Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

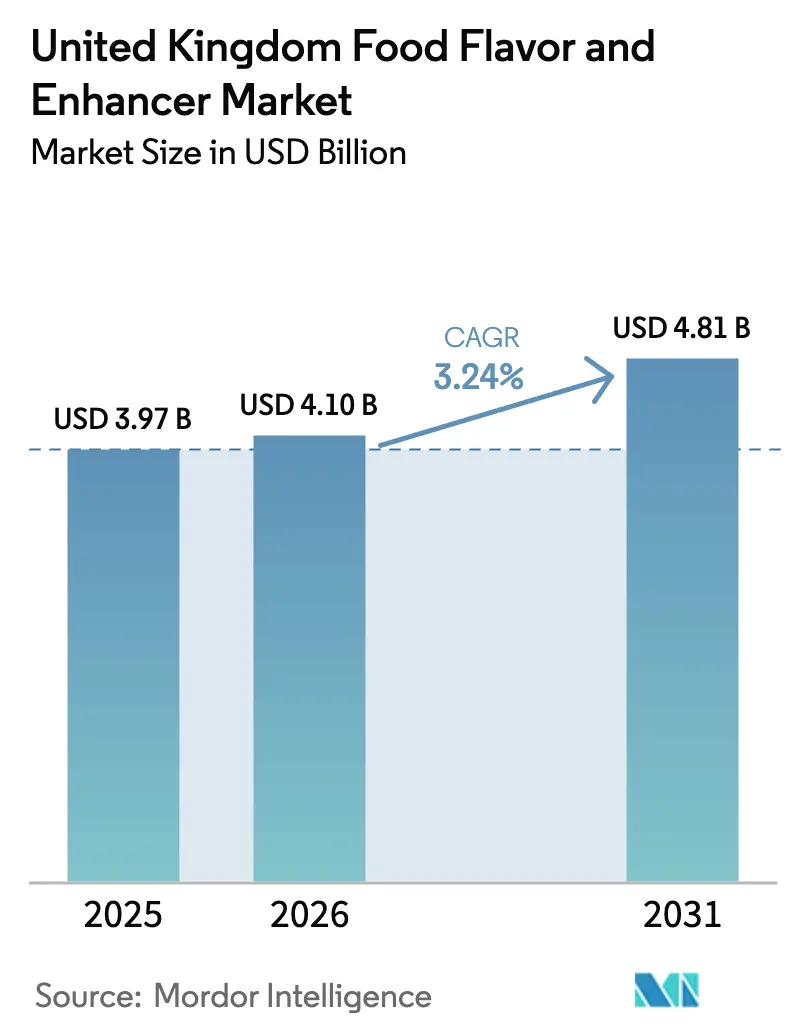

| Base Year Market Size (2025) | USD 3.97 Billion |

| Market Size (2026) | USD 4.1 Billion |

| Market Size (2031) | USD 4.81 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Food Flavor And Enhancer Market Analysis by Mordor Intelligence

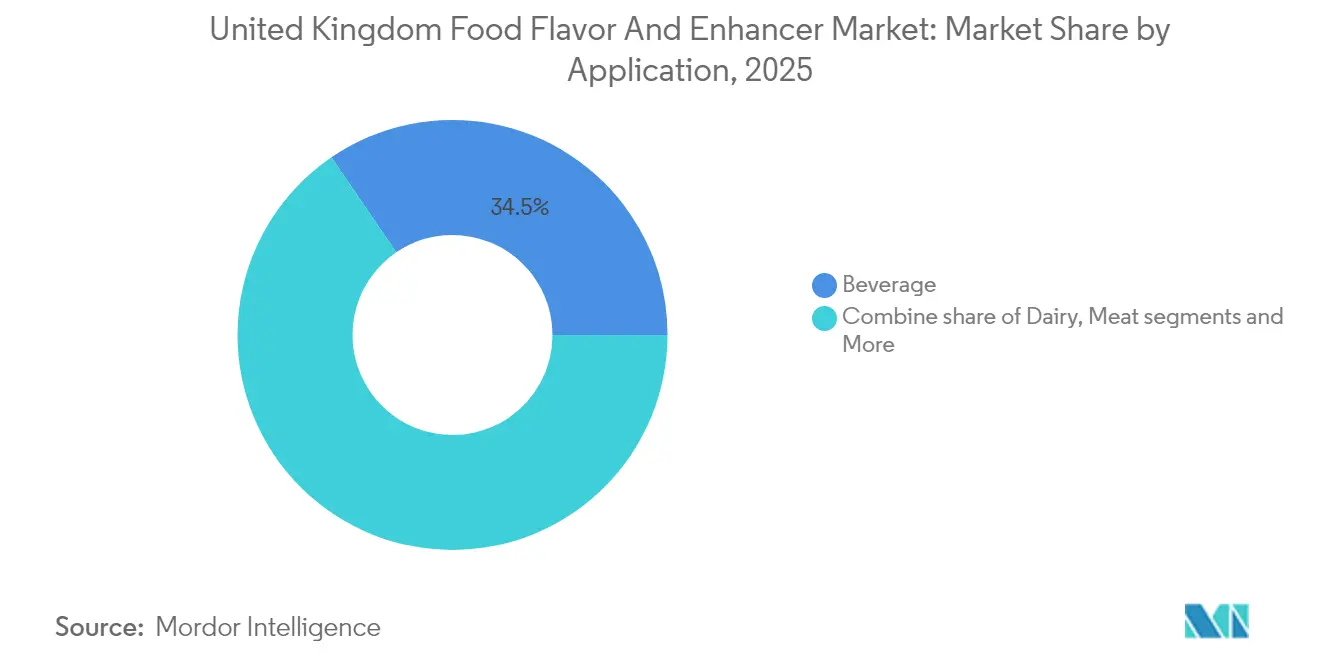

The United Kingdom food flavor and enhancer market size was valued at USD 3.97 billion in 2025 and estimated to grow from USD 4.1 billion in 2026 to reach USD 4.81 billion by 2031, at a CAGR of 3.24% during the forecast period (2026-2031). This growth reflects various influencing factors, including clean-label reformulation, post-Brexit regulatory changes, and efforts to enhance the taste of plant-based foods. Food flavors currently account for 66.13% of the market value and are expected to grow at the fastest rate, with a CAGR of 4.83%, driven by innovations in natural extracts and biotechnology-derived ingredients that align with Food Standards Agency (FSA) compliance and consumer preferences. Liquid formats hold a 40.21% market share; however, powder formulations are anticipated to grow at a CAGR of 4.73%, favored for their shelf stability, cost-effectiveness in transportation, and versatility in dry mixes. Beverages lead in application with a 34.92% share, but hybrid dairy applications, such as cow-milk-and-oat blends, are forecast to grow at the highest CAGR of 5.10%, meeting lactose-free requirements while improving consumer acceptance.

Key Report Takeaways

- By product type, food flavors led with 65.48% share in 2025 while growing at a 4.59% CAGR through 2031.

- By form, liquid formats controlled 39.56% of 2025 revenue, yet powder formats are forecast to accelerate at a 4.51% CAGR to 2031.

- By application, beverages held 34.52% of the 2025 United Kingdom food flavor and enhancer market share, and dairy is projected to expand at a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Food Flavor And Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for clean-label, natural, minimally processed flavors in packaged foods | +0.9% | United Kingdom, spillover to Republic of Ireland | Medium term (2-4 years) |

| Rising demand for advanced flavors in plant-based, vegan, and flexitarian diets | +0.7% | United Kingdom, with concentration in urban centers (London, Manchester, Edinburgh) | Medium term (2-4 years) |

| Expansion of the United Kingdom beverage sector driving liquid and specialty flavor demand | +0.6% | United Kingdom, led by England and Scotland | Short term (≤ 2 years) |

| Foodservice innovation requiring stable process flavors and enhancers | +0.5% | United Kingdom, emphasis on competitive socialising venues | Short term (≤ 2 years) |

| Increased demand for sugar-reduced products boosting sweetness modulators and enhancers usage | +0.4% | United Kingdom, aligned with Public Health England targets | Long term (≥ 4 years) |

| Flavor enhancers in meat substitutes delivering umami and savory depth | +0.4% | United Kingdom, early adopters in metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing preference for clean-label, natural, minimally processed flavors in packaged foods

Consumer scrutiny of ingredient lists has intensified, with 68% of shoppers in the United Kingdom actively seeking natural flavorings and 63% preferring recognizable ingredients, according to 2024 survey data [1]Source: Food Standard Agency, “Food & You 2 trends: Introduction,” food.gov.uk. This growing demand has resulted in a decline in the use of synthetic aroma chemicals and propylene glycol carriers, encouraging a transition toward water-soluble botanical extracts and supercritical carbon dioxide (CO₂) isolates. Precision fermentation has emerged as a practical alternative, enabling microorganisms that are specifically engineered to produce compounds such as vanillin or citrus aldehydes to achieve "natural" status under Food Standards Agency (FSA) guidelines. This is possible as long as the precursor substrate used in the process is plant-derived. Additionally, this method helps address the cost fluctuations associated with sourcing vanilla beans or bergamot peel. In 2024, Melt&Marble successfully raised EUR 5 million to expand the production of fermentation-derived animal-free fats that closely replicate dairy lipid profiles. These fats are targeted for use in hybrid yogurt and cheese applications, where clean-label claims play a significant role in supporting premium product positioning.

Rising demand for advanced flavors in plant-based, vegan, and flexitarian diets

The United Kingdom plant-based retail market experienced a contraction in its year-on-year performance, drawing attention to a significant gap in taste satisfaction. Among consumers who have discontinued purchasing, a majority attributed their decision to inferior flavor, while a substantial portion pointed to higher price points as a deterrent. Meat-alternative products have achieved household penetration in a considerable number of homes; however, the frequency of repeat purchases remains lower compared to dairy-alternative products. This trend suggests that current flavor enhancers, such as umami and kokumi additives, are not effectively replicating the complex flavors associated with the Maillard reaction, which is responsible for the savory taste of grilled beef or roasted chicken. Kerry Group's SucculencePB platform seeks to address the perception of juiciness by utilizing hydrocolloid-lipid emulsions, while Biospringer's yeast extracts provide savory, glutamate-rich flavor profiles without the need for a monosodium glutamate declaration, which is crucial for maintaining clean-label product positioning. Hybrid formulations, which combine animal protein with plant-based ingredients in varying proportions, are gaining traction as a practical compromise. These formulations require advanced flavor systems that can effectively mask undesirable pea or soy aftertastes while enhancing the overall meaty flavor profile. Research published in the Foods journal highlighted that consumers in the United Kingdom tend to reject cream cheese alternatives with nutty or oat-forward flavor notes. Instead, they show a clear preference for options that deliver creamy, smooth, and savory taste profiles.

Expansion of the United Kingdom beverage sector driving liquid and specialty flavor demand

The British Soft Drinks Association reported a retail volume of ~15 billion liters for 2024 [2]Source: British Soft Drinks Association, “UK Soft Drinks Report 2024,” britishsoftdrinks.com. Functional beverages have experienced notable growth, increasing by over 25% year-on-year, as consumers increasingly seek products offering benefits such as immunity support, energy enhancement, and improved gut health alongside hydration. Liquid flavor formats continue to dominate this category due to their superior dispersibility in aqueous systems and compatibility with hot-fill or aseptic processing methods, which are widely utilized in the industry. DSM-Firmenich's PrimeLock+ encapsulation technology has been developed to stabilize volatile citrus and tropical flavor notes. This is achieved through spray-drying with modified starches, effectively preventing oxidation and ensuring a shelf life of up to one year under ambient conditions. Additionally, sugar reduction mandates, which have significantly decreased the sugar content in soft drinks in recent years, have driven demand for sweetness modulators. These modulators enhance the perception of sucrose at lower concentrations, reducing caloric content without introducing the bitter or metallic aftertastes often associated with high-intensity sweeteners like stevia [3]Source: Public Health England Report “Producing and labelling food if there's no Brexit deal,” gov.uk .

Foodservice innovation requiring stable process flavors and enhancers

Competitive socializing venues, which combine dining with activities such as darts, mini-golf, or arcade games, experienced a remarkable 455% growth in the United Kingdom between 2018 and 2024. This significant expansion has created a strong demand for bold and visually appealing flavors that can withstand high-temperature cooking methods such as deep-frying, grilling, or baking. Process flavors must be able to endure thermal stress, with Maillard reaction products (chemical reactions between amino acids and reducing sugars), smoke condensates, and encapsulated spice oleoresins ensuring consistent flavor intensity. These flavors are designed to perform effectively whether applied to frozen potato products reheated at 200 degrees Celsius or battered proteins fried at 180 degrees Celsius. Kerry Group's Red Arrow smoke flavors and cooking-method profiles, including chargrilled, roasted, and pan-seared options, enable chefs to replicate back-of-house cooking techniques on a larger scale. This approach reduces labor costs while ensuring uniformity across batches. Furthermore, Mondelez International's 2025 bakery trend analysis identified fusion flavors, such as Middle Eastern options like rosewater, tahini, and pistachio, as well as West African flavors like hibiscus and baobab, as key differentiators in the premium segment. Operators in this segment achieve 30% higher check averages compared to value chains such as Greggs. Flavor stability under freeze-thaw cycles is equally critical. Liquid concentrates that are prone to phase separation or crystallization can result in waste and inconsistent dosing, ultimately impacting product quality and operational efficiency.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict United Kingdom and European Union regulations on food additives, labeling, and usage limits | -0.5% | United Kingdom, with Northern Ireland subject to EU Regulation 1334/2008 | Long term (≥ 4 years) |

| Evolving clean-label demands limiting synthetic flavor and enhancer usage | -0.4% | United Kingdom, accelerated in premium and health-focused segments | Medium term (2-4 years) |

| Supply-chain challenges for specific botanicals and plant-based flavor precursors | -0.3% | United Kingdom, dependent on imports from EU, Asia, and Africa | Short term (≤ 2 years) |

| High Research and Development (R&D) costs for customized clean-label flavor systems | -0.3% | United Kingdom, impacting mid-tier suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict United Kingdom and European Union regulations on food additives, labeling, and usage limits

The Food Standards Agency's (FSA) removal of 22 flavouring substances from the authorised list in 2024, along with the reduction of ethylene oxide residue limits to 0.1 milligrams per kilogram, has necessitated widespread reformulation in spice blends, seasonings, and savory snacks. Post-Brexit regulatory divergence has further increased compliance challenges as Great Britain follows retained European Union (EU) law with incremental amendments, while Northern Ireland remains aligned with EU Regulation 1334/2008. This divergence requires suppliers serving both markets to conduct dual-specification production runs. Obtaining Novel Foods authorisation for fermentation-derived ingredients can take over 18 months and incur costs exceeding GBP 100,000 (approximately USD 127,000) due to dossier preparation, toxicology studies, and administrative fees. These factors delay the commercialisation of precision-fermented products such as vanillin, cocoa, and dairy proteins. Additionally, maximum usage levels for glutamates (E620-E635) are restricted to 10 grams per kilogram in most categories, limiting formulation flexibility in high-umami applications like bouillon cubes and instant noodles. Traceability requirements under the Food Information to Consumers Regulation mandate full ingredient disclosure, which exposes proprietary flavor blends to potential reverse engineering. This poses a significant challenge for smaller formulators, as it undermines their competitive advantage.

Evolving clean-label demands limiting synthetic flavor and enhancer usage

Approximately 73% of consumers in the United Kingdom express concerns about artificial additives, with 52% regularly checking ingredient lists before making purchases. This scrutiny effectively restricts the use of formulations containing nature-identical or artificial flavorings. Retailers such as Tesco and Sainsbury's have implemented private-label standards that prohibit certain E-numbers, even when legally permissible, compelling suppliers to reformulate their products or face the risk of delisting. This trend particularly impacts synthetic flavoring agents like vanillin (lignin-derived), benzaldehyde (almond flavor), and diacetyl (butter flavor), which, despite offering cost advantages of 80 to 90 percent compared to natural alternatives, are perceived negatively by consumers. The growing preference for botanical extracts and fermentation-derived ingredients has increased raw material costs by 30 to 50 percent, putting pressure on margins for mid-sized flavor manufacturers that lack vertical integration or economies of scale. Additionally, clean-label requirements restrict the use of carrier solvents such as propylene glycol or triacetin, necessitating the adoption of water-soluble or powder formats. These alternatives, however, may compromise flavor intensity or shelf stability. Brands operating in this environment must carefully balance claims of authenticity with sensory performance, often requiring multiple reformulation cycles and extensive consumer testing to meet both regulatory and consumer expectations.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Flavors Outpace Synthetic as Clean-Label Mandates Intensify

In 2025, food flavors accounted for 65.48% of the market share and are projected to grow at a compound annual growth rate (CAGR) of 4.59% through 2031. This growth surpasses that of food enhancers, driven by the broader application versatility and premiumization opportunities in segments such as beverages, dairy, and confectionery. Natural flavors, extracted through methods like steam distillation, solvent extraction, or supercritical carbon dioxide (CO₂), are increasingly replacing synthetic alternatives. This shift is influenced by retailers enforcing private-label standards that exclude nature-identical compounds, even when chemically identical to botanical sources.

Precision fermentation is emerging as a hybrid production method. Companies like Ginkgo Bioworks and Melt&Marble are engineering microorganisms to produce vanillin, cocoa butter equivalents, and dairy lipids that meet the "natural" criteria under Food Standards Agency (FSA) definitions. This approach helps mitigate the cost volatility of raw materials such as vanilla beans, priced at USD 400-600 per kilogram in 2024, and cocoa, priced at USD 3,000-4,000 per metric ton.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Powder Formats Gain as Shelf Stability and Cost Efficiency Trump Liquid Convenience

In 2025, liquid flavors accounted for 39.56% of the market share, driven by their superior dispersion in aqueous beverage systems and compatibility with hot-fill or aseptic processing. However, powder formats are projected to grow at the fastest rate, with a compound annual growth rate (CAGR) of 4.51% through 2031, as manufacturers focus on shelf stability, reduced freight costs, and ease of handling in dry-mix applications. Spray-dried and encapsulated powders offer protection for volatile compounds such as aldehydes, esters, and terpenes from oxidation, extending shelf life to 24 months compared to 12 to 18 months for liquid concentrates stored under ambient conditions. DSM-Firmenich's PrimeLock+ technology utilizes modified starches and maltodextrins to encapsulate citrus and tropical oils, preventing flavor degradation in protein shakes and instant beverages.

Liquid flavors maintain dominance in carbonated soft drinks, functional beverages, and dairy products, where emulsification and immediate solubility are critical. Carriers such as propylene glycol and triacetin enable high flavor loading (10 to 50% active content) and prevent phase separation during cold storage. However, clean-label trends are driving a shift toward water-soluble or alcohol-based systems. In 2024, Britvic and AG Barr, two leading soft drink manufacturers in the United Kingdom, reported that concentrate and syrup formats (liquid) accounted for 65% of their flavor procurement by volume, highlighting the structural preference for liquid flavors in the market.

By Application: Dairy Surges as Hybrid Formulations and Functional Positioning Drive Premiumization

Beverage applications accounted for 34.52% of the market share in 2025, representing a retail value of GBP 22.3 billion and a volume of 15.7 billion liters. However, the dairy segment is projected to grow at a higher CAGR of 4.86% through 2031, driven by the rising demand for hybrid yogurt, high-protein formulations, and plant-dairy blends. These products require advanced flavor masking and enhancement solutions. For instance, in November 2024, Arla Foods introduced four yogurt innovations: LactoFREE natural yogurt, Skyr Whipped in three flavors (Strawberries & Cream, Caramelised Orange, Coconut & White Chocolate), and a 45-gram protein yogurt. Each of these products necessitated customized flavor systems to address challenges such as masking lactase enzyme bitterness, delivering indulgent flavor profiles, and enhancing protein perception without chalkiness.

The bakery and confectionery segments collectively account for approximately 20% of the market share, driven by trends in premiumization and fusion flavors. Mondelez's 2025 bakery trend analysis highlighted emerging flavor profiles such as chai, yuzu, miso, and sweet-salty combinations. Additionally, Middle Eastern flavors (e.g., rosewater, tahini, pistachio) and West African profiles (e.g., hibiscus, baobab) have gained popularity, commanding 30% higher check averages in foodservice settings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

England accounts for the largest share of the United Kingdom's food flavor and enhancer market, driven by its substantial population, which represents 84% of the national total (approximately 56 million residents). The concentration of food manufacturing, beverage production, and foodservice innovation in metropolitan areas such as London, Manchester, Birmingham, and Leeds further supports this dominance. The region's diverse application landscape, including premium craft beverages, plant-based dairy alternatives, and competitive socializing venues (which grew by 455% between 2018 and 2024), fuels demand for liquid flavor concentrates and encapsulated powder systems. Key players such as Britvic and AG Barr, both headquartered in England, reported combined soft drink volumes exceeding 1.2 billion liters in 2024, with 71% of these products featuring low or no-calorie claims. This trend has increased the need for sweetness modulators and natural fruit flavors to mask the aftertaste of stevia or sucralose.

Additionally, lean-label mandates are particularly stringent in English retail chains like Tesco, Sainsbury's, and Waitrose, which enforce private-label standards that exclude certain E-numbers, even when legally permitted. Consequently, suppliers are focusing on natural extracts and fermentation-derived ingredients to meet these requirements. The foodservice sector, particularly in London, also drives demand for bold, visually appealing flavor profiles that can endure high-temperature cooking methods. Experiential dining and fusion cuisines, such as Middle Eastern, West African, and Asian, continue to command premium pricing, further boosting the demand for innovative flavor solutions.

Scotland represents a strategically important segment of the market, with the whisky industry's flavor expertise and the craft beverage culture driving demand for premium botanical extracts, smoke flavors, and aged-spirit profiles in non-alcoholic and functional drinks. Urban centers like Edinburgh and Glasgow exhibit consumption patterns similar to England's metropolitan areas. However, rural and coastal regions in Scotland display a stronger preference for traditional savory flavors, such as smoked fish, game meats, and oat-based products, necessitating the use of umami enhancers and process-stable seasonings. The Scottish Government's focus on food and drink exports, with a target of 30 billion British pounds (approximately 38 billion United States dollars) by 2030, encourages flavor innovation in value-added products. Items such as smoked salmon, shortbread, and craft gin benefit from authenticity and provenance narratives, which support premium pricing, as highlighted in the Scottish Government Export Strategy. Additionally, Arla Foods operates dairy processing facilities in Scotland, and its November 2024 launch of LactoFREE and high-protein yogurts reflects the regional demand for functional dairy products. These products cater to consumer preferences for indulgence balanced with health-focused positioning, further driving growth in the market.

Competitive Landscape

The United Kingdom food flavor and enhancer market is moderately concentrated, with the top five multinational companies including Givaudan, DSM-Firmenich, Kerry Group, International Flavors & Fragrances (IFF), and Symrise accounting for a significant share of revenue. These companies leverage vertically integrated supply chains, proprietary encapsulation technologies, and co-creation partnerships with major food and beverage brands. The market focus has shifted toward multifunctional ingredients that combine taste, texture, nutrition, and shelf-life extension into a single platform. This approach streamlines development cycles and reduces formulation complexity for customers. For instance, Givaudan's USD 850 million acquisition of Edlong in March 2024 highlights this trend, enhancing its capabilities in dairy flavors and enzyme modification for hybrid yogurt and cheese applications. Similarly, Kerry Group's acquisitions of Natreon (USD 130 million, January 2024) for Ayurvedic botanicals and Niacet (USD 1 billion, May 2024) for food-preservation acids expand its portfolio into clean-label preservatives and functional ingredients, enabling integrated taste-and-safety solutions.

Opportunities for growth are emerging in precision fermentation, where regulatory pathways are still developing, and capital requirements (GBP 2-10 million for bioreactor infrastructure) favor well-funded players. Mid-tier companies such as Kalsec, MANE, and Takasago maintain niches in natural extracts, botanical sourcing, and regional foodservice channels but face margin pressures. Clean-label reformulations have increased raw-material costs by 30 to 50 percent, limiting their ability to pass on these costs to customers. Technology adoption is advancing rapidly, with artificial intelligence (AI)-driven formulation tools reducing iteration cycles from 12 to 24 months to 6 to 9 months by predicting sensory outcomes based on molecular composition. Givaudan and International Flavors & Fragrances are at the forefront of this capability. Additionally, patent filings in encapsulation, fermentation, and taste-receptor modulation have risen by 40 percent since 2022, reflecting heightened innovation competition.

Regulatory compliance remains a key differentiator. Suppliers with in-house toxicology and regulatory-affairs teams are better equipped to navigate Food Standards Agency (FSA) Novel Foods authorization and post-Brexit dual-specification requirements, enabling faster time-to-market and reduced customer risk. Emerging disruptors include fermentation startups such as Melt and Marble and Ginkgo Bioworks, as well as vertical-farming ventures targeting high-value herbs. However, commercialization timelines for these disruptors are expected to extend beyond 2027 for most initiatives.

United Kingdom Food Flavor And Enhancer Industry Leaders

Givaudan SA

dsm‑firmenich AG

International Flavors & Fragrances Inc.

Kerry Group plc

Sensient Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: JPL Flavours opened a new 75,000‑square‑foot UK headquarters in Bromborough, England, funded by over £11 million, featuring 16 collaborative labs and AI‑enabled product‑development capabilities to support efficient, sustainable flavor creation across sweet, savory, confectionery, dairy and sports nutrition applications.

- April 2025: British Baker introduced new bakery ingredients in the United Kingdom, including salted caramel frosting, natural cocoa flavoring, enzyme-based freshness enhancers, protein blends, and couverture chocolate. These products are designed to enhance flavor, texture, shelf life, and cost efficiency for United Kingdom bakers.

- October 2024: British distributor Daymer Ingredients Ltd and Dutch Food Technology (FoodTech) company Revyve BV announced a UK distribution agreement for Revyve’s yeast‑based, animal‑free, gluten‑free egg‑replacement texturising ingredients, enabling British food and beverage manufacturers to enhance texture, binding and emulsification in clean‑label applications

United Kingdom Food Flavor And Enhancer Market Report Scope

The UK food flavor and enhancer market include revenue generated through bakery and confectionery, dairy, savory, soups, pasta and noodles, beverage, and others. Additionally, the study covers market revenue of product types flavors and flavor enhancers in the United Kingdom.

By Product Type

| Food Flavor | Natural |

| Synthetic | |

| Food Enhancer | Glutamates |

| Yeast Extracts | |

| Others Types |

By Form

| Powder |

| Liquid |

| Others |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

| By Product Type | Food Flavor | Natural |

| Synthetic | ||

| Food Enhancer | Glutamates | |

| Yeast Extracts | ||

| Others Types | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Application | Dairy | |

| Bakery | ||

| Confectionery | ||

| Savory Snack | ||

| Meat | ||

| Beverage | ||

| Other Applications | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the United Kingdom food flavor and enhancer market in 2026?

The United Kingdom food flavor and enhancer market size is USD 4.1 billion in 2026 and is set to reach USD 4.81 billion by 2031.

Which segment grows fastest within the market?

Natural food flavors expand at a 4.59% CAGR, the highest among all product segments through 2031.

Which application area is projected to show the strongest growth?

Dairy applications lead with a 4.86% CAGR, fueled by hybrid yogurt and protein-fortified launches.

Who are the leading companies?

Givaudan, DSM-Firmenich, Kerry Group, IFF, and Symrise together hold a majority revenue share, underscoring moderate market concentration.

What recent regulation affects ingredient selection?

The FSA’s 2024 removal of 22 flavor substances and a stricter ethylene-oxide limit force reformulation across seasonings, snacks, and sauces.