Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

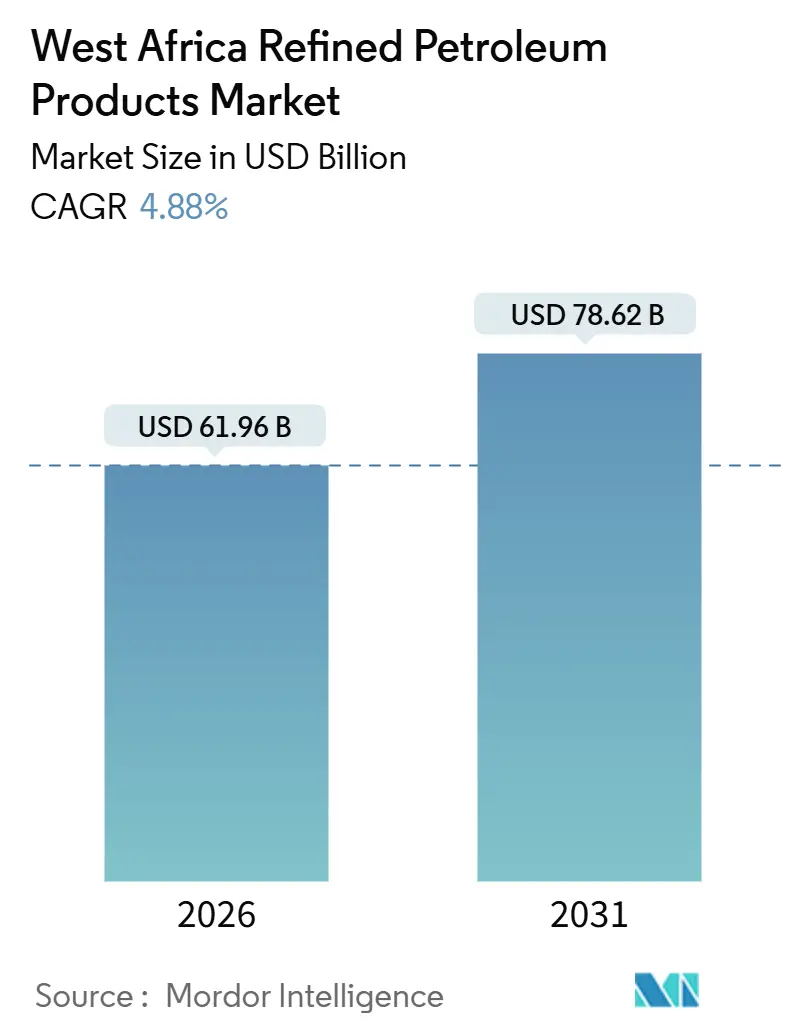

| Market Size (2026) | USD 61.96 Billion |

| Market Size (2031) | USD 78.62 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

West Africa Refined Petroleum Products Market Analysis by Mordor Intelligence

The West Africa Refined Petroleum Products Market size is estimated at USD 61.96 billion in 2026, and is expected to reach USD 78.62 billion by 2031, at a CAGR of 4.88% during the forecast period (2026-2031).

Rising domestic refining capacity, led by the 650,000-barrel-per-day Dangote facility, is displacing European and Asian imports, anchoring foreign-exchange savings, and drawing private investment despite currency weakness. Fiscal space created by Nigeria’s 2023 subsidy phase-out, coupled with modular refinery rollouts in Niger and northern Nigeria, is reshaping trade flows while online fuel-delivery platforms expand last-mile options for urban fleets. Demand is bifurcating: commercial users continue to absorb higher diesel prices, whereas households gravitate toward LPG and compressed natural gas, nudging product-mix dynamics toward cleaner fuels. Intensifying environmental rules, including IMO 2020 and emerging ECOWAS sulfur limits, are accelerating low-sulfur fuel uptake and sparking infrastructure upgrades at bunkering hubs in Ghana and Côte d’Ivoire.

Key Report Takeaways

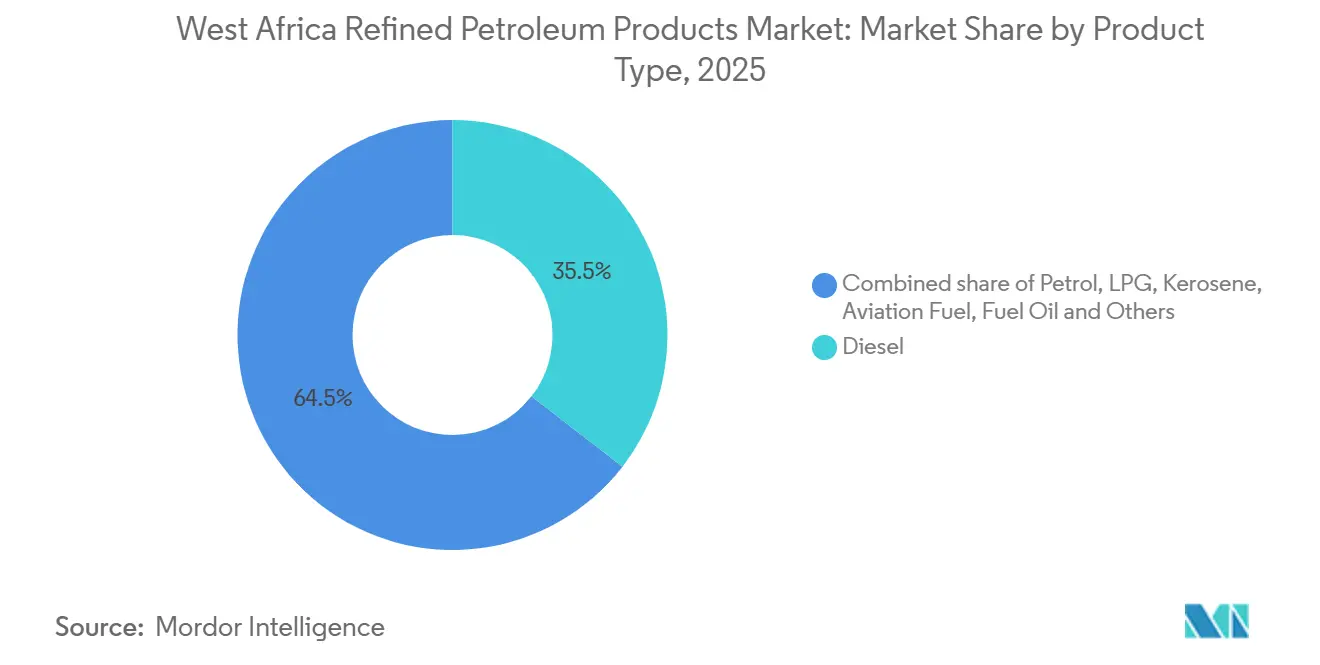

- By product type, diesel led with 35.5% of West Africa's refined petroleum products market share in 2025; LPG is forecast to register the fastest 7.3% CAGR to 2031.

- By sulfur content, high-sulfur fuels captured 54.9% share of the West Africa refined petroleum products market size in 2025, while low-sulfur grades are poised for a 6.2% CAGR through 2031.

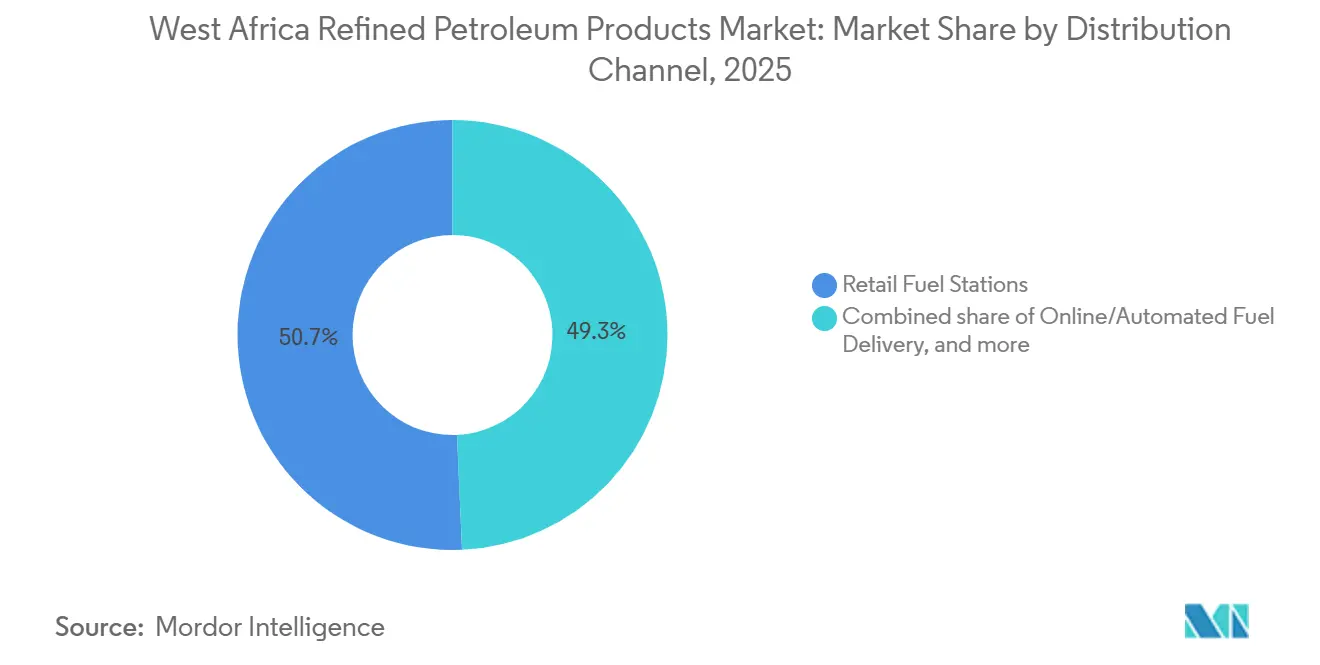

- By distribution channel, retail fuel stations controlled 50.7% of 2025 volume; online and automated delivery platforms are expanding at a 7.8% CAGR to 2031.

- By end-use sector, transportation accounted for a 60.1% share of the West Africa refined petroleum products market size in 2025, and petrochemicals are set to grow at a 6.5% CAGR through 2031.

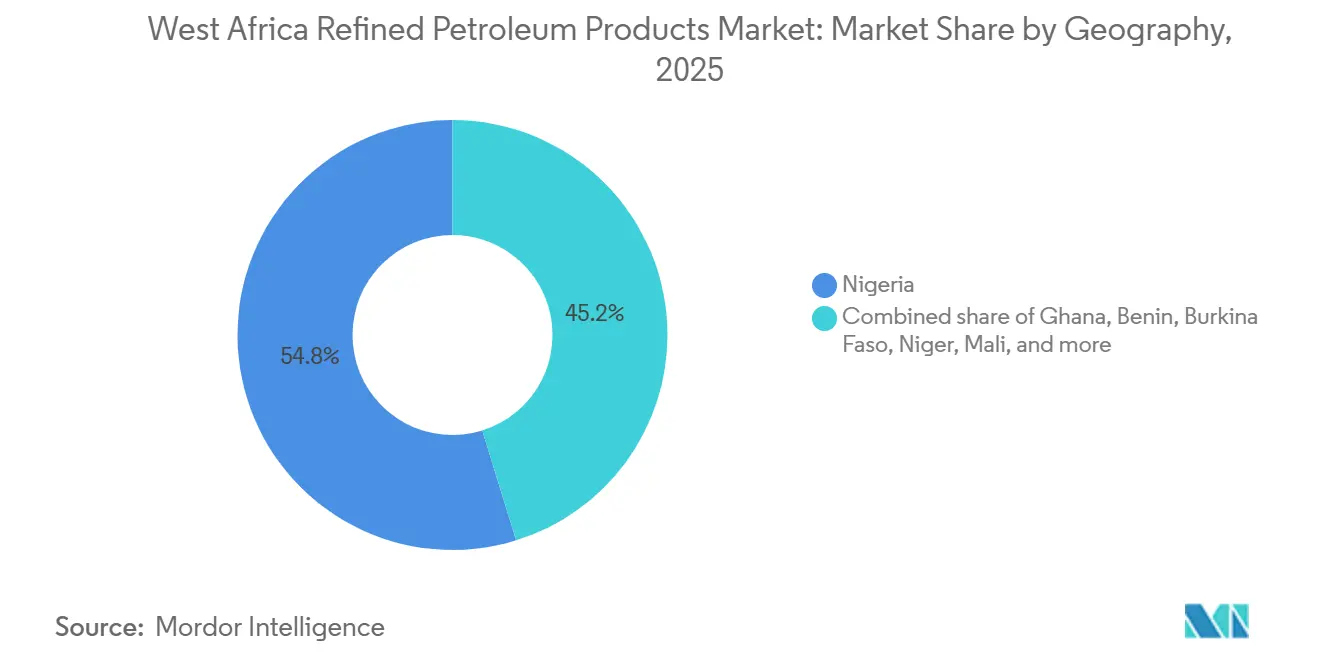

- By geography, Nigeria commanded 54.8% of regional demand in 2025, whereas Niger is projected to post the highest 6.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

West Africa Refined Petroleum Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle-fleet fuel demand | +1.2% | Nigeria, Ghana, Côte d'Ivoire | Medium term (2-4 years) |

| Deregulation & subsidy phase-out attracting investment | +1.5% | Nigeria, with spillover to Benin, Niger | Short term (≤ 2 years) |

| High import reliance due to refinery deficits | +0.8% | Benin, Burkina Faso, Mali, Niger | Long term (≥ 4 years) |

| Modular refinery build-out enabling intra-regional trade | +0.9% | Nigeria, Niger, with cross-border flows to francophone markets | Medium term (2-4 years) |

| Offshore bunkering hubs growth (Ghana, Côte d'Ivoire) | +0.6% | Ghana, Côte d'Ivoire, regional coastal shipping | Medium term (2-4 years) |

| Digital fuel-payment adoption at retail forecourts | +0.4% | Nigeria (Lagos, Abuja), Ghana (Accra), urban corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle-Fleet Fuel Demand

Vehicle registrations keep climbing as urbanization and ride-hailing services spread across Lagos, Accra, and Abidjan. Commercial fleets endured diesel and petrol price jumps exceeding 400% between 2023 and 2026, yet maintained mileage by passing fuel costs to end users. By contrast, price-sensitive households are switching to LPG and CNG, helped by Lagos-based conversion schemes that cut per-kilometer costs by roughly 70% compared with petrol.[1]Presidential CNG Initiative, “Roadmap for gas-powered mobility,” pi-cng.gov.ng As a result, the West Africa refined petroleum products market continues to depend on diesel for logistics even as gasoline growth moderates. Ghana’s 385 million-liter product exports in 2024 underscored its re-export role to landlocked Sahel states. This divergence suggests sustained commercial demand but softer consumer gasoline throughput over the forecast horizon.

Deregulation & Subsidy Phase-Out Attracting Investment

Nigeria redirected more than USD 5 billion in yearly fiscal savings after scrapping fuel subsidies in 2023, clearing headroom for private downstream projects. Dangote Refinery secured naira-denominated crude supply, shielding operations from dollar scarcity that stalled state refineries. International marketers such as TotalEnergies lifted their network count to about 540 outlets by 2024, while Mobil Oil Nigeria committed NGN 100 billion to station automation and digital payments. Regional traders in Benin and Niger have begun signing direct Dangote off-take deals, trimming supply-chain costs up to 20%.[2]Economic Community of West African States, “Harmonized downstream policy framework,” ecowas.int Nonetheless, the absence of a transparent pricing formula fuels spot-market volatility, obliging distributors to carry larger working-capital buffers.

High Import Reliance Due to Refinery Deficits

Landlocked Benin, Burkina Faso, Mali, and Niger still import most refined fuels via coastal depots, exposing them to freight surcharges and currency swings. Import dependence is forecast to dent long-run West Africa refined petroleum products market growth until new regional capacity comes online. Persistent deficits also spur informal cross-border trade, widening tax leakages that erode state revenues earmarked for infrastructure. Governments are therefore fast-tracking port and storage expansions, although execution delays keep import reliance stubbornly high.

Modular Refinery Build-Out Enabling Intra-Regional Trade

Compact 5,000–12,000 barrel-per-day plants in Imo State and northern Nigeria bypass congested ports and deliver fuels within 200 kilometers at costs 10%–15% below Apapa-cleared cargoes. Niger is leveraging these hubs through formal supply contracts that curb smuggling and customs losses. Additional LPG storage, projected at 700,000 metric tonnes by 2040, will co-locate with modular bottling plants, accelerating penetration in underserved Sahel households. Together, these shifts broaden intra-regional trade corridors and temper logistics premiums in the West Africa refined petroleum products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility & currency depreciation | -1.1% | Nigeria, Ghana, with spillover to CFA franc zones | Short term (≤ 2 years) |

| Port, pipeline & storage infrastructure bottlenecks | -0.9% | Nigeria (Apapa, Tin Can), Benin (Cotonou), regional corridors | Medium term (2-4 years) |

| Early shift to alternative fuels & e-mobility in capitals | -0.5% | Lagos, Accra, Abidjan urban centers | Long term (≥ 4 years) |

| Carbon-intensity rules (IMO 2020, ECOWAS drafts) | -0.4% | Coastal bunkering hubs, regional marine corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility & Currency Depreciation

The naira weakened from NGN 460 per USD in 2023 to NGN 1,675 per USD by January 2026, pushing petrol prices near NGN 1,030 per liter and compressing household purchasing power. NNPC accrued roughly USD 6 billion in arrears by September 2024, pivoting to crude-for-product swaps that fix exchange rates but curtail price flexibility. Dangote temporarily undercut retail benchmarks at NGN 899.50 per liter in 2024, yet the razor-thin margin discouraged station upgrades and expansions. Similar depreciation pressures shook the Ghanaian cedi and widened euro-naira mismatches under Benin’s CFA peg, complicating hedging strategies for importers. Such volatility deters long-term contracting in the West Africa refined petroleum products market.

Port, Pipeline & Storage Infrastructure Bottlenecks

Apapa and Tin Can Island handle over 70% of Nigeria’s seaborne fuel, yet vessel turnaround averages 21 days versus a regional norm of seven, saddling importers with daily demurrage of USD 15,000–25,000.[3]Nigerian Ports Authority, “Monthly port performance report,” npa.gov.ng Inland, the 330-kilometer System 2B pipeline runs below 40% capacity due to vandalism, forcing truck haulage that adds NGN 20 per liter to inland prices.[4]Nigerian National Petroleum Company, “Downstream operations update,” nnpcgroup.com Cotonou’s tank farms offer 150,000 cubic meters against a 300,000-cubic-meter need, triggering seasonal shortages in the Sahel. Ghana’s USD 12 billion Nawule hub will ease regional tightness after 2028, but interim bottlenecks stunt throughput, limiting overall West Africa refined petroleum products market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diesel Anchors, LPG Accelerates

Diesel accounted for 35.5% of the 2025 market, underpinned by logistics fleets and back-up power generation where grid reliability stands below 60%. Such resilience ensures diesel remains the commercial backbone of the West Africa refined petroleum products market over the forecast horizon. At the same time, Dangote dedicates more than 60% of export barrels to diesel and fuel oil, benefiting from European winter demand peaks. However, domestic gasoline growth is moderating as Oando’s petrol imports fell to zero cargoes in the first nine months of 2025 after Dangote met 60% of Nigeria’s needs.

LPG is set to expand at a 7.3% CAGR, the fastest among product types, as Nigeria targets 15 million metric tonnes annually by 2030 and Ghana eyes 50% household penetration. Subsidized cylinder programs and new bottling plants, such as Puma Energy’s Tema facility processing 1,200 cylinders per hour, are unlocking residential adoption. Kerosene usage is retreating, while aviation fuel enjoys steady uplift from new routes at Lagos, Accra, and Abidjan. Bitumen and naphtha volumes rise in tandem with infrastructure and petrochemical projects, hinting at a broader downstream diversification within the West Africa refined petroleum products market.

By Sulfur Content: Transition Underway, High-Sulfur Persists

High-sulfur fuels retained a 54.9% share in 2025, reflecting legacy generators and simple topping refineries. Yet low-sulfur products are on a 6.2% CAGR trajectory to 2031 as IMO 2020 and ECOWAS rules tighten emission limits. Global marine demand moved to a 75% VLSFO-dominant mix by 2025, stimulating tank upgrades in Takoradi and Abidjan to accommodate cleaner grades. Dangote’s hydrocrackers now output Euro-V gasoline and 10-ppm diesel, capturing premium export differentials while meeting domestic quality mandates.

Scrubber-equipped vessels still lift high-sulfur fuel oil, mainly destined for Nigerian and Ghanaian power plants where environmental tariffs remain low. Modular refineries lacking secondary conversion generate higher-sulfur outputs that circulate inland, where enforcement is softer. Over time, policy pressure and rising access to cleaner barrels will tilt the West Africa refined petroleum products market toward lower-sulfur blends, although a complete phase-out remains years away, given installed asset profiles.

By Distribution Channel: Retail Dominates, Digital Gains

Retail outlets commanded 50.7% of 2025 deliveries, led by TotalEnergies’ roughly 540 Nigerian stations and Mobil’s 200 Mobil-branded outlets. These networks anchor brand visibility and offer ancillary services such as lubricants and convenience retailing, cementing their role in the West Africa refined petroleum products market. Margins, however, narrowed to NGN 20–30 per liter after Dangote’s December 2024 pricing undercut NNPC benchmarks, pressuring operators to automate and diversify revenue streams.

Online and automated delivery platforms are scaling at a 7.8% CAGR, propelled by fintech uptake that lets fleets order fuel via mobile apps and receive same-day drop-offs. Start-ups in Lagos and Accra deploy GPS-tracked mini-tankers, eliminating queue times. Bulk contracts with mines and factories remain indispensable, but require credit insurance beyond the reach of small independents. Regulatory demands for a 1-million-liter minimum storage capacity further consolidate market power among vertically integrated players, reshaping competitive contours of the West Africa refined petroleum products industry.

By End-Use Sector: Transportation Leads, Petrochemicals Surge

Transportation absorbed 60.1% of 2025 volumes, reflecting heavy truck traffic on the Abidjan–Lagos corridor and booming ride-hailing fleets. Diesel retention in this segment safeguards baseline demand for the West Africa refined petroleum products market even during price spikes. Power-generation fuel oil persists as a stopgap in Nigeria, where industries self-generate up to 60% of electricity.

Petrochemicals will grow at a 6.5% CAGR to 2031 as Dangote’s polypropylene and naphtha units come online, supplying feedstock for packaging, textiles, and auto parts. Residential and commercial users transition from kerosene to LPG, supported by safety-verified cylinders and targeted subsidies. Agriculture and mining uphold steady diesel draws, while marine bunkering gains from revamped low-sulfur standards at Takoradi and Abidjan. Together, these shifts broaden end-use diversity and stabilize overall consumption patterns within the West Africa refined petroleum products market.

Geography Analysis

Nigeria held 54.8% of regional demand in 2025 on the back of a population of 220 million and a dense vehicle fleet. The West Africa refined petroleum products market size in Nigeria alone benefited from Dangote, covering 60% of petrol needs by mid-2025, trimming annual import bills by up to USD 30 billion. Yet subsidy removal and a weaker naira lifted pump prices to nearly NGN 1,030 per liter by 2026, straining household budgets and accelerating CNG conversions under the 1-million-vehicle initiative. Modular refineries like Waltersmith’s plant in Imo State, expanding to 10,000 barrels per day in 2025, offer inland supply at 10%–15% lower landed cost versus coastal depots.

Ghana and Côte d’Ivoire are emerging as bunkering and re-export pivots. Takoradi’s 13.5 million-liter marine gas-oil farm and Bunker Partner’s Africa Star 1 barge in Abidjan are funneling VLSFO to vessels rerouted from the Red Sea. Ghana’s 385 million-liter exports in 2024 highlight its gateway role, while the USD 12 billion Nawule hub, set for 2028 completion, will add 300,000 barrels per day of refining and 3 million cubic meters of storage, reinforcing Ghana’s processing stature. Côte d’Ivoire’s USD 950 million China Exim-financed terminal handled 40 million tonnes of cargo in 2024, spurring lubricant and bunker demand.

Niger’s 6.4% CAGR through 2031 tops the region as formal cross-border trade replaces smuggling, enabled by modular supply links from northern Nigeria. Benin’s Cotonou port faces tank-farm shortfalls that trigger Harmattan-season shortages, but expansion plans are underway. Burkina Faso and Mali rely on over-the-road supply via Abidjan and Cotonou, with security risks inflating logistics premiums. Smaller coastal states, Togo, Liberia, Sierra Leone, and Gambia, remain marginal but stand to benefit from harmonized ECOWAS fuel-quality standards aimed at smoothing intra-regional trade barriers.

Regulatory Landscape

Downstream rules across West Africa are tightening around market governance, fuel quality, and fiscal measures as the region absorbs the impact of large-scale refining additions. In Nigeria, Petroleum Industry Act (PIA) implementation has been reinforced through the Midstream and Downstream Petroleum Operations Regulations (2025), applied in early 2026 to consolidate prior instruments and clarify licensing and compliance expectations for operators under the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA). Nigeria also began enforcing a 0.5% levy on the wholesale price of petroleum products and natural gas in January 2026, adding a transparent charge into wholesale pricing in a deregulated environment.

Governments are also using policy tools to manage price conduct while preserving import channels for supply security. In June 2026, Nigeria directed the NMDPRA to curb profiteering by oil marketers, pointing to closer scrutiny of retail and wholesale practices after subsidy reforms. In July 2026, Nigeria authorized a 15% ad-valorem import duty on petrol and diesel to encourage domestic refining and influence import economics. In Ghana, the National Petroleum Authority (NPA) removed fuel and LPG price discounts effective March 16, 2026 to enforce uniform pricing practices. The draft NPA Bill under discussion proposes governance changes, including new sector funds (Distribution Fund and Infrastructure Fund) and adjustments to how margins are managed, which would affect downstream cashflows and infrastructure financing.

Competitive Landscape

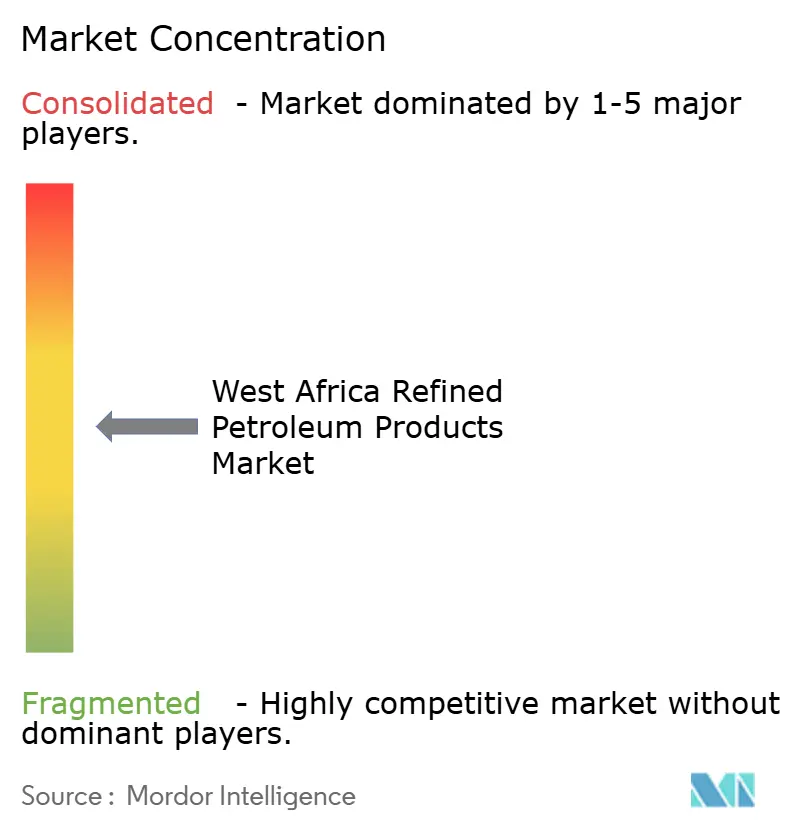

The West Africa refined petroleum products market is moderately fragmented. Global trading houses, Vitol, Trafigura, Mercuria, and Gunvor, move the bulk of Dangote’s approximately 6 million tonnes of product exports, leveraging sophisticated charter fleets and trade-credit lines. Regional players Sahara Group, Oando, and Puma Energy focus on storage and retail distribution, with Oando shifting to crude exports after petrol arbitrage vanished post-Dangote startup. TotalEnergies, maintaining about 540 Nigerian outlets, coupled with upstream portfolio pruning, will undergo downstream expansion by signing a multi-product off-take pact with Dangote in 2024.

Vertical integration is intensifying. TotalEnergies picked up a 50% operated stake in OPL257 in 2025 and sold 12.5% of Bonga to Shell and Agip for USD 510 million, aiming to boost gas-based LNG feedstock security. Oando’s 2023 acquisition of Nigerian Agip Oil Corporation doubled its reserves to 503 million barrels of oil equivalent but sidelined its legacy refined-product import unit. Digital payment rails under WAEMU level the playing field for smaller marketers, letting them compete on transaction speed rather than balance-sheet heft.

White-space opportunities lie in LPG cylinder distribution, low-sulfur bunkering, and automated last-mile delivery. Regulatory hurdles abound: Nigeria’s downstream authority now mandates 1-million-liter minimum storage for retail licenses, a threshold favoring entrenched firms. Nonetheless, modular refineries with local-content funding, such as Waltersmith’s 30% NCDMB stake, show alternative ownership models that large multinationals cannot easily replicate without ceding control. Collectively, these shifts are redrawing competitive lines within the West Africa refined petroleum products market.

West Africa Refined Petroleum Products Industry Leaders

Trafigura Group Pte Ltd

Vitol Holding BV

Sahara Group Ltd

NNPC Trading Ltd

TotalEnergies Marketing Nigeria PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Rising regional processing capacity and fuel-quality compliance requirements are creating investable whitespace in storage, blending, and distribution for cleaner products, particularly around middle distillates and low-sulfur marine fuels. Dangote Refinery has been an anchor: in June 2026, it completed a licensor performance test at 700,000 bpd, above its 650,000 bpd nameplate, strengthening the case for new short-haul coastal redistribution and ship-to-ship (STS) logistics via hubs such as Lome. As more barrels originate within the region, opportunities are concentrated in coastal tankage upgrades in bunkering corridors (Ghana and Côte d'Ivoire), which need segregation and handling for VLSFO and 10-ppm diesel. There is also growing demand for digital ordering and automated delivery models that reduce forecourt congestion for fleets.

New and expanding refineries across the broader West Africa supply basin are opening equipment, services, and offtake-led partnership opportunities tied to higher-spec output. In Ghana, Phase 2 of the Sentuo Oil Refinery project in Tema was launched in June 2026, targeting an increase in capacity from 40,000 bpd to 100,000 bpd, supporting more local supply and structured export ambition to neighboring markets through formal channels. Technology-led upgrades aimed at producing lower-sulfur fuels are also supporting demand for catalysts, hydrotreating, and hydrocracking services, along with compliant logistics. For example, Technip Energies received FEED contracts in April 2026 from SOGARA to modernize and expand the Port-Gentil refinery, including a modularized hydrocracker complex aligned with Africa 5 fuel-quality direction. These developments are shifting procurement from import-dependent spot buying toward regionally sourced supply, with value capture hinging on incremental investment in terminals, truck-loading gantries, cylinder and LPG bottling infrastructure, and credit-enabled B2B distribution.

Recent Industry Developments

- June 2026: Dangote Refinery completed a licensor performance test at 700,000 bpd, surpassing its original 650,000 bpd design capacity. The milestone strengthened confidence in higher-throughput operations and increased the availability of regionally sourced refined products for coastal redistribution. It also sharpened competitive pressure on import-linked supply chains as more volumes originate from within West Africa.

- October 2025: Senegal announced the start of construction for its second oil refinery, with the national refining company SAR citing an investment range of USD 2-5 billion. The project signals a push to raise domestic processing capability and reduce reliance on imported refined products. It also adds momentum to regional capacity additions that can reshape trade flows across Francophone West Africa.

- August 2024: Ghana started the first phase of its USD 12 billion petroleum hub in Nawule, Jomoro, planned to include refining, petrochemical plants, and large-scale storage. Early works on the hub underline Ghana's strategy to deepen its role as a regional re-export and bunkering gateway. The project also supports downstream opportunities in terminals, logistics, and fuel-quality compliant storage as the buildout progresses.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of refined petroleum products supplied and consumed across West Africa, covering major fuels and refinery outputs sold through retail and bulk channels to end users.

Scope exclusions: Excludes crude oil production and excludes standalone midstream transport and storage services unless the value is embedded in the delivered refined product price.

Segmentation Overview

- By Product Type

- Petrol (Gasoline)

- Diesel

- LPG

- Kerosene

- Aviation Fuel

- Fuel Oil (HSFO, VLSFO)

- Others (Bitumen, Naphtha)

- By Sulfur Content

- Low-Sulfur (Up to 10 ppm)

- High-Sulfur (Above 10 ppm)

- By Distribution Channel

- Retail Fuel Stations

- Commercial Bulk Sales

- Direct Supply Contracts

- Online/Automated Fuel Delivery

- By End-Use Sector

- Transportation

- Power Generation

- Industrial Manufacturing

- Petrochemicals

- Residential and Commercial

- Marine and Bunkering

- Agriculture and Mining

- By Geography

- Nigeria

- Ghana

- Benin

- Burkina Faso

- Niger

- Mali

- Rest of West Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research begins by building a consistent fact base using refined product availability and demand signals across West Africa. We rely on public datasets such as OPEC and IEA statistical releases, EIA country briefs, UN Comtrade trade statistics, and World Bank macro indicators to map imports, consumption direction, and price context.

To tighten assumptions, we also use national statistics office releases and central bank bulletins in key markets, port authority throughput updates, and customs or revenue agency publications where available. Company filings, investor presentations, and reputable press are then used to cross-check refinery utilization, product availability, and policy moves (such as subsidy reforms and fuel quality rules). For a few hard-to-observe elements like shipment timing and product mix shifts, selective paid subscriptions support company financials and intelligence, with additional import and export shipment-level checks. These sources are not exhaustive, and we used other public references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys help confirm product mix, channel margins, and how quickly price changes flow through to volumes. We speak with refiners and importers, bulk distributors, retail fuel networks, logistics intermediaries, and large end users across transport, power generation, and industrial use. We re-check insights across coastal import hubs and landlocked corridors so the assumptions stay grounded in how supply actually reaches each geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 55% | Functional/Unit leaders: 39% | |

| Smaller Players: 14% | Managers: 47% |

Market-Sizing & Forecasting

Sizing is built with a top-down and bottom-up blend. We start by reconstructing country supply balances that combine refinery output, net imports, and stock movement direction, then we value the balances using representative price series. After the first pass, we run targeted bottom-up checks, such as sampled station throughput tied to average retail prices, distributor volume indications, and bulk delivery channel checks, and we adjust totals only when those evidence lines align.

Key inputs used in the model include refinery throughput and utilization direction, seaborne import dependency by product, local currency to USD conversion timing, regulated versus deregulated pricing behavior, and demand pull from road transport and power generation. When product splits are not directly observable, shares are inferred using trade codes, refinery configuration clues, and interview-led validation, then the final mix is checked against known substitution patterns between fuels. Forecasts rely on scenario analysis anchored on macro growth, visibility on subsidies and price caps, and expected changes in refining capacity and import logistics, with expert feedback used to keep price and volume paths consistent.

Data Validation & Update Cycle

Validation is handled through multiple checks that compare model outputs with independent signals, such as the import bill direction, reported fuel tightness periods, and refinery operating updates that can shift product availability. When large variances show up, we review assumptions, challenge outliers, and trigger targeted re-contacts so the final numbers do not depend on a single input.

Before sign-off, reviews happen in steps, first at the assumption level and then at country and regional totals, so inconsistencies are corrected early. Reports are refreshed annually, and interim updates are made when material events occur, such as major pricing reforms, large refinery start-ups, or prolonged supply disruptions. Right before delivery, we complete a fresh pass so clients receive the latest updated view.

Mordor Intelligence's West Africa Refined Petroleum Products Market Size Compared With Other Published Estimates

Published market values for this space can look far apart, even when the geography sounds similar, because the product basket and the pricing basis are not always aligned. The gaps also come from how import dependence is treated, whether informal cross-border flows are implicitly assumed, and how currency conversion and inflation are applied in year-by-year value builds.

Some published figures use a narrower fuel-only set or a smaller country list, and some blend adjacent downstream items into the same total without showing the split. For Mordor Intelligence, the value is built from country supply balances for the refined fuel slate, and items like standalone midstream services and non-fuel downstream categories are kept outside scope unless they are explicitly counted as refined products in the balance.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 61.96 B (2026) | |

| Trade Publisher A | USD 10.20 B (2025) | Uses a narrower country set and a product grouping that can undercount bulk and industrial demand, and the value build may lean on selected retail-linked prices rather than a full country supply-balance valuation. |

| Global Consultancy B | USD 55.86 B (2024) | Anchors on an earlier base year and can blend additional downstream items into the refined products total, and the treatment of regulated pricing, FX timing, and subsidy pass-through is not clearly stated which can shift USD values. |

The table shows that differences mainly come from what is included in the refined product basket, the country coverage, and how volumes are paired with prices over time. With a supply-balance build and practical interview checks on product mix and channel behavior, we keep the estimate traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the West Africa refined petroleum products market in 2026?

The West Africa refined petroleum products market size stands at USD 61.96 billion in 2026 and is forecast to hit USD 78.62 billion by 2031.

What is driving LPG demand growth in West Africa?

Government targets of 15 million metric tonnes annual LPG use in Nigeria and 50% household penetration in Ghana are pushing LPG toward a 7.3% CAGR through 2031.

Which country is expanding refining capacity the fastest?

Nigeria is adding the most capacity, led by the 650,000-barrels-per-day Dangote refinery and several modular plants that collectively slash import dependence.

Why are low-sulfur fuels gaining traction in coastal West Africa?

IMO 2020 rules and forthcoming ECOWAS sulfur standards compel bunkering hubs in Ghana and Côte d’Ivoire to stock VLSFO and 10-ppm diesel, driving infrastructure upgrades.

What is the main risk to fuel distributors in Nigeria?

Currency volatility that pushed petrol prices above NGN 1,000 per liter squeezes retail margins and complicates hedging, deterring long-term supply contracts.

Page last updated on: