Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

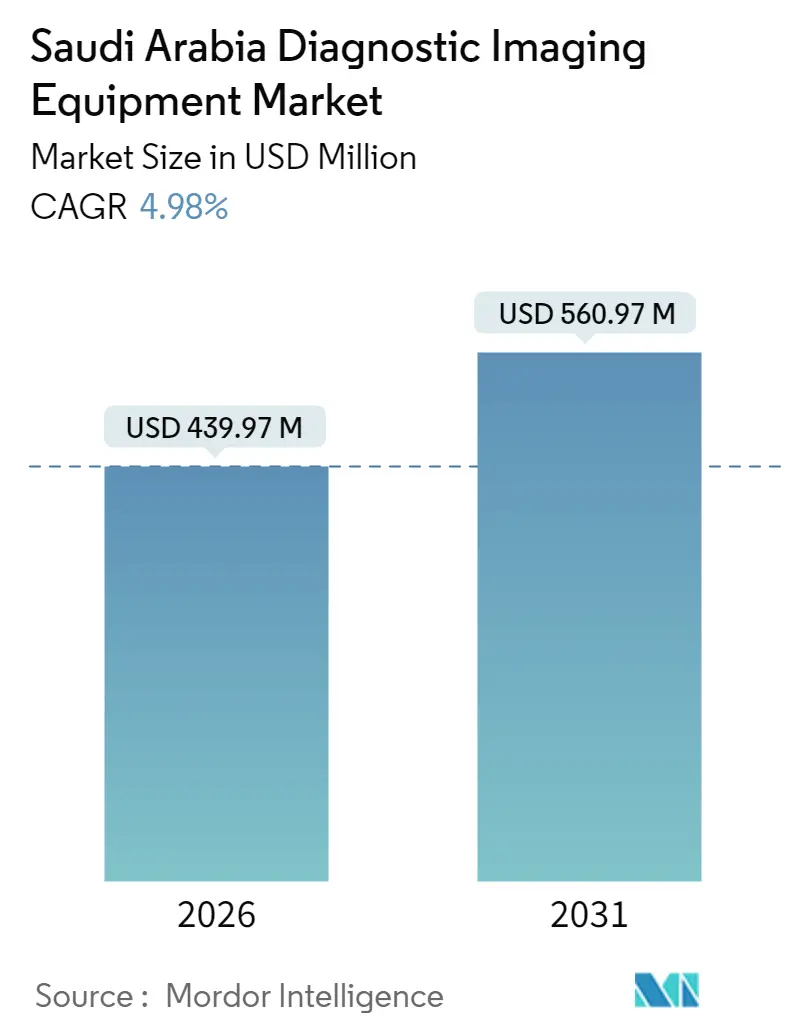

| Market Size (2026) | USD 439.97 Million |

| Market Size (2031) | USD 560.97 Million |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

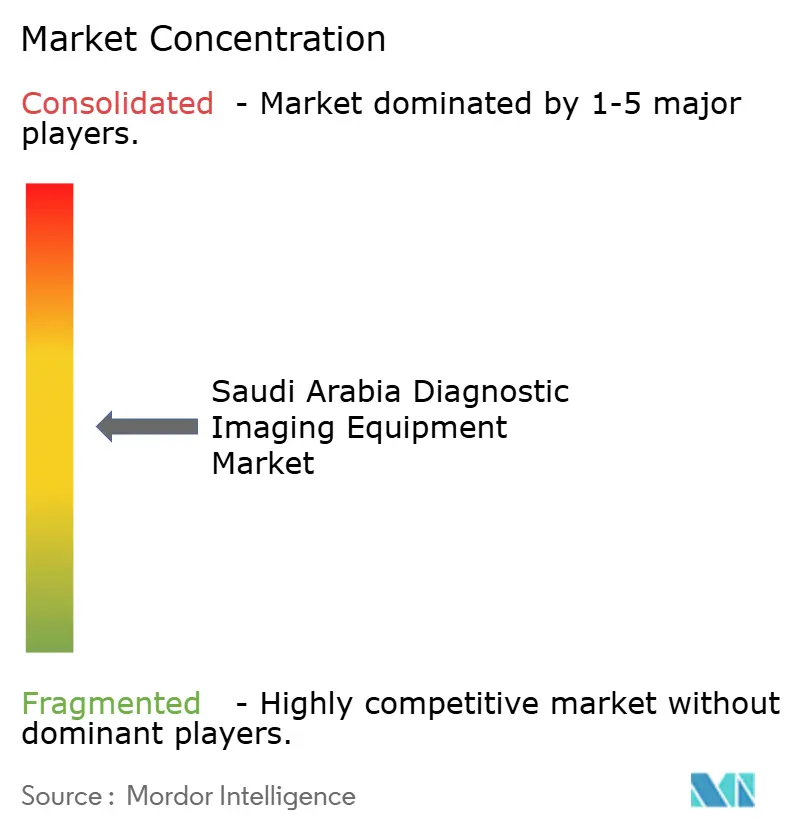

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

Saudi Arabia Diagnostic Imaging Equipment Market size in 2026 is estimated at USD 439.97 million, growing from 2025 value of USD 419.11 million with 2031 projections showing USD 560.97 million, growing at 4.98% CAGR over 2026-2031. This expansion reflects steady capital inflows triggered by Vision 2030, the privatization of public hospitals, and mounting demand for high-resolution modalities that address the Kingdom’s chronic-disease burden.[1]Source: Global Health Saudi, “How Saudi’s Vision 2030 Is Going to Transform the Healthcare Industry,” globalhealthsaudi.com Ongoing AI adoption, increased health-insurance penetration, and an 84,000-bed capacity goal further elevate equipment procurement, while image-exchange networks and virtual hospital initiatives accelerate scan volumes by linking 224 facilities to central radiology hubs. At the same time, the market wrestles with radiologist shortages, device-approval delays, and cybersecurity mandates, factors that temper the growth trajectory but also open niches for teleradiology and autonomous-workflow vendors.

Key Report Takeaways

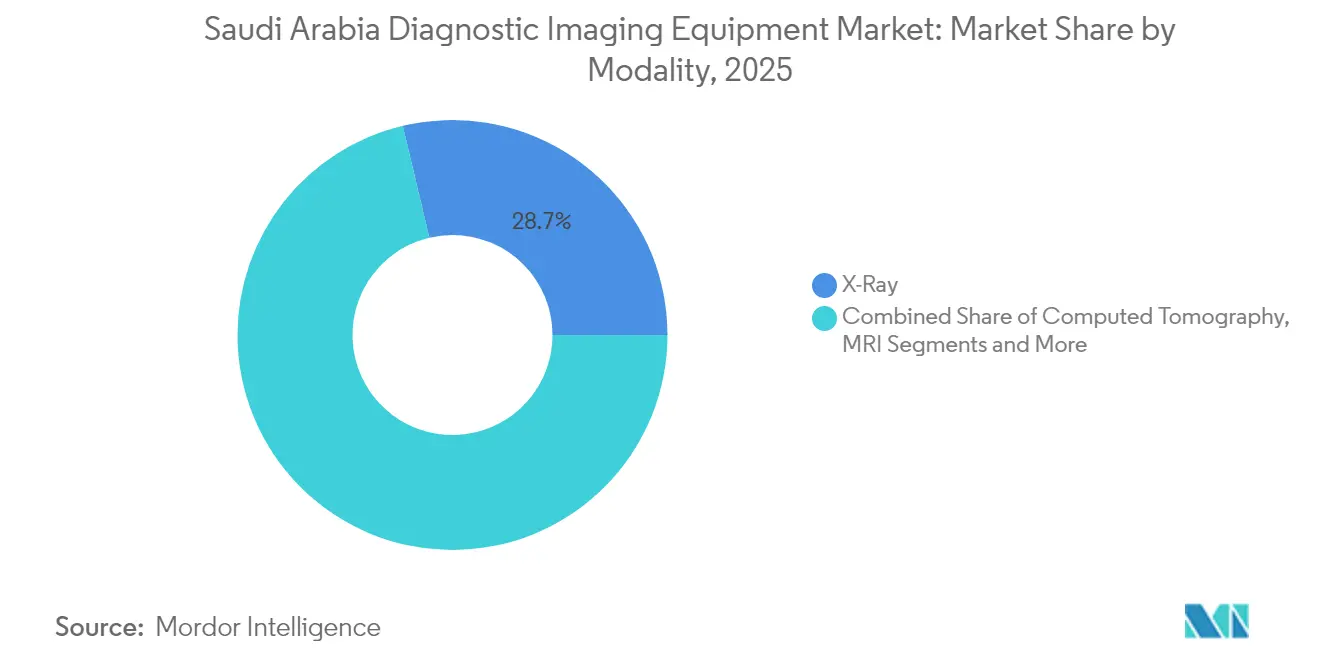

- By modality, X-Ray led with a 28.72% revenue share of the Saudi Arabia diagnostic imaging equipment market in 2025, whereas Ultrasound is forecast to post a 6.62% CAGR through 2031.

- By portability, fixed systems accounted for 80.22% of the Saudi Arabia diagnostic imaging equipment market size in 2025, while mobile and hand-held systems are projected to register a 6.18% CAGR over 2026-2031.

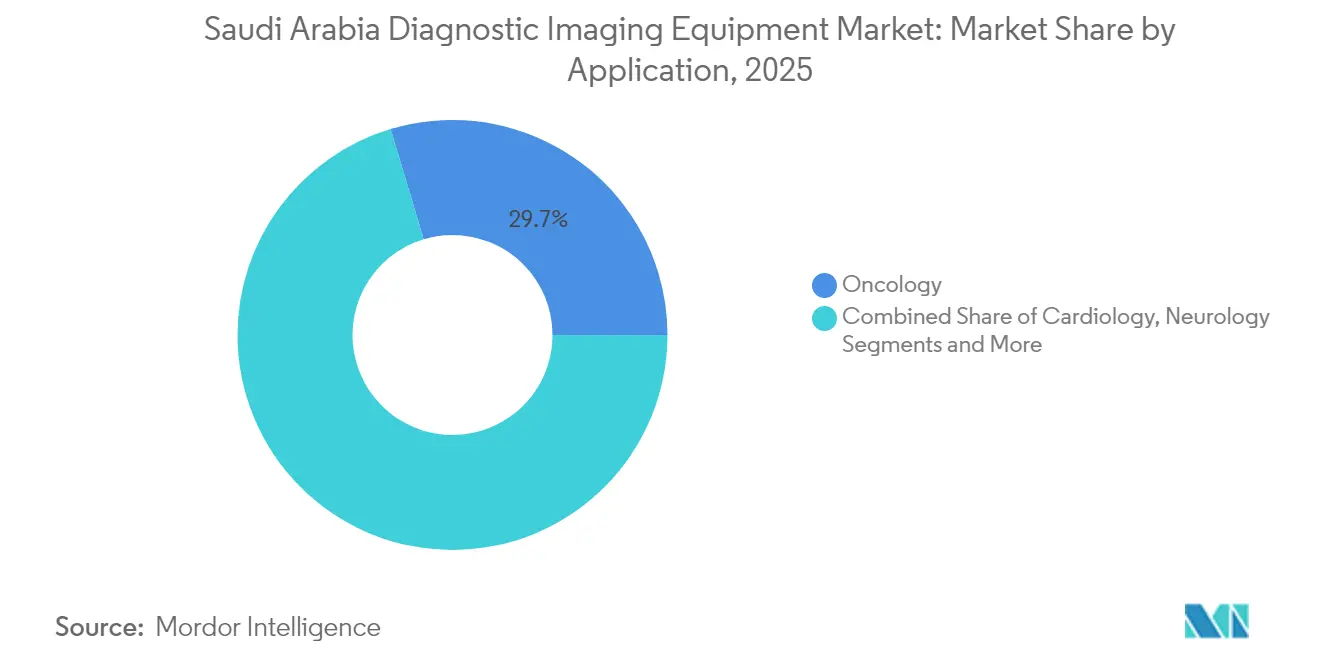

- By application, oncology captured 29.65% of the Saudi Arabia diagnostic imaging equipment market share in 2025, and cardiology is set to grow at a 5.96% CAGR to 2031.

- By end user, hospitals retained 64.30% of the Saudi Arabia diagnostic imaging equipment market in 2025, whereas diagnostic imaging centers are expected to expand at a 6.32% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Chronic Diseases | +1.2% | National, with concentration in urban centers | Long term (≥ 4 years) |

| Government Vision 2030 Healthcare Investment Surge | +1.8% | National, with priority in Riyadh, Eastern Province, Western Region | Medium term (2-4 years) |

| Increased Adoption of Advanced Imaging Technologies | +0.9% | National, led by major medical cities | Medium term (2-4 years) |

| Nationwide Image-Exchange Interoperability Projects | +0.6% | National, connecting 224+ hospitals | Short term (≤ 2 years) |

| Roll-Out of Private Health Insurance Boosting Scan Volumes | +0.7% | National, with higher impact in private sector facilities | Medium term (2-4 years) |

| AI-Powered Radiology Workflows Cutting Report Turnaround | +0.5% | Concentrated in tertiary care centers and smart hospitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Diseases

Cardiovascular disorders and diabetes affect nearly 70% of the Saudi population, driving persistent demand for cardiac CT, echocardiography, and liver ultrasound screenings that underpin long-run growth in the Saudi Arabia diagnostic imaging equipment market. Dedicated chronic-disease centers in Riyadh and Jeddah continuously acquire mid-tier CT scanners for rapid throughput, while AI protocols at King Faisal Specialist Hospital cut cardiac MRI turnaround by 33% and have been replicated at six tertiary facilities nationwide. Mobile X-ray fleets deployed under rural e-health programs extend preventative imaging to remote provinces, creating incremental scan volumes that flow back to central reading hubs. Demographic aging toward a projected 45 million residents by 2030 sustains volume growth across all modalities, reinforcing the modality-refresh cycle. Mandatory ISO 13485:2016 conformance pushes providers to standardize QC workflows as equipment fleets expand.

Government Vision 2030 Healthcare Investment Surge

A USD 66.6 billion public-health outlay in 2025 accelerates procurement pipelines for CT, MRI, and hybrid PET/CT systems, positioning the Saudi Arabia diagnostic imaging equipment market for mid-single-digit annual expansion.[2]Source: BioSpectrum Asia, “NEOM Is Fundamentally Reshaping Health by Placing a Strong Emphasis on Personalised Care,” biospectrumasia.com Privatization of 290 hospitals and 2,300 PHCs hands purchasing authority to new operators eager for AI-ready scanners, while NEOM’s USD 500 billion life-science district serves as a testbed for digital-twin diagnostic suites. Streamlined tenders led by NUPCO shave months from acquisition cycles, and bundled service contracts now cover training, cybersecurity, and dose‐optimization analytics, reducing total cost of ownership and speeding adoption.

Increased Adoption of Advanced Imaging Technologies

Twenty-plus AI applications built in-house at King Faisal Specialist Hospital have set a precedent for algorithm-enabled workflow efficiencies that rivals emulate, notably GE Healthcare’s AI-Sonic suite installed at Dr. Sulaiman Al-Habib’s new hospitals. Portable ultrasound and bedside MRI systems penetrate ICU and ED settings, shrinking time-to-diagnosis and freeing fixed suites for complex studies. The Saudi Data and AI Authority’s accreditation scheme for AI vendors enhances buyer confidence, and PACS-AI convergence supports on-the-fly triage in stroke and trauma units. As a result, AI-enhanced devices constitute a growing share of the Saudi Arabia diagnostic imaging equipment market, while legacy scanners undergo software retrofits rather than outright replacement, stretching capital budgets yet boosting productivity.

Nationwide Image-Exchange Interoperability Projects

The Seha Virtual Hospital links 224 institutions via a unified viewer that allows subspecialist radiologists in Riyadh to read rural scans within minutes, effectively expanding national diagnostic capacity without parallel workforce growth. Blockchain-secured routing ensures data sovereignty, meeting 2023 personal-data reforms. Early adopters report a 14% drop in ED length-of-stay and a 6% decline in repeat imaging, validating the economic case for further node expansion. Interoperability also facilitates large-scale annotated datasets that drive Saudi-specific AI model training, reinforcing a virtuous cycle of demand for cloud-native modalities and advanced analytics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Diagnostic Imaging Equipment | -0.8% | National, with higher impact on smaller private facilities | Medium term (2-4 years) |

| Shortage of Skilled Radiologists & Technicians | -1.1% | National, with acute shortages in rural areas | Long term (≥ 4 years) |

| Cyber-Security & Data-Sovereignty Concerns | -0.4% | National, with focus on cross-border data transfers | Short term (≤ 2 years) |

| Delay In Saudi-FDA Approvals for Novel Devices | -0.6% | National, affecting all new technology introductions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Diagnostic Imaging Equipment

A 3 Tesla MRI unit can exceed USD 3 million, while 128-slice CT systems hover near USD 2 million, expenditures that constrain capex-light providers and prolong ROI cycles within the Saudi Arabia diagnostic imaging equipment market. Service agreements add 8-12% annually to ownership costs, and local-content directives oblige OEMs to embed domestic supply percentages, nudging prices upward. Semiconductor shortages have lengthened lead times for detector arrays, delaying installation by up to six months for Tier-2 buyers. Consequently, mid-tier providers gravitate toward refurbished scanners and software upgrades, a tactic that tempers near-term market revenue yet fosters an aftermarket for maintenance and AI overlays.

Shortage of Skilled Radiologists & Technicians

Radiologist-to-population ratios trail OECD benchmarks, producing interpretation lags that bottle-neck modality utilization, especially during Hajj seasons when case volumes spike. Expat clinicians still comprise over 90% of advanced-imaging specialists, an imbalance that elevates turnover risk and salary inflation. Domestic training cohorts require 2-4 years to reach board eligibility, creating a skills gap that tele-interpretation and AI triage partially alleviate. Workforce shortages lower throughput and discourage smaller clinics from investing in high-end scanners, inhibiting the full revenue potential of the Saudi Arabia diagnostic imaging equipment market until talent pipelines mature.

Segment Analysis

By Modality: X-Ray Dominance Meets Ultrasound Innovation

X-Ray retained 28.72% of the Saudi Arabia diagnostic imaging equipment market share in 2025, anchored by trauma-care demand and universal availability in public and private EDs. Legacy DR rooms are undergoing flat-panel upgrades that boost throughput by 20%, while dose-tracking software supports pediatric safety compliance. Ultrasound, projected to grow at a 6.62% CAGR, benefits from handheld probes integrated with 5G tablets that enable point-of-care scans in ambulances and field clinics. Research-grade liver-ultrasound datasets assembled in Riyadh feed local AI liver-fat quantification tools, widening clinical use cases.

MRI expansion centers on 3 Tesla installations that elevate neuro-oncology diagnostics, whereas CT gains from ED triage protocols mandating whole-body trauma CT within 45 minutes. PET/CT volumes escalate in oncology centers that now manage 50,000 new cancer cases annually. Across modalities, AI decision-support layers produce time savings of 25-40 minutes per study, reinforcing the upgrade cycle in the Saudi Arabia diagnostic imaging equipment market.

Note: Segment shares of all individual segments available upon report purchase

By Portability: Fixed Systems Foundation Supports Mobile Innovation

Fixed Systems command an 80.22% market share in 2025, reflecting the substantial infrastructure investments in major medical cities and the technical requirements of high-end imaging modalities that require dedicated installation environments. The dominance of fixed systems aligns with the Kingdom's strategy of establishing centers of excellence within major hospitals, where advanced MRI, CT, and nuclear imaging systems provide comprehensive diagnostic capabilities for complex cases.

However, mobile and hand-held systems should clock a 6.18% CAGR as policy shifts push imaging toward community clinics. Bedside MRI and battery-powered X-ray carts cut ICU transport risks and free scanning slots for scheduled outpatients. The Healthcare Sandbox program expedites approvals for portable prototypes, shortening commercialization from 18 to 9 months. These mobility gains elevate scan penetration in Northern provinces, nudging total exam volumes and expanding the Saudi Arabia diagnostic imaging equipment market beyond metropolitan strongholds.

By Application: Oncology Leadership Yields to Cardiology Growth

Oncology represented 29.65% of 2025 revenue, reflecting multiphase CT, PET, and MRI follow-up protocols embedded in cancer pathways at five specialist centers. Adoption of radiomics-based tumor staging has raised per-patient imaging spend, driving sustained revenue. Cardiology, forecast at a 5.96% CAGR, accelerates as AI-echo quantification and CT-FFR tools gain reimbursement after positive health-technology assessments. Chronic-disease initiatives mandate biennial cardiac screenings for high-risk adults, elevating ultrasound and CT scan counts per capita.

Neurology remains a stable contributor, expanding with dedicated stroke units that demand 24/7 CT angiography. Orthopedics and emergency imaging services maintain incremental growth from sports-injury and road-traffic cases, collectively broadening the modality mix in the Saudi Arabia diagnostic imaging equipment market. The Saudi Food and Drug Authority's regulatory framework ensures that imaging applications across all medical specialties meet international safety and efficacy standards, with particular attention to radiation dose optimization and patient safety protocols.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Dominance Faces Imaging-Center Challenge

Hospitals commanded 64.30% of revenue in 2025, driven by public tertiary medical-city networks and large private groups that bundle imaging, surgery, and rehabilitation under one roof. These institutions negotiate multi-year managed-service contracts with OEMs, encompassing equipment, training, and AI analytics. Diagnostic imaging centers are poised for a 6.32% CAGR as insurance reforms promote outpatient diagnostics and entrepreneurs deploy niche services such as women-only imaging suites.

Almoosa Health’s IPO funds 700 new beds and a cluster of freestanding MRI-CT centers that target high-throughput screening demand. Specialty and day-surgery clinics adopt compact CT and O-arm systems for same-day procedures, broadening the Saudi Arabia diagnostic imaging equipment market penetration across care continuums. The Saudi Commission for Health Specialties' accreditation requirements ensure that all end-user facilities maintain appropriate professional standards and equipment quality, regardless of ownership structure or operational model.

Geography Analysis

Riyadh and the Central Region house most flagship hospitals, capturing the lion’s share of the Saudi Arabia diagnostic imaging equipment market. King Faisal Specialist Hospital’s smart-hospital model, integrating 20+ AI apps across radiology, sets the technology benchmark that neighboring facilities emulate. The Eastern Province logs the fastest revenue growth, propelled by Dallah Healthcare’s strategic acquisitions that double modality capacity in Dammam and Al-Ahsa. Strong petrochemical-industry health plans in Jubail further boost scan demand for occupational-medicine assessments.

The Western Region’s Makkah-Madinah corridor experiences seasonal spikes during Hajj and Umrah, where King Abdullah Medical City’s 1,550 beds deploy high-throughput CT angiography to manage cardiac emergencies among pilgrims. Scalable mobile imaging pods supplement fixed capacity during peak weeks, later redeployed to rural clinics post-season. NEOM’s northwest precinct emerges as a greenfield healthcare sandbox, ordering early-stage digital-twin scanners and augmented-reality visualization tools that will pilot next-generation imaging workflows.

Northern and Southern regions benefit from tele-imaging alliances that shuttle DICOM files over 5G backbones to Riyadh radiologists, reducing turnaround times from 60 hours to 12 hours in small provincial hospitals. Government subsidies offset installation costs for 16-slice CT units and portable ultrasound kits in these zones, ensuring equitable access and expanding the national footprint of the Saudi Arabia diagnostic imaging equipment market.

Competitive Landscape

TheSaudi Arabia diagnostic imaging equipment market is moderately fragmented, with GE Healthcare, Siemens Healthineers, and Philips controlling the premium-equipment tier through AI-ready scanner portfolios and end-to-end service ecosystems. GE Healthcare’s alliance with Dr. Sulaiman Al-Habib equips three new Hayat National Hospitals with MRI, CT, and ultrasound platforms bundled with predictive-maintenance analytics. Siemens Healthineers focuses on teleradiology orchestration and spectral CT, while Philips partners with NUPCO to embed cybersecurity-certified PACS in public sites.

Local players and fast-rising Chinese OEMs, notably United Imaging, leverage cost-advantaged PET/CT and whole-body MRI offerings to penetrate emerging hospital groups, gaining pilot orders at NEOM clinics and provincial MOH hospitals. PaxeraHealth, a U.S.-based cloud-PACS vendor, captures teleradiology share by optimizing Arabic-language reporting workflows, demonstrating the value of localization. Meanwhile, King Faisal Specialist Hospital’s in-house AI suite competes indirectly by offering home-grown algorithms for lung-nodule detection and breast-density scoring, underscoring the importance of software IP in market positioning.

New entrants face strict Saudi-FDA Class D requirements, yet the Healthcare Sandbox accelerates proof-of-concept deployments, as evidenced by Hyperfine’s bedside MRI pilots in Taif and Tabuk. Maintenance networks and post-market surveillance compliance increasingly differentiate vendors, given ISO 13485:2016 enforcement and the growing emphasis on device uptime. Overall, supplier rivalry intensifies around workflow-oriented value propositions rather than simple hardware specification, reshaping competitive dynamics in the Saudi Arabia diagnostic imaging equipment market.

Saudi Arabia Diagnostic Imaging Equipment Industry Leaders

Koninklijke Philips N.V.

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE HealthCare

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Saudi Development and Reconstruction Program for Yemen equips Marib General Hospital with the province’s first MRI scanner, expanding cross-border diagnostic capacity.

- October 2024: GE Healthcare partners with Hayat National Hospitals to furnish three facilities in Muhayl Aseer, Baysh, and Buraida with CT, MRI, and ultrasound lines, enhancing regional access.

- January 2024: GE Healthcare commits comprehensive imaging and patient-care solutions across all Dr. Sulaiman Al-Habib sites, cementing a multi-year managed-equipment contract.

Saudi Arabia Diagnostic Imaging Equipment Market Report Scope

As per the scope of this report, diagnostic imaging describes various techniques of viewing the inside of the body to help figure out the causes of an illness or injury and confirm a diagnosis. These systems are used to visualize the body to obtain a correct diagnosis and determine future care.

The Saudi Arabia diagnostic imaging equipment market is segmented by modality (MRI, computed tomography, ultrasound, X-ray, nuclear imaging, fluoroscopy, and mammography), applications (cardiology, oncology, neurology, orthopedics, gastroenterology, gynecology, and other applications), and end-user (hospital, diagnostic centers, and other end-users).

The report offers the value (in USD million) for the above segments.

By Modality

| MRI | Low-Field (< 1.5 T) |

| Standard (1.5–3 T) | |

| High-Field (3 T & above) | |

| Computed Tomography | ≤64-Slice CT |

| >64-Slice CT | |

| Ultrasound | Cart-based |

| Portable/Hand-held | |

| X-Ray | Analog |

| Digital | |

| Nuclear Imaging | PET |

| SPECT | |

| Other Modalities (Mammography, Fluoroscopy, etc.) |

By Portability

| Fixed Systems |

| Mobile and Hand-held Systems |

By Application

| Cardiology |

| Oncology |

| Neurology |

| Orthopedics |

| Gastroenterology |

| Gynecology & Obstetrics |

| Emergency Medicine |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Specialty & Day-Surgery Clinics |

| Other End Users |

| By Modality | MRI | Low-Field (< 1.5 T) |

| Standard (1.5–3 T) | ||

| High-Field (3 T & above) | ||

| Computed Tomography | ≤64-Slice CT | |

| >64-Slice CT | ||

| Ultrasound | Cart-based | |

| Portable/Hand-held | ||

| X-Ray | Analog | |

| Digital | ||

| Nuclear Imaging | PET | |

| SPECT | ||

| Other Modalities (Mammography, Fluoroscopy, etc.) | ||

| By Portability | Fixed Systems | |

| Mobile and Hand-held Systems | ||

| By Application | Cardiology | |

| Oncology | ||

| Neurology | ||

| Orthopedics | ||

| Gastroenterology | ||

| Gynecology & Obstetrics | ||

| Emergency Medicine | ||

| Other Applications | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Specialty & Day-Surgery Clinics | ||

| Other End Users | ||

Key Questions Answered in the Report

How large is the Saudi Arabia diagnostic imaging equipment market in 2026?

It stands at USD 439.97 million, with a forecast to reach USD 560.97 million by 2031 at a 4.98% CAGR.

Which imaging modality commands the highest share today?

X-Ray retains the lead with 28.72% of 2025 revenue.

What is the fastest-growing imaging application through 2031?

Cardiology is projected to advance at a 5.96% CAGR, buoyed by preventive cardiac-screening programs.

Why are mobile imaging systems gaining traction?

Portable units support rural outreach and point-of-care diagnostics, driving a 6.18% CAGR in the mobile-systems segment.

How does Vision 2030 influence equipment demand?

The plan's USD 66.6 billion health budget and hospital privatization push stimulate large-scale scanner procurement across public and private facilities.

What challenges limit near-term growth?

High equipment costs and a shortage of skilled radiologists reduce utilization and slow expansion despite strong demand drivers.

Page last updated on: