Tamaño y Participación del Mercado de Ingredientes de Proteína de Guisante de América del Norte

Visión General del Mercado

| Período de Estudio | 2021 - 2031 |

|---|---|

| Período de Datos Pronosticados | 2025 - 2031 |

| Período de Datos Históricos | 2021 - 2024 |

| Tamaño del Mercado (2026) | 511.92 Millones de dólares |

| Tamaño del Mercado (2031) | 633.68 Millones de dólares |

| Tasa de crecimiento (2025 - 2031) | 4.36% CAGR |

| Concentración del Mercado | Medio |

Jugadores principales *Nota aclaratoria: los principales jugadores no se ordenaron de un modo en especial Imagen © Mordor Intelligence. El uso requiere atribución según CC BY 4.0. | |

Análisis del Mercado de Ingredientes de Proteína de Guisante de América del Norte por Mordor Intelligence

El Mercado de Ingredientes de Proteína de Guisante de América del Norte fue valorado en USD 511,92 millones en 2026 y se proyecta que alcance USD 633,68 millones en 2031, registrando una tasa de crecimiento anual compuesta (CAGR) del 4,36% durante el período de previsión. Este crecimiento está impulsado principalmente por el creciente cambio hacia la nutrición de origen vegetal, ya que los consumidores priorizan fuentes de proteínas que se alinean con valores de salud, sostenibilidad y ética. La proteína de guisante ha ganado una popularidad significativa debido a su origen vegetal, propiedades hipoalergénicas y versatilidad en aplicaciones de alimentos, piensos y nutrición. Sirve como alternativa preferida a las proteínas de origen animal y a las proteínas con alto contenido alergénico. La creciente adopción de dietas veganas y flexitarianas, junto con la tendencia creciente de la fortificación proteica en alimentos cotidianos y suplementos, continúa expandiendo la base de consumidores potenciales del mercado.

Conclusiones Clave del Informe

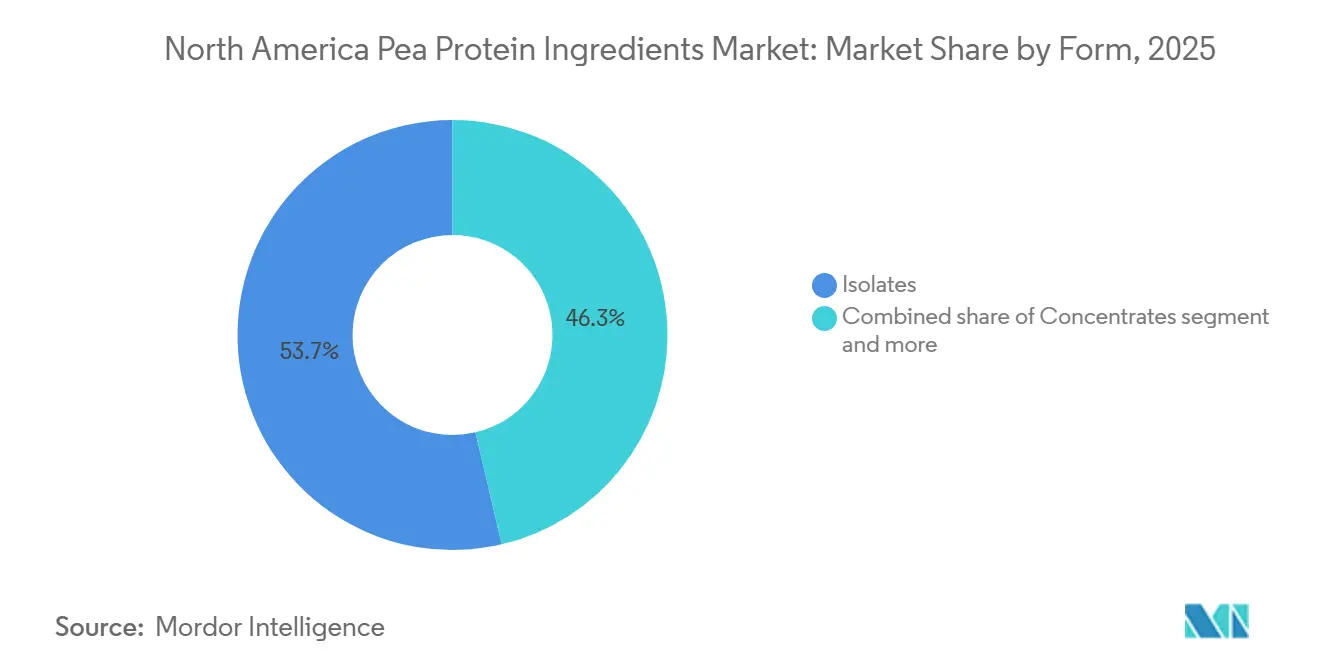

- Por forma, los aislados representaron el 53,68% de la participación del mercado de ingredientes de proteína de guisante de América del Norte en 2025, y se prevé que los concentrados registren la CAGR más rápida del 4,67% hasta 2031.

- Por naturaleza, los productos convencionales representaron el 76,54% de los ingresos en 2025, mientras que se proyecta que las variantes orgánicas crezcan a un ritmo del 5,78% anual.

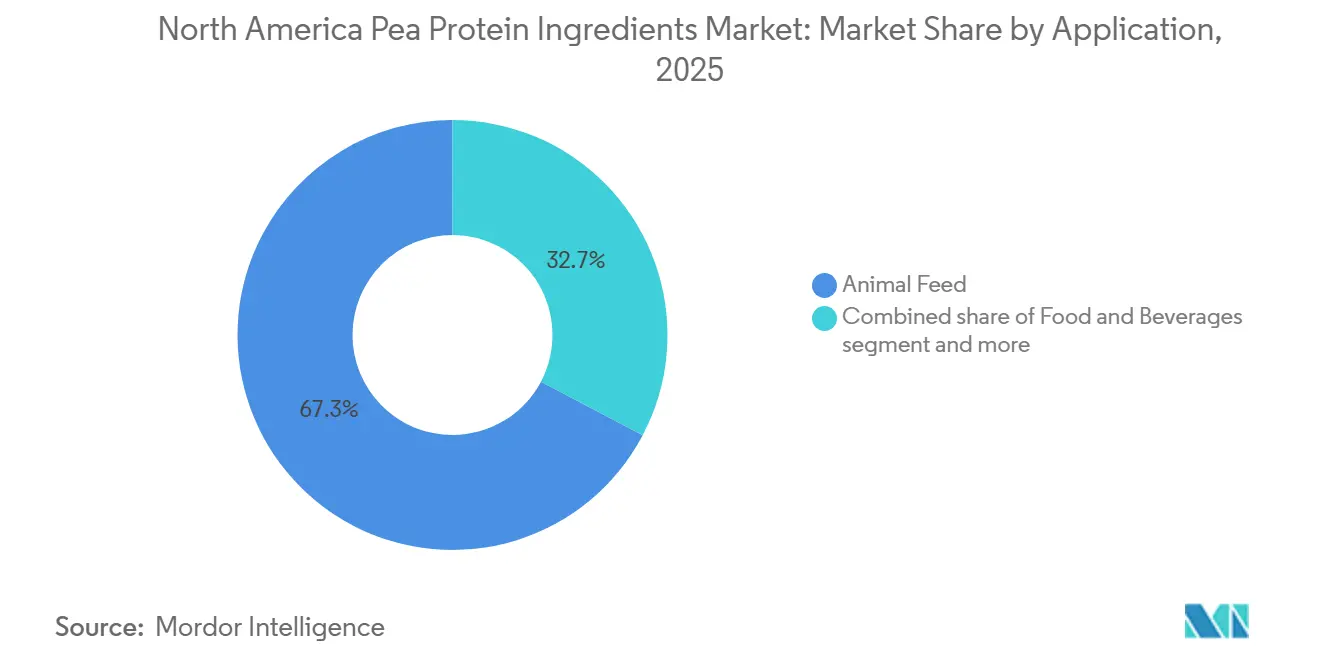

- Por aplicación, el alimento para animales representó el 67,28% del tamaño del mercado de ingredientes de proteína de guisante de América del Norte en 2025, y se espera que los suplementos se expandan a una CAGR del 5,91% hasta 2031.

- Por geografía, Estados Unidos generó el 69,23% de los ingresos de 2025, mientras que México está proyectado para una CAGR del 6,06% hasta 2031.

Nota: Las cifras del tamaño del mercado y los pronósticos de este informe se generan utilizando el marco de estimación patentado de Mordor Intelligence, actualizado con los datos y conocimientos más recientes disponibles a partir de enero de 2026.

Tendencias e Información del Mercado de Ingredientes de Proteína de Guisante de América del Norte

Análisis del Impacto de los Impulsores*

| Impulsor | (~) % de Impacto en la Previsión de CAGR | Relevancia Geográfica | Horizonte Temporal del Impacto |

|---|---|---|---|

| Avances tecnológicos en extracción y procesamiento | +1.2% | Estados Unidos, Canadá, con adopción temprana en centros de procesamiento de alimentos (California, Illinois, Manitoba) | Mediano plazo (2-4 años) |

| Preferencia del consumidor por etiquetado limpio y transparente | +0.9% | Estados Unidos, Canadá, México, más fuerte en centros urbanos y canales de venta minorista natural/orgánica | Corto plazo (≤ 2 años) |

| Creciente adopción de dietas veganas y flexitarianas | +0.8% | Estados Unidos, Canadá, con expansión hacia el México urbano (Ciudad de México, Guadalajara, Monterrey) | Mediano plazo (2-4 años) |

| Creciente enfoque en la sostenibilidad y menor huella ambiental | +0.7% | En toda América del Norte, más fuerte en la Costa Oeste de Estados Unidos, Columbia Británica y los sectores institucionales de servicios de alimentación | Largo plazo (≥ 4 años) |

| Propiedades superiores de emulsificación, espumado, gelificación y espesamiento | +0.6% | Estados Unidos, Canadá, particularmente en regiones de fabricación de alternativas lácteas y análogos de carne | Corto plazo (≤ 2 años) |

| Expansión de sustitutos cárnicos y alternativas lácteas | +1.0% | Estados Unidos, Canadá, México urbano, concentrado en categorías de alimentos de origen vegetal refrigerados y congelados | Mediano plazo (2-4 años) |

| Fuente: Mordor Intelligence | |||

Los avances tecnológicos están impulsando el mercado

Los avances tecnológicos son un impulsor clave para el mercado de ingredientes de proteína de guisante, mejorando significativamente la calidad del producto, la funcionalidad y el potencial de aplicación. El progreso continuo en las tecnologías de extracción y fraccionamiento de proteínas, incluidos los métodos avanzados de procesamiento húmedo y seco, está logrando mayores rendimientos de proteínas mientras se mantiene la integridad nutricional. Técnicas como la hidrólisis enzimática, la filtración por membrana y el procesamiento térmico controlado están mejorando la solubilidad, la dispersibilidad y la digestibilidad, al tiempo que minimizan eficazmente los sabores desagradables y la aspereza tradicionalmente asociados con la proteína de guisante. Estos desarrollos permiten la incorporación fluida de la proteína de guisante en bebidas con alto contenido proteico, alternativas cárnicas, suplementos dietéticos y productos de nutrición especializada, donde el rendimiento sensorial y la consistencia son esenciales. Además, la personalización impulsada por la tecnología, como los aislados y concentrados específicos para cada aplicación con mayor estabilidad al calor, emulsificación o propiedades de retención de agua, permite a los fabricantes satisfacer diversas necesidades de formulación.

Preferencia del consumidor por etiquetado limpio y transparente

La preferencia del consumidor por el etiquetado limpio y transparente es un impulsor significativo para el mercado de ingredientes de proteína de guisante. Los compradores examinan cada vez más las listas de ingredientes y favorecen los productos comercializados como naturales, orgánicos, mínimamente procesados y libres de aditivos artificiales. La proteína de guisante cumple estas expectativas debido a su origen vegetal, su condición de no modificado genéticamente, su naturaleza apta para alérgicos y su compatibilidad con listas de ingredientes cortas y fácilmente reconocibles. Esto la convierte en una opción preferida para la reformulación de etiqueta limpia en productos alimenticios, de bebidas y de nutrición. El cambio se ve reforzado por la evolución de las percepciones de los consumidores sobre la salud y el bienestar. Por ejemplo, según el Consejo Internacional de Información Alimentaria (IFIC), en 2024, el 36% de los estadounidenses buscó activamente alimentos etiquetados como naturales, orgánicos o saludables, lo que subraya el creciente impacto del etiquetado transparente en las decisiones de compra [1]Fuente: Consejo Internacional de Información Alimentaria (IFIC), "Encuesta de Alimentos y Salud IFIC 2024", ific.org. A medida que las marcas reformulan los productos para eliminar ingredientes sintéticos y mejorar la claridad de la etiqueta, la proteína de guisante se adopta cada vez más como una fuente de proteínas confiable que respalda las afirmaciones de etiqueta limpia sin comprometer la funcionalidad.

Creciente adopción de dietas veganas y flexitarianas

La creciente adopción de dietas veganas y flexitarianas es un impulsor clave para el crecimiento del mercado de ingredientes de proteína de guisante. Los consumidores están transitando progresivamente hacia hábitos alimenticios de origen vegetal debido a consideraciones de salud, éticas y ambientales. La proteína de guisante ha ganado prominencia como fuente de proteínas preferida en estas dietas debido a su perfil completo de aminoácidos, su origen vegetal y sus propiedades aptas para alérgicos. Estas características la hacen adecuada para diversos productos alternativos a la carne, los lácteos y los huevos. A medida que los consumidores flexitarianos buscan reducir el consumo de proteínas animales sin comprometer la nutrición ni el sabor, los fabricantes de alimentos están reformulando productos para incorporar proteína de guisante en sustitutos cárnicos, alternativas lácteas de origen vegetal, aperitivos proteicos y bebidas nutricionales. La versatilidad del ingrediente, su sabor neutro y sus propiedades funcionales permiten a las marcas replicar texturas y experiencias sensoriales familiares mientras satisfacen las expectativas de los consumidores veganos y flexitarianos.

Creciente enfoque en la sostenibilidad y menor huella ambiental

El creciente énfasis en la sostenibilidad y la reducción del impacto ambiental está impulsando el mercado, ya que tanto los fabricantes de alimentos como los consumidores priorizan cada vez más los ingredientes producidos mediante métodos ambientalmente responsables y prácticas eficientes en el uso de recursos. La proteína de guisante es reconocida por sus menores emisiones de gases de efecto invernadero, su reducido consumo de agua y su papel en el apoyo a la salud del suelo a través de la fijación de nitrógeno, en comparación con muchas fuentes de proteínas de origen animal. Estos beneficios de sostenibilidad posicionan a la proteína de guisante como una opción preferida para las marcas que buscan alcanzar objetivos corporativos de sostenibilidad, cumplir compromisos de ESG y adherirse a estándares de abastecimiento responsable, todo ello manteniendo el valor nutricional y la funcionalidad. A medida que las empresas de las industrias de alimentos, piensos y nutrición intensifican sus esfuerzos por minimizar su huella ambiental, la proteína de guisante se utiliza cada vez más en formulaciones de origen vegetal y productos híbridos para reducir la dependencia de las proteínas animales.

Análisis del Impacto de las Restricciones*

| Restricción | (~) % de Impacto en la Previsión de CAGR | Relevancia Geográfica | Horizonte Temporal del Impacto |

|---|---|---|---|

| Competencia de otras proteínas vegetales (soja, arroz, cáñamo) | -0.8% | Estados Unidos, Canadá, particularmente en aplicaciones de alimento para animales sensibles al precio y alimentos básicos | Corto plazo (≤ 2 años) |

| Interrupciones en la cadena de suministro y concentración geográfica en Saskatchewan | -0.5% | Canadá (Saskatchewan, Manitoba), con efectos en cascada sobre los procesadores de Estados Unidos y los importadores mexicanos | Corto plazo (≤ 2 años) |

| Limitaciones sensoriales y de sabor (notas a legumbre, sensación harinosa en boca) | -0.6% | Estados Unidos, México, más agudo en bebidas sin sabor y productos de nutrición deportiva con sabor suave | Mediano plazo (2-4 años) |

| Obstáculos regulatorios y de etiquetado en distintas jurisdicciones | -0.3% | Estados Unidos (variación a nivel estatal), México (orientación de COFEPRIS pendiente), Canadá (requisitos bilingües) | Mediano plazo (2-4 años) |

| Fuente: Mordor Intelligence | |||

Competencia de otras proteínas vegetales

La competencia de otras proteínas vegetales representa una restricción significativa para el mercado de ingredientes de proteína de guisante. Los formuladores tienen acceso a una variedad creciente de fuentes alternativas de proteínas, incluidas la soja, la haba, el garbanzo, la lenteja, el arroz, la avena y la micoproteína. Muchas de estas alternativas se benefician de cadenas de suministro establecidas, funcionalidad bien conocida, o ventajas de costo y rendimiento en aplicaciones específicas, lo que puede dificultar la adopción de la proteína de guisante. Por ejemplo, la proteína de soja sigue siendo popular debido a su alto contenido proteico y sus sólidas propiedades funcionales, mientras que opciones más nuevas como la haba y el garbanzo están ganando atención por sus perfiles de sabor mejorados y sus percibidos beneficios de sostenibilidad. Además, ciertas proteínas vegetales ofrecen mejor solubilidad, emulsificación o completitud de aminoácidos para aplicaciones específicas, lo que alienta a los fabricantes a utilizar mezclas de múltiples proteínas en lugar de depender exclusivamente de la proteína de guisante. Este entorno cada vez más competitivo añade complejidad a las formulaciones y ralentiza la penetración del mercado en ciertos segmentos.

Interrupciones en la cadena de suministro

Las interrupciones en la cadena de suministro representan una restricción significativa para el mercado de ingredientes de proteína de guisante, ya que la disponibilidad y consistencia de las materias primas dependen en gran medida de los rendimientos agrícolas, las variaciones estacionales y la capacidad de procesamiento. La producción de proteína de guisante requiere cosechas estables y una logística eficiente en las etapas de cultivo, almacenamiento y fraccionamiento. Las interrupciones causadas por la variabilidad climática, los retrasos en el transporte, la escasez de mano de obra o las interrupciones en el procesamiento pueden resultar en un suministro irregular e inconsistencias de calidad. Esta inestabilidad complica las estrategias de abastecimiento a largo plazo para los fabricantes de alimentos, piensos y nutrición, particularmente aquellos que necesitan un rendimiento funcional consistente y especificaciones de proteínas estandarizadas. Además, los retrasos en el comercio transfronterizo y la infraestructura de procesamiento limitada en ciertas regiones dificultan la entrega oportuna y el escalado, aumentando los desafíos de formulación para los fabricantes.

*Nuestras previsiones consideran los impactos de impulsores y restricciones como direccionales, no aditivos. Las previsiones de impacto reflejan el crecimiento base, los efectos de mezcla y las interacciones entre variables.

Análisis de Segmentos

Por Forma: Los Aislados Anclan las Aplicaciones Premium

Los aislados de proteína de guisante, que representaron una participación de mercado del 53,68% en 2025, están transitando de ser una fuente de proteínas funcional a un ingrediente altamente refinado y orientado a aplicaciones específicas, impulsando la innovación en el mercado de ingredientes de proteína de guisante. Esta dominancia se atribuye a su compatibilidad con formulaciones de alto contenido proteico y bajo contenido en carbohidratos, donde los fabricantes de alimentos y nutrición enfatizan el sabor neutro, la solubilidad rápida y el rendimiento consistente. Los avances tecnológicos en el fraccionamiento húmedo, la filtración por membrana y el procesamiento enzimático están mejorando la neutralidad del sabor, la dispersibilidad y la sensación en boca. Estas mejoras abordan desafíos anteriores como las notas desagradables a legumbre y la sedimentación, haciendo de los aislados una opción preferida para diversas aplicaciones, incluidas las bebidas de origen vegetal, las barras de proteínas y los sustitutos cárnicos.

Los concentrados de proteína de guisante, proyectados para crecer a una CAGR del 4,67% hasta 2031, están emergiendo como una alternativa rentable y versátil en el mercado de ingredientes de proteína de guisante. Son particularmente adecuados para aplicaciones que priorizan el enriquecimiento proteico moderado, la mejora de la textura y el atractivo de etiqueta limpia sobre la pureza proteica ultra alta. Su crecimiento está impulsado por la creciente demanda de formulaciones de estilo alimento integral que retienen más de los componentes nativos del guisante, alineándose con las preferencias de los consumidores por ingredientes mínimamente procesados y de origen natural. Las innovaciones en el fraccionamiento en seco y las técnicas de procesamiento suave están mejorando los perfiles de sabor y la consistencia funcional, reduciendo el amargor mientras se preservan los beneficios relacionados con la fibra, como la saciedad y el apoyo digestivo.

Por Naturaleza: Las Primas Orgánicas Impulsan el Crecimiento de Nicho

La proteína de guisante convencional, que representó una participación dominante del 76,54% en 2025, sigue siendo un componente clave en el mercado de ingredientes de proteína de guisante debido a su amplia disponibilidad, propiedades funcionales consistentes y versatilidad en aplicaciones de alimentos y nutrición de alto volumen. Esta dominancia se atribuye a su fuerte idoneidad para las categorías de productos convencionales, donde los fabricantes priorizan el suministro confiable, la calidad estandarizada y las características de procesamiento predecibles. La proteína de guisante convencional se beneficia de una infraestructura agrícola y de procesamiento bien establecida, lo que garantiza un abastecimiento estable de materias primas y una producción escalable. Esto respalda su uso extensivo tanto en formulaciones industriales como de servicios de alimentación.

La proteína de guisante orgánica, proyectada para crecer a una CAGR del 5,78% hasta 2031, está emergiendo como un segmento de alto valor dentro del mercado de ingredientes de proteína de guisante, impulsada por la creciente demanda de ingredientes orgánicos certificados, de etiqueta limpia y con trazabilidad transparente. Su crecimiento está impulsado por la creciente adopción en alimentos de origen vegetal premium, suplementos nutricionales orgánicos, nutrición infantil y productos de salud natural, donde la credibilidad de la certificación y la trazabilidad de los ingredientes juegan un papel significativo en la diferenciación de marca. Los fabricantes utilizan cada vez más la proteína de guisante orgánica para respaldar afirmaciones relacionadas con atributos libres de ciertos componentes y sostenibilidad, incluidas las prácticas agrícolas sin organismos modificados genéticamente, sin pesticidas y ambientalmente responsables. Estos atributos atraen a los consumidores conscientes de la salud y del medio ambiente.

Por Aplicación: La Dominancia en Piensos se Encuentra con el Impulso de los Suplementos

El alimento para animales, que representó una participación significativa del 67,28% en 2025, destaca el papel esencial de la proteína de guisante como fuente de proteínas de origen vegetal nutricionalmente eficiente en los segmentos de ganadería, acuicultura y nutrición de mascotas. Esta dominancia se atribuye a su alta digestibilidad, su favorable perfil de aminoácidos y su versatilidad funcional, lo que la hace adecuada para formulaciones de piensos para aves de corral, porcino, rumiantes, peces y animales de compañía. La proteína de guisante se utiliza cada vez más como sustituto parcial de la harina de soja y las proteínas de origen animal, lo que permite a los formuladores de piensos diversificar las fuentes de proteínas mientras mantienen métricas de rendimiento clave como las tasas de crecimiento, la eficiencia de conversión alimentaria y la salud intestinal. Su bajo perfil alergénico y sus reducidos factores antinutricionales, en comparación con algunas proteínas vegetales tradicionales, respaldan aún más su adopción, particularmente en formulaciones de acuicultura y alimentos premium para mascotas.

Los suplementos, proyectados para crecer a una CAGR del 5,91% hasta 2031, están emergiendo como un segmento de aplicación dinámico para los ingredientes de proteína de guisante, impulsados por la creciente adopción de estilos de vida de fitness, bienestar y activos. Este crecimiento está estrechamente vinculado al aumento de la participación en actividades de fitness estructuradas. Por ejemplo, según la Asociación de Salud y Fitness, casi 77 millones de estadounidenses utilizaron instalaciones de fitness en 2024, lo que subraya la gran base de consumidores que busca suplementación proteica para apoyar la recuperación muscular, la resistencia y la salud en general [2]Fuente: Asociación de Salud y Fitness, "Informe del Consumidor de Salud y Fitness de EE. UU. 2025" healthandfitness.org. La proteína de guisante está ganando popularidad en los suplementos dietéticos debido a su origen vegetal, su alta digestibilidad y sus propiedades hipoalergénicas, lo que la hace adecuada para una amplia gama de consumidores, incluidos veganos, personas con intolerancia a la lactosa y aquellos que evitan las proteínas de soja o suero de leche.

Análisis Geográfico

Estados Unidos, que representó una participación de mercado dominante del 69,23% en 2025, representa el mercado más maduro y comercialmente avanzado para los ingredientes de proteína de guisante en América del Norte. Este liderazgo se atribuye a la bien establecida infraestructura de procesamiento de alimentos y bebidas del país, la fuerte presencia de proveedores globales de ingredientes y los marcos regulatorios y de etiquetado claros que facilitan la rápida comercialización de proteínas de origen vegetal. El mercado de Estados Unidos se beneficia del uso extensivo de la proteína de guisante en alimento para animales, fabricación de alimentos, suplementos dietéticos y nutrición deportiva. Esto está respaldado por sólidas capacidades de Investigación y Desarrollo (I+D) y una estrecha colaboración entre los proveedores de ingredientes y los propietarios de marcas.

México, proyectado para crecer a una CAGR del 6,06% hasta 2031, está emergiendo como el mercado de más rápido crecimiento en la región, impulsado por cambios estructurales en el consumo de alimentos y la fabricación. Factores como la rápida urbanización, la creciente exposición a formatos de venta minorista modernos y la expansión de la fabricación localizada de alternativas lácteas de origen vegetal y alimentos fortificados están acelerando la adopción de ingredientes de proteína de guisante. México también se está beneficiando de las crecientes inversiones de empresas alimentarias multinacionales que buscan establecer centros de producción regionales, lo que facilita el acceso a ingredientes de origen vegetal y reduce la dependencia de las importaciones. A medida que los productores domésticos de alimentos y bebidas incorporan cada vez más la proteína de guisante en productos asequibles para el mercado masivo, se espera que México desempeñe un papel cada vez más significativo en el impulso del crecimiento del volumen regional durante el período de previsión.

Canadá ocupa una posición estratégicamente importante en el mercado de proteína de guisante de América del Norte, principalmente debido a su dominio en el cultivo y procesamiento de guisantes en la cadena de valor ascendente. Según Saskatchewan Pulse Growers, Canadá es uno de los principales productores mundiales de guisantes amarillos, proporcionando una base de materia prima confiable y de alta calidad que respalda tanto el consumo doméstico como las exportaciones. En 2023/24, la producción canadiense consistió en un 86% de guisantes amarillos, un 11% de guisantes verdes y un 3% de otros tipos [3]Fuente: Saskatchewan Pulse Growers, "Oportunidades del Mercado de Guisantes", saskpulse.com. Esta fortaleza en la cadena de valor ascendente mejora la seguridad del suministro para la región y respalda el crecimiento a largo plazo al garantizar calidad consistente, trazabilidad y escalabilidad en aplicaciones de alimentos, piensos y nutrición.

Panorama Competitivo

El mercado de ingredientes de proteína de guisante de América del Norte demuestra una concentración moderada, con una combinación de grandes proveedores de ingredientes diversificados y un número creciente de actores regionales y orientados a aplicaciones específicas. Las empresas clave como Archer Daniels Midland Company, Bunge Global SA, Cargill, Incorporated, Glanbia PLC e Ingredion Incorporated dominan el mercado. Estas empresas aprovechan el amplio acceso a materias primas, redes de procesamiento globales y sólidas relaciones con fabricantes en las industrias de alimentos, piensos y nutrición. Su ventaja competitiva se ve reforzada por las economías de escala, las cadenas de suministro verticalmente integradas y los amplios portafolios de productos, incluidos aislados, concentrados y proteínas texturizadas, que atienden tanto aplicaciones de alto volumen como especializadas.

La adopción de tecnología se ha convertido en un factor crítico para mantener la competitividad. Los actores líderes están realizando inversiones significativas en tecnologías avanzadas como el fraccionamiento, el tratamiento enzimático y el enmascaramiento de sabores para mejorar la solubilidad, la neutralidad del sabor y la consistencia funcional de los ingredientes de proteína de guisante. La innovación en soluciones específicas para cada aplicación, como aislados estables al calor para bebidas, concentrados de alta retención de agua para alternativas cárnicas y proteínas con digestibilidad mejorada para alimento para animales, permite a las empresas diferenciar sus ofertas más allá del precio. Además, las asociaciones estratégicas, los acuerdos de codesarrollo con marcas de alimentos y la expansión de los centros de Investigación y Desarrollo (I+D) refuerzan su posición en el mercado al acelerar la comercialización de formulaciones personalizadas que se alinean con la creciente demanda de productos de etiqueta limpia y de origen vegetal.

Están surgiendo nuevas oportunidades en segmentos de nicho como la fórmula infantil hipoalergénica, la nutrición para personas mayores y clínica, y el alimento para acuicultura. Estas áreas están experimentando una mayor demanda de fuentes de proteínas altamente digestibles, libres de alérgenos y nutricionalmente precisas. Tanto los actores establecidos como los innovadores más pequeños tienen el potencial de desarrollar soluciones de proteína de guisante de alto valor y especializadas con perfiles de aminoácidos adaptados y atributos funcionales para satisfacer estas necesidades. A medida que la competencia se intensifica, las empresas están desplazando su enfoque hacia la premiumización, la sostenibilidad y la innovación orientada a aplicaciones, en lugar de perseguir únicamente la expansión de volumen. Este enfoque está dando forma a un panorama competitivo que equilibra las ventajas de la escala con la diferenciación tecnológica y nutricional.

Líderes de la Industria de Ingredientes de Proteína de Guisante de América del Norte

Archer Daniels Midland Company

Bunge Global SA

Cargill, Incorporated

Glanbia PLC

Ingredion Incorporated

- *Nota aclaratoria: los principales jugadores no se ordenaron de un modo en especial

Desarrollos Recientes de la Industria

- Enero de 2025: Axiom Foods lanzó Vegotein N Neutral, un ingrediente de proteína de guisante, para satisfacer la creciente demanda de proteína de guisante en el mercado. Contiene una concentración de proteína del 80% y es completamente digestible. El ingrediente se produce utilizando guisantes amarillos no modificados genéticamente cultivados en América del Norte.

- Diciembre de 2024: Burcon NutraScience Corporation introdujo PeazazzC, una proteína de guisante de sabor limpio desarrollada para el creciente mercado de proteínas de origen vegetal. Derivada de guisantes de campo no modificados genéticamente de América del Norte, es adecuada para diversas aplicaciones, incluidas bebidas, alternativas lácteas, productos de panadería y barras de nutrición.

- Julio de 2024: Ingredion Incorporated introdujo su producto de fortificación proteica cultivado y producido en América del Norte, VITESSENCE Pea 100 HD, una proteína de guisante específicamente diseñada para barras prensadas en frío. Este producto ayuda a mantener la suavidad de las barras prensadas en frío durante su vida útil, mejora la textura y los atributos sensoriales, y añade valor nutricional para satisfacer las preferencias de los consumidores.

Alcance del Informe del Mercado de Ingredientes de Proteína de Guisante de América del Norte

La proteína de guisante es un polvo proteico de alta calidad y origen vegetal elaborado a partir de guisantes amarillos partidos, popular en dietas veganas, sin lácteos y aptas para alérgicos, valorado por su digestibilidad, contenido de hierro y aminoácidos esenciales. Los ingredientes de proteína de guisante de América del Norte están segmentados por forma, naturaleza, aplicación y geografía. Por forma, el mercado está segmentado en concentrados, aislados y texturizados/hidrolizados. Por naturaleza, el mercado está segmentado en convencional y orgánico. Por aplicación, el mercado está segmentado en alimento para animales, cuidado personal y cosméticos, alimentos y bebidas, y suplementos. Por geografía, el mercado está segmentado en Estados Unidos, Canadá, México y el resto de América del Norte. Las Previsiones del Mercado se Proporcionan en Términos de Valor (USD) y Volumen (Toneladas).

| Concentrados |

| Aislados |

| Texturizados/Hidrolizados |

| Convencional |

| Orgánico |

| Alimento para Animales | |

| Cuidado Personal y Cosméticos | |

| Alimentos y Bebidas | Panadería |

| Bebidas | |

| Cereales de Desayuno | |

| Condimentos/Salsas | |

| Productos Lácteos y Alternativas Lácteas | |

| Productos de Carne/Aves/Mariscos y Alternativas Cárnicas | |

| Productos Alimenticios Listos para Consumir/Listos para Cocinar | |

| Aperitivos | |

| Suplementos | Alimentos para Bebés y Fórmula Infantil |

| Nutrición para Personas Mayores y Nutrición Médica | |

| Nutrición Deportiva/de Rendimiento |

| Estados Unidos |

| Canadá |

| México |

| Resto de América del Norte |

| Por Forma | Concentrados | |

| Aislados | ||

| Texturizados/Hidrolizados | ||

| Por Naturaleza | Convencional | |

| Orgánico | ||

| Por Aplicación | Alimento para Animales | |

| Cuidado Personal y Cosméticos | ||

| Alimentos y Bebidas | Panadería | |

| Bebidas | ||

| Cereales de Desayuno | ||

| Condimentos/Salsas | ||

| Productos Lácteos y Alternativas Lácteas | ||

| Productos de Carne/Aves/Mariscos y Alternativas Cárnicas | ||

| Productos Alimenticios Listos para Consumir/Listos para Cocinar | ||

| Aperitivos | ||

| Suplementos | Alimentos para Bebés y Fórmula Infantil | |

| Nutrición para Personas Mayores y Nutrición Médica | ||

| Nutrición Deportiva/de Rendimiento | ||

| Por Geografía | Estados Unidos | |

| Canadá | ||

| México | ||

| Resto de América del Norte | ||

Definición de mercado

- Usuario Final - El Mercado de Ingredientes Proteicos opera sobre una base B2B. Los fabricantes de Alimentos, Bebidas, Suplementos, Alimento para Animales y Cuidado Personal y Cosméticos se consideran usuarios finales en el mercado estudiado. El alcance excluye a los fabricantes que compran suero de leche líquido/seco para su uso como agente aglutinante, espesante u otras aplicaciones no proteicas.

- Tasa de Penetración - La Tasa de Penetración se define como el porcentaje del Volumen del Mercado de Usuario Final Fortificado con Proteínas en el Volumen Total del Mercado de Usuario Final.

- Contenido Proteico Promedio - El contenido proteico promedio es el contenido proteico medio presente por cada 100 g de producto fabricado por todas las empresas de usuario final consideradas en el alcance de este informe.

- Volumen del Mercado de Usuario Final - El volumen del mercado de usuario final es el volumen consolidado de todos los tipos y formas de productos de usuario final en el país o región.

| Palabra clave | Definición |

|---|---|

| Alfa-lactoalbúmina (α-Lactoalbúmina) | Es una proteína que regula la producción de lactosa en la leche de casi todas las especies de mamíferos. |

| Aminoácido | Es un compuesto orgánico que contiene grupos funcionales tanto amino como ácido carboxílico, necesarios para la síntesis de proteínas corporales y otros compuestos importantes que contienen nitrógeno, como la creatina, las hormonas peptídicas y algunos neurotransmisores. |

| Escaldado | Es el proceso de calentar brevemente las verduras con vapor o agua hirviendo. |

| BRC | Consorcio Británico de Comercio Minorista |

| Mejorador de pan | Es una mezcla a base de harina de varios componentes con propiedades funcionales específicas diseñadas para modificar las características de la masa y otorgar atributos de calidad al pan. |

| BSF | Mosca Soldado Negro |

| Caseinato | Es una sustancia producida al añadir un álcali a la caseína ácida, un derivado de la caseína. |

| Enfermedad celíaca | La enfermedad celíaca es una reacción inmunitaria a la ingesta de gluten, una proteína que se encuentra en el trigo, la cebada y el centeno. |

| Calostro | Es un fluido lácteo que liberan los mamíferos que han dado a luz recientemente, antes de que comience la producción de leche materna. |

| Concentrado | Es la forma menos procesada de proteína y tiene un contenido proteico que oscila entre el 40% y el 90% en peso. |

| Base de proteína seca | Se refiere al porcentaje de "proteína pura" presente en un suplemento después de que el agua que contiene se elimina completamente mediante calor. |

| Suero de leche en polvo | Es el producto resultante de secar el suero de leche fresco que ha sido pasteurizado y al que no se le ha añadido ningún conservante. |

| Proteína de huevo | Es una mezcla de proteínas individuales, que incluye ovoalbúmina, ovomucoide, ovoglobulina, conalbúmina, vitelina y vitelenina. |

| Emulsionante | Es un aditivo alimentario que facilita la mezcla de alimentos que son inmiscibles entre sí, como el aceite y el agua. |

| Enriquecimiento | Es el proceso de adición de micronutrientes que se pierden durante el procesamiento del producto. |

| ERS | Servicio de Investigación Económica del USDA |

| Extrusión | Es el proceso de forzar ingredientes blandos mezclados a través de una abertura en una placa perforada o matriz diseñada para producir la forma requerida. El alimento extruido se corta luego a un tamaño específico mediante cuchillas. |

| Haba | También conocida como Faba, es otro nombre para los frijoles amarillos partidos. |

| FDA | Administración de Alimentos y Medicamentos |

| Laminado | Es un proceso en el que típicamente un grano de cereal (como maíz, trigo o arroz) se descompone en sémola, se cocina con sabores y jarabes, y luego se prensa en copos entre rodillos enfriados. |

| Agente espumante | Es un ingrediente alimentario que hace posible formar o mantener una dispersión uniforme de una fase gaseosa en un alimento líquido o sólido. |

| Servicios de alimentación | Se refiere a la parte de la industria alimentaria que incluye empresas, instituciones y compañías que preparan comidas fuera del hogar. Incluye restaurantes, cafeterías escolares y hospitalarias, operaciones de catering y muchos otros formatos. |

| Fortificación | Es la adición deliberada de micronutrientes que no se encuentran en ellos de forma natural o que se pierden durante el procesamiento, para mejorar el valor nutricional de un producto alimenticio. |

| FSANZ | Normas Alimentarias de Australia y Nueva Zelanda |

| FSIS | Servicio de Inspección y Seguridad Alimentaria |

| FSSAI | Autoridad de Seguridad y Normas Alimentarias de India |

| Agente gelificante | Es un ingrediente que funciona como estabilizador y espesante para proporcionar espesor sin rigidez mediante la formación de gel. |

| GHG | Gas de Efecto Invernadero |

| Gluten | Es una familia de proteínas que se encuentran en los cereales, incluidos el trigo, el centeno, la espelta y la cebada. |

| Cáñamo | Es una clase botánica de cultivares de Cannabis sativa cultivados específicamente para uso industrial o medicinal. |

| Hidrolizado | Es una forma de proteína fabricada exponiendo la proteína a enzimas que pueden romper parcialmente los enlaces entre los aminoácidos de la proteína y descomponer proteínas grandes y complejas en piezas más pequeñas. Su procesamiento facilita y acelera su digestión. |

| Hipoalergénico | Se refiere a una sustancia que causa menos reacciones alérgicas. |

| Aislado | Es la forma más pura y procesada de proteína que ha sido sometida a separación para obtener una fracción proteica pura. Típicamente contiene ≥ 90% de proteína en peso. |

| Queratina | Es una proteína que ayuda a formar el cabello, las uñas y la capa exterior de la piel. |

| Lactoalbúmina | Es la albúmina contenida en la leche y obtenida del suero de leche. |

| Lactoferrina | Es una glicoproteína de unión al hierro que está presente en la leche de la mayoría de los mamíferos. |

| Altramuz | Son las semillas de leguminosas amarillas del género Lupinus. |

| Millennial | También conocido como Generación Y o Gen Y, se refiere a las personas nacidas entre 1981 y 1996. |

| Monogástrico | Se refiere a un animal con un estómago de un solo compartimento. Ejemplos de monogástricos incluyen humanos, aves de corral, cerdos, caballos, conejos, perros y gatos. La mayoría de los monogástricos generalmente son incapaces de digerir muchos materiales alimenticios con celulosa, como los pastos. |

| MPC | Concentrado de proteína de leche |

| MPI | Aislado de proteína de leche |

| MSPI | Aislado de proteína de soja metilada |

| Micoproteína | La micoproteína es una forma de proteína unicelular, también conocida como proteína fúngica, derivada de hongos para el consumo humano. |

| Nutricosmética | Es una categoría de productos e ingredientes que actúan como suplementos nutricionales para cuidar la belleza natural de la piel, las uñas y el cabello. |

| Osteoporosis | Es una condición médica en la que los huesos se vuelven frágiles y quebradizos por la pérdida de tejido, típicamente como resultado de cambios hormonales o deficiencia de calcio o vitamina D. |

| PDCAAS | La puntuación de aminoácidos corregida por digestibilidad proteica (PDCAAS) es un método para evaluar la calidad de una proteína basándose tanto en los requisitos de aminoácidos de los humanos como en su capacidad para digerirla. |

| Consumo per cápita de proteína animal | Es la cantidad promedio de proteína animal (como leche, suero de leche, gelatina, colágeno y proteínas de huevo) que está disponible para el consumo de cada persona en una población real. |

| Consumo per cápita de proteína vegetal | Es la cantidad promedio de proteína vegetal (como proteínas de soja, trigo, guisante, avena y cáñamo) que está disponible para el consumo de cada persona en una población real. |

| Quorn | Es una proteína microbiana fabricada utilizando micoproteína como ingrediente, en la que el cultivo de hongos se seca y se mezcla con albúmina de huevo o proteína de patata, que actúa como aglutinante, y luego se ajusta en textura y se prensa en diversas formas. |

| Listo para Cocinar (RTC) | Se refiere a productos alimenticios que incluyen todos los ingredientes, donde se requiere alguna preparación o cocción mediante un proceso indicado en el envase. |

| Listo para Consumir (RTE) | Se refiere a un producto alimenticio preparado o cocinado con antelación, sin necesidad de cocción o preparación adicional antes de ser consumido. |

| RTD | Listo para Beber |

| RTS | Listo para Servir |

| Grasa saturada | Es un tipo de grasa en la que las cadenas de ácidos grasos tienen todos enlaces simples. Generalmente se considera poco saludable. |

| Salchicha | Es un producto cárnico elaborado con carne finamente picada y condimentada, que puede ser fresca, ahumada o en escabeche, y que generalmente se embute en una tripa. |

| Seitán | Es un sustituto cárnico de origen vegetal elaborado a partir de gluten de trigo. |

| Cápsula blanda | Es una cápsula a base de gelatina con relleno líquido. |

| SPC | Concentrado de proteína de soja |

| SPI | Aislado de proteína de soja |

| Espirulina | Es una biomasa de cianobacterias que puede ser consumida por humanos y animales. |

| Estabilizador | Es un ingrediente añadido a los productos alimenticios para ayudar a mantener o mejorar su textura original y sus características físicas y químicas. |

| Suplementación | Es el consumo o provisión de fuentes concentradas de nutrientes u otras sustancias destinadas a complementar los nutrientes de la dieta y corregir deficiencias nutricionales. |

| Texturizante | Es un tipo específico de ingrediente alimentario que se utiliza para controlar y alterar la sensación en boca y la textura de los productos alimenticios y de bebidas. |

| Espesante | Es un ingrediente que se utiliza para aumentar la viscosidad de un líquido o masa y hacerlo más espeso, sin cambiar sustancialmente sus otras propiedades. |

| Grasa trans | También llamados ácidos grasos trans insaturados o ácidos grasos trans, es un tipo de grasa insaturada que se produce naturalmente en pequeñas cantidades en la carne. |

| TSP | Proteína de soja texturizada |

| TVP | Proteína vegetal texturizada |

| WPC | Concentrado de proteína de suero de leche |

| WPI | Aislado de proteína de suero de leche |

Metodología de Investigación

Mordor Intelligence sigue una metodología de cuatro pasos en todos nuestros informes.

- Paso 1: Identificar las Variables Clave: Las variables clave cuantificables (del sector y externas) relativas al segmento de producto específico y al país se seleccionan de un grupo de variables y factores relevantes basándose en investigación documental y revisión bibliográfica, junto con aportaciones de expertos primarios. Estas variables se confirman posteriormente mediante modelos de regresión (cuando sea necesario).

- Paso 2: Construir un Modelo de Mercado: Con el fin de desarrollar una metodología de previsión sólida, las variables y factores identificados en el Paso 1 se contrastan con los datos históricos de mercado disponibles. Mediante un proceso iterativo, se establecen las variables necesarias para la previsión del mercado y el modelo se construye sobre la base de estas variables.

- Paso 3: Validar y Finalizar: En este importante paso, todos los datos de mercado, variables y valoraciones de los analistas se validan a través de una extensa red de expertos en investigación primaria del mercado estudiado. Los encuestados se seleccionan en distintos niveles y funciones para generar una imagen holística del mercado estudiado.

- Paso 4: Resultados de la Investigación: Informes Sindicados, Encargos de Consultoría Personalizada, Bases de Datos y Plataformas de Suscripción