approved substances. Major German discounters and French hypermarkets now reserve premium shelf space and price points for zero-residue lines, creating a direct revenue incentive for growers to replace chemical sprays with microbial alternatives. This consumer-driven specification is reshaping supply contracts, with processors and packers inserting residue clauses that shift liability for non-compliance back to the farm level. Spain's export-oriented fruit and vegetable sector is responding by investing in microbial seed treatments and foliar biofungicides, recognizing that access to Northern European markets hinges on demonstrable residue compliance rather than price competitiveness alone.

Expansion of European Union Carbon-Credit Schemes Rewarding Bio-Fertilizer Use

The European Union's Carbon Farming Initiative, launched in pilot form in 2024, offers growers financial compensation for verified greenhouse gas reductions achieved through practices such as reduced tillage, cover cropping, and the application of nitrogen-fixing inoculants. France and Germany are leading the early implementation, with carbon-credit prices ranging from USD 26 to USD 42 per ton of CO2 equivalent, depending on the rigor of verification and the scale of the project. The scheme also incentivizes microbial biostimulants that enhance soil organic carbon accumulation, although measurement protocols remain under development and vary by member state. This carbon-credit architecture is still in its early stages, with fewer than 5% of Europe Union farms enrolled as of early 2025, yet, it represents a structural shift in farm economics that could eventually make microbial inoculants cost-neutral or even profit-positive, independent of their agronomic benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront product and distribution costs | -2.4% | Southern and Eastern Europe smallholder farms, moderate in the West | Short term (≤ 2 years) |

| Limited farmer awareness and training gaps | -1.8% | Eastern Europe, Southern Italy, and Spain's smallholder regions | Medium term (2-4 years) |

| Lengthy two-step Europe Union microbial registration process | -1.5% | Pan-European | Long term (≥ 4 years) |

| Cold-chain and logistics gaps in Central and Eastern Europe | -1.1% | Poland, Romania, Bulgaria, Hungary, Czech Republic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Product and Distribution Costs

Microbial products typically cost 20 to 40% more per hectare than chemical equivalents, a price gap driven by fermentation, cold-storage, and shorter shelf-life economics that inflate production and distribution expenses. For smallholder farms in Southern and Eastern Europe, where average holdings range from 3 to 8 hectares, and cash-flow constraints limit input budgets, this premium represents a meaningful barrier to trial adoption. Growers operating on thin margins prioritize inputs with proven, immediate returns, whereas microbials often require multi-season observation to demonstrate cumulative soil-health benefits that justify higher costs. Distribution infrastructure compounds the challenge, as microbial products demand refrigerated transport and storage to maintain viable cell counts, adding logistics expenses that chemical distributors avoid. In Poland and Romania, where rural cold-chain networks remain underdeveloped, distributors pass these costs to end users, further widening the price gap. Some manufacturers are responding by offering pay-for-performance contracts that tie payment to yield outcomes, yet these arrangements require third-party verification and remain rare outside Western European markets, where agronomic advisory services can monitor trial plots and document results.

Limited Farmer Awareness and Training Gaps

Effective microbial application hinges on precise timing, soil temperature, moisture levels, and compatibility with other inputs, yet many European extension services lack the resources or expertise to train growers in these protocols. In Eastern Europe and Southern Italy, where public advisory budgets have stagnated, farmers often receive generic recommendations that fail to account for microbial-specific requirements such as avoiding tank-mixing with copper-based fungicides or applying inoculants within narrow soil-temperature windows. This knowledge deficit leads to suboptimal results, eroding confidence and dampening repeat purchase rates. Spain's horticultural sector has partially addressed the gap through cooperative-led training programs, where agronomists conduct on-farm demonstrations and provide season-long support, yet such initiatives remain concentrated in high-value export crops rather than broadacre systems. The lack of standardized application guidelines also creates liability concerns, as growers are uncertain about proper use and may default to familiar chemical programs rather than risk crop failure with unfamiliar biologicals. Industry associations are advocating for European Union-funded extension programs that embed microbial training into national advisory curricula, though implementation timelines extend beyond 2027 in most member states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bacteria Dominance Masks Fungal Segment Surge

Bacteria-based microbials captured 64.70% of the Europe agricultural microbial market size in 2025, anchored by established genera such as Bacillus, Pseudomonas, and Rhizobium that deliver proven efficacy in nitrogen fixation, phosphate solubilization, and biocontrol of fungal pathogens. The bacterial segment's maturity is attracting consolidation, with BASF SE and Bayer AG acquiring smaller inoculant firms to secure proprietary strains and fermentation capacity. Fungal products are benefiting from recent innovations in liquid formulations, which improve shelf stability and field application uniformity compared to traditional wettable powders. Regulatory frameworks under the Europe Biocidal Products Regulation and Plant Protection Products Regulation influence approval timelines, with bacterial and fungal strains often qualifying for expedited review when they exhibit low mammalian toxicity and environmental persistence.

Fungi microbials are expanding at a 15.12% CAGR through 2031, driven by grower demand for dual-function products that suppress soil-borne diseases while improving soil structure and organic matter content. Viral microbials, dominated by baculoviruses targeting lepidopteran pests, serve niche applications in high-value crops where highly specific pest control justifies premium pricing and minimizes non-target impacts on beneficial insects. Protozoa remain an emerging segment, primarily applied in controlled-environment agriculture to suppress soil-borne nematodes and root pathogens. However, research into field-scale formulations is accelerating as production costs decline.

By Application: Fruits and Vegetables Lead, Commercial Crops Accelerate

The fruits and vegetables led with 36.50% revenue share in 2025, reflecting the sector's high-value economics that justify premium-priced microbial inputs and the stringent residue specifications imposed by export markets. The fruits and vegetables segment benefits from Spain's greenhouse industry, which produces over 4 million metric tons of tomatoes, peppers, and cucumbers annually under integrated biological programs that combine microbial biocontrols with predatory insects to meet zero-residue standards . Italy's stone-fruit and citrus growers are similarly transitioning to microbial fungicides to manage diseases such as brown rot and citrus canker, driven by retailer de-listing threats and consumer preference for residue-free produce.

Pulses and oilseeds are projected to grow at a 14.67% CAGR through 2031, as carbon-credit schemes and regenerative-agriculture incentives reward nitrogen-fixing inoculant use in legume rotations. Grains and cereals represent a mature application segment, with microbial seed treatments widely adopted in wheat and barley systems to enhance germination and early-season vigor. Growth rates in this category lag behind those of other segments due to market saturation in Western Europe. Pulses and oilseeds are experiencing the fastest growth among commercial crops, as rhizobium inoculants for soybeans, peas, and lentils deliver measurable nitrogen-fixation benefits, reducing synthetic fertilizer costs by USD 52 to USD 104 per hectare.

By Mode of Application: Soil Treatment Anchors Market, Foliar Gains Momentum

By mode of application, soil treatment accounted for 44.40% of the Europe agricultural microbial market size in 2025, reflecting its compatibility with existing pre-plant tillage and seeding workflows that minimize labor and equipment investments. The dominance of soil treatment stems from its effectiveness in delivering high microbial populations directly to the root zone, where bacteria and fungi colonize plant tissues and establish long-term symbiotic relationships. Germany's potato and sugar-beet sectors favor soil-incorporated microbials to suppress soil-borne pathogens such as Rhizoctonia and Verticillium, applying products during spring tillage operations that integrate seamlessly into conventional field preparation.

Foliar spray adoption is projected to rise at a 14.32% CAGR to 2031, propelled by precision-application technologies such as GPS-guided sprayers and drone-mounted nozzles that reduce product waste and improve coverage uniformity. Foliar spray adoption is accelerating in Spain's greenhouse vegetable systems, where weekly applications of Bacillus and Trichoderma formulations prevent outbreaks of botrytis and powdery mildew, which can devastate enclosed environments. Precision sprayers equipped with variable-rate controllers adjust microbial dosing based on real-time canopy density and disease-pressure sensors, optimizing efficacy while minimizing input costs.

Geography Analysis

France is projected to account for 20.85% of the Europe agricultural microbial market in 2025. This is supported by 2.8 million hectares of certified organic farmland, primarily focused on wine-grape, fruit, and vegetable systems, where microbial fungicides and biostimulants are now standard practices. Government initiatives under the Ecophyto 2025 plan, which aims to achieve a 50% reduction in chemical pesticide use, provide subsidies to growers adopting integrated biological programs. These subsidies help offset the 20% to 40% cost premium of microbial products compared to chemical alternatives. Additionally, the expansion of protein crops, mandated under the European Union's Common Agricultural Policy to reduce feed imports, is driving demand for rhizobium inoculants in soybean, pea, and lentil rotations, with over 1.5 million hectares planted in 2024.

Poland is projected to grow at an 17.10% CAGR through 2031, marking the fastest growth rate among European countries. This growth is driven by increased adoption from a low baseline, supported by European Union Green Deal funds and the rapid expansion of certified organic farmland, which doubled between 2020 and 2024. Poland's integration into premium Western European supply chains is encouraging vegetable and berry growers to implement zero-residue production systems, relying on microbial biocontrols. Furthermore, government subsidies cover up to 30% of microbial input costs for farms transitioning to organic certification. The country's cold-chain infrastructure is also improving, as multinational distributors invest in refrigerated warehouses near major agricultural zones, addressing historical challenges related to product viability and field performance.

The United Kingdom's post-Brexit regulatory environment has shortened microbial approval timelines, attracting multinational firms to conduct first-in-market launches that generate field-performance data and grower testimonials ahead of Europe Union-wide registration. British berry and leafy-green producers are early adopters of novel baculovirus and bacterial strains, leveraging faster approvals to differentiate their produce in premium retail channels. Spain's Almería greenhouse cluster, spanning over 30,000 hectares of protected cultivation, serves as a global testing ground for biological pest management. Growers integrate microbial sprays, predatory insects, and pheromone traps into their year-round production cycles, eliminating chemical residues.

Competitive Landscape

The Europe agricultural microbial market exhibits moderate concentration, with the top players including BASF SE, Bayer AG, Syngenta AG, Syngenta Group Co., Ltd., and Corteva Inc. commanding a significant combined share in 2024. These companies dominate through vertical integration strategies that control fermentation capacity, cold storage networks, and distribution channels, ensuring product viability from the bioreactor to the farm gate. Strategic moves center on acquiring smaller biotech firms with proprietary microbial strains, expanding European production facilities to shorten supply chains, and partnering with precision-agriculture platforms to embed microbial recommendations into digital advisory tools.

Emerging disruptors include start-ups that deploy machine learning algorithms to screen thousands of microbial strains and predict synergistic combinations tailored to specific agro-climatic zones, thereby lowering development costs and accelerating time-to-market. Technology adoption is reshaping competitive dynamics, as firms that integrate microbial products with precision-application equipment and real-time soil sensors can offer growers outcome-based guarantees that de-risk trial adoption and build long-term loyalty.

BASF's 2024 patent filings for encapsulated bacterial formulations that extend shelf life to 36 months without refrigeration illustrate the innovation focus on overcoming cold-chain constraints that limit Eastern European penetration [3]Source: European Patent Office, “Patent Database,” epo.org . Koppert's expansion of biocontrol production capacity in Spain and France positions the firm to serve Southern European greenhouse clusters with shorter lead times and lower freight costs than Northern European competitors.

Europe Agricultural Microbial Industry Leaders

BASF SE

Bayer AG

Syngenta Group Co. Ltd.

Corteva Inc.

Koppert Group B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Koppert and Amoéba, an industrial Greentech company, have introduced their strategic partnership to develop and commercialize an innovative agricultural microbial solution. This collaboration aims to strengthen the sustainable agriculture portfolio by introducing an environmentally conscious crop protection alternative to the European market.

- October 2023: BASF funded a USD 52 million expansion of its microbial fermentation facility in Ludwigshafen, Germany, adding 30 percent capacity to meet rising demand for liquid bacterial inoculants across Western Europe. The investment includes new cold-storage infrastructure and automated bottling lines designed to extend shelf life and reduce distribution costs.

- October 2022: Corteva Agriscience received Europe Union approval for a novel Pseudomonas strain targeting soil-borne fungal pathogens in potato and sugar-beet systems, following a 6-year registration process.

Europe Agricultural Microbial Market Report Scope

Agricultural microbials refer to naturally occurring microorganisms, including bacteria, fungi, viruses, and protozoa, that enhance crop productivity and protect plants from pests, diseases, and environmental stresses. These biological solutions improve soil health, increase nutrient availability, and promote plant growth. The Europe Agricultural Biologicals Market is segmented by Type (Bacteria, Fungi, and Others), Application (Grains and Cereals, Pulses and Oilseeds, Commercial Crops, Fruits and Vegetables, and Other Crop Types), and Geography (Germany, UK, France, Spain, Italy, Netherlands, Russia, and Rest of Europe). The value is provided in USD for the above segments.

By Type

| Bacteria |

| Fungi |

| Others |

By Application

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Commercial Crops |

| Other Crop Types |

By Mode of Application

| Soil Treatment |

| Foliar Spray |

| Seed Treatment |

By Geography

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Turkey |

| Russia |

| Rest of Europe |

| By Type | Bacteria |

| Fungi | |

| Others | |

| By Application | Fruits and Vegetables |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Commercial Crops | |

| Other Crop Types | |

| By Mode of Application | Soil Treatment |

| Foliar Spray | |

| Seed Treatment | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the Europe agricultural microbial market in 2026?

It is valued at USD 3.31 billion and is projected to double to USD 6.45 billion by 2031.

Which microbial type expands fastest in Europe?

Fungi, mainly baculoviruses, are forecast to grow at a 15.12% CAGR through 2031.

Which countries lead the way in microbial adoption in Europe?

Germany, France, and the United Kingdom command the largest revenue pools due to organic acreage, fast-track approvals, and zero-residue retail standards.

What challenges limit uptake in Eastern Europe?

High upfront costs, limited cold-chain infrastructure, and fragmented extension services reduce product viability and farmer confidence.

Page last updated on: