Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

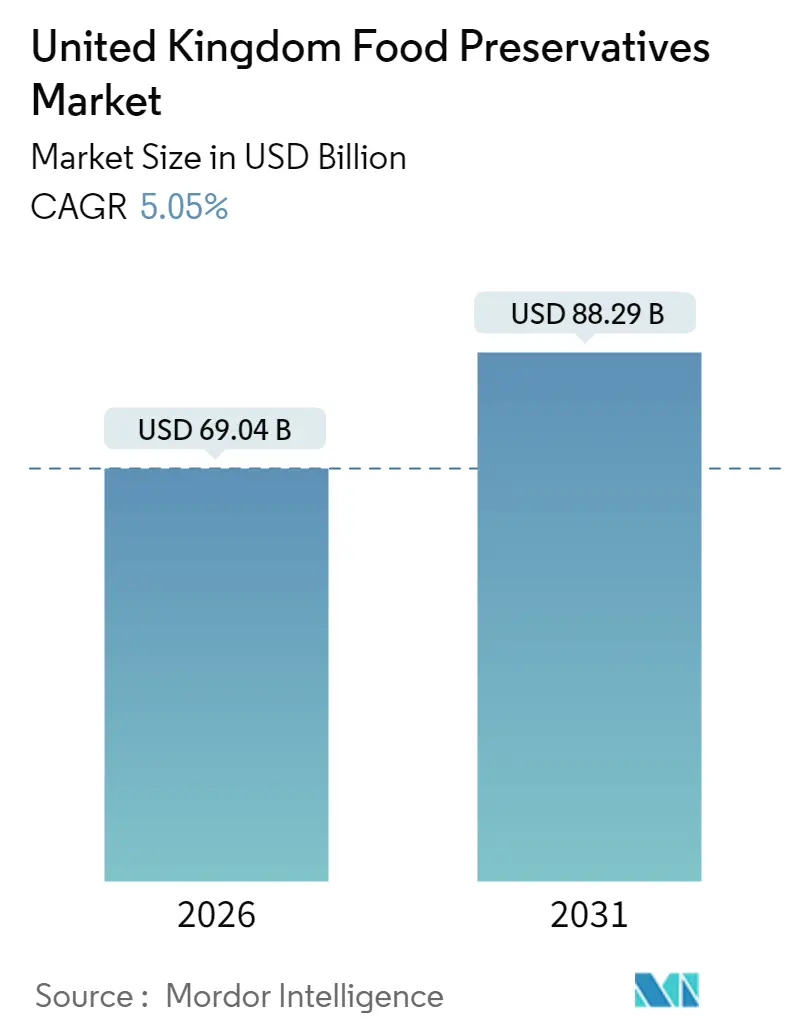

| Market Size (2026) | USD 69.04 Billion |

| Market Size (2031) | USD 88.29 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Food Preservatives Market Analysis by Mordor Intelligence

The United Kingdom Food Preservatives Market is expected to grow from USD 65.72 billion in 2025 to USD 69.04 billion in 2026 and is forecast to reach USD 88.29 billion by 2031 at 5.05% CAGR over 2026-2031. Over this span, the market is being reshaped by three key forces: the Food Standards Agency's heightened scrutiny on synthetic nitrites and sulphites, a notable 29.7% consumer retreat from E-number ingredients, and a post-Brexit shift towards localizing supply chains, favoring domestic raw-material sourcing. Ready meals, growing at a robust 7.82% CAGR, are driving up the demand for preservatives. This is largely due to the need for extended shelf-life stability in humid conditions during ambient logistics. Furthermore, with private-label products commanding 63% of the market volume, suppliers are under pressure to maintain aggressive cost discipline. In this challenging landscape, manufacturers are finding an edge. By integrating fermentation-derived antimicrobials with advanced packaging technologies like high-pressure processing, they're successfully extending shelf-life without the need for additional E-number disclosures.

Key Report Takeaways

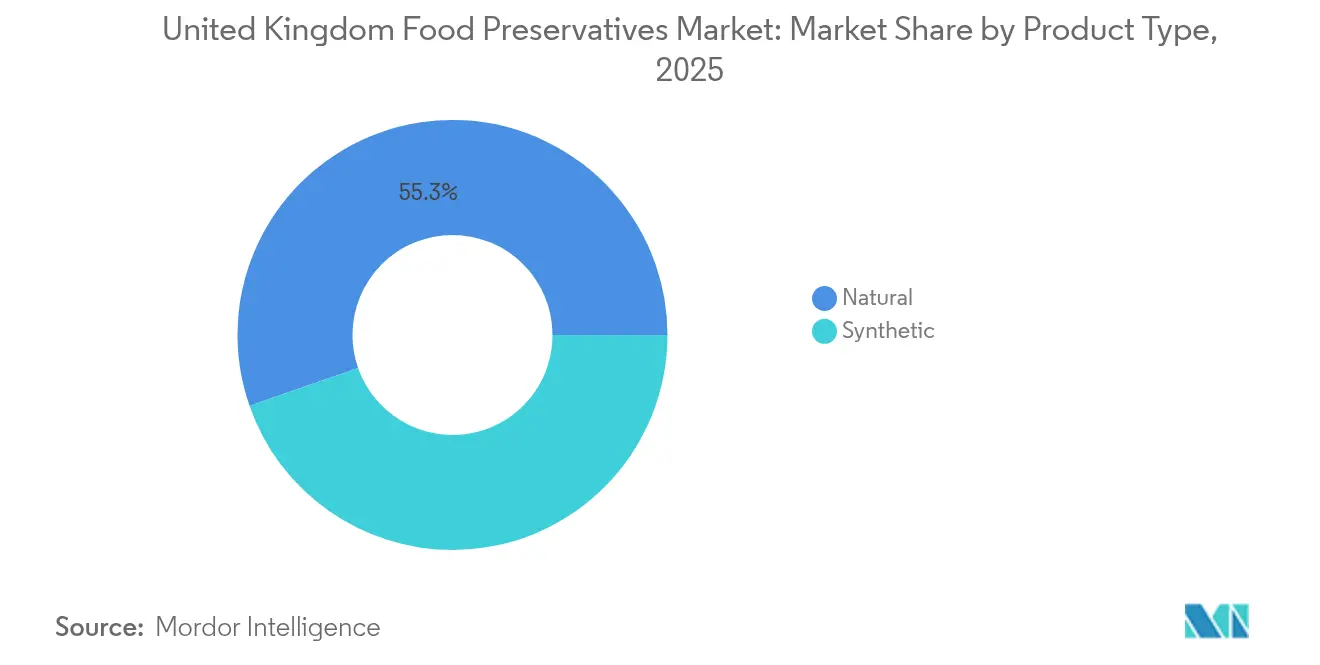

- By product type, synthetic options captured 44.66% of the United Kingdom Food Preservatives Market share in 2025, whereas natural alternatives are forecast to grow at a 5.79% CAGR to 2031.

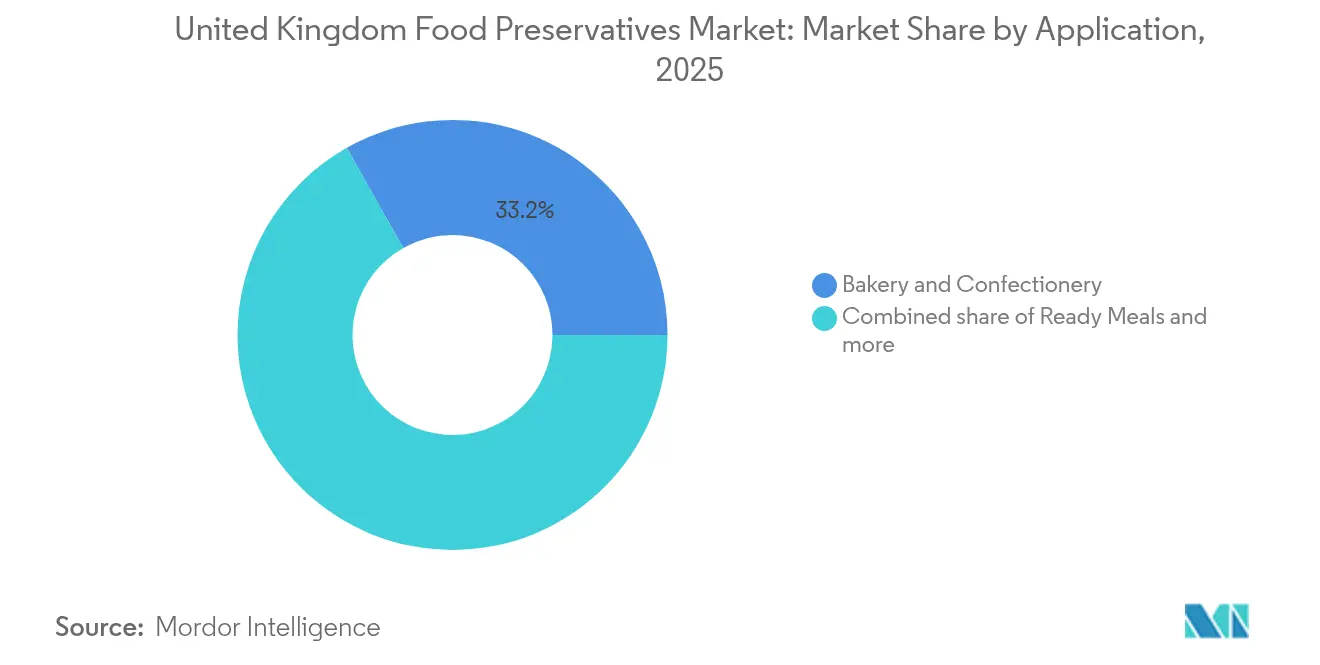

- By application, bakery and confectionery held 33.18% of the United Kingdom Food Preservatives Market size in 2025, while ready meals are accelerating at a 7.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Food Preservatives Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label demand surge | +1.2% | National, with a concentration in Southeast England and urban centers | Medium term (2-4 years) |

| Growth of the United Kingdom ready-to-eat and online grocery channels | +0.9% | National, with early gains in London, Manchester, and Birmingham metro areas | Short term (≤ 2 years) |

| Regulatory pressure limiting synthetic nitrites and sulphites | +0.8% | National, FSA jurisdiction across England, Wales, Scotland, and Northern Ireland | Long term (≥ 4 years) |

| Retail private-label reformulation race | +0.7% | National, led by major supermarket chains in high-footfall regions | Medium term (2-4 years) |

| Post-Brexit raw-material localisation incentives | +0.5% | National, with supply-chain hubs in the Midlands and Northern England | Long term (≥ 4 years) |

| Rise of MAP/HPP creating combo-preservative demand | +0.6% | National, concentrated in food manufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clean-label demand surge

United Kingdom shoppers are increasingly prioritizing natural ingredients, with 29.7% actively cutting back on synthetic additives and 11.3% highlighting additives as a top concern in product selection, according to Attest. This consumer shift is prompting widespread reformulations, especially in ready meals. For instance, Marks & Spencer's "Eat Well" range came under fire for its inclusion of over 30 ingredients, notably stabilisers and emulsifiers. However, the challenge for manufacturers goes beyond merely swapping ingredients. They now grapple with the tension between clean-label marketing and the economics of shelf life. Natural preservatives, such as rosemary extract and mixed tocopherols, offer inconsistent antimicrobial benefits influenced by factors like pH, water activity, and storage conditions. Highlighting the industry's pivot, Syensqo unveiled "Riza", a rosemary-based antioxidant platform, in September 2024. This platform, part of their GBP 45 million (USD 57 million) acquisition of Azerys in July 2024, underscores the race among suppliers to cater to both discerning consumers and technical performance standards. While the Food Standards Agency's consistent 79% consumer trust rating lends credibility to this shift, the 30-50% cost premium for natural alternatives poses a significant hurdle, one that only scaling and advancements in fermentation technology might overcome.

Growth of the United Kingdom ready-to-eat and online grocery channels

By 2030, the ready meals segment is set to grow at a CAGR of 7.82%, outpacing the broader market by 245 basis points. This growth is fueled by the rise of online grocery shopping and distribution networks that prioritize extended shelf-life without the need for refrigeration. As a result, there's a surge in demand for combo-preservatives. Manufacturers are now using modified atmosphere packaging in tandem with natural antimicrobials, aiming for shelf-lives of 14-21 days to align with e-commerce logistics. Addressing this demand, Kemin is set to launch Shield V in 2024. This buffered vinegar-botanical mold inhibitor offers clean-label benefits for high-moisture bakery and prepared meals, all without the need for E-number disclosures. However, challenges arise in the United Kingdom's humid supply chain. Here, traditional sorbate-benzoate blends lose their potency, pushing the industry towards innovative preservation methods. These new strategies meld organic acids, plant extracts, and controlled atmospheres. Meanwhile, private-label products, holding a 63% volume share and dominating 90% of discounter shelves, are driving this evolution. Retail giants like Tesco and Sainsbury's, grappling with a slim 3.0% margin pressure as reported by the Competition and Markets Authority, are on the lookout for cost-effective preservative solutions to extend shelf-life.

Regulatory pressure limiting synthetic nitrites and sulphites

In 2024, the Food Standards Agency intensified its scrutiny of synthetic preservatives, notably nitrites in meats and sulphites in dried fruits and wines. This has prompted manufacturers to seek out natural alternatives, even at the expense of cost and efficacy. While the Agency hasn't outright banned these substances, its 2024 guidance underscores the principle of keeping nitrite use "as low as reasonably achievable." This creates a compliance gray area, nudging manufacturers towards reformulation to sidestep potential litigation. Further complicating matters, trace limits for ethylene oxide, set at 0.1 mg/kg for gums and 0.02 mg/kg for polysorbates, disrupted supply chains in 2024. This led to ingredient substitutions in bakery, confectionery, and sauce applications. The market is now split: larger manufacturers, buoyed by research and development budgets, are turning to fermentation-derived antimicrobials like nisin and natamycin. In contrast, smaller processors grapple with a cost-efficacy dilemma, jeopardizing their profit margins. A case in point is Corbion's August 2025 collaboration with Brain Biotech, aiming to pioneer bio-based preservation technologies. However, with commercialization stretching over 2-3 years, immediate reformulations will depend on existing natural extracts, which come with inconsistent performance.

Retail private-label reformulation race

With private-label products commanding a 63% share in volume and 55% in value, retailers have emerged as the primary gatekeepers for preservative innovations. However, these retailers grapple with a 3.0% operating margin, setting a cost ceiling that natural preservatives find challenging to breach. A stark contrast emerges when comparing the outcomes of two initiatives: the voluntary sugar-reduction program, which managed a mere 3.5% reduction against its ambitious 20% target, and the mandatory Soft Drinks Industry Levy, achieving a commendable 45% cut. This disparity underscores a key insight from the United Kingdom Government: retailer-driven reformulations, in the absence of regulatory nudges, yield only modest advancements. Consequently, suppliers are pivoting their competition strategy, focusing on the cost-per-day-of-shelf-life metric rather than solely on ingredient purity. This shift has spurred a rising demand for hybrid solutions, merging synthetic and natural preservatives to meet desired price-performance benchmarks. A 2024 survey by Action on Salt highlights an 85% compliance rate with voluntary salt targets. This success, attributed to innovations like Kerry's Tastesense and Tate & Lyle's SODA-LO sodium reducers, underscores a pivotal lesson: reformulation triumphs when suppliers leverage innovation to absorb costs, rather than shifting them downstream. The bakery and confectionery sectors present a lucrative opportunity, boasting a 33.92% market share in 2024. With ambient distribution needs and a push for preservatives that extend shelf life sans E-numbers, these sectors are ripe for high-volume reformulation endeavors.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and variable efficacy of natural preservatives | -0.6% | National, with acute pressure in cost-sensitive private-label segments | Short term (≤ 2 years) |

| Technical hurdles in the humid United Kingdom ambient bakery supply chain | -0.4% | National, concentrated in the ambient bakery and confectionery distribution | Medium term (2-4 years) |

| Ethylene-oxide trace-limit rule disrupting gum/polysorbate inputs | -0.3% | National, FSA jurisdiction with supply-chain impact across the EU-United Kingdom trade | Short term (≤ 2 years) |

| Consumer backlash on "E-numbers" labelling | -0.5% | National, with higher intensity in urban and health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost and variable efficacy of natural preservatives

Natural preservatives, while commanding a 30-50% cost premium over their synthetic counterparts, exhibit significant variability in antimicrobial performance. This variability, influenced by factors such as pH ranges, water activity levels, and storage temperatures, creates a cost-efficacy dilemma. This dilemma particularly hampers adoption in price-sensitive private-label segments. For instance, Nisin, known for its effectiveness against gram-positive bacteria like Listeria, loses its potency in high-pH applications. Similarly, natamycin, valued for its antifungal properties, degrades under UV exposure[1]Source: International Association for Food Protection, “Effectiveness of Natural Preservatives Under Different pH Conditions,” foodprotection.org . As a result, manufacturers often resort to overdosing or combining multiple preservatives to meet desired shelf-life targets. This challenge is further intensified by supply-chain volatility, especially for botanical extracts like rosemary. Here, harvest yields and extraction efficiencies are susceptible to fluctuations in weather and advancements in processing technology. The market's strategic landscape reveals a clear divide: premium brands are willing to absorb the cost differential, positioning themselves as clean-label champions. In contrast, private-label products, which hold a 63% volume share, remain tethered to synthetic options like sorbates and benzoates. These synthetic alternatives, while delivering consistent performance, come at a more economical price point. On the horizon, fermentation-derived solutions, such as Chr. Hansen's antimicrobial cultures, present a promising middle ground. By harnessing biotechnology, they aim to scale natural production. However, with commercialization timelines stretching 2-3 years, the near-term adoption is still hampered by concerns over cost and technical risks.

Technical hurdles in the humid United Kingdom ambient bakery supply chain

In the United Kingdom, the ambient bakery distribution network grapples with high humidity and temperature fluctuations during transport and retail display. These challenges often lead to mold and yeast issues, which natural preservatives find hard to tackle cost-effectively. While traditional calcium propionate works effectively at a dosage of 0.1-0.3%, it faces consumer pushback due to its E-number labelling. On the other hand, natural alternatives such as vinegar and cultured wheat, though effective, need 2-3 times higher concentrations to match the shelf-life of calcium propionate. This increased concentration can alter taste and texture profiles, as highlighted by the Food Standards Agency. This challenge is especially pronounced in the bakery and confectionery segment, which commanded a 33.92% market share in 2024. This segment depends on a 7-14 day ambient shelf-life to facilitate nationwide distribution from centralized production facilities. In response to these challenges, Kemin introduced 'Shield V' in 2024, a buffered vinegar-botanical blend. By merging organic acids with plant extracts, 'Shield V' offers mold inhibition without compromising on flavor. However, its adoption is hindered by a 40-50% cost premium over synthetic propionates. This scenario presents a strategic dilemma for manufacturers: they can either invest in controlled-atmosphere packaging to lessen preservative use, accept a shorter shelf-life leading to increased waste, or continue using synthetic preservatives despite mounting clean-label pressures.

Segment Analysis

By Product Type: Natural Preservatives Gain Despite Cost Headwinds

Natural preservatives are projected to grow at a 5.79% CAGR through 2031, surpassing the market by 74 basis points, while synthetic alternatives held a 44.66% share in 2025. This shift reflects manufacturers layering natural antimicrobials like nisin, natamycin, and rosemary extract over synthetic bases to achieve clean-label claims and cost-effective shelf life. Nisin, effective against Listeria and Clostridium, is used in ready meals and processed meats despite its 50-70% cost premium over sorbates. Natamycin's antifungal properties make it vital for cheese coatings and bakery applications, despite E235 labeling. Vinegar-based preservatives, leveraging acetic acid, are gaining share in sauces and dressings, offsetting higher dosage needs with flavor compatibility. Rosemary extract and mixed tocopherols, antioxidants rather than antimicrobials, are replacing synthetic BHA and BHT in edible oils and snacks to combat rancidity.

Synthetic preservatives like sorbates, benzoates, and propionates dominate cost-sensitive applications such as private-label bakery and confectionery due to their low dosage (0.1-0.3%) and predictable efficacy. Calcium propionate leads ambient bakery preservation despite E-number backlash, as its mold-inhibiting performance in high-moisture environments outperforms vinegar or cultured wheat at similar costs. Potassium sorbate retains use in beverages and dairy, where pH control ensures low-dosage efficacy, while benzoates face gradual displacement over benzene-formation concerns in acidic formulations. Fermentation-derived preservatives, such as cultured dextrose and fermented sugar, occupy a regulatory gray zone, enabling clean-label claims without the cost of botanical extracts. Corbion's August 2025 partnership with Brain Biotech to develop bio-based antimicrobials highlights this innovation, targeting commercialization within 2-3 years to address the cost-efficacy gap.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Ready Meals Outpace Bakery as Shelf-Life Economics Shift

Ready meals are projected to grow at a 7.35% CAGR through 2031, driven by online grocery expansion and distribution networks requiring extended shelf-life without refrigeration. Unlike bakery items, ready meals have unique preservative needs due to multi-component formulations with varying pH and water activity across proteins, starches, and vegetables. These require tailored antimicrobial strategies combining organic acids, plant extracts, and modified atmosphere packaging to achieve 14-21 day shelf-life targets. Consumer scrutiny adds complexity, as seen with Marks & Spencer's "Eat Well" range, criticized for over 30 ingredients, including stabilizers and emulsifiers. Manufacturers must balance preservative efficacy with clean-label demands. Kemin’s 2024 launch of "Shield V," a buffered vinegar-botanical blend, addresses this by inhibiting mold in high-moisture applications without E-number disclosure, though its 40-50% cost premium limits adoption to premium ready-meal tiers.

Bakery and confectionery, holding a 33.18% share in 2025, face challenges from the United Kingdom's humid supply chain, where mold and yeast issues require preservatives that conflict with clean-label trends. Calcium propionate, used at 0.1-0.3% dosage, faces backlash due to its E-number status, prompting a shift to alternatives like vinegar and cultured wheat, which require 2-3 times higher concentrations, affecting taste and texture. Meat and poultry are also transitioning as regulatory scrutiny on synthetic nitrites drives adoption of natural alternatives like celery powder (containing natural nitrates) and cherry powder, though these pose challenges in color stability and pathogen control. Other segments, including snacks, sauces, dressings, and edible oils, have distinct preservative needs. Oils and snacks focus on lipid oxidation control (using tocopherols and rosemary extract), while aqueous sauces prioritize microbial inhibition (with sorbates and benzoates). Application-specific innovation is critical, suppliers who customize preservative systems to meet the unique pH, water activity, and distribution needs of each category will gain a competitive edge, while generic solutions risk margin compression from private-label competition.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

This market analysis focuses on the United Kingdom, highlighting the Southeast England food-manufacturing corridor and Midlands processing hubs as key centers of preservative demand. These hubs supply retail networks nationwide. Post-Brexit trade frictions have complicated raw material sourcing, particularly for imported botanical extracts like rosemary and fermentation substrates. Manufacturers now balance cost advantages from EU suppliers with the resilience of domestic blending and toll manufacturing. Brenntag's 2024 acquisitions of Monarch Chemicals UK (GBP 35.1 million, USD 44.5 million) and Lawrence Industries UK (GBP 30 million, USD 38 million) emphasize the value of distribution networks that combine imported natural extracts with domestic carriers to meet clean-label and cost demands. While the Food Standards Agency aligns with EU standards, ensuring regulatory continuity, potential divergence, such as adopting more lenient thresholds for natural preservatives, which could reshape long-term formulation strategies and support domestic processing.

Food-manufacturing clusters in the United Kingdom primarily serve nationwide retail chains, resulting in standardized formulations and minimal regional variations. However, Scotland's regulatory framework under Food Standards Scotland and Northern Ireland's partial EU alignment create niche compliance challenges. Larger manufacturers address these with dual-formulation strategies, while smaller processors face higher costs. This dynamic creates a two-tier supply chain: multinationals like DSM-Firmenich, Corbion, and Kerry Group produce pan-United Kingdom formulations meeting the strictest standards, while regional distributors customize blends to exploit cost advantages in less-regulated segments. The rise of online grocery shopping in 2024-2025 is reshaping distribution, with delivery windows extending from 2-3 days to 5-7 days. This shift drives demand for preservative systems that maintain organoleptic quality during longer ambient exposure without triggering E-number disclosures.

With 79% of United Kingdom consumers trusting the Food Standards Agency, regulatory support exists for preservative innovation. However, 29.7% of shoppers actively reducing additive intake signals a shift that regulatory approval alone cannot address. Manufacturers are now competing on transparency and consumer education, with clean-label claims increasingly backed by third-party certifications and enhanced supply-chain traceability that exceed FSA standards. Scotland and Wales offer untapped potential, as their food-processing clusters lag behind Southeast England. Localized preservative blending and distribution in these regions could reduce logistics costs while meeting clean-label requirements. Tate & Lyle's USD 1.8 billion acquisition of CP Kelco, finalized in Q4 2024, positions the company to supply compliant pectin and cellulose gums from United Kingdom blending facilities. However, this transition requires reformulating around alternative hydrocolloids with distinct functional properties.

Competitive Landscape

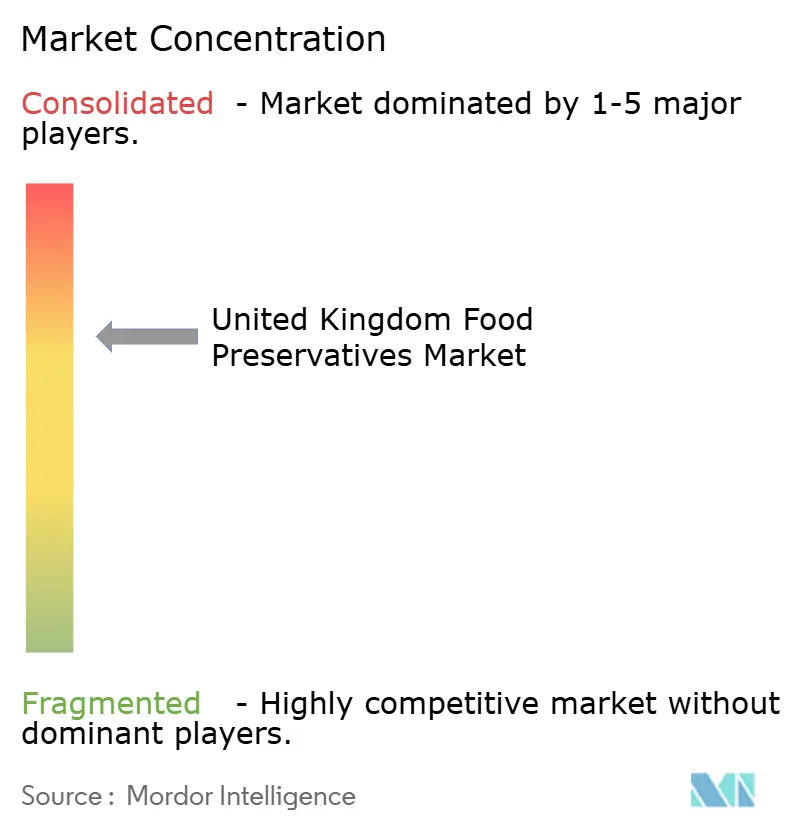

The United Kingdom food preservatives market is moderately fragmented, with the top five suppliers, Tate & Lyle, Kerry Group, Cargill, DSM-Firmenich, and Corbion, holding a significant share. Regional distributors such as Brenntag and Univar Solutions, along with specialty suppliers like Kemin and Chr. Hansen, focus on application-specific formulations and technical services. Strategic positioning revolves around three main axes: utilizing fermentation-derived natural preservatives for cost-efficacy, leveraging distribution networks to blend imported extracts domestically, and forming technical partnerships to customize preservative systems based on customer needs, like pH and shelf-life. Corbion's partnership with Brain Biotech in August 2025 aims to develop bio-based antimicrobials, showcasing the innovation needed to challenge synthetic products. With a target commercialization of 2-3 years, this move could significantly influence market shares. In June 2024, Tate & Lyle made waves with a USD 1.8 billion acquisition of CP Kelco, marking the segment's largest merger and acquisition deal. This acquisition not only secures pectin and gum portfolios but also addresses disruptions from ethylene oxide trace limits. Furthermore, it allows Tate & Lyle to venture into higher-margin texture-modification areas, expanding beyond just commodity preservatives.

There's potential in hybrid preservative systems that merge synthetic bases with natural topcoats. This approach can secure clean-label claims without incurring full reformulation costs, making it attractive to private-label suppliers with tight 3.0% margin constraints. New players on the scene include precision-fermentation startups, which are scaling up the production of antimicrobial peptides and organic acids. However, the capital-intensive nature of their operations, combined with regulatory approval timelines stretching 3-5 years, curtails their immediate market influence. Technology adoption in the sector is divided: industry giants like Cargill and DSM-Firmenich are turning to high-pressure processing and modified atmosphere packaging to lessen preservative usage. In contrast, smaller processors, constrained by capital, stick to traditional single-preservative methods.

This landscape hints at a consolidation trend, as integrated suppliers, benefiting from scale economies in fermentation and distribution, can spread research and development and logistics costs over a wider portfolio. This leaves smaller niche players at risk of margin compression or acquisition. Brenntag's 2024 acquisitions of Monarch Chemicals, Lawrence Industries, and Solventis Group in the UK highlight this trend, as distributors bolster regional blending capacities to challenge the direct-sales strategies of multinational suppliers.

United Kingdom Food Preservatives Industry Leaders

Cargill, Incorporated

Corbion N.V.,

Tate & Lyle PLC

Kerry Group plc

Koninklijke DSM N.V

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Corbion announced a strategic partnership with Brain Biotech to co-develop natural preservation technologies leveraging fermentation-derived antimicrobials. The collaboration targets bio-based solutions that address clean-label demand while closing the cost-efficacy gap versus synthetic preservatives, with commercialization expected within 2-3 years across bakery, ready meals, and meat applications.

- June 2024: Tate & Lyle completed its USD 1.8 billion acquisition of CP Kelco, securing global leadership in pectin and specialty gums. The transaction addresses ethylene-oxide trace-limit disruptions by providing compliant hydrocolloid portfolios while expanding into texture-modification adjacencies that command premium pricing versus commodity preservatives.

- July 2024: Brenntag acquired Monarch Chemicals UK for GBP 35.1 million (USD 44.5 million), adding blending and distribution facilities that strengthen its position in natural food additives UK suppliers. The acquisition enables Brenntag to aggregate imported botanical extracts with domestic carriers, meeting clean-label requirements while optimizing logistics costs across Southeast England and Midlands manufacturing hubs.

United Kingdom Food Preservatives Market Report Scope

The United Kingdom food preservatives market offers a variety of preservatives including natural and synthetic types applicable to beverage, dairy & frozen products, bakery, meat, poultry & seafood, confectionery, sauces & salad mixes, and other industries. The report contains top-line revenues and market share analysis of the key players, highlighting the most adopted strategies of the companies in the market studied.

Product Type

| Synthetic | Sorbates |

| Benzonates | |

| Propionates | |

| Other | |

| Natural | Nisin |

| Natamycin | |

| Vinegar | |

| Rosemary Extract | |

| Mixed Tocopherols | |

| Others |

Application

| Bakery and Confectionery |

| Meat and Poultry |

| Ready Meals |

| Sweet and Savory Snacks |

| Sauces and Dressings |

| Edible Oils |

| Other Applications |

| Product Type | Synthetic | Sorbates |

| Benzonates | ||

| Propionates | ||

| Other | ||

| Natural | Nisin | |

| Natamycin | ||

| Vinegar | ||

| Rosemary Extract | ||

| Mixed Tocopherols | ||

| Others | ||

| Application | Bakery and Confectionery | |

| Meat and Poultry | ||

| Ready Meals | ||

| Sweet and Savory Snacks | ||

| Sauces and Dressings | ||

| Edible Oils | ||

| Other Applications | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the United Kingdom food preservatives market?

The United Kingdom food preservatives market size is USD 69.04 billion in 2026.

How fast is the category of natural preservatives growing?

Natural preservatives are expanding at a 5.79% CAGR through 2031, faster than overall market growth.

Which application is seeing the quickest preservative demand growth?

Ready meals lead with a 7.35% CAGR as e-grocery adoption extends ambient shelf-life needs.

Why are synthetic preservatives still prevalent in private-label products?

Private-label lines face tight 3.0% operating margins, making low-cost sorbate, benzoate, and propionate solutions essential to hit shelf-life targets economically.

How does high-pressure processing influence preservative usage?

HPP lets manufacturers cut sorbate and benzoate levels by 30 to 40%, enabling “cleaner” labels without sacrificing safety, though the equipment investment limits uptake to large processors.

What impact does Brexit have on preservative sourcing?

Post-Brexit customs friction encourages domestic blending and fermentation capacity, but limits the United Kingdom's botanical cultivation, keeping many natural inputs reliant on EU imports.