Africa Biological Organic Fertilizers Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

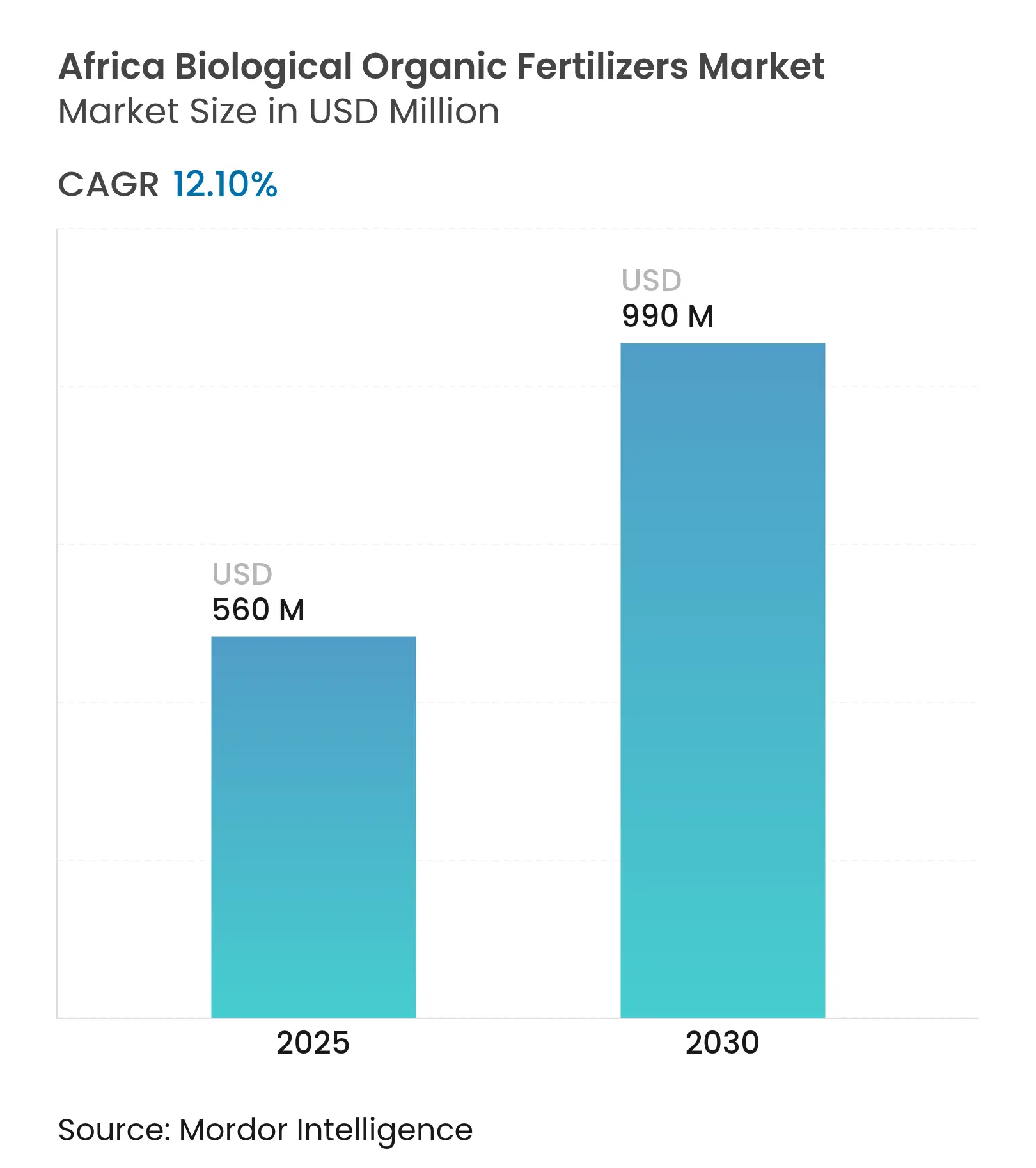

| Market Size (2025) | USD 560 Million |

| Market Size (2030) | USD 990 Million |

| Growth Rate (2025 - 2030) | 12.10 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Africa Biological Organic Fertilizers Market Analysis by Mordor Intelligence

The Africa biological organic fertilizers market size stood at USD 560 million in 2025 and is forecast to advance at a 12.1% CAGR, reaching USD 990 million by 2030. Rising soil degradation on 83% of the continent’s arable land and policy support for agro-ecological practices are steering fertilizer demand toward bio-based solutions. Development finance institutions are increasing capital flows into sustainable inputs, while regional declarations such as the Nairobi Declaration are aligning 54 national strategies behind soil-health investment. Emerging carbon-credit programs, the proliferation of tech-enabled waste-to-fertilizer start-ups, and corporate procurement standards that favor regenerative agriculture are accelerating the transition.

Key Report Takeaways

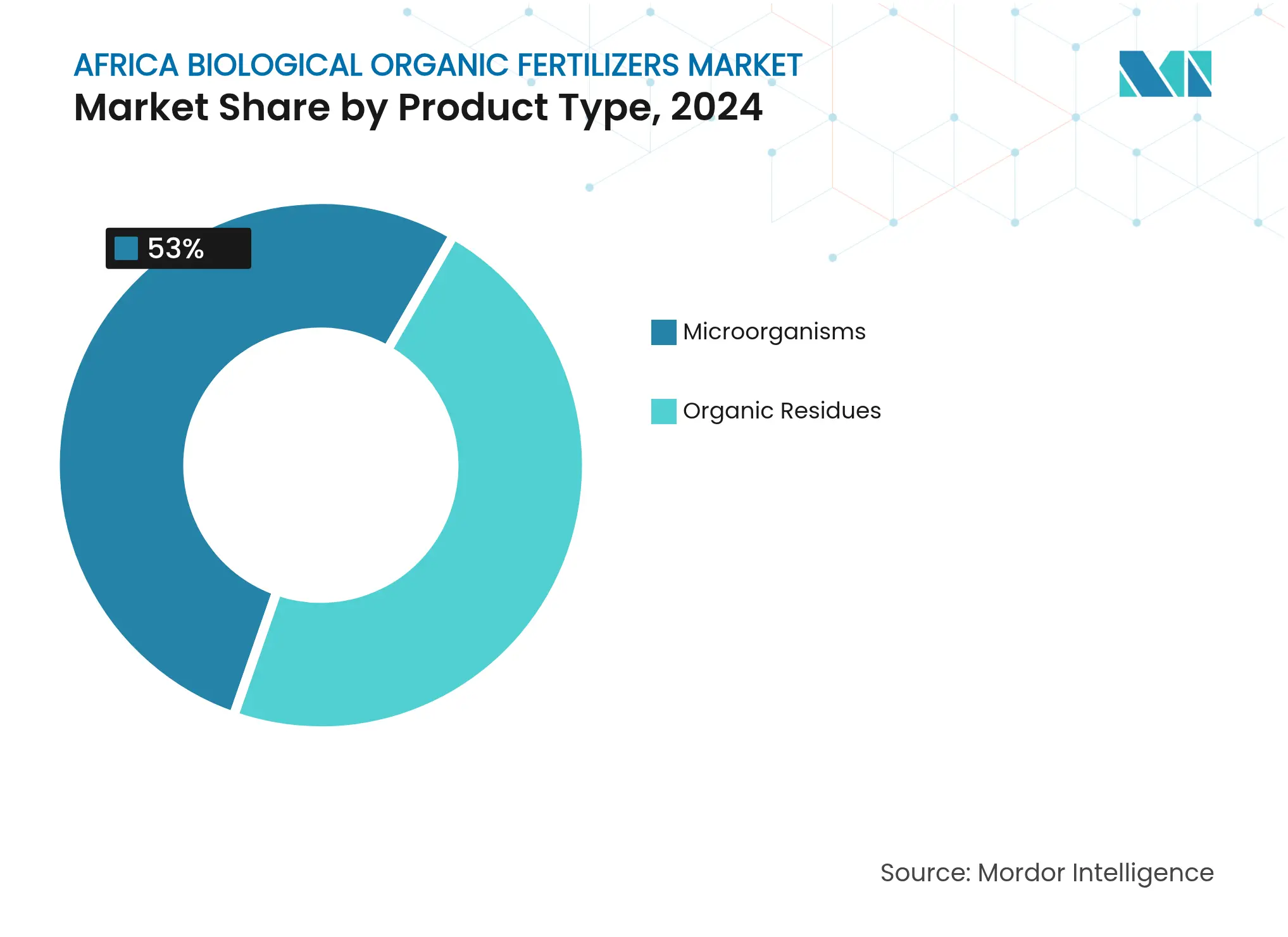

- By product type, organic residues captured 47% of the Africa biological organic fertilizers market share in 2024, and microorganisms are forecast to grow at a 15.6% CAGR to 2030.

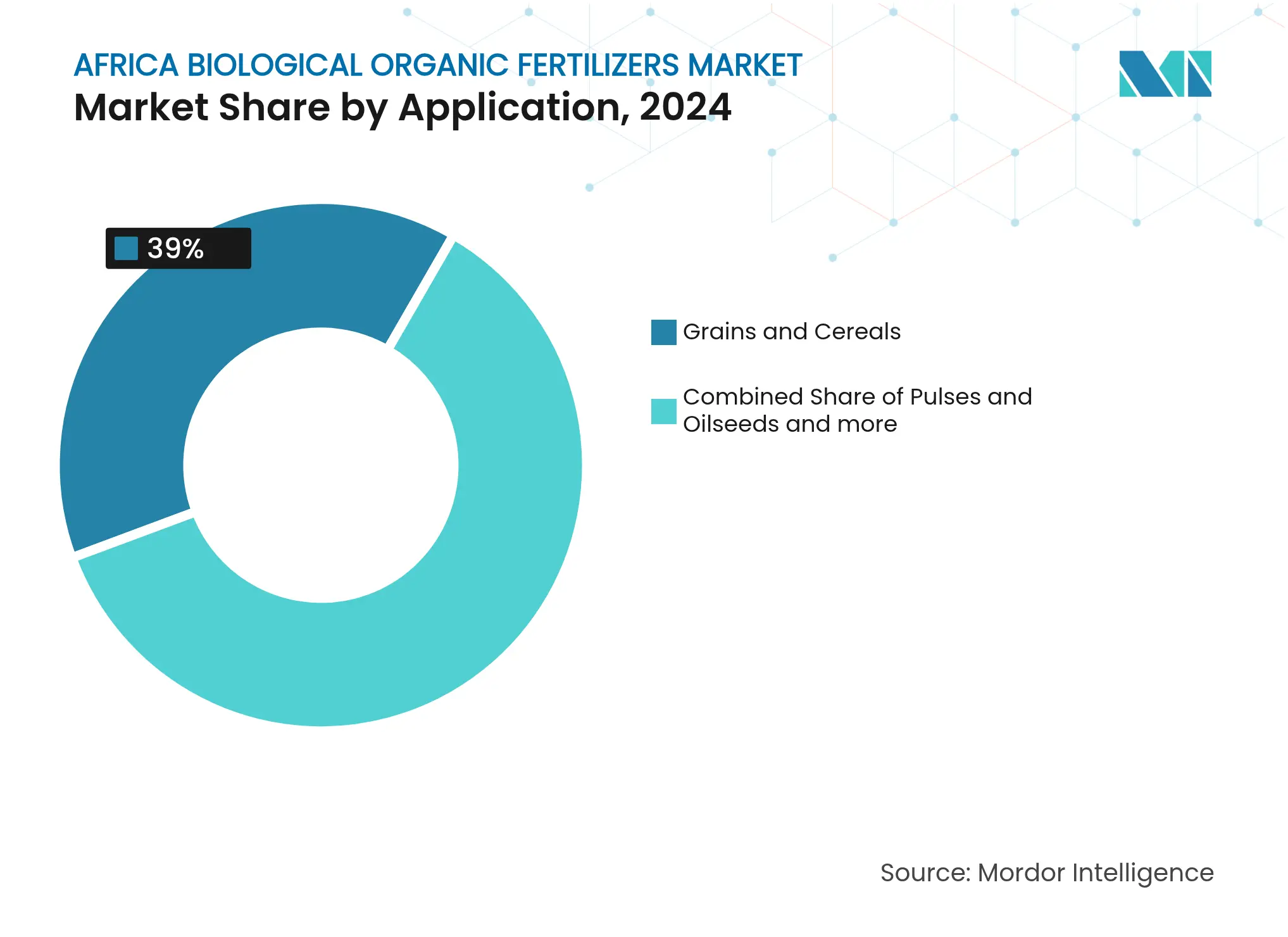

- By application, fruits and vegetables commanded 39% of the Africa biological organic fertilizers market size in 2024, and commercial crops are advancing at a 13.2% CAGR through 2030.

- By geography, South Africa leads with 27.0% market share in 2024, while Ethiopia is projected to expand at a 14.3% CAGR through 2030.

Africa Biological Organic Fertilizers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of Organic Farmland Expansion of Organic Farmland | +2.8% | East Africa and West Africa core, spill-over to Southern Africa | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.8%

|

Geographic Relevance

:East Africa and West Africa core, spill-over to Southern

Africa |

Impact Timeline

:

Medium term (2-4 years)

|

Growing Demand for Regenerative Agriculture Inputs Growing Demand for Regenerative Agriculture Inputs | +2.1% | Kenya, Ghana, South Africa lead, pan-continental uptake | Long term (≥4 years) | |||

Government Subsidies for Bio-inputs Government Subsidies for Bio-inputs | +1.9% | West Africa and East Africa, pilot programs in North Africa | Short term (≤2 years) | |||

Scaling Carbon-Credit–Linked Fertilizer Programs Scaling Carbon-Credit–Linked Fertilizer Programs | +1.6% | East Africa core, expanding into West Africa and Southern Africa | Medium term (2-4 years) | |||

Emergence of Tech-enabled Waste-to-Fertilizer Start-ups Emergence of Tech-enabled Waste-to-Fertilizer Start-ups | +1.4% | Nigeria, Kenya, and South Africa urban centers | Medium term (2-4 years) | |||

Climate-smart Funding from DFIs and Impact Investors Climate-smart Funding from DFIs and Impact Investors | +1.2% | ECOWAS and EAC blocs, continent-wide reach | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of Organic Farmland

Certified organic acreage is rising as governments align with the African Union’s soil-health agenda. Kenya’s pilot soil-carbon programs delivered 15–20% yield gains and issued verified credits that paid farmers USD 350,000 [1]Source: World Bank Group, “Advancing Climate-Smart Agriculture Technologies in Africa,” worldbank.org. The African Development Bank granted EUR 5 million (USD 5.4 million) to the International Institute of Tropical Agriculture in 2025 to scale similar demonstrations in six countries [2].Source: African Development Bank Group, “African Development Bank Provides €5 Million Grant to IITA,” afdb.org Participatory Guarantee Systems supported by the IFOAM- Organics International framework are lowering certification costs, only 0.2% of farmland is currently certified, leaving considerable room for conversion [3]Source: IFOAM-Organics International, “Africa,” ifoam.bio.

Growing Demand for Regenerative Agriculture Inputs

The World Bank expanded its Climate Research for Africa (AICCRA) program by USD 40 million in 2024 to validate regenerative practices across six African states. Corporations such as Fresh Del Monte in 2024, opened a biofertilizer plant in Kenya to decarbonize fruit supply chains. Research from Nigeria shows microbial inoculants reduce soil acidity while improving nutrient availability, reinforcing market readiness for premium bio-inputs. This convergence of technology and sustainability creates premium market segments where performance justifies higher input costs compared to conventional alternatives.

Government Subsidies for Bio-inputs

Several governments are redirecting fertilizer incentives. In 2024, the African Development Bank’s Fertilizer Financing Mechanism launched a USD 2 million program in Mozambique that channels guarantees toward organic products. Nigeria earmarked USD 540 million for agro-industrial hubs that include local biofertilizer capacity. Successful rollouts depend on extension services that safeguard quality and prevent counterfeit inputs. However, subsidy effectiveness depends on complementary extension services and quality control mechanisms that prevent counterfeit products from undermining farmer confidence in the organic alternative.

Scaling Carbon-Credit–Linked Fertilizer Programs

Carbon finance adds new revenue streams. Kenya’s soil-carbon project issued 24,788 credits under Verra and created a template for smallholder aggregation. The World Bank’s USD 2.3 billion Eastern and Southern Africa program approved in 2022 incorporates payment-for-performance mechanisms that reward nutrient solutions with proven sequestration. Methodological complexity remains a barrier, prompting calls for simplified protocols. However, methodological complexity and transaction costs currently limit carbon credit access to larger-scale operations, requiring simplified protocols and aggregation mechanisms to reach smallholder farmers effectively.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Competition from Subsidized Synthetic Fertilizers Competition from Subsidized Synthetic Fertilizers | -2.4% | West Africa and East Africa | Short term (≤2 years) | (~) % Impact on CAGR Forecast:

-2.4%

|

Geographic Relevance

:

West Africa and East Africa

|

Impact Timeline

:

Short term (≤2 years)

|

Fragmented Smallholder Supply Chains Fragmented Smallholder Supply Chains | -1.8% | Central Africa most acute,continent-wide | Medium term (2-4 years) | |||

Quality-Assurance Gaps and Counterfeit Products Quality-Assurance Gaps and Counterfeit Products | -1.2% | Nigeria, Kenya, Ghana urban markets | Short term (≤2 years) | |||

Limited Cold-chain for Liquid Biofertilizers Limited Cold-chain for Liquid Biofertilizers | -0.9% | Tropical zones and remote areas | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Competition from Subsidized Synthetic Fertilizers

Synthetic fertilizer subsidies create artificial price advantages that undermine organic alternatives, with African governments spending billions annually on chemical input programs that distort market signals and perpetuate soil degradation cycles. Government price controls keep chemical fertilizers artificially cheap even as research links overuse to declining soil health. Program redesign toward outcome-based metrics is gaining traction, yet entrenched interests slow policy shifts. The political economy of agricultural subsidies reflects elite capture and external donor pressures rather than smallholder farmer needs, creating institutional resistance to organic fertilizer promotion despite demonstrated soil health benefits.

Fragmented Smallholder Supply Chains

Smallholder agriculture dominates African farming systems with average plot sizes below 2 hectares, creating distribution challenges that increase organic fertilizer costs and limit market penetration across rural communities. Average farm sizes below two hectares raise last-mile distribution costs. Digital marketplaces and cooperative aggregation are emerging, but weak rural logistics inflate prices relative to synthetics. Fragmentation creates quality control challenges where counterfeit products undermine farmer confidence, requiring regulatory frameworks and certification systems that can operate effectively across diverse linguistic and cultural contexts.

Segment Analysis

By Product Type: Microorganisms Drive Innovation Despite Residue Dominance

Organic residues retained 47% of the Africa biological organic fertilizers market share in 2024, reflecting plentiful crop and livestock waste. Microorganisms are forecast to register a 15.6% CAGR, the fastest within the Africa biological organic fertilizers market, as growers adopt nitrogen-fixing bacteria and phosphate-solubilizing fungi for precision nutrition. Crop residues will remain the volume leader, yet residue-only programs face nutrient-density constraints that microbial blends offset. Companies are integrating spore-based inoculants into composted substrates, yielding uniform granules that fit existing spreaders. Regulatory clarity on microbial registration will further unlock growth as domestic manufacturers scale fermentation capacity in Kenya and Ghana.

A surge in field trials under International Fund for Agricultural Development (IFAD)-supported programmes shows yield lifts of 18% in maize when residue compost is fortified with rhizobia. Producers are adding mycorrhizal fungi to improve phosphorus uptake in depleted soils prevalent across the Sahel. Investor attention is shifting toward microbial consortia that tolerate high temperatures, which removes cold-chain barriers and cuts logistics costs by up to 25%.

Note: Segment shares of all individual segments available upon report purchase

By Application: Commercial Crops Accelerate Sustainability Transition

Fruits and vegetables held 39% of demand in 2024, benefiting from export premiums linked to organic certification. The Africa biological organic fertilizers market size for commercial crops is projected to climb at a 13.2% CAGR, outpacing staples as coffee, tea, and cocoa exporters as they respond to deforestation-free and carbon-neutral mandates. Ghanaian cocoa cooperatives using bio-fertilizer under the African Development Bank guarantees reported a tenfold increase in fertilizer supply.

Grains and cereals remain pivotal for food security, but adoption lags due to thin profit margins. Governments are piloting blended subsidy schemes that cover part of the cost differential between bio and chemical inputs, which could double organic penetration in staple crops by 2030. Pulses and oilseeds are gaining attention for their nitrogen-fixing role, cutting synthetic demand and broadening the Africa biological organic fertilizers market footprint. Specialty crops such as moringa and medicinal herbs provide niche, high-value avenues where certification premiums justify rapid switch-overs.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

South Africa leads with 27.0% market share in 2024 and demonstrates 13.9% CAGR through 2030, leveraging established agricultural value chains and advanced manufacturing capabilities through companies like African Black Soldier Fly that convert organic waste into high-value agricultural inputs while addressing urban waste management challenges. The country's National Organic Waste Composting Strategy provides regulatory frameworks that support commercial-scale organic fertilizer production, while mining sector expertise enables integrated nutrient solutions. Research demonstrates that biochar represents a viable alternative to synthetic fertilizers for smallholder farmers, with South African institutions leading continental research on soil health restoration. In may 2025, the African Development Bank's guarantee for Zambeef's operations extends South African agricultural expertise across Southern Africa, creating regional value chains that support over 86,000 farmers through integrated organic fertilizer programs. However, the country's relatively developed synthetic fertilizer infrastructure creates competitive pressures that require organic alternatives to demonstrate clear performance advantages and cost competitiveness.

Ethiopia emerges as the fastest-growing market, expand at a 14.3% CAGR through 2030, driven by the World Bank's AICCRA (Climate Research for Africa) project expansion in 2024 and the Oromia Forest Landscape Program that combines sustainable agriculture with forest management across multiple regions. The country benefits from USD 40 million, in additional International Development Association (IDA) grants for climate-smart agriculture technologies, establishing demonstration sites that validate organic fertilizer effectiveness for smallholder farmers [4]Source: World Bank Group, “Oromia Forested Landscape Program: Protecting Forests and Improving Livelihoods,” worldbank.org. Research in the South Gondar Zone identifies key determinants of organic fertilizer adoption, including education levels, extension service access, and farmland fertility status, providing insights for targeted market development strategies.

Egypt represents significant market share in 2024, positioning itself as a strategic market opportunity through established agricultural export industries and government initiatives supporting sustainable farming practices. The country's position in North Africa provides access to Mediterranean export markets that increasingly require sustainability certifications, creating premium pricing opportunities for organic produce.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

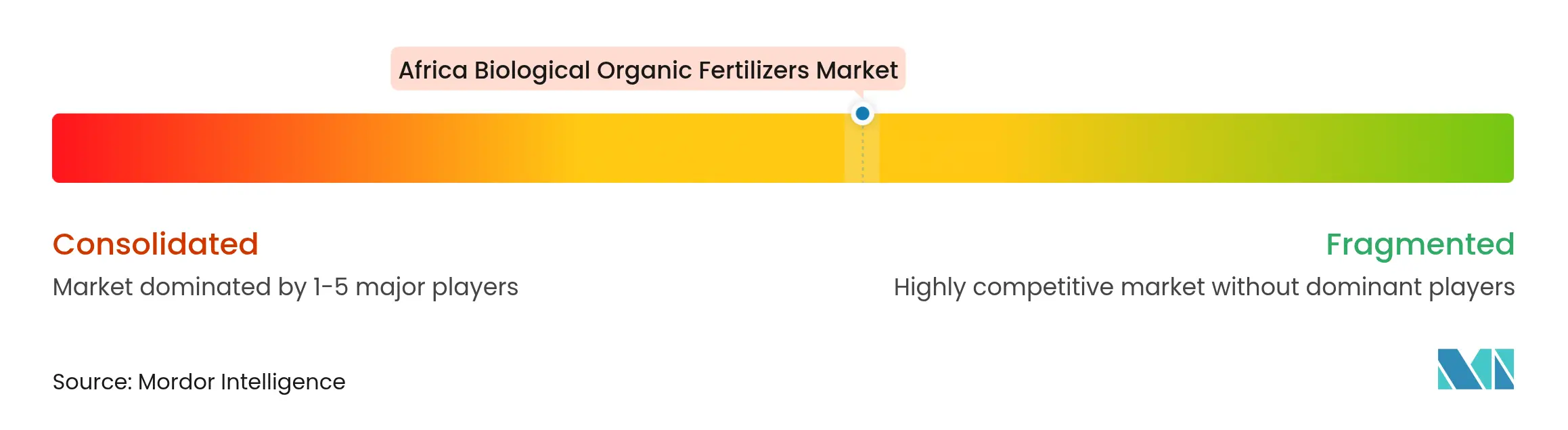

Market Concentration

The Africa biological organic fertilizers market exhibits a moderate concentration ratio, with players like FOMI (Organo-Mineral Fertilizers Industries), Safi Organics Limited, Micro Biological Fertilizer International, Bioceres Crop Solutions, and T. Stanes and Company Limited. Strategic themes include vertical integration, circular-economy feedstocks, and carbon-credit enablement. Strategic themes include vertical integration, circular-economy feedstocks, and carbon-credit enablement. Partnerships with DFIs provide concessional funding, lowering weighted-average capital costs and accelerating plant construction. Regional specialists leverage localized biomass streams and distribute them through agro-dealer networks that understand smallholder preferences. Quality assurance aligned with ISO/TC 134 standards is becoming a differentiator, as subpar imports erode trust and invite stricter regulation.

Technology licensing is another route: microbial pioneers are out-licensing strains to residue-rich cooperatives that lack fermentation capacity. Competitive advantage increasingly hinges on data analytics, with firms offering digital agronomy services that monitor soil health and verify carbon outcomes, strengthening client retention and premium pricing.

Merger opportunities are rising as global nutrient players scout Africa for green-growth assets. Technology licensing is another route: microbial pioneers are out-licensing strains to residue-rich cooperatives that lack fermentation capacity. Competitive advantage increasingly hinges on data analytics, with firms offering digital agronomy services that monitor soil health and verify carbon outcomes, strengthening client retention and premium pricing.

Africa Biological Organic Fertilizers Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Kenya hosted the establishment of the Pan-African Fertilizer Industry Association, following unanimous endorsement from Africa's fertilizer industry stakeholders. The association aims to enhance Africa's fertilizer production, trade capabilities, and utilization to improve agricultural productivity and support farmers across the continent.

- October 2024: OFA has launched a liquid organic fertilizer crafted in Ghana, lauded for its social and environmental advantages. This fertilizer's use has been linked to bolstered crop resilience against drought, a boon during extended dry periods, thereby promoting food security and sustainability.

- May 2024: Fresh Del Monte Produce Inc., in collaboration with Vellsam Materias Bioactivas, has established a biofertilizer plant in Kenya. This facility focuses on converting pineapple residues into biofertilizers, representing a crucial initiative for promoting waste reduction and sustainable agricultural practices in the region.

Table of Contents for Africa Biological Organic Fertilizers Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Expansion of Organic Farmland

- 4.2.2Growing Demand for Regenerative Agriculture Inputs

- 4.2.3Government Subsidies for Bio-inputs

- 4.2.4Scaling Carbon-Credit-Linked Fertilizer Programs

- 4.2.5Emergence of Tech-enabled Waste-to-Fertilizer Start-ups

- 4.2.6Climate-smart Funding from DFIs and Impact Investors

- 4.3Market Restraints

- 4.3.1Competition from Subsidized Synthetic Fertilizers

- 4.3.2Fragmented Smallholder Supply Chains

- 4.3.3Quality-Assurance Gaps and Counterfeit Products

- 4.3.4Limited Cold-chain for Liquid Biofertilizers

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value)

- 5.1Product Type

- 5.1.1Microorganisms

- 5.1.2Organic Residues

- 5.2Application

- 5.2.1Grains and Cereals

- 5.2.2Pulses and Oilseeds

- 5.2.3Fruits and Vegetables

- 5.2.4 Commercial Crops (Tea, Coffee, Cotton, Sugarcane)

- 5.2.5Other Crop Types

- 5.3Geography

- 5.3.1South Africa

- 5.3.2Ethiopia

- 5.3.3Egypt

- 5.3.4Rest of Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Safi Organics Limited

- 6.4.2Micro Biological Fertilizer International

- 6.4.3Bioceres Crop Solutions

- 6.4.4J.M. Huber Corporation

- 6.4.5T. Stanes and Company Limited

- 6.4.6SoilGrow

- 6.4.7EcoOrganic Fertilizers Ghana Ltd.

- 6.4.8Kynoch Fertilizer

- 6.4.9MBFi

- 6.4.10FOMI (Organo-Mineral Fertilizers Industries)

7. Market Opportunities and Future Outlook

Africa Biological Organic Fertilizers Market Report Scope

Biological organic fertilizers market are derived from many animal and plant-based residues and mineral ores, and they are also developed from beneficial microorganisms. The African organic fertilizers market is segmented by Product Type (Microorganism and Organic Residues), Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Commercial crops, and Other Crop Types), and Geography (South Africa, Ethiopia, Egypt, and the Rest of Africa). The report offers market size and forecast in terms of value (USD) for the above-mentioned segments.