Active Noise And Vibration Control (ANVC) System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

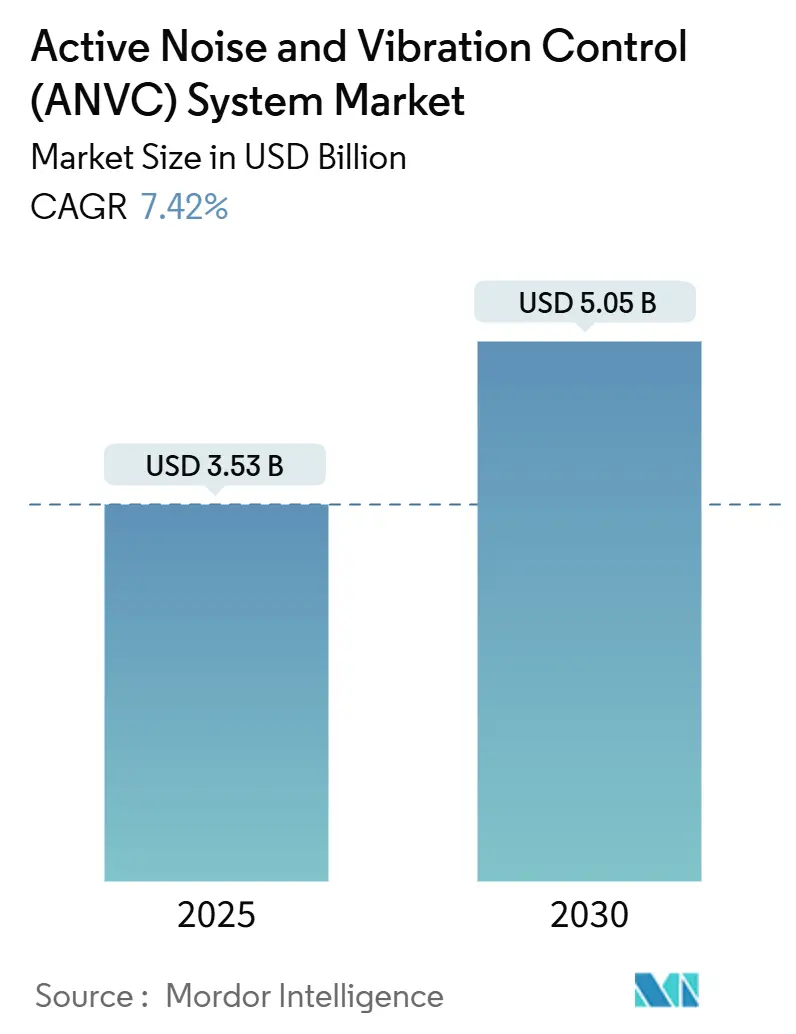

| Market Size (2025) | USD 3.53 Billion |

| Market Size (2030) | USD 5.05 Billion |

| Growth Rate (2025 - 2030) | 7.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active Noise And Vibration Control (ANVC) System Market Analysis by Mordor Intelligence

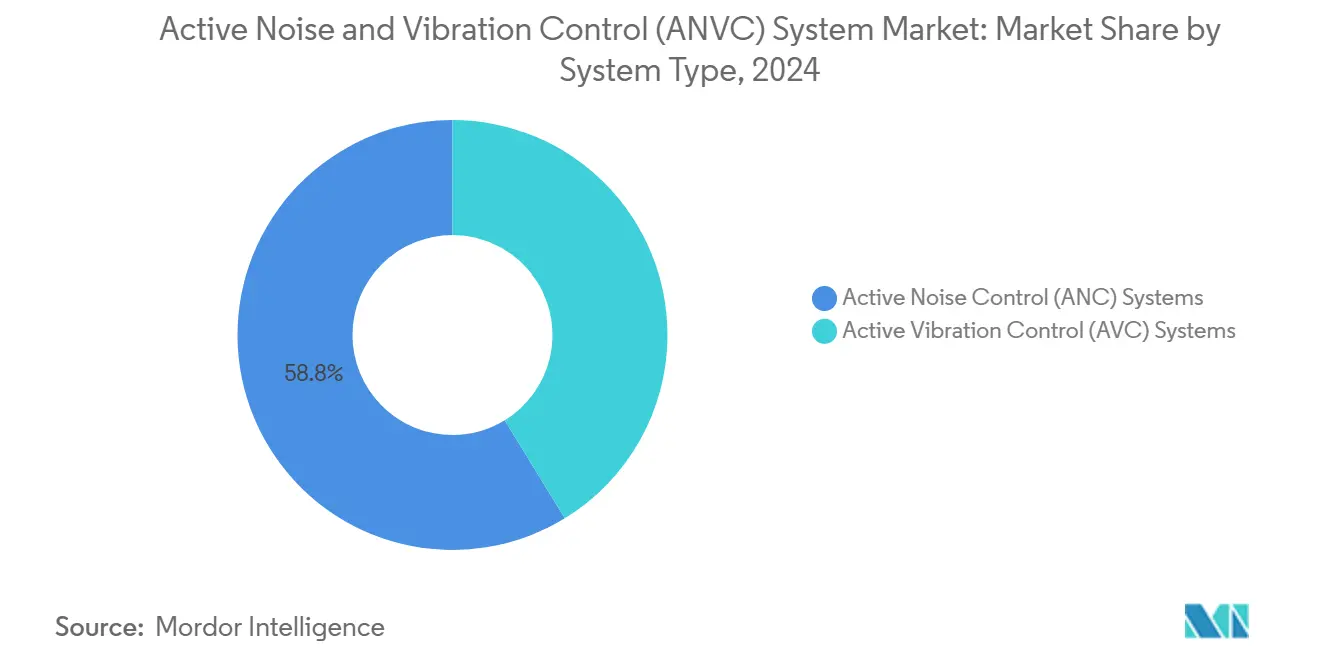

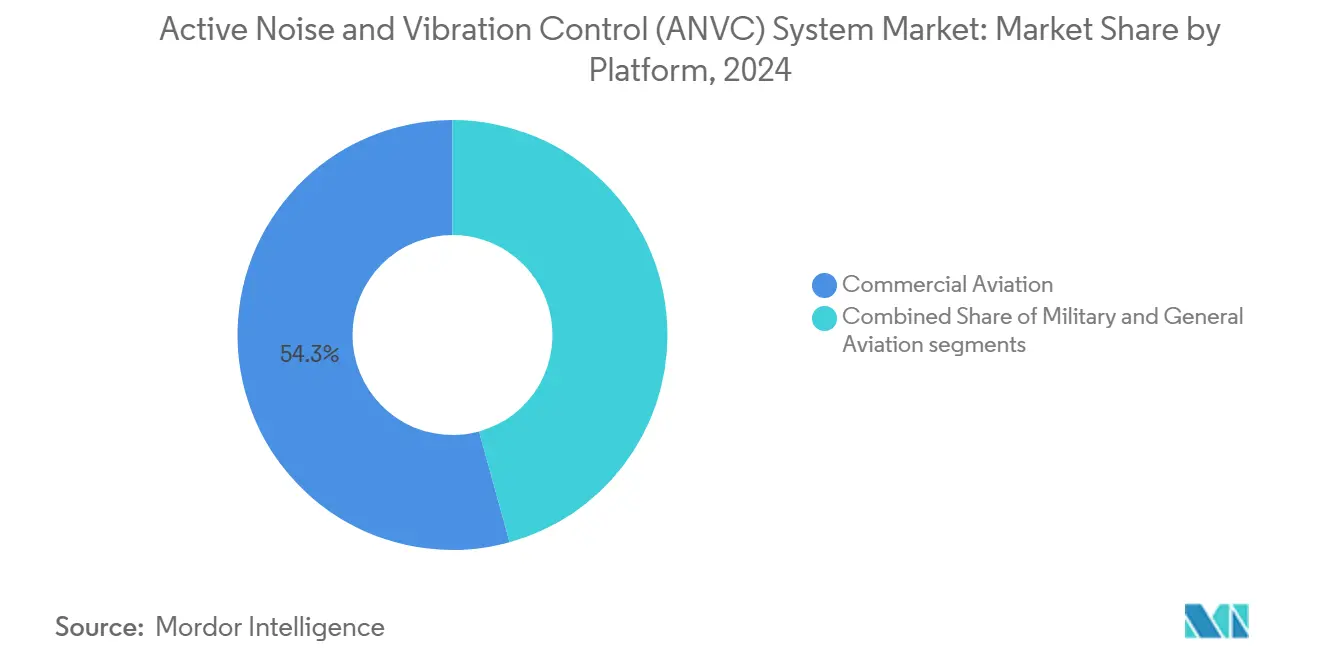

The active noise and vibration control (AVNC) system market size reached USD 3.53 billion in 2025 and is forecasted to reach USD 5.05 billion by 2030, expanding at a 7.42% CAGR during the forecast period. Electrification in vehicles and aircraft, stricter global noise regulations, and premium-segment comfort expectations jointly reinforce demand for adaptive noise and vibration suppression technologies. North America led with 40.24% revenue in 2024 on the back of stringent automotive NVH benchmarks and defense procurement of acoustic stealth systems, while Asia-Pacific registered the fastest 8.45% CAGR due to China’s electric-vehicle output and new airport construction throughout India and Southeast Asia. Across platforms, commercial aviation generated 54.28% of 2024 sales as airlines balanced ride quality with fuel-saving weight targets. Hardware retained a 73.45% share, yet software grew quickly at 8.21% as AI algorithms and digital twins refined real-time control logic. Active noise control (ANC) systems remained the dominant solution, holding 58.75% share in 2024 and expanding at 7.94% CAGR amid broad automotive, aviation, and industrial adoption.

Key Report Takeaways

- By system type, ANC systems commanded 58.75% of 2024 revenue and are advancing at a 7.94% CAGR through 2030.

- By component, hardware held a 73.45% share in 2024, while software is projected to rise at an 8.21% CAGR over 2025-2030.

- By platform, commercial aviation captured 54.28% 2024 revenue, whereas general aviation is on track for the fastest 8.72% CAGR to 2030.

- By geography, North America represented 40.24% of 2024 sales, yet Asia-Pacific is poised for an 8.45% CAGR through 2030.

Global Active Noise And Vibration Control (ANVC) System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cabin noise complexity from electric and hybrid powertrain adoption | +1.2% | Global (early gains in Europe, North America) | Medium term (2-4 years) |

| Strengthening noise and vibration compliance regulations | +0.9% | Global (strict EU, North America enforcement) | Long term (≥ 4 years) |

| Rising demand for passenger comfort in premium automotive and aviation segments | +1.5% | North America, Europe, Asia-Pacific premium routes | Short term (≤ 2 years) |

| Integration of digital twin and AI technologies for real-time vibration and noise optimization | +1.8% | Global (tech leadership in North America, Asia-Pacific) | Medium term (2-4 years) |

| Expanding defense investments in active acoustic signature suppression systems | +1.1% | North America, Asia-Pacific, Europe | Long term (≥ 4 years) |

| Increased OEM focus on holistic NVH (Noise, Vibration, Harshness) performance differentiation | +0.9% | Global aerospace hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cabin Noise Complexity from Electric and Hybrid Powertrain Adoption

With combustion roar gone, electric propulsion elevates gear-mesh, inverter-switching, and aerodynamic broadband noise that peaks between 700 Hz and 1.6 kHz. Active solutions must track fast torque changes as motors throttle from 20% to 100% power in three seconds, forcing controller bandwidth above 3 kHz. Structural modes that once sat outside the audible range now couple with cabin panels, driving redesign of sensor layouts. Early demonstrator fleets show that integrating tunable actuators into battery enclosures cuts cabin SPL by 6 dB without thick liners, saving 18 kg per fuselage section. The retrofit backlog is large, but owners weigh acoustic gains against downtime and recertification paperwork.

Integration of Digital Twin and AI Technologies for Real-Time Optimization

Digital-twin models fed by in-flight sensor data create a closed loop that predicts cabin acoustics and updates control laws every few milliseconds, raising performance certainty in variable flight profiles.[1]NASA, “Aeronautical Engineering: A Continuing Bibliography,” nasa.gov AI-enhanced controllers shorten the tuning cycle from hours to minutes, which improves line-fit economics for narrowbody programs. Defense labs adapt the same framework to helicopter rotor noise, letting crews vary acoustic signatures in contested airspace. Suppliers now embed cybersecurity hardening in firmware because adversaries could spoof reference signals and reveal mission positions. The biggest hurdle is cross-domain certification, as regulators must validate both the physical model and the adaptive code for every update.

Rising Demand for Passenger Comfort in Premium Automotive and Aviation Segments

Business jet operators advertise sub-60 dB cabins on six-hour legs, a target enabled only by broadband active linings that cancel tonal components below 500 Hz. Airlines retrofit premium-economy cabins with distributed headrest actuators that attenuate 8 to 12 dB in mid-frequency bands, increasing Net Promoter Scores on trans-Pacific routes. Electric regional aircraft intensify the need because motor whine exposes secondary HVAC and airframe noises that turbofans used to mask. Certification teams demonstrate compliance with ICAO Chapter 14 by combining structural damping and active cancellation, preserving weight budgets. The result is a new upsell tier where seat makers and noise control suppliers co-package wellness metrics such as cognitive-fatigue reduction for pilots and passengers.

Expanding Defense Investment in Acoustic-Signature Suppression Systems

Modern battle networks employ acoustic detection arrays that cue loitering munitions within 180 seconds, so armed forces fund suppression kits that drop helicopter external noise by 9–12 dB in hover.[2]Josh Luckenbaugh, “Army Making Moves in Signature Management Chess Match,” National Defense Magazine, nationaldefensemagazine.org Fighter programs add helmet-mounted units that cancel cockpit tones above 105 dB, boosting radio intelligibility at 8 g. Drone manufacturers pursue “signature-swap” modules that overlay fake tonal patterns to mislead passive sensors. Projects demand MIL-STD-461 compliance, which lengthens system-integration schedules, but premium pricing offsets R&D risk. Suppliers that pair vibration control for avionics racks with wideband acoustic cancellation win multiyear sustainment contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit and integration costs for legacy vehicle and platform fleets | -1.4% | Global (older aircraft regions) | Short term (≤ 2 years) |

| Performance reliability limitations in extreme temperature and operational environments | -0.8% | Global (harsh military zones) | Medium term (2-4 years) |

| Fragmented intellectual property landscape hindering technology standardization | -0.6% | Global (aerospace hubs) | Long term (≥ 4 years) |

| Cybersecurity concerns related to algorithm-driven control systems | -0.9% | Global (defense, critical infrastructure) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit and Integration Costs for Legacy Fleets

Installing a full cabin cancellation suite on a 1990s-era widebody requires structural reinforcements, new wiring harnesses, and supplemental type certification that can exceed USD 15 million per aircraft. Military transports must also validate electromagnetic compatibility with avionics, adding 1,200 labor-hours per frame. Smaller charter operators delay upgrades until heavy check intervals to avoid extra downtime, stretching payback periods to eight years. Modular lining panels with embedded virtual microphones promise 30% labor savings, yet they face limited field data. Leasing companies push for portable head-rest modules that avoid airframe modification, but acoustic performance falls below crew rest thresholds on long-haul segments.

Cybersecurity Concerns Related to Algorithm-Driven Control Systems

Air traffic cyberattacks in 2025 exposed vulnerabilities where threat actors injected false reference signals, causing control loops to amplify noise instead of canceling it. Regulators responded by requiring post-quantum cryptographic authentication for firmware updates, which adds latency and raises processor loads by 18%. Military programs demand dual-core lockstep architectures so a companion core validates every control command in microseconds. While these safeguards slow time-to-market, they also open niches for suppliers of low-power hardware encryption. Airlines now allocate budget lines for penetration testing during cabin-retrofit bids, making cybersecurity maturity a procurement differentiator.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: ANC Systems Maintain Broadband Leadership

ANC units delivered 58.75% of 2024 revenue as part of the AVNC system market share, owing to proven broadband effectiveness below 500 Hz, where passive liners struggle.[3]Kay Kochan et al., “Active Noise Control inside the Loadmaster Area of a Turboprop Transport Aircraft,” AIAA, aiaa.org After airlines switched to distributed feed-forward controllers, commercial widebody cabins recorded 10-20 dB reductions on mid-deck sections. Military transports apply the same technology to loadmaster stations, using multi-input multi-output architectures that adapt to cargo-bay reverberation patterns. The AVNC system market size for ANC solutions is projected to expand at a 7.94% CAGR, underpinned by AI-driven algorithms that auto-identify secondary paths during flight. Vibration-control counterparts focus on shunt-damping fuselage frames and rotorcraft blade-pass frequencies, but they trail in volume because of heavier actuators.

ANC suppliers embed virtual microphone arrays to lower sensor counts from 32 to 12, reducing wiring mass by 6 kg per frame. European demonstrators' flight-test data show performance is within ±2 dB during temperature swings from -20 °C to 55 °C. However, extreme desert operations can double secondary-path variance, requiring thermal compensation tables that lengthen calibration. OEMs bundle ANC with other cabin-wellness packages, capturing premiums of USD 150,000 per ship-set on business jets.

By Component: Software Rises as Strategic Multiplier

Hardware commanded 73.45% of 2024 sales, reflecting expensive amplifiers, piezo actuators, and MEMS sensor arrays that form the backbone of any active system. Yet software is the fastest-growing component, expected to log an 8.21% CAGR through 2030 as fleets upgrade digital signal processing stacks. Edge AI libraries compress computational loads to fit eight-channel controllers on single-board computers, freeing cockpit rack space. Cloud-derived models upload anonymized acoustic data, refine adaptive filters offline, and push optimized coefficients during overnight maintenance windows. This iterative workflow boosts in-service SPL reduction by 1–3 dB during the first six months of operation.

Code reuse across platforms gives suppliers licensing leverage: a certified control kernel ported from a widebody to a tilt-rotor can save USD 4 million in validation effort. Despite growth, software still depends on reliable hardware paths; actuator saturation or sensor drift will collapse control authority. Therefore, leading vendors co-design firmware and power amplifiers, chasing closed-loop latency below 0.8 ms to retain phase margin at kilohertz bandwidths.

By Platform: General Aviation Shows Highest Momentum

Commercial aviation held a 54.28% revenue share in 2024 due to a large fleet size and tight noise regulations on long-haul routes. Airlines upgrade new-build narrowbodies with factory-installed ANC liners that shave 15 kg compared with thicker passive kits, offsetting the weight of extra seats. In contrast, general aviation is the fastest-growing platform, forecast at an 8.72% CAGR to 2030 as owners of USD 70 million business jets seek ultra-quiet cabins for transcontinental trips. These operators approve capital upgrades quickly because quiet interiors directly translate into perceived luxury and resale value.

Helicopter EMS operators adopt vibration control to cut medical-equipment failure rates, opening cross-selling for cabin acoustics. Military combat aircraft invest in pilot helmet ANC, but integration with oxygen masks introduces feedback paths that lower achievable attenuation. Suppliers respond with hybrid bone-conduction reference sensors that maintain 15 dB cancellation under 9 g loads. Across all platforms, OEMs market low-noise branding to win airport slots as community metrics become part of landing-fee formulas.

Geography Analysis

North America led the AVNC system market in 2024 with a 40.24% revenue share, driven by robust defense budgets and a dense cluster of aerospace OEMs. Programs like the US Army’s signature-management trials demand cockpit systems that modulate acoustic profiles within three-minute shoot-and-scoot timelines. US commercial carriers accelerate narrowbody retrofits to meet new FAA community-noise rules that tighten night-time SPL limits around major hubs. Suppliers benefit from a mature maintenance ecosystem, although cyber incidents at several airports in 2025 have added compliance layers to software certification.

Asia-Pacific is the fastest-growing region, projected at an 8.45% CAGR through 2030, reflecting rising fighter procurement and expanding final-assembly lines in China, Japan, and South Korea. For example, the Republic of Korea Air Force evaluates ANC headsets that cut cockpit noise from 105 dB to 93 dB, expecting to roll out fleetwide within three years. Chinese OEMs localize actuator production to reduce import dependency, while Japanese tier-ones collaborate with European sensor firms on high-temperature MEMS arrays. Supply-chain disruptions remain a short-term hurdle, but government grants under aerospace self-reliance programs offset cost inflation and sustain demand.

Europe contributes a steady volume through strict EASA noise frameworks that force every new type certificate to demonstrate cumulative margins below Chapter 14 thresholds.[4]European Union Aviation Safety Agency, “Technology and Design,” easa.europa.eu Clean-Sky projects fund active-lining prototypes that blend structural and acoustical functions, decreasing cabin SPL without increasing fuselage weight. Manufacturers in France and Germany integrate metamaterial panels that work alongside ANC, targeting 5 dB extra attenuation in the 250 Hz band. Brexit-related customs checks slow component flow to the United Kingdom, nudging OEMs toward continental suppliers. Meanwhile, urban air mobility ventures in Italy and Spain treat low noise as a licensing prerequisite, pushing rapid adoption of lightweight ANC modules.

Competitive Landscape

The AVNC system market remains moderately fragmented, with the top five suppliers holding more than 30% of global sales. Aerospace specialists like Moog and Tenneco focus on high-force actuators for structural vibration tasks. Intellectual-property overlap among Boeing, Airbus, and control-algorithm vendors spawns cross-licensing deals that raise barriers for new entrants. Vertical integration is a central theme: Honeywell’s 2025 acquisition of CAES extends its control stack into RF domains, enabling combined acoustic and electromagnetic signature management for defense aircraft.

Strategic moves also center on European consolidation. TriMas bought GMT Aerospace to add structural damping expertise to complement its anti-vibration mounts. KPS Capital Partners combined multiple acoustic brands under Catalyst Acoustics Group to serve broader aviation and industrial bases. Yet scaling remains difficult because each airframe needs custom secondary-path modeling, which inflates engineering costs.

Cybersecurity capability emerges as a new differentiator. Vendors that ship controllers with hardware root-of-trust and post-quantum algorithms win defense programs where firmware integrity is mission-critical. At the same time, companies that offer combined vibration, acoustic, and condition-monitoring packages capture long-term health-management revenue streams. The competitive environment, therefore, rewards firms that integrate multi-physics modeling, secure digital updates, and global MRO support in one offering.

Active Noise And Vibration Control (ANVC) System Industry Leaders

Moog Inc.

HUTCHINSON S.A.

Bosch General Aviation Technology GmbH (Robert Bosch GmbH)

Ultra Precision Control Systems (Ultra Electronics Holdings Limited)

Parker-Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bell Boeing Joint Project Office (JPO) received a USD 46 million contract to integrate the V-22 Gearbox Vibration Monitoring/Osprey Drive System Safety and Health Information (ODSSHI) system, which includes 91 ODSSHI kits and spare parts.

- March 2025: Insta Group and Saab AB expanded their collaboration to enhance the Insta Active Noise Reduction (ANR) solution. The partnership focuses on customizing the Insta ANR system for future fighter helmets, optimizing performance across various operational scenarios, and ensuring reliable communication in challenging conditions.

Global Active Noise And Vibration Control (ANVC) System Market Report Scope

| Active Noise Control (ANC) Systems |

| Active Vibration Control (AVC) Systems |

| Hardware |

| Software |

| Commercial Aviation | Widebody |

| Narrowbody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Missions | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System Type | Active Noise Control (ANC) Systems | ||

| Active Vibration Control (AVC) Systems | |||

| By Component | Hardware | ||

| Software | |||

| By Platform | Commercial Aviation | Widebody | |

| Narrowbody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Missions | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue level does the Active Noise and Vibration Control System market reach by 2030?

The AVNC system market was valued at USD 3.53 billion in 2025 and is forecasted to reach USD 5.05 billion by 2030, expanding at a 7.42% CAGR during the forecast period.

Which system type holds the largest share today?

Active noise control systems account for 58.75% of 2024 revenue because of broadband effectiveness in low-frequency bands.

Which platform segment is growing fastest?

General aviation shows the highest 8.72% CAGR as business jet owners seek quieter cabins.

Why is Asia-Pacific expanding more rapidly than other regions?

Rising defense aviation budgets and new commercial aircraft assembly lines drive an 8.45% CAGR through 2030.

How are cybersecurity requirements affecting adoption?

New regulations mandate post-quantum authentication for control firmware, increasing validation time but opening niches for secure hardware suppliers.

What recent Mergers and Acquisitions activity shapes competition?

Deals such as Honeywell–CAES and TriMas–GMT Aerospace illustrate vertical integration that bundles actuators, algorithms, and secure electronics.

Page last updated on: