Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

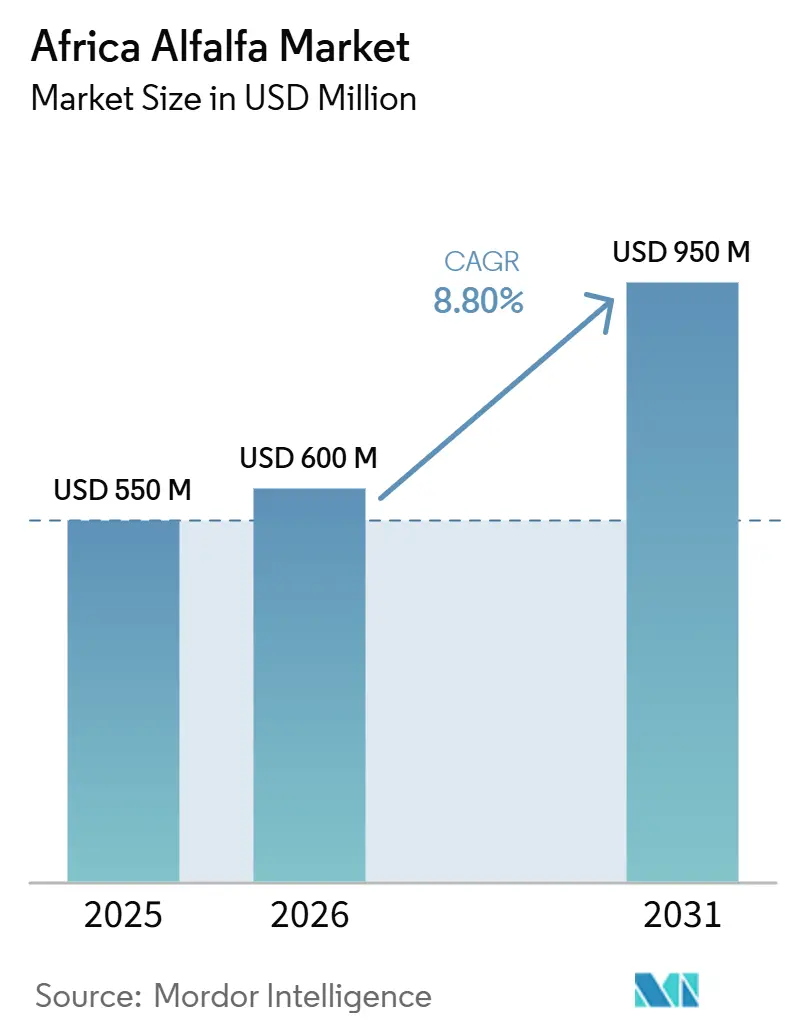

| Base Year Market Size (2025) | USD 550 Million |

| Market Size (2026) | USD 600 Million |

| Market Size (2031) | USD 915 Million |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Alfalfa Market Analysis by Mordor Intelligence

The Africa alfalfa market size has grown from USD 550 million in 2025 to USD 600 million in 2026 and is forecast to reach USD 915 million by 2031, registering a CAGR of 8.8% during 2026-2031. A steady shift in dairy and livestock feeding toward protein-rich rations supports the market, as these rations align more effectively with commercial production systems than open grazing alone. A structural supply gap across several consuming countries also shapes the market, keeping imports and cross-border sourcing central to volume availability through the forecast period. Trade patterns changed in 2025 as tariff action disrupted US alfalfa flows into China, strengthening the value of multi-origin sourcing and flexible trade routing for suppliers serving African buyers. Water stress remains the main operating constraint in North Africa because alfalfa is a water-intensive crop, and several key markets are already managing severe irrigation pressure. Despite this constraint, the market continues to benefit from growth in commercial dairy, feed processing, premium forage demand, and investment in traceable supply chains that can meet stricter quality expectations.

Key Report Takeaways

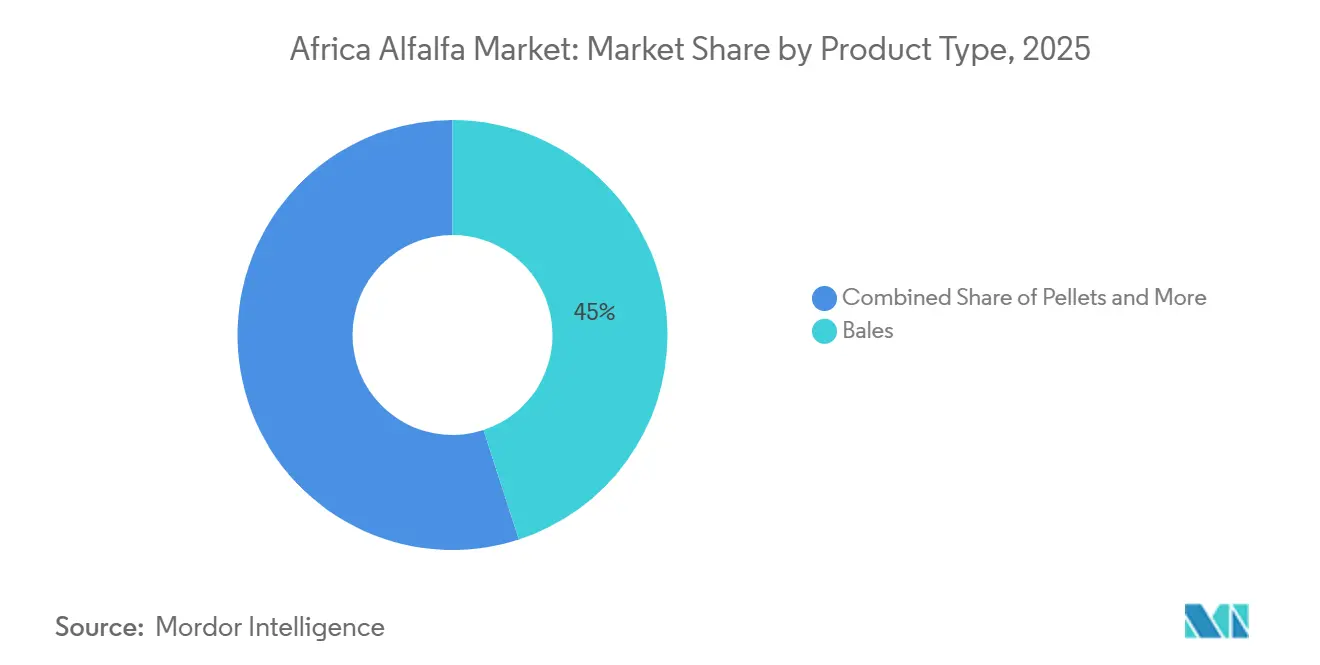

- By product type, bales were the largest segment, with a 45.0% market share of the Africa alfalfa market in 2025, while pellets are forecasted to be the fastest-growing segment, registering a CAGR of 12.2% during 2026 and 2031.

- By application, dairy cattle feed accounted for 39% of the market size in 2025, while poultry feed is projected to record the highest CAGR at 11.3% between 2026 and 2031

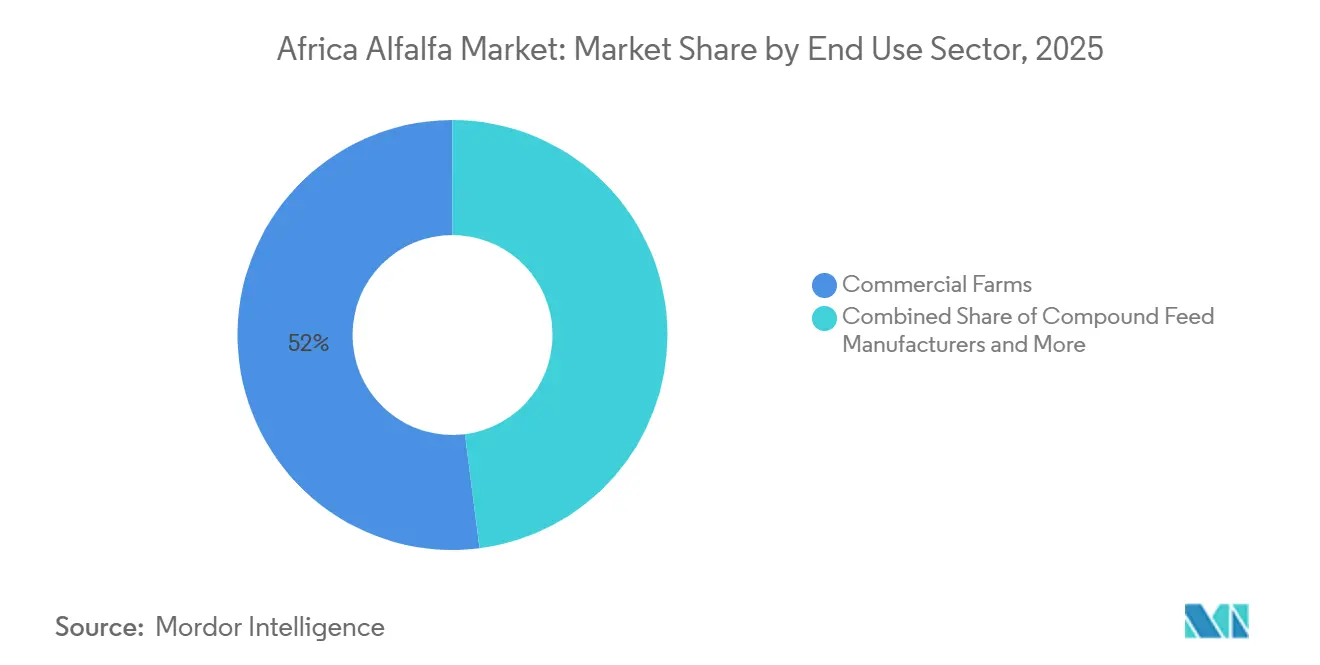

- By end use sector, commercial farms represented 52% of the market in 2025, while pet food and specialty nutrition is forecasted to advance at an 11.4% CAGR between 2026 and 2031.

- By geography, Egypt held 34.50% share in 2025, while Kenya is forecast to grow at the fastest CAGR of 12.0% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for protein-rich dairy feed rations | +2.5% | Africa-wide, with strongest pull in Egypt, Kenya, South Africa, and Nigeria | Medium term (2-4 years) |

| Growth in export-oriented forage markets | +1.8% | Egypt, South Africa, and trade-linked East African markets | Short term (≤ 2 years) |

| Rising preference for organic and non-gmo products | +1.0% | South Africa, Morocco, and premium commercial buyers | Long term (≥ 4 years) |

| Growing carbon credit potential from legume crop rotations | +0.5% | South Africa and selected East and West African commercial farms | Long term (≥ 4 years) |

| Advances in precision drying and moisture management after harvest | +1.0% | Egypt, South Africa, and export-focused processing corridors | Short term (≤ 2 years) |

| Expanding demand from equine and specialty livestock feed | +0.6% | South Africa, Morocco, Kenya, and niche premium buyers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Protein-Rich Dairy Feed Rations

The market is closely linked to the region’s dairy feed transition, as commercial farms shift from low-yield feeding systems to more balanced rations. Alfalfa remains central to this transition because its protein density supports total mixed ration programs used by modern dairy operations. This dynamic stabilizes demand in countries where processors consistently reward higher milk volume and quality. The shift is also extending beyond large farms, as cooperative-linked producers increasingly adopt structured feed programs to improve herd output and milk quality.

Growth in Export-Oriented Forage Markets

Global forage trade dynamics will also shape the market, with supply resilience becoming as important as price. In early 2025, China imposed a 125% tariff on U.S. alfalfa, disrupting trade flows before lowering the levy to 7% in May 2025[1]Source: Al Dahra, “How US-China Tariffs Disrupted Alfalfa Trade—and Al Dahra Secured Global Supply with a Multi-Origin Model,” aldahra.com. This kind of policy shock is likely to push suppliers to diversify destination markets and reroute volumes more flexibly. For Africa, Egypt and South Africa may emerge as practical buffer markets for buyers seeking continuity of supply. The trend should further strengthen multi-origin procurement strategies among import-dependent customers across the region. Suppliers with access to multiple production origins will therefore be better positioned to absorb freight disruptions, policy shifts, and demand swings.

Rising Preference for Organic and Non-Gmo Products

The market is beginning to develop a premium tier, where traceability, residue control, and verified growing practices add value. This trend is most important in commercial dairy, equine, and specialty nutrition channels, where buyers are less willing to accept feed variability. Al Dahra’s 2024 sustainability disclosures showed an expansion of reduced-disturbance and no-till practices in Romania, supporting a traceability model relevant to premium export channels serving African buyers[3]Source: Al Dahra, “2024 Sustainability Report,” aldahra.com. However, certification systems remain uneven across African markets, limiting domestic premium supply. Even so, the market is moving toward a structure where documented quality can generate stronger buyer loyalty than undifferentiated bulk supply.

Growing Carbon Credit Potential from Legume Crop Rotations

The Africa alfalfa market benefits from alfalfa’s role in rotation systems on larger commercial farms, particularly in areas where soil exhaustion and declining land productivity are becoming more visible constraints. As a nitrogen-fixing perennial legume, alfalfa improves soil structure, reduces fertilizer dependence, and supports long-term field productivity. A 2024 study on legume-based systems by Ahmadu Bello University found stronger soil carbon outcomes than continuous monocropping, reinforcing the agronomic case for forage rotations. This factor is particularly relevant for larger farms and organized growers that can capture productivity gains and potential carbon-linked income. Over time, these benefits may influence acreage decisions beyond short-term forage pricing..

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water availability constraints and irrigation policy challenges | -1.8% | North Africa, with spillover into water-stressed East African zones | Long term (≥ 4 years) |

| Freight volatility and export logistics risk | -1.5% | Africa-wide, with strongest impact in inland and landlocked markets | Short term (≤ 2 years) |

| Competitive pressure from grass hay and silage alternatives | -1.2% | Sub-Saharan African smallholder and informal feed systems | Medium term (2-4 years) |

| Compliance challenges related to phytosanitary standards and residue limits | -0.7% | Export and import corridors centered on Egypt, South Africa, Kenya, and Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water Availability Constraints and Irrigation Policy Challenges

Water scarcity remains the clearest long-term restraint on the African alfalfa market, as alfalfa requires 400-600 m³ of water per metric ton of dry matter. Morocco has experienced six consecutive years of drought since 2018 to 2025, and pressure remains more severe because much of its cultivated land relies on rain-fed conditions. Algeria also faces rising irrigation demand, which could exceed sustainable aquifer recharge if current patterns continue. The issue extends to Egypt, where the largest consuming market must manage both domestic feed demand and the water cost embedded in forage production amid tighter Nile-related pressures. These conditions increase local production costs and limit how quickly the African alfalfa market can expand through domestic acreage alone.

Volatility in Freight Costs and Export Logistics

Freight remains a structural drag on the market, as many demand centers are far from ports, processing units, and reliable storage points. Long inland routes increase delivered costs and reduce the attractiveness of transporting low-value bulk products for suppliers. This challenge is more acute in landlocked and interior regions, where road-heavy logistics dominate and route efficiency remains weak. It also affects exporters, as rate volatility can quickly erode margins in a product for which transport accounts for a large share of the final value. As a result, the market continues to depend heavily on operators that can manage multi-leg logistics while maintaining quality and pricing discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pellet Adoption Reshaping Inland Supply Economics

Bales retained a 45% market share of the Africa alfalfa market in 2025, reflecting the format’s suitability for low-infrastructure handling across dairy and livestock farms. Farmers can store 50-100-kilogram bales in basic sheds and move them without specialized handling systems, making them practical for small and mid-sized operators. Compressed bales continue to support export-oriented trade, where container efficiency matters more than farm-level convenience. Cubes remain a smaller but stable format for buyers who require cleaner handling and more uniform feed quality.

Pellets are the fastest-growing product type in the market and are projected to register a 12.2% CAGR between 2026 and 2031. Their appeal is strongest among urban-fringe feed mills and integrated livestock systems that already use automated handling. Pellets reduce transport inefficiencies, extend storage life, and fit mechanized feeding lines more easily than loose or standard baled forage. This trend is gradually shifting the industry away from format decisions based solely on basic availability and toward choices driven by logistics efficiency and processing compatibility. Over time, wider power access and improved feed infrastructure are anticipated to narrow the gap between traditional bales and higher-density processed formats.

By Application: Poultry Feed Emerging as the High-Growth Demand Vector

Dairy cattle feed accounted for 39% of the market size in 2025, reflecting the crop’s established role in protein-rich rations for confinement and semi-confinement dairy systems. This application remains the anchor of the demand structure, as dairy buyers place a higher value on nutrient consistency and repeat procurement. Beef cattle and small ruminant feed contribute a steady volume, but these segments are typically more seasonal and price sensitive. Camelid demand remains niche and concentrated in a limited set of livestock systems across the Horn of Africa.

Poultry feed is the fastest-growing market segment and is forecast to register a 11.3% CAGR between 2026 and 2031. The expansion of broiler and layer operations is driving this growth, as these operations increasingly adopt structured feed programs to improve yield and product quality. Alfalfa meal supports this shift by serving as a concentrated supplement in automated feeding systems and enabling product differentiation linked to natural pigmentation and feed quality. The African alfalfa industry also benefits, as poultry buyers often operate through formal feed channels rather than informal farmgate forage trade. If domestic cultivation projects scale successfully in countries such as Nigeria, poultry demand could eventually be met through a more localized balance of farm production and processing.

By End Use Sector: Commercial Farms Lead, While Specialty Buyers Raise the Margin Ceiling

Commercial farms accounted for 52% of the market in 2025, making them the largest end-use group by value. Their leadership is supported by scale, contract-based procurement, and a greater willingness to pay for consistent protein quality. These farms include large dairy units, beef feedlots, and integrated poultry businesses that rely on predictable forage quality rather than opportunistic seasonal purchases. Compound feed manufacturers represent the next layer of demand, as they use alfalfa as a concentrated ingredient in commercial blends and benefit from direct supplier negotiations.

Pet food and specialty nutrition is forecasted to grow at a CAGR of 11.4% between 2026 and 2031, making it the fastest-growing end-use segment in the market. This channel remains small, but it offers better pricing for documented origin, low residue levels, and stable analytical quality. Household and hobby animal owners remain fragmented and primarily bale-oriented, so their purchases are still more closely tied to local availability than to feed specifications. This contrast is pushing the industry toward a more segmented demand model, in which premium processors can direct small volumes into higher-value channels without relying on mass-market expansion. Suppliers that already serve export-grade buyers are well positioned, as the quality standards required for specialty nutrition overlap with the controls used in formal trade.

Geography Analysis

Egypt holds 34.50% of the market share in 2025, making it the largest country market in the region. This position reflects its well-established dairy and feed base, supported by irrigated production systems and a large domestic livestock economy. Egypt also serves as a regional trade platform, giving it influence over pricing, sourcing, and processing. South Africa remains another important node in the Africa alfalfa market, as it combines domestic demand with export-oriented capabilities and a stronger base in formal livestock nutrition.

Kenya is the fastest-growing country in the market and is projected to register a 12.0% CAGR between 2026 and 2031. Its growth reflects the link between forage development and improvements in the dairy system. ILRI-backed programs have expanded bundled forage interventions across multiple regions and reached 50,000 farmers in 2026. Kenya’s long-term importance is also supported by Al Dahra’s memorandum of understanding in 2025 with the government to develop 200,000 acres of irrigated farmland at Galana-Kulalu Ranch. This combination of policy support, production ambition, and formal livestock demand gives the market a stronger structural base than a simple import-driven growth story would suggest.

Nigeria and Ethiopia are emerging demand frontiers within the market, but their growth paths differ. Ethiopia has advanced through ILRI-led climate-smart forage packages, where alfalfa forms part of a broader productivity model rather than serving as a stand-alone commercial crop[2]Source: International Livestock Research Institute, “In Ethiopia, bundled forage innovations are closing the livestock feed gap,” ilri.org . Nigeria’s growth route is more investment driven, with new cultivation efforts testing the extent to which domestic supply can substitute imports in commercial livestock systems. Morocco and Algeria remain important consuming areas, but severe water pressure leaves both markets structurally exposed to supply constraints and import reliance.

Competitive Landscape

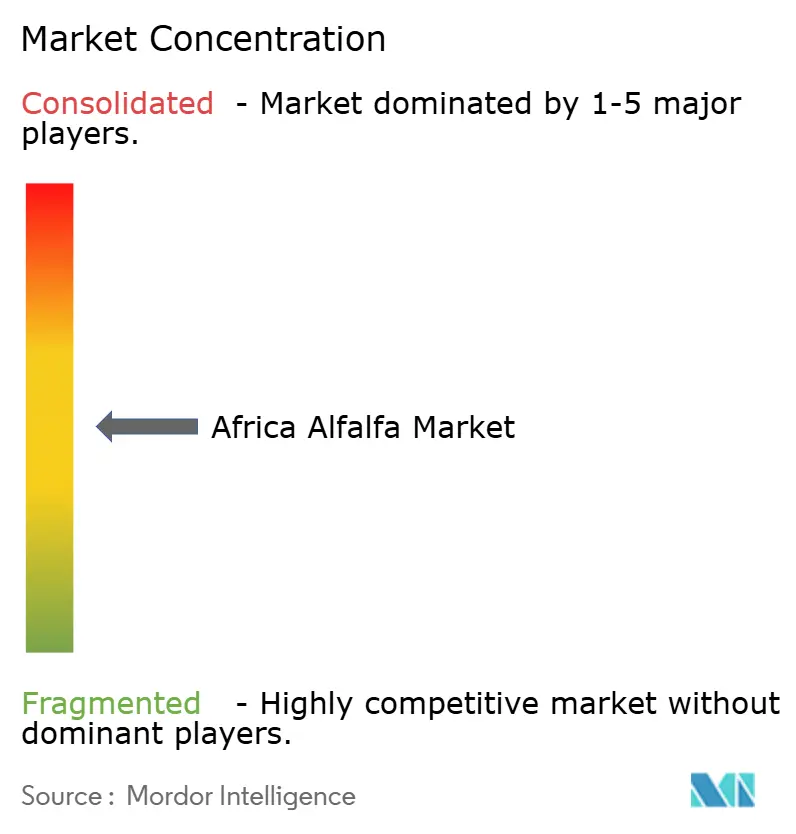

The top five players in the market accounted for a major share of revenue in 2025, indicating moderate concentration rather than dominance by a small group of suppliers. Al Dahra ACX Global Inc. led the market , supported by its ability to supply buyers from multiple production origins instead of relying on a single geography. This multi-origin model became more valuable during the 2025 tariff shock, which reshaped trade routes and redirected volumes across destination markets. Anderson Hay and Grain Inc.'s restructuring process has created uncertainty around its near-term operating profile. This situation creates room for mid-tier suppliers to compete more actively across North and East African corridors.

Competition in the market is shifting from basic trading scale toward processing quality, supply resilience, and compliance capability. Suppliers with pelletization, moisture control, and advanced storage systems can preserve value more effectively across long inland routes and formal feed chains. Al Dahra’s reported shift in 2025 to biomass-powered dehydration in Spain demonstrates a strategic effort to improve processing efficiency and quality control at origin. Its Kenya farmland agreement also supports future origin diversification linked to African demand growth, rather than relying only on overseas production hubs. These initiatives raise the competitive threshold for companies that still depend mainly on conventional bale trade without stronger infrastructure or traceability.

The Africa alfalfa market still offers white space for players that can serve premium channels and underdeveloped inland markets with consistent quality. The next stage of competition will likely depend on which companies can combine trade flexibility, technical processing, and standards compliance at a repeatable cost. Carbon-linked rotation systems and premium forage traceability add another layer of differentiation because they align with the needs of specialty buyers and formal livestock operations. This dynamic keeps the market open to competition, even as larger multinational suppliers continue to set the pace in the most structured trade corridors.

Africa Alfalfa Industry Leaders

Al Dahra ACX Global Inc.

Anderson Hay and Grain Inc.

Border Valley Trading

Alfalfa Monegros SL

Grupo Osés Agroalimentaria S.L. (NAFOSA S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Al Dahra’s EUR 20 million (USD 22.8 million) Serbia investment in 2026 is anticipated to strengthen its alfalfa supply base by improving irrigation, logistics, and drainage. The upgrade can boost output reliability and export readiness, supporting multi-origin sourcing into Africa as demand rises.

- June 2025: Al Dahra’s sixth consecutive Sustainability Report reinforces its long-term alfalfa supply strategy, with regenerative and reduced-disturbance farming now covering about 76% of cultivated land in Romania. The company also reiterated its ambition to expand its global farmland footprint from roughly 100,000 hectares toward 500,000 hectares, signaling a larger and more resilient production base for forage supply.

- December 2025: The Jigawa State Government of Nigeria and El-Meena Farms Ltd launched a USD 540 million public-private alfalfa development project, selecting Saudi Arabia's Alkhorayef Group as the irrigation infrastructure partner. The initiative targets 100,000 hectares, 2.0 million metric tons of annual alfalfa output, and over 100,000 direct jobs, with projected annual export revenues of USD 440–540 million to Gulf markets.

Africa Alfalfa Market Report Scope

Alfalfa hay is obtained from the alfalfa plant, also known as lucerne and Medicago sativa. It is cultivated as an important forage crop and is widely used in animal nutrition because of its high protein content and forage value.

The Africa Alfalfa Market is Segmented by Product Type (Bales, Pellets, Cubes, and Compressed Bales), by Application (Dairy Cattle Feed, Beef Cattle Feed, Poultry Feed, Equine Feed, Small Ruminant Feed, Camelids and Other Livestock Feed), by End Use Sector (Commercial Farms, Compound Feed Manufacturers, Household And Hobby Animal Owners, and Pet Food and Specialty Nutrition), and by Geography (Egypt, South Africa, Kenya, Morocco, Algeria, Nigeria, Ethiopia, and Rest Of Africa). The Market Size and Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

By Geography

| Egypt |

| South Africa |

| Kenya |

| Morocco |

| Algeria |

| Nigeria |

| Ethiopia |

| Rest of Africa |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition | |

| By Geography | Egypt |

| South Africa | |

| Kenya | |

| Morocco | |

| Algeria | |

| Nigeria | |

| Ethiopia | |

| Rest of Africa |

Key Questions Answered in the Report

What is the forecasted value of Africa alfalfa market by 2031?

The Africa alfalfa market is forecast to reach USD 915 million by 2031 from USD 600 million in 2026, advancing at a 8.80% CAGR over 2026-2031.

Which product type leads demand across the market?

Bales led in 2025 with 45% of market share as they fit low-infrastructure storage and handling needs across dairy and livestock farms.

Which end users drive the most revenue in market?

Commercial farms accounted for 52% of 2025 value because they buy on contract and place higher weight on protein consistency and repeat supply.

Which country has the strongest current position in Africa alfalfa?

Egypt held 34.50% share in 2025, making it the largest country market, while Kenya is projected to record the fastest growth at 12.00% CAGR.

What is the main long-term risk for the supply growth?

Water scarcity is the main structural risk because alfalfa is water intensive and major North African markets are already under severe irrigation pressure.

Page last updated on: