Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

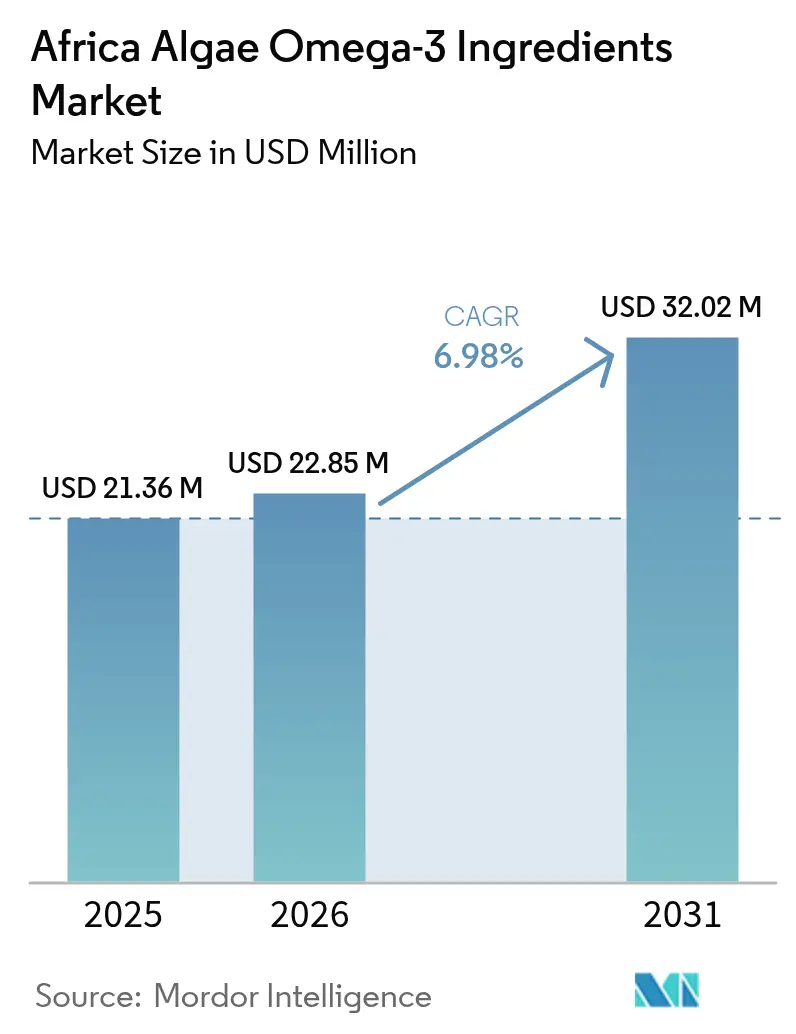

| Base Year Market Size (2025) | USD 21.36 Million |

| Market Size (2026) | USD 22.85 Million |

| Market Size (2031) | USD 32.02 Million |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Algae Omega-3 Ingredients Market Analysis by Mordor Intelligence

Africa algae omega-3 ingredients market size in 2026 is estimated at USD 22.85 million, growing from 2025 value of USD 21.36 million with 2031 projections showing USD 32.02 million, growing at 6.98% CAGR over 2026-2031. This outlook is underpinned by policy momentum for infant-formula docosahexaenoic acid (DHA) fortification, accelerating demand for vegan and halal supplements in major cities, and blue-economy programs that funnel public capital into algaculture. Shifts away from volatile fish-oil supply chains toward fermentation-based DHA and eicosapentaenoic acid (EPA) are also reshaping competitive strategies, as incumbents redeploy assets from marine-oil refining to heterotrophic microalgae production. Functional beverage launches, aquafeed reformulation, and consumer preference for clean-label nutrition create additional tailwinds, while high algal-oil input costs and multi-jurisdictional approvals remain structural headwinds. South Africa’s transparent regulatory environment, Nigeria’s fast-growing urban middle class, and ongoing pilot projects in East Africa collectively position the Africa algae omega-3 market for sustained, albeit uneven, expansion across the continent.

Key Report Takeaways

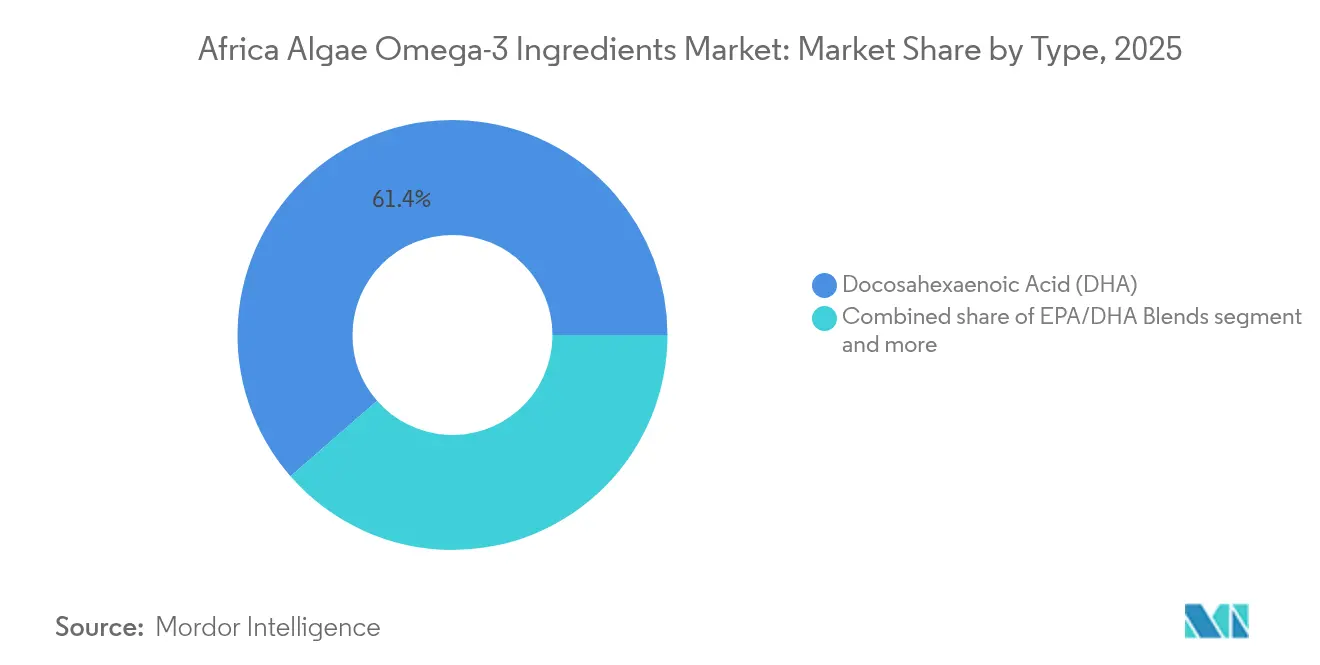

- By type, docosahexaenoic acid accounted for 61.42% of the Africa algae omega-3 ingredients market share in 2025, whereas EPA/DHA blends are forecast to post a 7.12% CAGR through 2031.

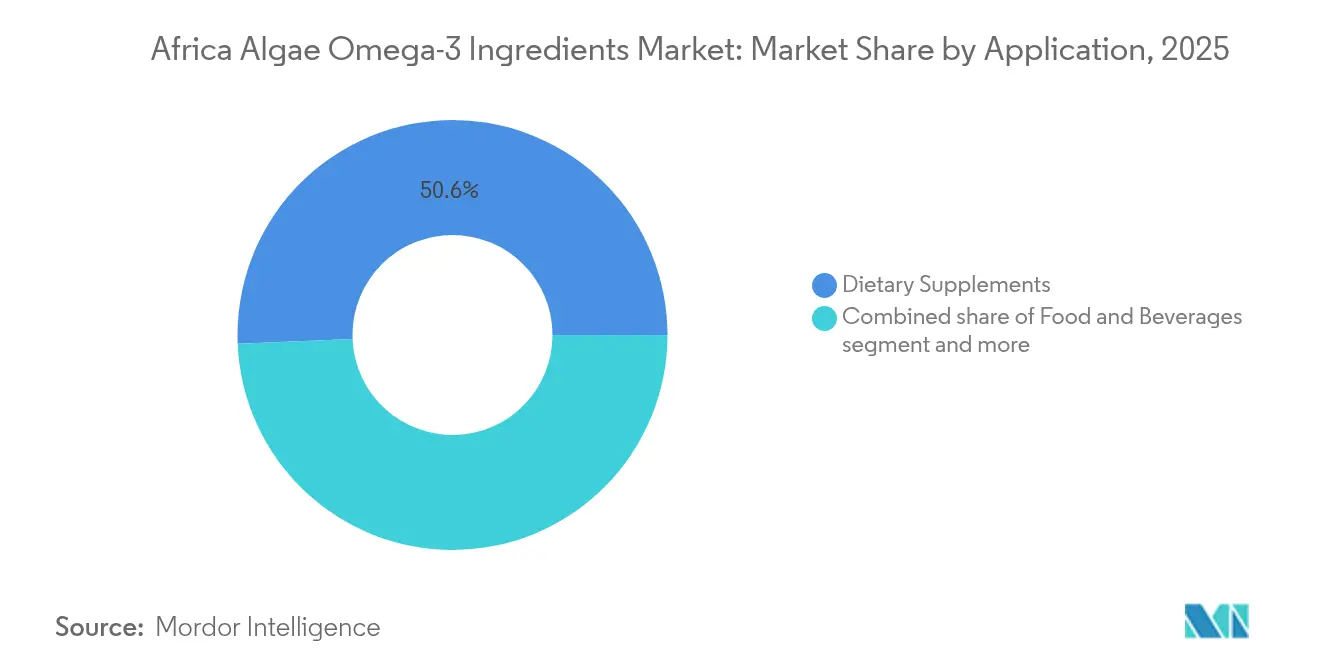

- By application, dietary supplements led with 50.65% revenue share in 2025; food and beverages are set to expand at a 7.6% CAGR over 2026-2031.

- By geography, South Africa captured 28.12% of 2025 demand, while Nigeria is projected to grow at a 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Algae Omega-3 Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infant-formula DHA fortification rules widening to Africa | +0.8% | East Africa (Kenya, Tanzania, Uganda, Rwanda), with spillover to Egypt and Nigeria | Medium term (2-4 years) |

| Demand for functional food and beverage products | +1.2% | South Africa, Nigeria urban centers, Egypt | Short term (≤ 2 years) |

| Rising adoption of DHA-rich algae ingredients for heart health and healthy aging formulations | +0.9% | South Africa, Egypt, urban Nigeria | Medium term (2-4 years) |

| Increasing government support for blue economy initiatives | +0.7% | Namibia, Kenya, Tanzania, South Africa | Long term (≥ 4 years) |

| Surging vegan/halal supplement demand in urban hubs | +1.1% | Nigeria (Lagos, Abuja), South Africa (Johannesburg, Cape Town), Egypt (Cairo) | Short term (≤ 2 years) |

| Increased application of algae omega-3 in aquafeed to replace fishmeal | +1.5% | Egypt (aquaculture zones), Nigeria (catfish farming), Kenya (tilapia operations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infant-formula DHA fortification rules widening to Africa

East African governments are aligning infant formula nutrient standards with Codex Alimentarius guidelines, creating favorable regulatory conditions for algal DHA suppliers. Tanzania's 2024 Food Fortification Regulations, introduced in March 2025, require fortificant traceability and establish a legal framework for incorporating micronutrients, including omega-3 fatty acids, into edible oils and complementary foods, although DHA is not yet a mandatory fortificant. Kenya's draft infant formula regulations, released for stakeholder feedback in late 2024, propose a minimum DHA content of 20 milligrams per 100 kilocalories, consistent with European Union Regulation 2016/127 [1]Source: European Union, "Document 02016R0127-20230317," eur-lex.europa.eu. These regulations also mandate that DHA sources must be free from marine contaminants, a requirement that benefits algae-based DHA over fish oil. Similarly, Uganda's National Bureau of Standards is developing comparable specifications, with implementation anticipated by 2026. This regulatory alignment is significant as infant formula represents a high-margin, low-volume market where manufacturers are willing to pay a premium for clean-label, allergen-free DHA, mitigating the cost disadvantage of algae-based sources.

Demand for functional food and beverage products

Urban consumers in South Africa and Nigeria are increasingly opting for functional beverages fortified with omega-3 as a convenient alternative to capsule supplements. Food manufacturers are capitalizing on this trend by implementing premium pricing strategies. In South Africa, new food-additive regulations set to take effect in January 2025 aim to streamline the approval process for novel omega-3 carriers, thereby reducing the time-to-market for fortified products such as juice, yogurt, and ready-to-drink smoothies. Meanwhile, in Nigeria, the urban middle class, primarily located in Lagos and Abuja, is driving demand for imported functional beverages. Local manufacturers are also beginning to co-pack fortified products using algal-oil concentrates supplied by companies such as Corbion and DSM-Firmenich, elaborating on the growing collaboration between global suppliers and local producers.

Rising adoption of DHA-rich algae ingredients for heart health and healthy aging formulations

In South Africa and Egypt, healthcare professionals, including cardiologists and geriatricians, are increasingly recommending omega-3 supplementation for patients with elevated triglycerides and age-related cognitive decline. This has created a clinical distribution channel for algal DHA, operating separately from traditional retail outlets. In South Africa, the updated 2024 cholesterol-management guidelines specifically recommend omega-3 as an adjunctive therapy for hypertriglyceridemia. Additionally, pharmacists are now offering algae-based soft gels to cater to vegetarian patients who avoid fish oil. In Egypt, public-awareness campaigns initiated by the National Committee for Control of Non-Communicable Diseases promote omega-3 intake to support cardiovascular health, although these campaigns do not currently distinguish between fish- and algae-derived sources. Demographic trends further highlight the market potential for omega-3 products. As of 2025, children under 15 years old account for approximately 26.2% of South Africa’s population, equating to about 16.5 million individuals. Meanwhile, around 10.5% of the population, or roughly 6.6 million people, are aged 60 and above, as reported by Statistics South Africa, reflecting a growing aging population that could benefit from interventions targeting cardiovascular and cognitive health [2]Source: Statistics South Africa, "Inside the Numbers: SA Population Trends for 2025," statssa.gov.za.

Increasing government support for blue economy initiatives

Government support for blue economy initiatives across Africa is contributing to the growth of the algae-omega-3 ingredients market by fostering a supportive regulatory and infrastructural framework for marine and aquaculture industries. Policies aimed at promoting sustainable fisheries, aquaculture, and marine resource management help lower barriers to algae cultivation and the production of DHA/EPA oils. By prioritizing sustainable alternatives to overexploited marine oils, these initiatives align with environmental and nutritional objectives, driving investment in algae-based omega-3 production and strengthening the regional supply chain. An example of such an initiative is the PROFISHBLUE program, launched by the Southern African Development Community (SADC) with support from the African Development Bank. This program enhances fisheries governance and trade corridors within the region [3]Source: South African Development Community, " SADC, AfDB and Partners launch ProFishBlue programme for the SADC Region," sadc.int. By improving value-chain infrastructure, financing, and cross-border trade for aquatic products, PROFISHBLUE indirectly supports algae-omega-3 ingredient producers by boosting production capacity, streamlining distribution, and increasing investor confidence in sustainable, marine-derived ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High algal DHA production costs vs fish oil | -0.9% | Global, with acute impact in price-sensitive Nigeria and Egypt markets | Short term (≤ 2 years) |

| Import dependency on algal oil concentrates | -0.6% | Nigeria, Egypt, Rest of Africa (excluding South Africa) | Medium term (2-4 years) |

| Regulatory delays for novel algae strains | -0.5% | South Africa (SAHPRA), Nigeria (NAFDAC), Egypt (NFSA) | Medium term (2-4 years) |

| Exchange-rate volatility affecting import pricing | -0.7% | Nigeria (naira depreciation), Egypt (pound devaluation), South Africa (rand fluctuations) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High algal DHA production costs vs fish oil

The high production cost of algal DHA compared to conventional fish oil remains a significant restraint on the growth of the algae-omega-3 ingredients market in Africa. The cultivation of microalgae, oil extraction, and maintaining consistent purity and stability require advanced technology, controlled environments, and energy-intensive processes. These factors increase per-unit costs, making algal DHA considerably more expensive than fish-derived omega-3, which benefits from established, large-scale extraction methods and supply chains. This cost disparity impacts affordability and adoption, particularly in price-sensitive African markets. Functional foods, supplements, and fortified products must compete with lower-cost alternatives, such as fish oil. Consequently, manufacturers may be reluctant to adopt algal DHA at scale unless factors such as increased consumer awareness, regulatory incentives, or sustainability-driven premium positioning help offset the higher costs. This creates a significant barrier to achieving widespread market penetration.

Import dependency on algal oil concentrates

Import dependency on algal oil concentrates remains a significant challenge for the algae-omega-3 ingredients market in Africa. Most countries in the region lack large-scale domestic production facilities for high-quality algal DHA/EPA oils, compelling manufacturers and supplement producers to rely on imports from regions such as North America, Europe, or Asia. This reliance increases the market's vulnerability to supply chain disruptions, shipping delays, and geopolitical risks, which can impact product availability and raise costs for local manufacturers. The dependence on imported algal oils also limits opportunities for local value addition and hinders the growth of a domestic algae-omega-3 industry. Factors such as high import tariffs, foreign exchange fluctuations, and logistical challenges further escalate costs, making these products less competitive compared to locally sourced fish oils or other omega-3 alternatives. As a result, import dependency constrains market growth and creates obstacles to achieving self-sufficiency in the African algae-omega-3 market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: DHA Dominance Reflects Infant and Cognitive Applications

Docosahexaenoic acid (DHA) accounted for 61.42% of total revenue in 2025, highlighting its dominance in infant formula fortification and cognitive health supplements, particularly as regulatory monographs specifically reference DHA but not eicosapentaenoic acid (EPA). DHA's prominence is driven by its critical role in early brain development and its inclusion in regulatory guidelines for infant nutrition, making it a preferred choice for manufacturers. The Africa algae omega-3 market size for DHA-only formulations remains significantly larger than that for pure EPA oils, a disparity expected to continue until cardiovascular-specific guidelines referencing EPA gain broader clinical acceptance. The EPA/DHA Blends are projected to grow at a 7.12% CAGR through 2031. EPA, while recognized for its cardiovascular benefits, has yet to achieve the same level of regulatory and clinical endorsement as DHA, limiting its market penetration.

However, fragmented African regulations classify blends as novel ingredients, requiring each dossier to undergo an independent review process, which delays product launches by an additional 12-18 months. This regulatory complexity creates significant barriers for new product introductions, slowing the pace of innovation in the market. Consequently, the Africa algae omega-3 market is expected to continue favoring DHA-focused products through at least 2028, although the adoption of blends is anticipated to gradually increase as aquafeed usage expands. The gradual shift toward blends will likely be influenced by advancements in regulatory harmonization and increased awareness of EPA's benefits in aquaculture and human health applications.

By Application: Dietary Supplements Lead, Fortification Accelerates

Dietary supplements accounted for 50.65% of the 2025 demand, maintaining the leading position due to the advantages of capsules, such as precise dosing, a two-year shelf life, and simplified import logistics. The Africa algae omega-3 market size attributed to supplements benefits from SAHPRA and NAFDAC regulations, which classify them as Category D complementary medicines, streamlining approvals compared to food additives. However, fortified foods and beverages are emerging as a key growth area, with a 7.6% CAGR, driven by brand owners’ ability to command 30-50% price premiums for functional SKUs in supermarket aisles.

Regulators are both promoting and monitoring fortification efforts. Tanzania’s 2025 enforcement of micronutrient labeling and traceability requirements highlights government interest in mass-market nutrition strategies. In Nigeria, the informal retail sector remains a challenge, with 80% of food sales occurring outside modern trade channels. However, e-commerce platforms and upscale grocery stores in Lagos are fostering early consumer awareness of omega-3-fortified beverages, paving the way for wider adoption.

Geography Analysis

South Africa accounted for 28.12% of the projected 2025 revenue, supported by SAHPRA's transparent regulatory framework, well-established distribution networks for imported nutraceuticals, and a consumer base accustomed to omega-3 supplementation. The country's regulatory clarity and efficient supply chains have positioned it as a key market for omega-3 products, with consumers showing a strong preference for health and wellness supplements. Additionally, the growing awareness of the health benefits of omega-3 among South African consumers is expected to further drive demand in the years to come.

Nigeria is experiencing the fastest regional growth, with a CAGR of 7.05%, driven by NAFDAC's 2025 regulations legitimizing algae-derived omega-3 products and urban population growth, fostering a middle class increasingly investing in preventive healthcare. The regulatory advancements are expected to encourage more product launches, while the growing middle class is likely to sustain demand for premium health products, including omega-3 supplements. Furthermore, the increasing prevalence of lifestyle-related health issues is prompting Nigerian consumers to incorporate omega-3 products into their preventive health measures.

The rest of Africa, including Kenya, Tanzania, Uganda, Namibia, and smaller markets, is benefiting from blue-economy initiatives and pilot programs for infant formula fortification, which could scale up quickly if initial results prove successful. These initiatives are fostering innovation in the region, with potential for significant growth in omega-3 applications across various segments, including maternal and child health.

Competitive Landscape

The Africa Algae Omega-3 Market is highly concentrated, with key players adopting vertical integration strategies. These strategies encompass strain development, heterotrophic fermentation, downstream processing, and direct sales to infant formula brands and nutraceutical contract manufacturers. This comprehensive approach creates significant barriers to entry for smaller competitors, particularly those without proprietary strains or co-manufacturing agreements, limiting their ability to compete effectively in the market.

Despite these challenges, opportunities exist in localized production, halal-certified blends, and aquafeed formulations tailored for African species such as tilapia and catfish. As of 2025, Africa lacks a commercial-scale algae fermentation facility, which presents a significant opportunity for a regional player to establish a greenfield plant. Such a facility could address key market needs by invoicing in local currency, reducing lead times to 2-4 weeks, and offering customized EPA-to-DHA ratios for African formulators. These capabilities would not only enhance supply chain efficiency but also cater to the specific requirements of the regional market.

Halal certification, provided by Islamic Services of America and recognized across West Africa and the Gulf Cooperation Council, represents a unique and defensible market positioning. Smaller brands can capitalize on this certification to command premium pricing, particularly in Nigeria, where a significant portion of the population practices Islam. By focusing on halal-certified products and addressing localized needs, smaller players can carve out a niche in the market, leveraging cultural and regional preferences to build a competitive advantage.

Africa Algae Omega-3 Ingredients Industry Leaders

-

dsm-firmenich

-

Corbion N.V.

-

Archer-Daniels-Midland Company (ADM)

-

Roquette Frères

-

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ADM expanded its presence in Africa by opening a new facility in the Lagos Free Trade Zone, Nigeria. This facility serves as a regional hub for operations across the continent and supports multiple business lines, including Human Nutrition, Carbohydrate Solutions, and Animal Nutrition. It is designed to foster innovation and collaboration, enabling the local formulation and adaptation of products for regional markets.

- September 2024: DSM‑Firmenich inaugurated a new Animal Nutrition & Health premix and additives manufacturing plant in Sadat City. The facility spans 10,000 m² and boasts an annual production capacity of 10,000 tons. It features modern manufacturing infrastructure provided by Bühler Technologies, including a full plant control system and barcoding for traceability. The plant is built to meet international standards for product quality, safety, and environmental sustainability.

Africa Algae Omega-3 Ingredients Market Report Scope

The Africa algae omega-3 market is segmented by type, concentration, application and by geography. Based on type, the market is segmented into Eicosapentanoic acid (EPA) and Docosahexanoic acid (DHA). Based on concentration the market is segmented as high concentrated, medium concentrated, and low concentrated. Based on application the market is segmented into food and beverages which is further sub-segmented into infant formula and fortified food & beverages; and dietary supplements, pharmaceuticals, animal nutrition and clinical nutrition.Based on geography, the study provides an analysis of the algae omega-3 market in South Africa, Nigeria, Kenya, and rest of Africa.

By Type

| Eicosapentaenoic Acid (EPA) |

| Docosahexaenoic Acid (DHA) |

| EPA/DHA Blends |

By Application

| Food and Beverages |

| Dietary Supplements |

| Infant Formula and Baby Food |

| Other Applications |

By Geography

| South Africa |

| Egypt |

| Nigeria |

| Rest of Africa |

| By Type | Eicosapentaenoic Acid (EPA) |

| Docosahexaenoic Acid (DHA) | |

| EPA/DHA Blends | |

| By Application | Food and Beverages |

| Dietary Supplements | |

| Infant Formula and Baby Food | |

| Other Applications | |

| By Geography | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

Key Questions Answered in the Report

What revenue did the Africa algae omega-3 ingredients market generate in 2026?

The sector recorded USD 22.85 million in 2026 and is projected to climb to USD 32.02 million by 2031.

Which product type leads regional sales?

Docosahexaenoic acid dominates with 61.42% share thanks to widespread infant-formula and cognitive-health usage.

Which country is growing fastest?

Nigeria is forecast to expand at 7.05% CAGR as new NAFDAC rules encourage traceable algae sources and urban health awareness rises.

What factor drives functional-beverage fortification?

Encapsulation advances that mask marine flavors now let plant-based drinks deliver clinically relevant DHA and EPA doses.

Page last updated on: