Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

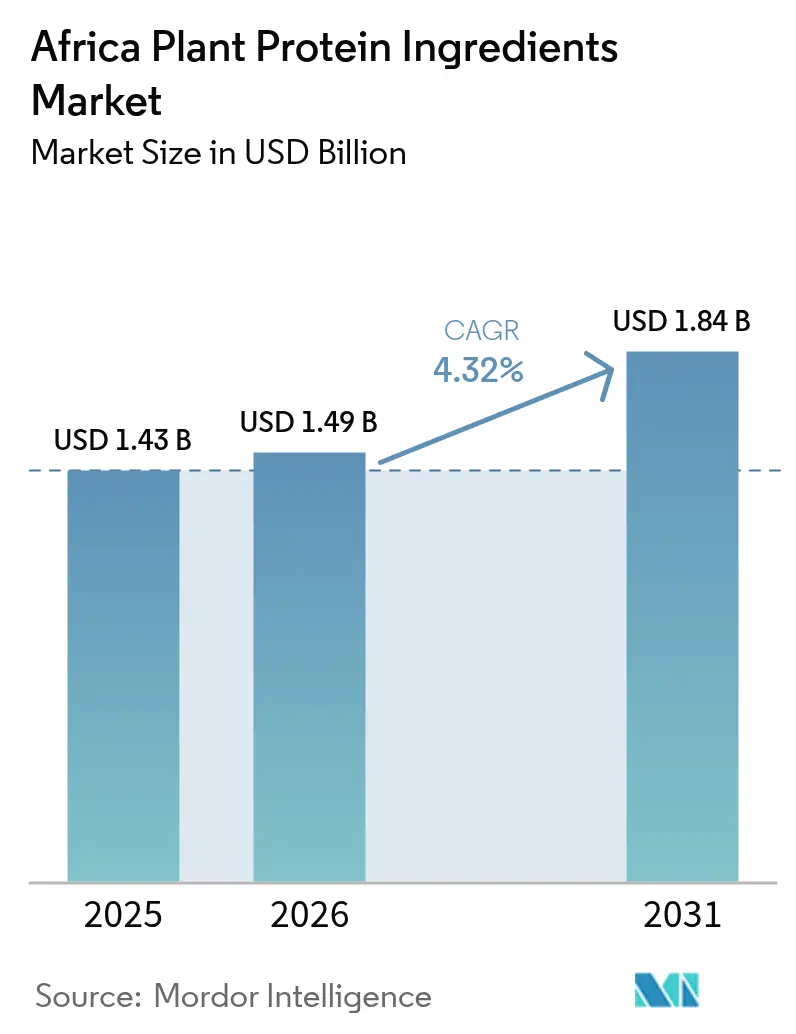

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 1.84 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

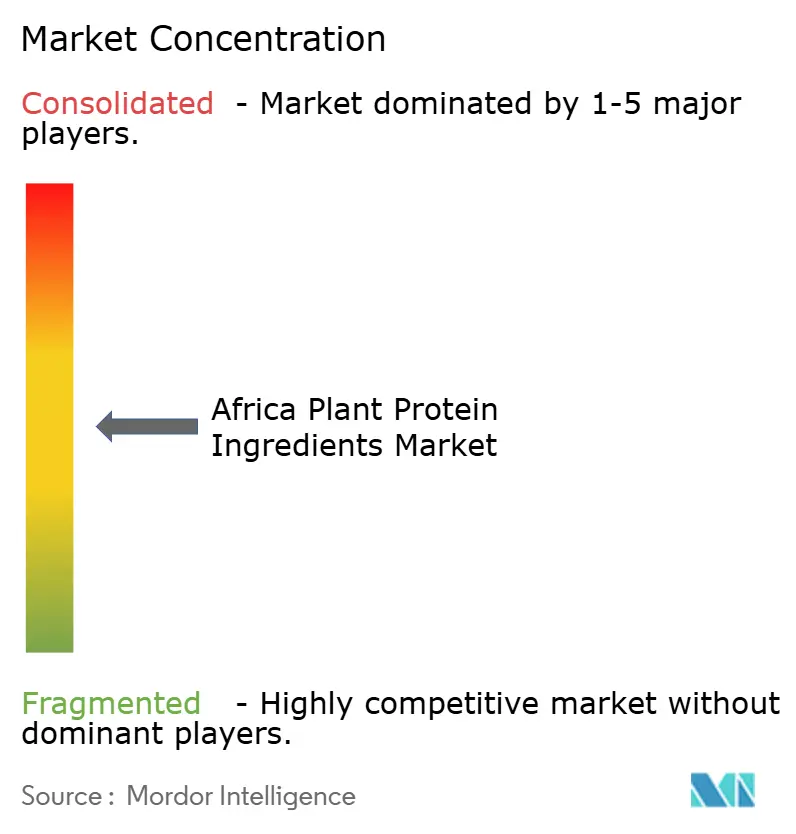

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Plant Protein Ingredients Market Analysis by Mordor Intelligence

The Africa plant protein ingredients market size in 2026 is estimated at USD 1.49 billion, growing from 2025 value of USD 1.43 billion with 2031 projections showing USD 1.84 billion, growing at 4.32% CAGR over 2026-2031. This growth is driven by several factors, including the rising urban population, the implementation of stricter allergen-labeling regulations, and the commercial introduction of locally sourced pea and cowpea proteins. Manufacturers are increasingly shifting from reliance on imported wheat and soy concentrates to indigenous legumes, aiming to reduce exposure to foreign exchange fluctuations. Retailers are responding to consumer demand for clean-label products by emphasizing traceable supply chains. Multinational corporations are strengthening vertical integration strategies to secure consistent raw material supplies, while regional processors are capitalizing on their proximity to crops to develop niche African foods fortified with protein. Despite these positive trends, challenges such as fragmented regulatory frameworks and climate-induced variations in crop yields pose risks to market growth. However, initiatives like free-trade agreements and public research funding are expected to create significant long-term opportunities for the market.

Key Report Takeaways

- By protein type, soy protein captured 67.05% of the Africa plant protein ingredients market share in 2025, while pea protein is projected to expand at a 5.86% CAGR through 2031.

- By category, conventional ingredients commanded 89.65% of the Africa plant protein ingredients market size in 2025, but organic counterparts are set to grow at a 6.1% CAGR to 2031.

- By end user, food and beverage applications held 50.78% of the Africa plant protein ingredients market in 2025; nutritional supplements will register the fastest 6.45% CAGR through 2031.

- By geography, Nigeria led with 36.98% of the Africa plant protein ingredients market share in 2025 and is on course for a 5.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Plant Protein Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness of health benefits linked to plant-based diets | +0.9% | Nigeria, South Africa, Kenya (urban centers) | Medium term (2-4 years) |

| Increasing prevalence of lactose intolerance and milk allergies | +0.8% | Sub-Saharan Africa (70-90% adult prevalence) | Short term (≤ 2 years) |

| Shift toward flexitarian, vegan, and vegetarian lifestyles | +0.7% | South Africa, Nigeria (urban youth demographics) | Medium term (2-4 years) |

| Growing demand for clean-label and natural ingredients | +0.6% | South Africa, Kenya, Nigeria (retail-driven) | Long term (≥ 4 years) |

| Consumer concern for sustainability and lower carbon footprint | +0.5% | South Africa, Nigeria (corporate sustainability mandates) | Long term (≥ 4 years) |

| Adoption of plant protein in infant and sports nutrition | +0.8% | Nigeria, South Africa, Kenya (premium segments) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Awareness of Health Benefits Linked to Plant-Based Diets

Urban consumers in Lagos, Johannesburg, and Nairobi are increasingly associating plant protein consumption with health benefits, including a lower risk of cardiovascular issues and better weight management. This perception has been strengthened by the influence of social media personalities and targeted nutrition campaigns from organizations such as the South African Heart and Stroke Foundation. Recent findings indicate a significant portion of South African youth in the 18 to 35 age group have reduced their red meat intake over the past year, primarily due to health-related concerns [1]Source: Rhodes University, “Youth Dietary Shifts in South Africa,” ru.ac.za. This behavioral change is fueling demand for plant protein products across categories like ready-to-eat meals, protein bars, and fortified beverages, where manufacturers are able to charge notable price premiums compared to traditional offerings. The trend is not limited to high-income neighborhoods, as middle-income households in Nigeria's secondary cities are increasingly incorporating plant-based staples such as soy-fortified garri and cowpea-enriched porridges into their diets, driving growth in mid-tier price ranges. However, the absence of standardized nutrition labeling in many African markets poses a challenge, as it limits consumers' ability to verify protein content claims. This has slowed adoption among more skeptical buyers, who often prioritize taste and texture over health-focused attributes.

Increasing Prevalence of Lactose Intolerance and Milk Allergies

Lactose intolerance affects an estimated 70% to 90% of sub-Saharan African adults due to the genetic absence of lactase persistence, limiting dairy consumption and increasing demand for plant-based milk alternatives and protein-fortified beverages. In South Africa, soy milk and oat milk have gained popularity, with retail sales of plant-based dairy alternatives growing by 14% year-over-year in 2024, according to Nielsen data cited by local distributors. Infant formula manufacturers are under regulatory pressure to provide hypoallergenic options, leading brands such as Nestlé and Danone to introduce pea protein-based formulas that comply with South Africa's Foodstuffs, Cosmetics and Disinfectants Act regulations on allergen labeling. In Nigeria, the Federal Ministry of Health issued updated guidelines in 2024 requiring clear disclosure of milk-derived ingredients, accelerating reformulation timelines for both imported and locally produced infant nutrition products. The combination of genetic predisposition and regulatory enforcement supports growth in plant protein ingredients, although affordability remains a challenge in rural areas where traditional dairy products are less expensive than imported alternatives.

Shift Toward Flexitarian, Vegan, and Vegetarian Lifestyles

Flexitarian eating patterns, defined by occasional meat consumption and a greater emphasis on plant proteins, are gaining traction among Africa's urban middle class. This trend is influenced by environmental documentaries, animal welfare campaigns, and the growing presence of plant-based restaurants in cities such as Johannesburg, Cape Town, and Lagos. According to The Good Food Institute, South Africa allocated government grants in 2024 to support alternative protein research, highlighting the government's acknowledgment of the sector's growth potential [2]Source: Good Food Institute, “Alternative Protein Funding in South Africa,” gfi.org. Local startups, including The Herbivore in Cape Town and Veggie Victory in Lagos, have introduced plant-based burger patties and sausages made from pea and soy protein. These products have secured shelf space in premium grocery stores and quick-service restaurants, appealing to younger consumers who view plant-based eating as a lifestyle choice rather than a dietary limitation. This perception allows brands to charge significant premiums over traditional meat products. However, the adoption of plant-based alternatives remains largely confined to high-income urban areas, with limited acceptance in rural regions where cultural preferences favor animal protein and plant-based options are often regarded as inferior substitutes.

Growing Demand for Clean-Label and Natural Ingredients

Consumers in South Africa and Kenya are increasingly examining ingredient lists, preferring products with simple, recognizable components over those containing synthetic additives or highly processed isolates. This growing preference for clean-label products is driving demand for minimally processed plant protein concentrates and organic certifications. However, organic certifications remain limited due to a scarcity of accreditation bodies and the high costs of audits, which discourage smallholder farmers from obtaining organic status. Retailers such as Woolworths and Pick n Pay in South Africa have expanded their private-label offerings to include non-GMO soy protein and pea protein sourced from verified supply chains. This aligns with consumer willingness to pay premiums of 15% to 25% for transparency. Ingredient suppliers are also investing in traceability platforms that document protein origins, processing methods, and sustainability metrics, anticipating potential regulatory requirements similar to Europe's Farm to Fork strategy. Despite these developments, the lack of harmonized clean-label definitions across African markets poses challenges. Manufacturers must navigate varying standards in countries like Nigeria, South Africa, and Kenya, each interpreting terms such as "natural" and "minimally processed" differently, adding to compliance complexities.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity for international certification | -0.6% | Nigeria, South Africa (divergent frameworks) | Medium term (2-4 years) |

| Food fraud and adulteration risks with plant protein concentrates | -0.4% | Nigeria, Kenya (enforcement gaps) | Short term (≤ 2 years) |

| Price volatility and unreliable raw material supply due to weather/climate | -0.7% | Nigeria, South Africa (drought-prone zones) | Short term (≤ 2 years) |

| Supply chain disruptions due to logistics or trade barriers | -0.5% | Sub-Saharan Africa (infrastructure deficits) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity for International Certification

Divergent regulatory frameworks across African markets create substantial compliance challenges for plant protein ingredient suppliers. Each country enforces unique registration, labeling, and testing requirements, with no mutual recognition protocols in place. For example, Nigeria's National Agency for Food and Drug Administration and Control (NAFDAC) mandates facility inspections, batch testing, and the submission of separate dossiers for each protein type[3]Source: NAFDAC, “Food Registration Guidelines,” nafdac.gov.ng. This rigorous process can take between 12 to 18 months to complete and involves costs ranging from USD 50,000 to USD 100,000 per product line. These high costs and lengthy timelines discourage smaller manufacturers from entering the market. While multinational corporations can manage these expenses through economies of scale, regional processors and startups often face disproportionate challenges. This limits their ability to innovate and delays the introduction of novel protein sources, such as hemp and potato protein, which could otherwise diversify and enhance the market.

Food Fraud and Adulteration Risks with Plant Protein Concentrates

The adulteration of plant protein concentrates with cheaper fillers, such as melamine, wheat flour, or rice starch, poses significant challenges to quality and safety, particularly in regions with limited laboratory testing capabilities and enforcement mechanisms. For instance, in 2024, the Standards Organisation of Nigeria (SON) issued alerts regarding mislabeled soy protein imports that contained undeclared wheat protein. This issue not only triggered allergic reactions among consumers with celiac disease but also eroded consumer trust in plant-based products. Advanced authenticity testing methods, such as isotope ratio mass spectrometry (IRMS) and DNA barcoding, offer solutions but remain prohibitively expensive and inaccessible for most African food manufacturers. This creates opportunities for fraudulent suppliers to exploit information gaps. Furthermore, the absence of traceability systems in informal supply chains—which account for an estimated 60% to 70% of food distribution in countries like Nigeria and Kenya—exacerbates the risk of fraud, as protein concentrates often pass through multiple intermediaries before reaching end users. Industry associations, such as the African Organisation for Standardisation (ARSO), are actively working to develop regional authentication protocols. However, progress has been slow due to funding constraints and the limited technical expertise available among member states, highlighting the need for greater investment and capacity building in this area.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Soy protein held a significant 67.05% share of the market in 2025, reflecting its long-standing presence supported by established supply chains, familiarity among African farmers with soybean cultivation, and cost advantages over newer alternatives. Nigeria and South Africa together produce approximately 1.2 million metric tons of soybeans annually, which supports domestic crushing and the production of soy protein concentrate. This concentrate is widely used in bakery, beverage, and meat alternative applications, showcasing its versatility and strong market presence.

Pea protein, on the other hand, is expected to grow at a compound annual growth rate (CAGR) of 5.86% through 2031, marking it as the fastest-growing protein type. This growth is driven by a shift toward allergen-free options that meet stricter labeling regulations and address consumer concerns about the phytoestrogen content in soy. Wheat protein, primarily produced in Ethiopia and Egypt where wheat cultivation is prevalent, is used in bakery and pasta applications but faces challenges due to increasing gluten sensitivity, limiting its growth to established end-user segments. Potato protein remains a niche product, constrained by limited cultivation in Africa and high import costs. Meanwhile, rice protein is gaining popularity in infant formula applications due to its hypoallergenic properties and neutral taste, which make it suitable for blending with other ingredients.

By Category: Conventional Dominance Masks Organic Opportunity

In 2025, conventional plant protein ingredients held 89.65% of the market share. This dominance reflects challenges such as limited infrastructure for organic certification, high audit costs, and a price-sensitive consumer base that prioritizes affordability over organic credentials. Organic certification requires third-party verification by organizations like Ecocert or the South African Organic Sector Organisation (SAOSO). These processes cost between USD 3,000 and USD 10,000 annually and demand traceability documentation, which smallholder farmers often find difficult to maintain.

Despite these challenges, organic plant proteins are expected to grow at a compound annual growth rate (CAGR) of 6.1% through 2031, outpacing conventional variants. This growth is driven by South African retailers expanding clean-label private brands and export-oriented processors targeting European markets, where organic products command premiums of 40% to 60%. Retailers such as Woolworths and Pick n Pay have introduced organic soy and pea protein in ready-to-eat meals and protein bars. These products cater to affluent consumers willing to pay ZAR 80 to ZAR 120 (USD 4.40 to USD 6.60) per serving, which is double the price of conventional alternatives.

By End User: Food Dominance Yields to Nutrition Premiumization

Food and beverage applications held a 50.78% share of the market in 2025, covering categories such as bakery, beverages, dairy alternatives, meat substitutes, and ready-to-eat meals. These products utilize plant proteins to enhance nutritional value, improve texture, and reduce costs. The bakery segment remains the largest within this category, as soy and wheat proteins contribute to better dough elasticity and longer shelf life for bread, biscuits, and pastries. These products are widely distributed through Africa's informal retail networks. Beverages, particularly plant-based milk alternatives, experienced a 14% growth in 2024. This growth was driven by the rising prevalence of lactose intolerance and increasing health awareness, prompting consumers to replace dairy milk with soy, oat, and almond-based options, especially in South African supermarkets.

Nutritional supplements are expected to grow at a compound annual growth rate (CAGR) of 6.45% through 2031, making it the fastest-growing segment among end users. This growth is supported by higher disposable incomes, the growing popularity of fitness culture, and the reformulation of infant formula with hypoallergenic pea and rice proteins. Additionally, sports nutrition products, such as protein powders and recovery bars, are increasingly targeting urban gyms and online fitness communities, catering to the needs of health-conscious consumers.

Geography Analysis

Nigeria led the market in 2025, capturing 36.98% of the market share. This leadership is driven by a population exceeding 220 million, rapid urbanization that centralizes purchasing power in cities like Lagos and Abuja, and government efforts to reduce reliance on food imports by promoting local protein processing. The Middle Belt soybean zone produces approximately 800,000 metric tons annually, supporting domestic crushing operations that supply soy protein concentrates to bakery, beverage, and animal feed manufacturers. However, challenges such as erratic rainfall and limited irrigation infrastructure create yield fluctuations, forcing manufacturers to blend domestic and imported protein, which increases costs and limits profit margins. Additionally, the National Agency for Food and Drug Administration and Control (NAFDAC) imposes stringent registration requirements and approval timelines of 12 to 18 months, discouraging smaller suppliers and consolidating the market among established processors with the resources to manage compliance costs.

South Africa is the fastest-growing segment, supported by its advanced retail infrastructure, established organic certification bodies, and consumer preferences for clean-label and sustainable products. Retailers like Woolworths, Pick n Pay, and Shoprite have expanded their plant-based private label offerings, catering to affluent consumers in Johannesburg, Cape Town, and Durban. These consumers are willing to pay a premium of 15% to 25% for non-GMO and organic plant proteins, further driving market growth in the region.

The rest of Africa, including Kenya, Ghana, Ethiopia, and smaller markets, exhibits diverse and fragmented demand patterns shaped by varying dietary traditions, income levels, and regulatory environments. In Kenya, the urban middle class in cities like Nairobi and Mombasa is driving demand for plant-based dairy alternatives and sports nutrition products. Meanwhile, Ethiopia's wheat protein production supports its domestic pasta and bakery industries, highlighting the region's varied market dynamics.

Competitive Landscape

The Africa Plant Protein Ingredients Market shows a moderately competitive environment, where multinational ingredient suppliers such as Cargill, Archer Daniels Midland (ADM), and Ingredion operate alongside regional processors that source locally grown soybeans, cowpeas, and wheat. Multinational companies leverage their economies of scale in imported pea and soy protein isolates, global research and development networks, and established partnerships with large food manufacturers. These strengths allow them to deliver consistent quality and technical support, which smaller competitors often find challenging to match. Regional processors, however, focus on their proximity to raw materials, lower logistics costs, and the ability to customize products for niche applications, such as traditional African foods enriched with indigenous legume proteins.

This two-tier market structure creates opportunities in mid-market segments, where customers seek quality assurance beyond artisanal producers but cannot afford the pricing of multinational suppliers. Emerging players can address this gap by emphasizing regional branding and adopting traceability platforms that document the origin and processing methods of proteins. Technology adoption varies widely, with multinationals utilizing advanced methods like extrusion and membrane filtration to produce high-purity isolates, while regional processors rely on conventional milling and air classification techniques. These traditional methods yield lower protein concentrations but require minimal capital investment, making them accessible to smaller players.

Emerging disruptors in the market include South African startups such as The Herbivore and Veggie Victory, which use social media marketing and direct-to-consumer channels to build brand loyalty among urban flexitarians, bypassing traditional retail distribution channels. Patent filings related to plant protein processing in Africa remain limited, with only 12 applications submitted to the African Regional Intellectual Property Organization (ARIPO) in 2024. This indicates minimal formal innovation activity and underscores potential opportunities for companies willing to invest in proprietary extraction or functionalization technologies.

Africa Plant Protein Ingredients Industry Leaders

Archer Daniels Midland Co.

Kerry Group plc

International Flavors & Fragrances Inc.

Wilmar International Ltd

Roquette Frères SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zyra Protein introduced a plant-based protein powder featuring only four ingredients: pea protein, date powder, strawberry powder, and salt. The product emphasizes clean-label nutrition and simplicity, targeting health-conscious consumers.

- January 2025: Griffith Foods introduced its first Alternative Proteins Portfolio. This initiative aims to provide plant-based protein solutions, improve nutrition, promote sustainability, and enhance food accessibility in global and underserved markets, including Africa, with plans for ongoing expansion.

- July 2024: The Food Innovation Lab at UFS developed affordable, protein-rich soy-based snacks and dairy alternatives, including flavoured soymilk, yoghurt, and snacks using soybean byproducts.

Africa Plant Protein Ingredients Market Report Scope

Hemp Protein, Pea Protein, Potato Protein, Rice Protein, Soy Protein, Wheat Protein are covered as segments by Protein Type. Animal Feed, Food and Beverages, Personal Care and Cosmetics, Supplements are covered as segments by End User. Nigeria, South Africa are covered as segments by Country.By Protein Type

| Soy Protein | Concentrates |

| Hydrolyzed | |

| Isolates | |

| Wheat Protein | Concentrates |

| Hydrolyzed | |

| Isolates | |

| Pea Protein | Concentrates |

| Hydrolyzed | |

| Isolates | |

| Potato Protein | |

| Rice Protein | |

| Hemp Protein | |

| Others |

By Category

| Organic |

| Conventional |

By End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| RTE/RTC Foods | |

| Snacks | |

| Personal Care and Cosmetics | |

| Nutritional Supplements | Baby and Infant Formula |

| Elderly and Medical Nutrition | |

| Sport/Performance Nutrition |

By Geography

| Nigeria |

| South Africa |

| Rest of Africa |

| By Protein Type | Soy Protein | Concentrates |

| Hydrolyzed | ||

| Isolates | ||

| Wheat Protein | Concentrates | |

| Hydrolyzed | ||

| Isolates | ||

| Pea Protein | Concentrates | |

| Hydrolyzed | ||

| Isolates | ||

| Potato Protein | ||

| Rice Protein | ||

| Hemp Protein | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Foods | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Nutritional Supplements | Baby and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

| By Geography | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms