Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

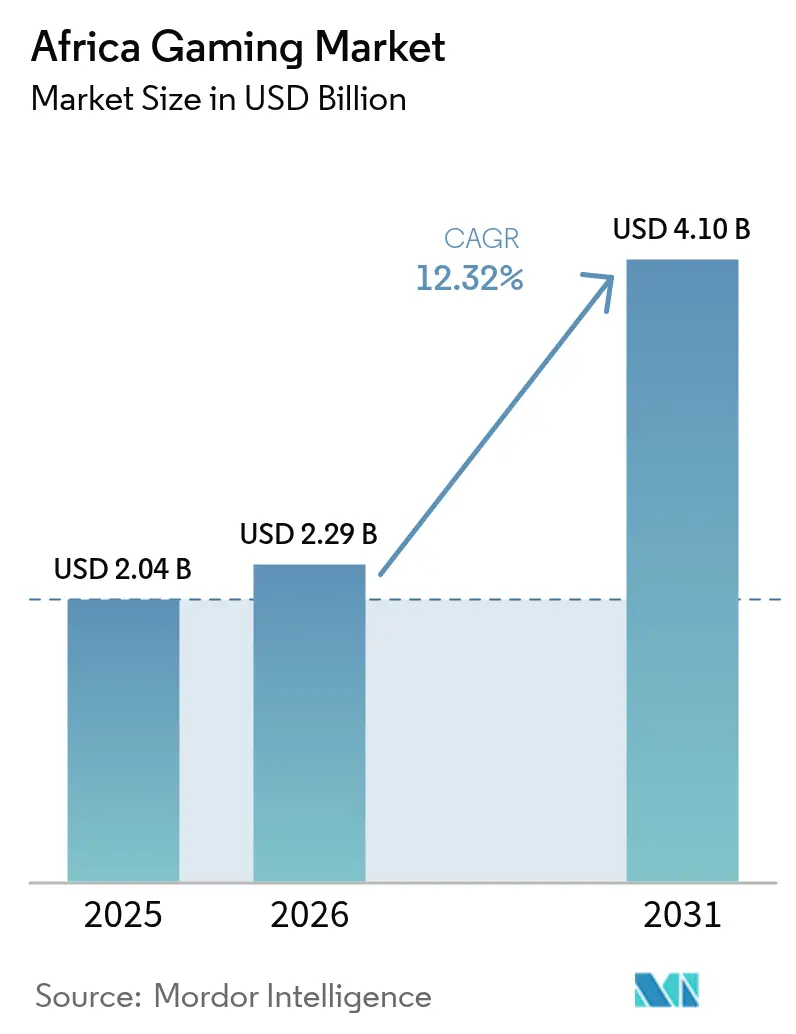

| Base Year Market Size (2025) | USD 2.04 Billion |

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 4.1 Billion |

| Growth Rate (2026 - 2031) | 12.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Gaming Market Analysis by Mordor Intelligence

Africa Gaming Market size in 2026 is estimated at USD 2.29 billion, growing from 2025 value of USD 2.04 billion with 2031 projections showing USD 4.10 billion, growing at 12.32% CAGR over 2026-2031.

The ecosystem’s upward curve rests on smartphone ubiquity, fintech-enabled micro-transactions, and expanding edge-data-center capacity that shortens latency for cloud services. Mobile titles already supply nearly 90% of revenue, but cloud delivery is poised to reshape platform dynamics as infrastructure investments from Microsoft, Sony, and regional telcos come online. Local studios capitalize on cultural storytelling to engage first-time gamers, and international publishers reinforce that content pipeline through equity stakes and co-development deals. Regulatory decisions such as South Africa’s decision to drop the 9% excise duty on low-cost handsets underscore policy momentum toward digital inclusion. [1]Paula Gilbert, “South Africa Plans to Stop Import Tax on Low-Cost Smartphones,” connectingafrica.com Headwinds persist in the form of inconsistent power supply, hardware tariffs, and fragmented intellectual-property enforcement, yet momentum in e-sports leagues and fintech innovation offsets many structural risks.

Key Report Takeaways

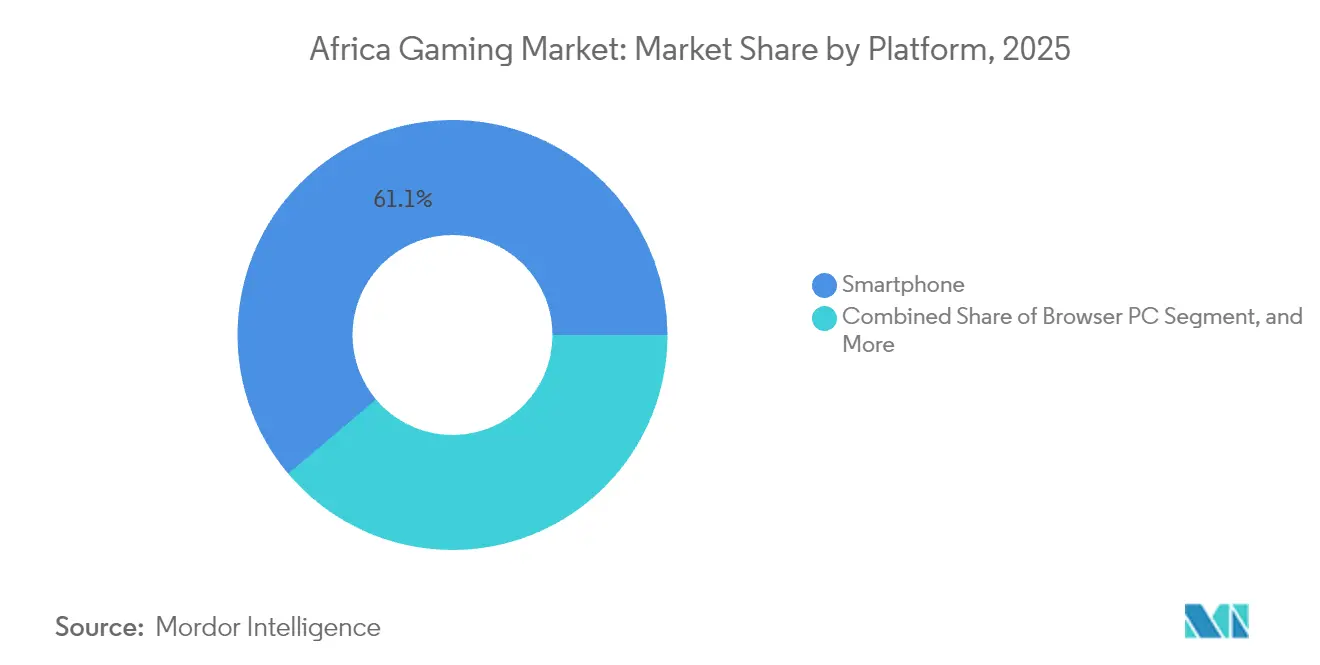

- By platform, smartphones led with 61.15% revenue share of the Africa gaming market in 2025, while cloud gaming is forecast to expand at a 13.72% CAGR through 2031.

- By game genre, action/adventure commanded 33.05% of the Africa gaming market share in 2025, whereas MOBA titles are advancing at a 13.28% CAGR to 2031.

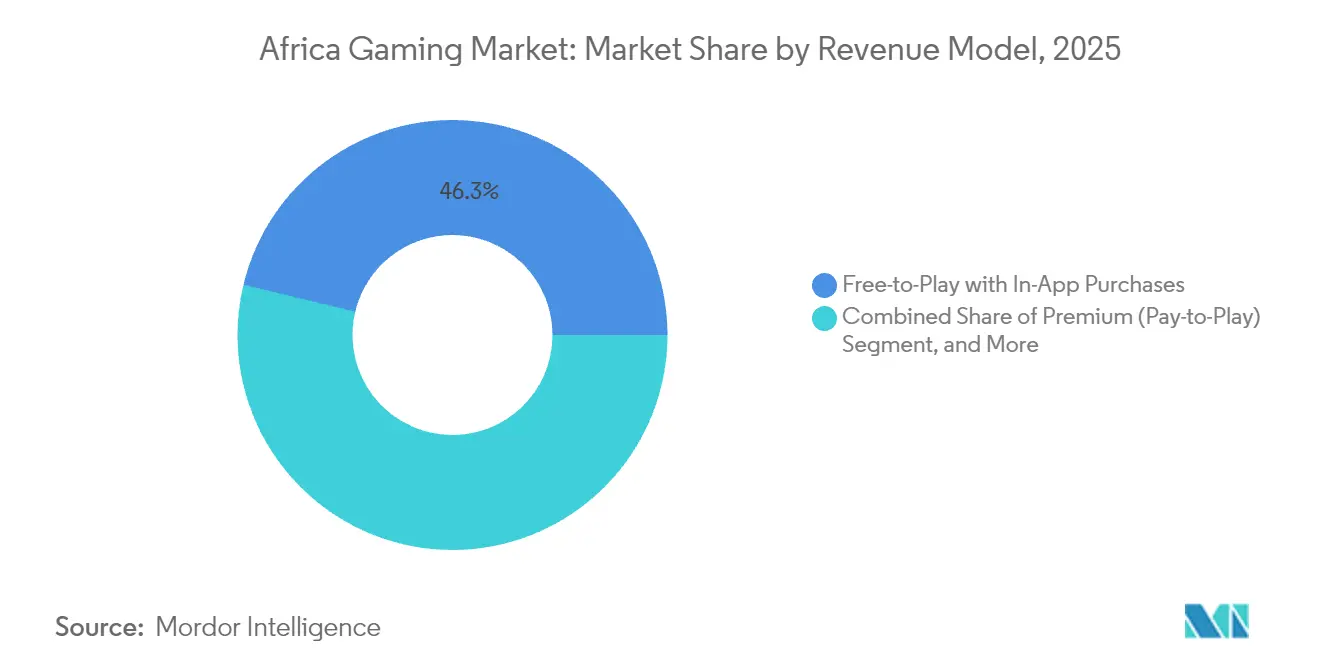

- By revenue model, free-to-play with in-app purchases accounted for 46.25% of the Africa gaming market size in 2025; subscription services are projected to grow at a 13.52% CAGR.

- By gamer demographics, the 18-35 cohort represented 51.85% of gamers of the Africa gaming market in 2025, while the under-18 segment is set to grow at a 13.01% CAGR.

- By country, Nigeria held 27.10% of the 2025 revenue of the Africa gaming market, but Kenya is pacing the region with a 12.96% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging smartphone penetration and affordable data plans | +3.2% | Global, with strongest impact in Nigeria, Kenya, Egypt | Medium term (2-4 years) |

| Increasing localisation of content and language support | +1.8% | Nigeria, South Africa, Kenya, Ghana | Long term (≥ 4 years) |

| Expansion of mobile-money and fintech micro-transactions | +2.5% | Kenya, Tanzania, Uganda, Nigeria | Short term (≤ 2 years) |

| Government e-sports initiatives and national leagues | +1.4% | Rwanda, Ghana, Nigeria, South Africa | Medium term (2-4 years) |

| Cloud-gaming infrastructure roll-outs (edge data centres) | +2.1% | South Africa, Nigeria, Kenya, Egypt | Long term (≥ 4 years) |

| Africa-specific ad-tech platforms boosting F2P monetisation | +1.5% | Nigeria, South Africa, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Smartphone Penetration and Affordable Data Plans

Shipments climbed 6% year-on-year to 19.4 million units in Q1 2025, with North Africa recording 34% growth. [2]TelecomLead Editors, “Africa's Smartphone Market in Q1-2025 Shows Tentative Optimism,” telecomlead.com TRANSSION continues to command a 47% share, reflecting its mastery of entry-level pricing that aligns with local income levels. More than 95% of the continent’s 349 million gamers play on mobile, reinforcing the platform’s primacy. The proliferation of 4G-enabled phones, 85% of total shipments, elevates user readiness for data-heavy titles. A median age below 20 ensures a pipeline of digital natives that treat mobile gaming as a primary entertainment outlet rather than an occasional pastime.

Increasing Localisation of Content and Language Support

Disney’s “Iwájú” partnership with Nigeria’s Maliyo Games marks a watershed as global IP leans on African storytelling for authenticity. Localization studies show 76% of consumers prefer experiences in their native language, and the continent’s 3,000 cultures make cultural resonance a decisive retention lever. Kiro’o Games’ milestone Xbox launch illustrates the pay-off: culturally grounded titles enjoy longer session times and higher conversion rates. French, Arabic, and Swahili versions widen addressable audiences, while vernacular voice-overs enrich narrative immersion. Studios that master cultural nuance secure stronger monetization metrics and attract cross-media licensing.

Expansion of Mobile-Money and Fintech Micro-Transactions

M-Pesa processed USD 314 billion in annual value for 51 million clients, establishing a continental payment backbone for one-click in-game purchases. Micro-transaction baskets averaging USD 0.25 fit local buying power and vault conversion rates relative to credit-card gateways. M-Pesa’s China link via Thunes unlocks cross-border potential that can extend African IP to Asian gamers. Subscription models benefit too, as consumers become comfortable with recurring mobile debits. Fintech integrations accelerate market entry for overseas publishers, who can launch without traditional banking partnerships.

Government E-Sports Initiatives and National Leagues

Seventeen African federations now belong to the Global Esports Federation, mainstreaming competitive gaming. Ghana’s 2024 federation pact and Rwanda’s dedicated organization offer structured pathways for talent development. Carry1st’s management of Call of Duty: Mobile qualifiers, spanning seven regions with a USD 15,000 purse, signals alignment between local organizers and global circuits. The March 2025 launch of Africa’s dedicated League of Legends server slashes ping times, bolstering spectator appeal. National leagues attract sponsorship from telcos and consumer brands, converting viewership into diversified revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import tariffs on consoles and PC hardware | -2.1% | Kenya, Nigeria, Ghana, with varying impact across markets | Medium term (2-4 years) |

| Persistent electricity reliability issues | -1.8% | South Africa, Nigeria, Ghana, Kenya | Short term (≤ 2 years) |

| Limited local venture funding for studios | -1.3% | Continental, with acute impact in Nigeria, Kenya, Ghana | Long term (≥ 4 years) |

| Patchy enforcement of digital-IP protection laws | -0.9% | Nigeria, Kenya, South Africa, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs on Consoles and PC Hardware

Kenya’s 25% duty plus 16% VAT inflates console prices to multiples of the monthly median income, discouraging adoption. [3]Dutify Insights, “Duty and Tax Rates for Video Game Console,” dutify.com South Africa’s zero-duty console policy, but 15% VAT, highlights regional disparities that fragment addressable demand. Tariffs curtail gaming-café rollouts, limiting community hubs for e-sports qualification events. Hardware cost barriers push consumers toward mobile or cloud alternatives, unintentionally accelerating the Africa gaming market’s post-console trajectory. Government leniency on low-cost handsets hints at potential tariff reconsideration for gaming devices, but timelines remain uncertain.

Persistent Electricity Reliability Issues

Load-shedding schedules routinely interrupt gameplay in South Africa, undermining multiplayer retention metrics. Nigerian home users confront generator costs that erode disposable income for in-game purchases. Data-center investors deploy renewable microgrids to mitigate grid instability, yet capital intensity keeps rack rates elevated. Satellite internet providers like Starlink circumvent terrestrial bottlenecks, offering consistent ping but at premium subscription levels. Studio workflows shift to cloud-based development to reduce on-site compute dependency, but outages still extend build cycles and limit release cadence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Dominance Drives Cloud Transition

Smartphones generated 61.15% of 2025 revenue, underscoring that the Africa gaming market size leans heavily on mobile-first engagement. The Africa gaming market share of smartphones benefits from affordable entry-level devices and zero-rated gaming data offers from telcos. Cloud gaming, however, is scaling fastest at a 13.72% CAGR on the back of hyperscale data-center investment, promising console-grade experiences without hardware imports. Tablets remain niche, catering to educational titles consumed by families. Console uptake lags owing to tariff drag, positioning cloud services as a viable detour around customs costs.

Growth vectors align with telco-OTT bundles that package gaming subscriptions, edge caching that compresses latency, and pay-as-you-go micro-payments that democratize access. Browser PC titles retain traction among urban professionals who game during work breaks, while downloaded PC games confront bandwidth ceilings. As infrastructure matures, cloud platforms may cannibalize high-end PC and console segments, but smartphones will continue to anchor user-acquisition funnels for the Africa gaming market.

By Game Genre: Action Leads, MOBA Accelerates

Action/adventure titles held a 33.05% share in 2025, buoyed by casual control schemes and relatable story arcs drawn from African folklore. MOBA’s projected 13.28% CAGR rides on the March 2025 League of Legends server that removed latency penalties for competitive play. Sports franchises, especially football, sustain consistent monetization through annual roster updates. Shooter/FPS adoption is slower because of high data loads and sociocultural sensitivities to violent themes. Casual puzzle apps excel at onboarding, while simulation games attract mature demographics with strategic depth.

The genre mix illustrates the Africa gaming industry’s maturation: early adopters gravitate to short-session casual play, and rising infrastructure capacity ushers in skill-based competitive formats. Local studios localize mythic narratives, nudging conversion by resonating with cultural archetypes. As competitive gaming prize pools rise, MOBA may overtake action titles in revenue, but action’s evergreen appeal ensures steady floor demand.

By Revenue Model: F2P Dominance, Subscription Growth

Free-to-play with in-app purchases captured 46.25% of the 2025 Africa gaming market size, confirming micro-transaction compatibility with mobile-money wallets. Subscriptions, although only 8.5% of spend, are scaling at 13.52% CAGR, aided by Xbox Game Pass mobile bundles via carrier billing. Premium pay-to-download models face friction from limited card penetration, while in-game advertising fills monetization gaps for non-spenders. E-sports media rights, though nascent, are set to rise as league infrastructures mature.

Developers optimize for lifetime value over upfront sales, segmenting spenders into micro-, mid-, and whale tiers anchored to mobile-money transaction histories. Africa-specific ad-tech unlocks CPM uplift by serving culturally relevant creatives in local languages. As cloud services scale, hybrid models combining subscription access with cosmetic micro-transactions could emerge as the revenue sweet spot for the Africa gaming market.

By Gamer Demographic: Youth Drives, Gen Z Accelerates

The 18-35 cohort provided 51.85% of users and most discretionary spend in 2025, converting cultural nostalgia and competitive pride into sustained ARPDAU. Under-18 gamers, expanding at a 13.01% CAGR, will swell the onboarding pipeline for the next decade, accelerated by smartphone penetration in secondary-school populations. Gamers aged 36-50 favor casual and strategy titles that accommodate intermittent play, while the 50-plus segment remains small but reachable through hyper-casual puzzle apps with large fonts and simple mechanics.

Gender parity trends surface in mature markets such as South Africa, where women now account for 46% of gamers. As younger cohorts age into higher income brackets, their ingrained gaming habits will compound revenue growth. Esports scholarships and STEM-aligned serious games further normalize gaming among parents and educators, opening additional demographic slices.

Geography Analysis

Nigeria delivered USD 553 million in 2025 revenue on the strength of its 220 million-person population and fintech prowess that eases micro-transaction flows. Telecommunications operators bundle zero-rated gaming traffic, deepening engagement even during inflationary cycles. The Nigeria Copyright Commission’s stepped-up IP enforcement foreshadows a friendlier climate for premium launches.

South Africa houses 26.5 million players, a 44% penetration rate that reflects robust broadband and a developer base of roughly 60 studios. Mobile games account for 91% of spend, yet console and PC niches flourish amid higher disposable incomes. Elimination of the 9% handset excise duty in April 2025 further broadens the funnel for entry-level consumers.

Kenya’s 12.96% CAGR stems from the world’s most sophisticated mobile-money network, M-Pesa, and impending hyperscale cloud capacity under the Microsoft-G42 USD 1 billion plan. Regulatory clarity from the Betting Control and Licensing Board enhances investor confidence in game launches. Egypt, leveraging its 111 million residents and cross-regional cultural influence, dominated the USD 0.61 billion 2025 market tally. Algeria and Ghana round out the next cohort, supported by telco fiber roll-outs and nascent e-sports programs. Rest-of-Africa markets such as Rwanda and Tanzania combine youth demographics with policy enthusiasm for digital skilling, setting the stage for second-wave adoption across the Africa gaming market.

Competitive Landscape

The Africa gaming market hosts a mix of bootstrapped studios and multinational heavyweights in a moderately fragmented setting. Carry1st’s USD 27 million Series C, anchored by Sony, demonstrates an appetite for platform publishers that marry fintech integration with culturally tuned hits. Disney’s co-development pact with Maliyo Games underscores global IP’s reliance on local narrative expertise. [4]Jeffrey Rousseau, “Carry1st Receives Investment From Sony,” gamesindustry.biz

International entrants prefer partnership and investment approaches over direct greenfield competition, hedging against regulatory complexity while tapping ready-made cultural insights. Telcos strike content-plus-data bundles with publishers, and satellite providers like Starlink position connectivity as a competitive moat for premium live-service experiences.

Meanwhile, regional independents like Nyamakop and Kiro’o Games leverage government grants and cross-platform engines such as Unity to ship globally viable IP. Competitive advantage pivots on mobile-money integration, localization depth, and community management rather than photorealistic graphics. Overall, the top five revenue-generating companies command roughly 35% combined share, keeping acquisition chatter active but leaving runway for newcomers.

Africa Gaming Industry Leaders

-

Carry1st (Pty) Ltd.

-

Maliyo Games Ltd.

-

Leti Arts Ltd.

-

Kucheza Gaming Ltd.

-

Gamesole Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NIP Group formed a Digital Computing Division through a crypto-mining hardware acquisition to finance its e-sports ecosystem.

- June 2025: pawaTech signed a four-year licensing pact with Choplife Gaming to expand betPawa into Nigeria.

- June 2025: Nyamakop returned with “Relooted,” reinforcing local content momentum.

- May 2025: Carry1st hosted the African qualifiers for the 2025 Call of Duty: Mobile World Championship with a USD 15,000 prize pool.

- April 2025: GamesConnect Africa launched to catalyze pan-African developer collaboration.

- March 2025: Cassava Technologies and Nvidia announced Africa’s first AI factory in South Africa, slated for Jun 2025.

- March 2025: Africa received its dedicated League of Legends server, cutting latency for MOBA gamers.

- February 2025: Equinix opened its first Johannesburg IBX data center, offering 20,000 sq ft of colocation space.

Africa Gaming Market Report Scope

Gaming is referred to as playing electronic games conducted through multiple means, such as computers, mobile phones, consoles, or other mediums. The rising prevalence of high-speed internet connections, especially in emerging economies, has made online gaming practical for more people in recent years. The scope of the research includes mobile, console, and PC browsers and downloaded games.

The African gaming market is segregated by platform (browser PC, smartphone, tablets, gaming console, and downloaded/box PC) and country (Nigeria, Ethiopia, Egypt, Morocco, Kenya, Algeria, and South Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Platform

| Browser PC |

| Downloaded/Box PC |

| Gaming Console |

| Smartphone |

| Tablet |

| Cloud Gaming |

By Game Genre

| Action/Adventure |

| Sports |

| Shooter/FPS |

| MOBA |

| Casual/Puzzle |

| Simulation/Strategy |

By Revenue Model

| Premium (Pay-to-Play) |

| Free-to-Play with In-App Purchases |

| Subscription (Game Pass, Apple Arcade etc.) |

| In-Game Advertising |

| Esports Media and Sponsorship |

By Gamer Demographics

| Age <18 |

| Age 18-35 |

| Age 36-50 |

| Age >50 |

By Country

| Nigeria |

| South Africa |

| Egypt |

| Kenya |

| Algeria |

| Rest of Africa |

| By Platform | Browser PC |

| Downloaded/Box PC | |

| Gaming Console | |

| Smartphone | |

| Tablet | |

| Cloud Gaming | |

| By Game Genre | Action/Adventure |

| Sports | |

| Shooter/FPS | |

| MOBA | |

| Casual/Puzzle | |

| Simulation/Strategy | |

| By Revenue Model | Premium (Pay-to-Play) |

| Free-to-Play with In-App Purchases | |

| Subscription (Game Pass, Apple Arcade etc.) | |

| In-Game Advertising | |

| Esports Media and Sponsorship | |

| By Gamer Demographics | Age <18 |

| Age 18-35 | |

| Age 36-50 | |

| Age >50 | |

| By Country | Nigeria |

| South Africa | |

| Egypt | |

| Kenya | |

| Algeria | |

| Rest of Africa |

Key Questions Answered in the Report

How large is the Africa gaming market in 2026?

The Africa gaming market size stands at USD 2.29 billion in 2026 and is projected to reach USD 4.10 billion by 2031.

Which platform generates most gaming revenue across Africa?

Smartphones contribute 61.15% of total 2025 revenue, reflecting Africa’s mobile-first digital landscape.

What factors drive cloud-gaming adoption on the continent?

Hyperscale data-center investment, edge nodes that cut latency, and tariff-free access to premium content fuel a 13.72% CAGR for cloud gaming.

Which country represents the fastest-growing opportunity?

Kenya leads growth with a 12.96% CAGR forecast through 2031, supported by advanced mobile-money ecosystems and new cloud infrastructure.

Which revenue model is scaling most quickly?

Subscription services are growing at 13.52% CAGR, propelled by carrier-billed bundles that remove payment friction.

What is the main regulatory challenge for publishers?

Divergent import tariffs and inconsistent IP enforcement remain significant hurdles, trimming the sector’s CAGR by an estimated 2.1 percentage points.

Page last updated on: