Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

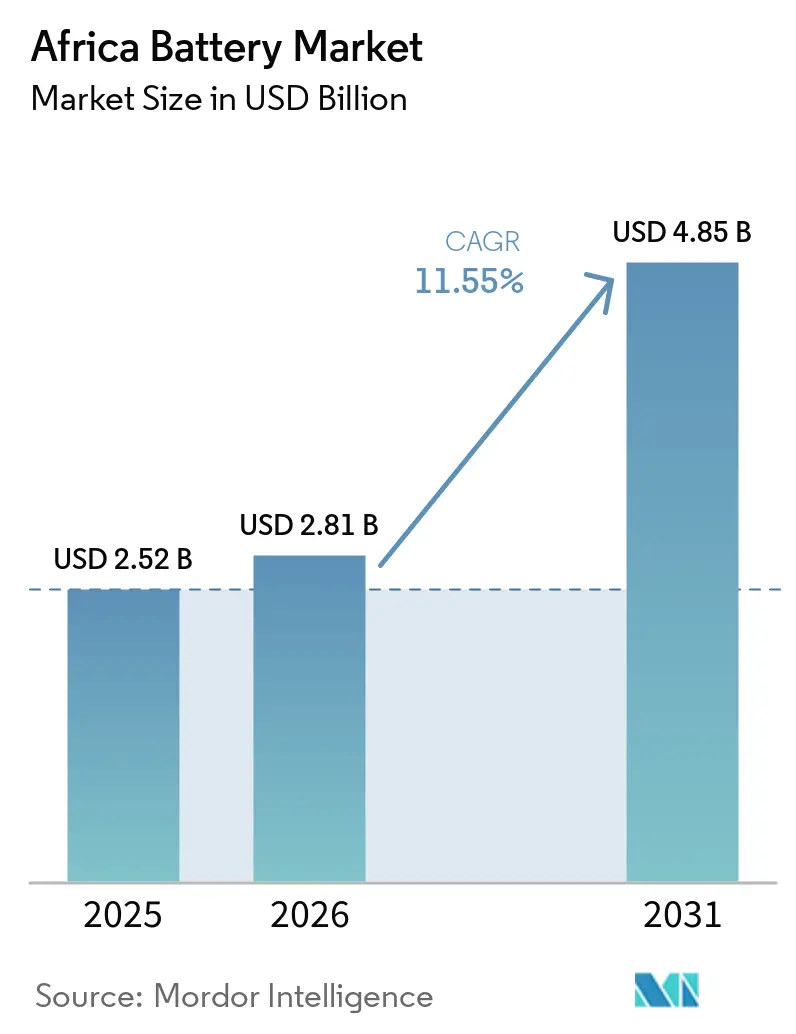

| Base Year Market Size (2025) | USD 2.52 Billion |

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 11.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Battery Market Analysis by Mordor Intelligence

The Africa Battery Market size was valued at USD 2.52 billion in 2025 and is estimated to grow from USD 2.81 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 11.55% during the forecast period (2026-2031).

Rising electrification goals, intensifying decarbonization mandates, and falling lithium-ion prices are sharpening investment in energy storage, while automotive and telecom players pivot away from diesel. Chinese cell makers are embedding themselves in local supply chains, giving African buyers shorter delivery cycles and cost relief. Governments are courting battery factories with tax holidays and land grants, aiming to anchor value chains onshore. Meanwhile, weak grid reliability, which left only 43% of sub-Saharan Africa connected in 2024, turns distributed solar-plus-storage solutions into a necessity rather than a luxury.[1]International Energy Agency, “Africa Energy Outlook 2024,” iea.org

Key Report Takeaways

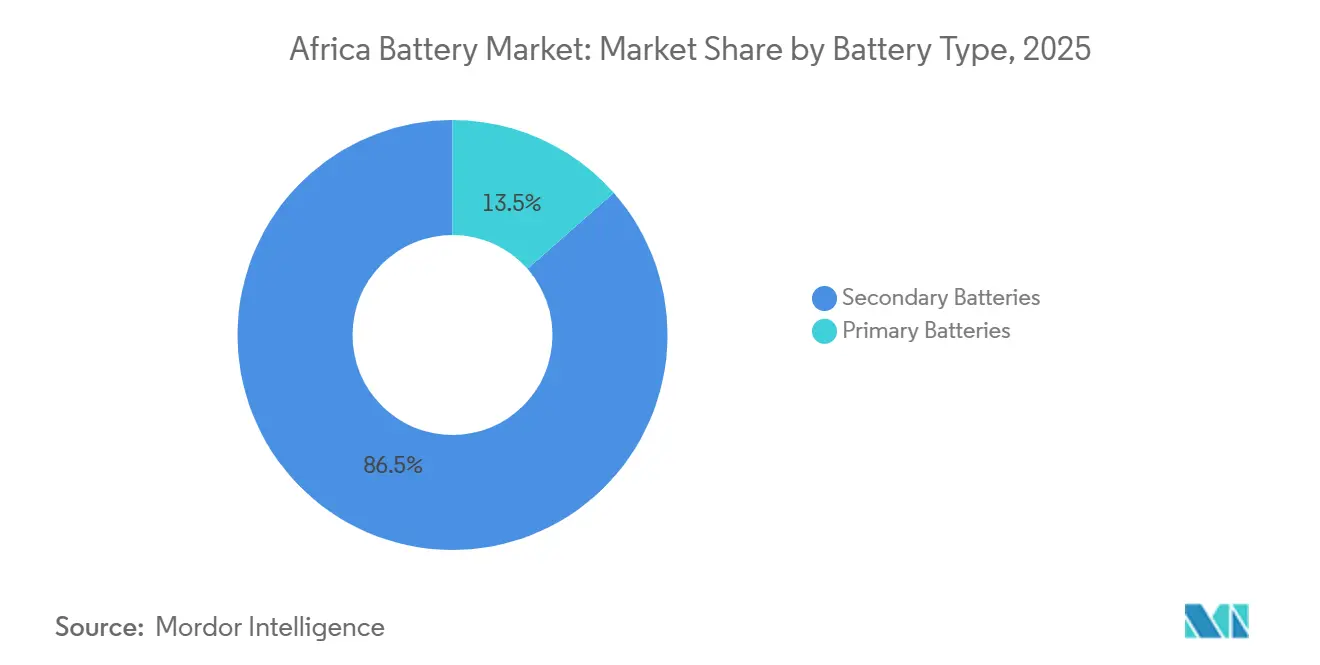

- By battery type, secondary batteries held 86.5% of revenue in 2025 and are forecast to post a 12.1% CAGR through 2031, outpacing primary chemistries.

- By technology, lithium-ion captured 52.9% of the Africa battery market share in 2025 and is set to expand at a 12.4% CAGR to 2031.

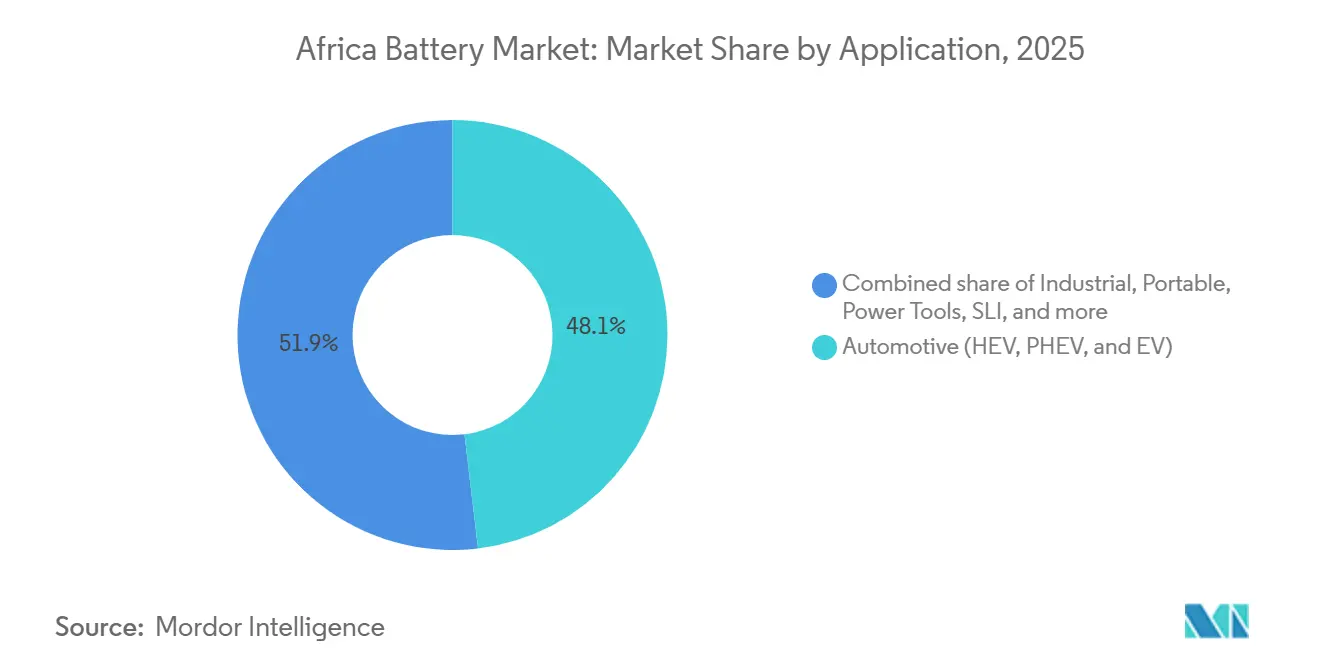

- By application, industrial uses are projected to advance at a 13.5% CAGR, while automotive remained the largest slice with 48.1% revenue share in 2025.

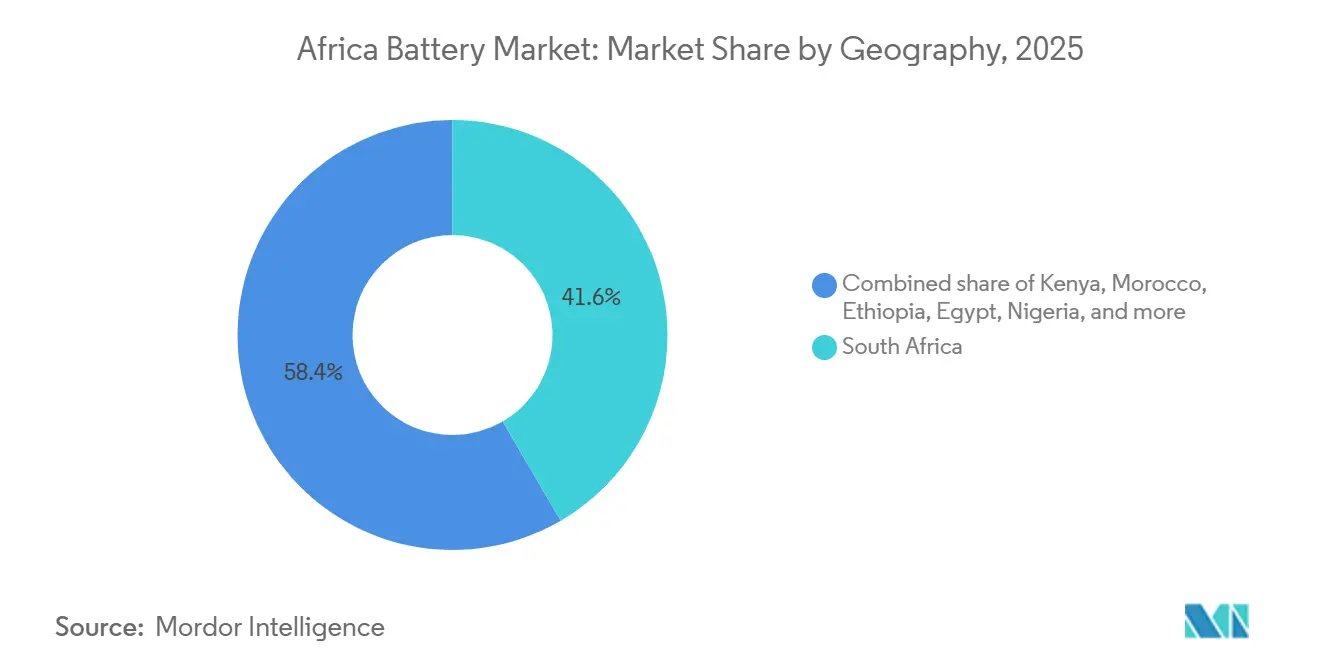

- By geography, South Africa commanded 41.6% of the Africa battery market size in 2025; Ethiopia is the fastest-growing country with a 13.8% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Lithium-Ion Prices | +2.3% | South Africa, Morocco, Egypt | Short term (≤ 2 years) |

| Surge in Off-Grid Solar + BESS Deployments | +2.8% | Ethiopia, Kenya, Nigeria | Medium term (2-4 years) |

| Government Incentives for Local Manufacturing | +1.6% | South Africa, Morocco, Egypt | Medium term (2-4 years) |

| Rapid Electrification of Two-/Three-Wheelers | +1.4% | Nigeria, Kenya, Ethiopia | Medium term (2-4 years) |

| Telecom-Tower Retrofit Cycle | +1.9% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Chinese-Backed Lithium-Processing Build-Out | +1.2% | Morocco, DRC, Zimbabwe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Prices

Global pack prices slipped to USD 115 per kWh in 2024 and to USD 94 per kWh in China, finally undercutting diesel gensets for African telecom towers and microgrids. Operators such as MTN and Airtel retrofit sites with lithium-ion systems that last up to 10 years, trimming the total cost of ownership by about 30% and slashing maintenance trips. South African and Egyptian utilities now pair multi-hour storage with solar farms, exemplified by the 540 MW Kenhardt project that integrates 1,140 MWh of batteries to meet evening peaks.[2]Scatec, “Kenhardt Project Fact Sheet,” scatec.com Chinese cathode and anode plants opening in Morocco further compress supply-chain costs, creating a virtuous circle of affordability.

Surge in Off-Grid Solar + BESS Deployments

Off-grid solar-plus-storage microgrids are proliferating where extending grids remains uneconomic. Ethiopia targets 35% off-grid electrification by 2030 using solar arrays with 4-8 hour battery reserves.[3]World Bank, “Ethiopia Electrification Program,” worldbank.org Egypt, Botswana, and Zambia adopted similar models, securing debt from multilateral banks that now view storage cash flows as bankable. Telecom and agricultural cold-chain operators gain uptime improvements that justify higher upfront spend, advancing rural energy access and economic activity.

Government Incentives for Local Battery Manufacturing

South Africa’s 150% tax deduction on renewable capital and its ZAR 1 billion fund tilt economics toward domestic assembly.[4]South African Revenue Service, “ETI and Renewable Tax Guide 2025,” sars.gov.za Morocco offered land and grid connections to attract Gotion High-Tech’s USD 1.3 billion, 20 GWh gigafactory slated for 2026, reinforcing North Africa as a bridge to European EV supply. Egypt’s El Nasr Automotive joined Chinese partners for a 500,000-unit yearly line that will feed the two-wheeler sector. These incentives create cost gaps of up to 20% against import-reliant peers.

Rapid Electrification of Two-/Three-Wheelers

Africa’s electric two- and three-wheeler fleet grew 40% year-on-year to about 9,000 units in 2024. Swap-battery models from firms like Spiro remove range anxiety and upfront sticker shock, enabling a plan to assemble 100,000 bikes annually in Nigeria. Kenya’s BasiGo deployed 150 e-buses that hit payback in four years, while Nigeria’s Innoson targets tricycle fleets. Limited public charging infrastructure confines most users to depot or swap models, yet falling cell costs and urban air-quality rules sustain momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Supply Bottlenecks | -1.8% | DRC, Zimbabwe, South Africa | Medium term (2-4 years) |

| Patchy Grid & Charging Network | -1.5% | Nigeria, Kenya, Ethiopia | Long term (≥ 4 years) |

| Counterfeit / Low-Quality Influx | -1.2% | Kenya, Nigeria | Short term (≤ 2 years) |

| Policy Fragmentation | -0.9% | Nigeria, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Supply Bottlenecks

The DRC’s 30% processing rule idled cobalt shipments, adding 4-6 week delays and 12% to Asian buyers’ landed costs. Zimbabwe’s rail capacity caps lithium exports, doubling freight versus Australian peers, while South African manganese miners truck ore because of rail unreliability. Artisanal cobalt, roughly 20% of global supply, now sits in compliance limbo under the EU due diligence law, exposing buyers to legal and reputational risk.

Counterfeit / Low-Quality Battery Influx

Kenya seized 12,000 fake lead-acid units in 2024, yet only four counties field dedicated product inspectors. Nigeria estimates counterfeits at 25% of its replacement market, hurting premium brands and prompting stricter certification rules. Lack of consumer awareness compounds risk; unbranded lithium-ion packs have sparked fires in solar home systems, pushing regulators to demand IEC 62619 compliance from 2025 onward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Dominance Reshapes Value Chains

Secondary batteries delivered 86.5% of 2025 revenues, and their 12.1% CAGR is set to reinforce that dominance. Automotive and industrial clients value rechargeability’s lower lifetime cost, while lithium-ion replaces lead-acid in high-cycle roles. Primary cells cling to a 13.5% share mainly in low-drain devices. The Africa battery market size for secondary chemistries is projected to eclipse USD 4 billion by 2031, with lithium-ion securing most gains.

The Africa battery market share of primary cells will keep shrinking as extended producer responsibility fees rise in Kenya and South Africa. Lead recyclers such as First National Battery recover 96% of materials, yet lithium-ion recycling remains scarce, signaling an investment opportunity. Gotion’s Moroccan plant will shorten delivery times and hedge currency swings, further tilting buyers toward rechargeables.

By Technology: Lithium-Ion Ascendancy Amid Legacy Persistence

Lithium-ion’s 52.9% slice in 2025 came with a 12.4% growth outlook through 2031, underpinned by higher energy density and price declines. Local assemblers like Solar MD bundle imported cells into custom packs for rooftop solar, meeting week-long lead times. Lead-acid retains pockets in SLI and UPS applications, but its 7.2% CAGR lags lithium-ion’s momentum, signaling steady share loss.

NiMH and NiCd combined held roughly 4% revenue, serving forklifts and hybrid vehicles that prize temperature tolerance. Flow and sodium-sulfur pilots prove technical fit for long-duration storage, yet costs and safety keep them niche. Emerging sodium-ion cells could enter African stationary sites by 2027 as cost-sensitive buyers weigh density trade-offs.

By Application: Industrial Surge Outpaces Automotive

Automotive remained the largest application at 48.1% revenue in 2025, but industrial demand posted the fastest 13.5% CAGR. Telecom-tower retrofits alone reshape procurement, replacing diesel and lead-acid with lithium-ion hybrids that cut ownership costs by a quarter. Utility-scale solar projects embed multi-hour storage to firm supply and defer grid upgrades, while warehouses adopt lithium-ion forklifts to maximize uptime.

Electric two-wheeler batteries add volume, though consumer electronics growth moderates amid smartphone saturation. Start-stop vehicle technology lags due to cost-sensitive segments, trimming lead-acid replacement cycles. The Africa battery market size for industrial users is forecast to surpass automotive by 2029 as storage becomes integral to energy strategy.

Geography Analysis

South Africa possessed 41.6% of 2025 revenue, buoyed by an automotive base and the continent’s largest utility-scale storage pipeline. Fiscal incentives and load-shedding headaches propel residential storage assemblers such as Solar MD to triple capacity. Yet rail bottlenecks and grid instability inflate costs, nudging some projects northward.

Ethiopia leads growth with a 13.8% CAGR on the back of hydropower surplus and village microgrids. Egypt sits at a 12% share, leveraging Benban solar stabilization and EV policies. Nigeria and Kenya each hover at 8-10% share, with two-wheeler electrification and telecom upgrades driving demand despite counterfeit headwinds. Morocco’s gigafactory launch in 2026 positions it as an exporter to Europe, reshaping trade flows.

The rest of Africa supplies roughly 18% revenue, anchored by mining microgrids in Botswana and Zambia and rural solar rollouts in Côte d’Ivoire and Ghana. Infrastructure deficits persist, yet dropping battery costs and pay-as-you-go finance models unlock fresh pockets of demand across the Sahel and Great Lakes.

Competitive Landscape

Chinese giants CATL, BYD, and Gotion dictate lithium-ion supply and deepen African footholds through assembly deals, while legacy lead-acid firms First National Battery and Chloride Exide defend entrenched channels. Gotion’s Moroccan gigafactory cuts freight 15-20% versus Asian imports, spurring rivals to localize or cede share. Domestic packagers Solar MD, Balancell, and Freedom Won win on quick delivery and tailored service during South Africa’s frequent outages.

Turnkey packages from Saft and Huawei appeal to cash-strapped utilities that need financing along with hardware. Recycling remains a white space; only two lithium-ion plants operate continent-wide, with legislative momentum building for extended producer responsibility. Counterfeit risk and varying standards force brands to adopt blockchain traceability and seek SABS or IEC marks to protect their reputation.

Africa Battery Industry Leaders

Exide Industries Ltd

Duracell Inc.

Panasonic Energy

Energizer Holdings Inc.

First National Battery (Metair)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: South African EV infrastructure company Zero Carbon Charge (CHARGE) launched the country’s first off-grid, solar-powered EV charging stations along the Johannesburg–Durban corridor in May 2026. The stations operate independently from the national grid using solar generation and battery storage systems, highlighting the growing role of batteries in Africa’s transport electrification ecosystem. The company plans to deploy 60 charging stations nationwide by 2027.

- April 2026: Zhejiang Huayou Cobalt, a Chinese mining giant, made history by orchestrating Africa's inaugural export of lithium sulphate from Zimbabwe. This lithium sulphate was derived from the company's newly minted USD 400 million lithium plant, which began operations in 2025 and boasts an impressive annual production capacity of 50,000 metric tons. This milestone signifies a pivotal shift for Africa, moving from merely exporting raw spodumene concentrate to processing battery materials locally.

- March 2026: Chinese automaker Geely announced plans in 2026 to expand its South African lineup to nearly 10 models, including battery electric vehicles (BEVs) and plug-in hybrids. Its affordable E2 electric vehicle reportedly sold out shortly after launch, reflecting increasing demand for lithium-ion battery-powered mobility solutions in Africa.

- February 2026: SOLA Group reached financial close and commenced construction on Naos-1, South Africa's largest privately contracted solar-plus-storage project, featuring 300 MW (435 MWp) of solar generation and 660 MWh of battery energy storage, backed by long-term power purchase agreements with industrial consumers.

Africa Battery Market Report Scope

A battery is a device that converts chemical energy contained within its active materials directly into electric energy by means of an electrochemical oxidation-reduction (redox) reaction.

The Africa battery market is segmented by type, technology, application, and geography. By type, the market is segmented into primary batteries and secondary batteries. By technology, the market is segmented into lead-acid, Li-ion, nickel-metal hydride, nickel-cadmium, sodium-sulfur, solid-state, flow batteryand emerging chemistries. By application, the market is segmented into automotive batteries, industrial batteries, portable batteries, power tools, SLI, and other applications. The report also covers the market size and forecasts for the Africa battery market across major countries. The report offers the market size in value terms in USD for all the abovementioned segments.

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

By Geography

| South Africa |

| Egypt |

| Kenya |

| Nigeria |

| Morocco |

| Ethiopia |

| Rest of Africa |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications | |

| By Geography | South Africa |

| Egypt | |

| Kenya | |

| Nigeria | |

| Morocco | |

| Ethiopia | |

| Rest of Africa |

Key Questions Answered in the Report

How big is the Africa battery market in 2026?

The market is valued at USD 2.81 billion in 2026, on its way to USD 4.85 billion by 2031, tracking an 11.55% CAGR.

Which battery technology is growing fastest in Africa?

Lithium-ion is expanding at a 12.4% CAGR thanks to price drops and local gigafactory investments.

What is driving industrial battery demand?

Telecom-tower retrofits, utility solar-plus-storage projects, and warehouse electrification help industrial applications post the highest 13.5% CAGR.

Which African country leads battery manufacturing?

Morocco will host a 20 GWh Gotion gigafactory in 2026, positioning it as the continent's largest production base.

What are the top restraints on market growth?

Raw-material bottlenecks, counterfeit batteries, and patchy charging infrastructure collectively shave almost 5% off potential CAGR.

Are recycling facilities keeping pace with battery waste?

Lead-acid recycling is well-established, but only two lithium-ion plants operate in Africa, leaving a gap in circular-economy capacity.

Page last updated on: