Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

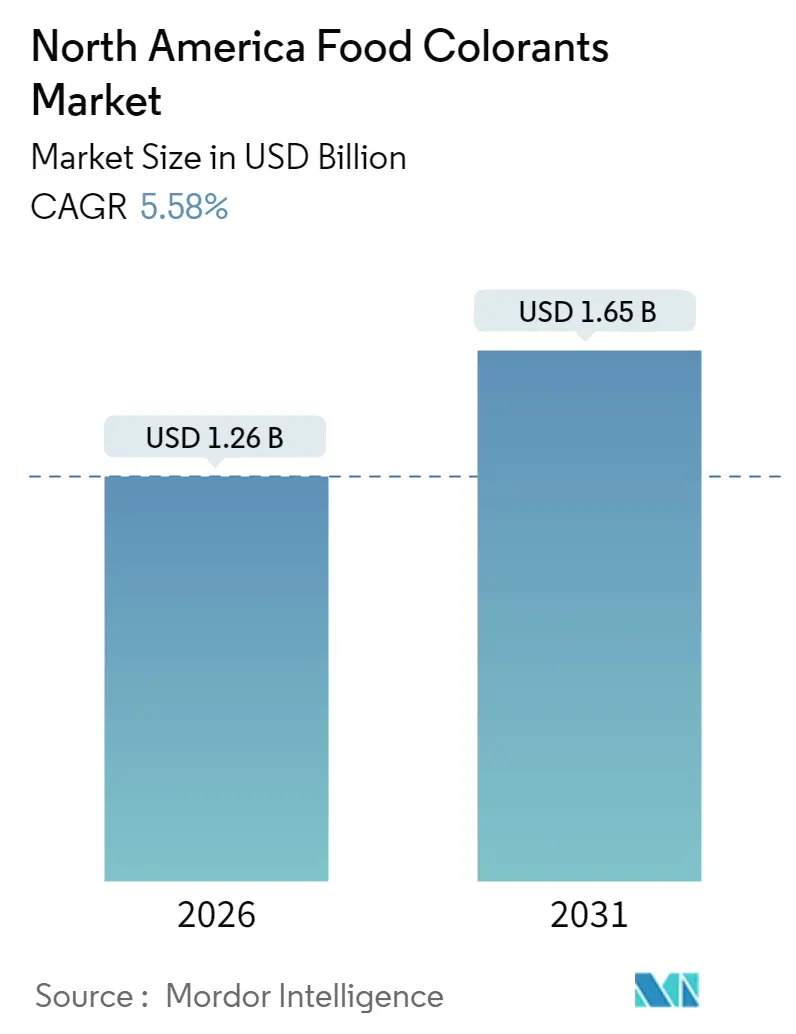

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Food Colorants Market Analysis by Mordor Intelligence

The North American food colorant market size was valued at USD 1.19 billion in 2025 and estimated to grow from USD 1.26 billion in 2026 to reach USD 1.65 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031). This growth is primarily attributed to the FDA's mandate to phase out petroleum-based synthetic dyes by December 2026, which has shifted natural colorants from a niche segment to mainstream adoption[1]Source: Food and Drug Administration, “FDA Announces Plan to End Use of Petroleum-Based Synthetic Food Dyes by 2026,” fda.gov. Natural solutions market share is expected to increase as manufacturers secure long-term supply contracts to support reformulation efforts. Innovation in the sector is accelerating, with developments such as heat-stable spirulina blues, corn-derived anthocyanins, and fermentation-based pigments addressing historical performance limitations. These advancements are enabling broader applications across baked snacks, dairy products, and shelf-stable beverages. In this evolving competitive landscape, vertically integrated suppliers with control over crop inputs or proprietary microbial strains are well-positioned to benefit. Their strategic advantage allows them to capitalize on the expected price stabilization during the phase-out of synthetic dyes.

Key Report Takeaway

- By product type, natural colors led with 55.98% of the North American food colorant market share in 2025, and grew at a CAGR of 6.68% forecast to 2031.

- By color, red pigments retained a 27.91% share of the North American food colorant market size in 2025, while blue registered the fastest 8.21% CAGR forecast to 2031.

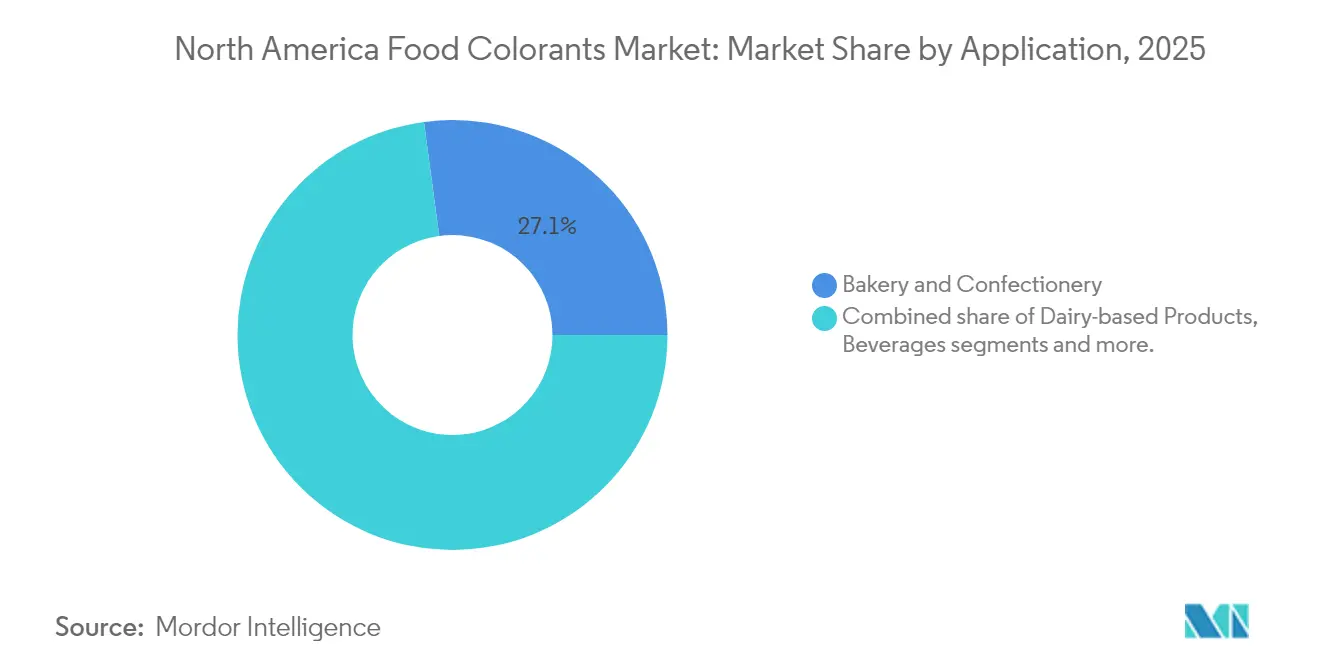

- By application, bakery and confectionery captured 27.12% of the North American food colorant market size in 2025; nutraceuticals are projected to grow at an 8.48% CAGR through 2031.

- By form, liquids accounted for 52.02% revenue share in 2025, with powders advancing at an 8.07% CAGR to 2031.

- By geography, United States captured 72.18% of the market value in 2025, and Mexico is expected to post a 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Food Colorants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed food industry driving market growth | +1.4% | United States, Mexico | Short term (≤ 2 years) |

| Increasing awareness of food aesthetics and appeal to boost the market | +1.2% | United States, Canada | Medium term (2-4 years) |

| Visual appeal of food products drives market growth | +0.8% | Region-wide | Medium term (2-4 years) |

| Regulatory shifts accelerating natural colorant adoption | +0.8% | Region-wide | Long term (≥ 4 years) |

| Rising demand for clean label products drives market growth | +0.8% | Region-wide | Short term (≤ 2 years) |

| Technological advancements in food colorant production boost market expansion | +0.6% | Region-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Processed Food Industry Driving Market Growth

The processed food sector in North America is experiencing significant growth, which serves as a major driver for the food colorant market. Manufacturers are increasingly recognizing the strategic importance of color in shaping consumer purchasing decisions. In 2024, ultra-processed foods accounted for a substantial share of the U.S. food supply. According to the International Food Information Council, nearly 79% of U.S. adults consider processed foods when making shopping decisions. This heightened focus on visual appeal is further amplified in the current social media-driven marketplace, where visually appealing food products gain a distinct competitive advantage in marketing. Leading companies, such as PepsiCo, are responding to this trend by reformulating their flagship products to incorporate natural colorants. For example, their Simply Ruffles Hot and Spicy chips now use tomato powder and red chile pepper as natural alternatives to synthetic red color, aligning with consumer preferences for cleaner and more natural ingredients.

Increasing Awareness of Food Aesthetics and Appeal to Boost the Market

Heightened consumer awareness of food aesthetics has elevated the role of color from a basic visual feature to a critical quality indicator, symbolizing freshness, flavor, and authenticity. In response to this evolving demand, manufacturers are increasingly prioritizing significant investments in premium-quality colorants to ensure their products exhibit consistent and visually appealing hues throughout their lifecycle. However, this trend is not limited to visual enhancement alone. Consumers are progressively favoring colorants derived from natural sources that also offer added nutritional benefits. For example, anthocyanins extracted from natural ingredients such as blueberries and purple carrots not only provide vibrant and attractive colors but also deliver antioxidant properties, aligning with the preferences of health-conscious consumers. This integration of aesthetic appeal and functional benefits is driving innovation in product development, with food manufacturers now adopting advanced colorant selection strategies that incorporate nutritional attributes alongside visual considerations.

Visual Appeal of Food Products Drives Market Growth

With the transformation of digital media in food marketing, the visual appeal of food products has become a crucial factor in gaining a competitive advantage. Companies are leveraging advanced colorant technologies to create distinctive and recognizable visual identities, thereby enhancing brand recognition and securing a strong position in premium market segments. Beyond mere aesthetics, the role of color extends to influencing consumer taste perceptions, making it a key element in the overall sensory experience. This connection between color and sensory appeal is driving significant advancements in the development of application-specific colorant formulations designed to retain their vibrancy and stability under a wide range of processing conditions. The market is also witnessing an increasing demand for customized color solutions tailored to meet the unique requirements of specific product categories. For example, companies such as Givaudan Sense Colour are at the forefront of innovation, developing natural colorants derived from sources like microalgae, anthocyanins, and beetroot. These solutions are engineered to deliver consistent and reliable performance, particularly in plant-based applications, where maintaining color integrity is critical.

Regulatory Shifts Accelerating Natural Colorant Adoption

Regulatory initiatives promoting transparency and clean labeling have significantly accelerated the adoption of natural colors in the food industry. With stricter requirements for ingredient sourcing disclosures, food manufacturers are transitioning from synthetic dyes to plant-derived, label-friendly alternatives such as beetroot red, turmeric, spirulina, and annatto. In January 2024, the FDA's ban on Red No. 3 marked a critical step toward removing synthetic dyes from the North American food supply. By April 2025, the FDA, in collaboration with Health and Human Services, announced plans to phase out all petroleum-based synthetic dyes by the end of 2026. These regulatory developments are creating substantial market opportunities for natural colorant alternatives. At the state level, California and West Virginia have implemented bans on several synthetic dyes in school cafeterias, setting a regulatory precedent that could extend to other institutional sectors. This evolving regulatory environment is fostering innovation in natural colorant technologies. For instance, in January 2024, Phytolon partnered with Ginkgo Bioworks to scale up the production of fermentation-derived colors, addressing potential supply challenges as market demand grows.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to food color to restrain the market | -06% | Region-wide | Medium term (2-4 years) |

| Strict FDA regulations impacting the sales of food colorant market | -0.8% | United States | Short term (≤ 2 years) |

| High production costs and limited availability of natural ingredients | -0.4% | Region-wide | Short term (≤ 2 years) |

| Stringent labeling requirements hamper the market | -0.5% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Related to Food Color to Restrain the Market

Health concerns associated with synthetic food colorants pose significant challenges to the market, as growing scientific evidence links these additives to negative health outcomes, particularly in children. A comprehensive review by the Office of Environmental Health Hazard Assessment of seven FDA-certified synthetic dyes identified potential neurobehavioral effects, further eroding consumer trust in artificial colorants[2]Source: Office of Environmental Health Hazard Assessment, “Synthetic Food Dye Risk Assessment,” oehha.ca.gov. Additionally, findings from the Environmental Working Group reveal that synthetic dyes are disproportionately used in products targeted at children, increasing scrutiny from parents and health-focused organizations. The market also faces obstacles due to the technical limitations of natural alternatives, which often require higher usage levels and specialized handling to deliver comparable visual performance. These limitations are especially evident in applications requiring heat stability or extended shelf life, restricting the adoption of natural ingredients despite growing consumer demand.

Strict FDA Regulations Impacting the Sales of Food Colorant Market

Manufacturers are encountering significant challenges due to the increasingly stringent regulatory frameworks for food colorants. The FDA's certification process for synthetic colors necessitates comprehensive safety evaluations and batch-specific testing, leading to higher compliance costs and altering market dynamics. Additionally, fragmented state-level regulations require national brands to implement region-specific formulation strategies, further complicating compliance efforts. This regulatory fragmentation disproportionately impacts smaller manufacturers with limited research and development resources, potentially curbing innovation within the market. Furthermore, the FDA's concurrent efforts to accelerate approvals for natural colorants while phasing out synthetic dyes create a timing gap that may cause temporary supply disruptions. As manufacturers reformulate products to meet compliance deadlines, these challenges could affect short-term market growth trajectories.

Segment Analysis

Product Type: Natural Colors Lead Market Transformation

Natural colors dominate the North American food colorant market with a 55.98% share in 2025 and are projected to grow at 6.68% CAGR from 2026-2031, substantially outpacing synthetic alternatives. This growth highlights a pivotal market shift driven by stricter regulatory frameworks and increasing consumer demand for clean-label ingredients. Technological advancements are rapidly overcoming historical performance challenges in the natural segment. For instance, in March 2024, Sensient Technologies introduced a heat-stable spirulina that retains vibrant blue hues even under processing conditions that previously degraded natural pigments.

Additionally, startups such as Phytolon and Michroma are leveraging fermentation technologies to develop fungal-derived pigments with superior stability and color intensity compared to traditional plant extracts. These innovations have the potential to close the performance gap with synthetic alternatives, transforming the economics of natural colorant production. Additionally, Consumers are increasingly opting for food products with natural coloring. The 2024 Food and Health Survey by the International Food Information Council revealed that 67% of consumers are willing to pay a premium for packaged products labeled as eco-friendly.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Color: Red Dominates While Blue Accelerates

Red colorants maintain market leadership with 27.91% share in 2025, driven by widespread application across confectionery, beverages, and processed foods, while blue colorants are emerging as the fastest-growing segment at 8.21% CAGR (2026-2031). The FDA's ban on Red No. 3 and upcoming restrictions on Red No. 40 are driving significant changes in the red segment, creating notable reformulation challenges for manufacturers. This regulatory shift is fostering innovation in natural red alternatives. For instance, Givaudan Sense Colour is leveraging its Amaize line to develop corn-derived anthocyanins that match the performance of synthetic options.

Simultaneously, the blue segment is witnessing swift expansion, propelled by innovations in spirulina-derived colorants. Additionally, cutting-edge technologies harnessing butterfly pea flower extract granted FDA approval in 2025 are broadening the horizons of the natural blue color palette. Moreover, breakthroughs in extraction and processing techniques are bolstering this growth by enhancing the quality, stability, and cost-effectiveness of natural blue colorants.

Application: Bakery and Confectionery Leads While Nutraceuticals Surge

Bakery and confectionery applications lead the North American food colorant market with 27.12% share in 2025, while nutraceuticals emerge as the fastest-growing segment at 8.48% CAGR (2026-2031). The bakery segment's market leadership highlights the critical importance of color in visually driven categories, where product appearance heavily influences consumer perceptions of quality and freshness. However, the shift toward natural alternatives presents technical challenges, particularly in achieving heat stability during baking processes. Statistics Canada reported that Canada's bakery and tortilla manufacturing industry generated a monthly gross domestic product of CAD 4,501 million in 2023.

The nutraceutical segment's rapid growth is fueled by the dual functionality of natural colorants, which enhance visual appeal while offering potential health benefits through bioactive compounds such as anthocyanins and carotenoids. This alignment with the nutraceutical value proposition drives innovation, as colorants contribute to both product aesthetics and nutritional value. As ongoing research continues to validate the health benefits of natural pigments, this trend is expected to gain further momentum.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Form: Liquid Dominates While Powder Gains Momentum

Liquid colorants maintain market leadership with 52.02% share in 2025, valued for their ease of incorporation and consistent performance across diverse applications, while powder formats are growing at an accelerated 8.07% CAGR (2026-2031). The liquid segment's leadership is driven by its superior dispersion capabilities, ensuring consistent coloration, particularly in critical sectors like beverages and dairy, where uniformity is essential. Liquid colourants disperse more evenly and quickly in both water-based and some oil-based systems, ensuring consistent colour throughout the product.

Conversely, the growth of the powder segment is propelled by advancements in microencapsulation technologies, which improve stability, extend shelf life, and simplify handling processes for manufacturers. These innovative powder formulations deliver logistical benefits, including lower shipping costs, extended product longevity, and easier storage. Furthermore, the segment is gaining traction through the development of specialized powder systems tailored for complex applications, such as fat-based products, where liquid colorants face dispersion challenges. This expansion is unlocking new market opportunities for powder formats in previously constrained areas.

Geography Analysis

The United States dominates the North American food colorant market, accounting for the largest regional share at 72.18% in 2025, while demonstrating a strategic pivot toward natural alternatives driven by regulatory developments and consumer preferences. The FDA's directive to phase out petroleum-based synthetic dyes by 2026 has accelerated this transition, reshaping the U.S. market landscape. State-level actions, such as bans on synthetic dyes in school cafeterias in California and West Virginia, are setting precedents that could extend to other institutional settings. Companies like California Natural Color are investing in expanding domestic production capacity for natural colorants to address potential supply shortages as synthetic options are phased out. Regional innovation clusters, particularly in California and the Midwest, are capitalizing on their proximity to agricultural inputs to develop vertically integrated production models for plant-based colorants.

Canada presents a distinct market dynamic within North America, characterized by a well-established regulatory framework and early adoption of natural alternatives. Health Canada's List of Permitted Food Colours has historically enforced stricter standards compared to U.S. regulations, positioning the Canadian market as a leader in natural colorant adoption. This regulatory advantage has enabled Canada to serve as a testing ground for natural colorant innovations, allowing manufacturers to validate product performance and consumer acceptance before broader North American rollouts. Additionally, Canada’s robust agricultural sector supports domestic production of plant-based colorants, with emerging vertical integration between agricultural producers and manufacturers enhancing supply chain efficiency and market competitiveness.

Mexico demonstrates the highest growth potential in the North American food colorant market growing at a CAGR of 6.32% through 2031, driven by the rapid expansion of its processed food sector and increasing export alignment with U.S. and Canadian markets. Mexican food manufacturers are proactively adopting natural colorants to align with North American regulatory trends and maintain market access as synthetic restrictions tighten. The country’s rich agricultural biodiversity offers opportunities to develop unique natural colorants from indigenous plant sources, enabling differentiated product offerings in the broader North American market. Significant investments in production facilities for natural colorants are underway, leveraging Mexico’s lower manufacturing costs and proximity to agricultural inputs to establish competitive advantages. This strategic positioning is particularly critical as supply constraints for natural alternatives are expected following the FDA’s synthetic dye phase-out, positioning Mexico as a key supplier for the North American market during this transition.

Competitive Landscape

The North American food colorant market demonstrates moderate fragmentation, with key players such as Sensient Technologies Corporation, Oterra A/S, Archer Daniels Midland Company, and Givaudan SA competing alongside specialized natural colorant producers and emerging biotechnology firms. Regulatory changes are driving a shift from synthetic to natural colorants, presenting strategic growth opportunities for companies with advanced natural formulation expertise. The market is also experiencing consolidation as major players acquire niche natural colorant manufacturers to diversify their product portfolios. Additionally, significant opportunities exist in developing tailored natural colorant solutions for specific applications, particularly in challenging segments like baked goods and shelf-stable beverages, where synthetic options have traditionally been preferred due to their superior stability and performance characteristics.

Emerging players are increasingly adopting precision fermentation techniques to manufacture pigments, effectively reducing their reliance on traditional crop cycles and mitigating the risks associated with agricultural volatility. This innovative approach enables year-round production, ensuring a consistent supply of pigments regardless of external agricultural factors. Biotech entrants are strategically strengthening their foothold in the market by licensing microbial strains to contract manufacturers. This strategy allows them to accelerate their path to commercialization while avoiding the substantial capital expenditures typically required for building and operating extraction facilities.

Strategic acquisitions remain a key driver in refining and diversifying industry portfolios. In response to growing retailer demands for greater transparency in product sourcing, several suppliers have implemented blockchain-enabled traceability solutions. These technologies provide end-to-end visibility, allowing pigments to be tracked seamlessly from their origin, whether derived from farms or fermentation processes, to the final product. Collectively, these advancements signify a transformative shift in the competitive landscape, where success increasingly depends on a comprehensive offering that integrates resilient supply chains, state-of-the-art stabilization technologies, and verifiable sustainability credentials.

North America Food Colorants Industry Leaders

Sensient Technologies Corporation

Oterra A/S

Archer Daniels Midland Company

Givaudan SA

Dohler Group SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: ADM introduced a new blue colorant, sourced from the huito fruit, boasting enhanced stability across various pH levels. This move fills a notable void in the market for natural colorants.

- October 2024: California Natural Color unveiled its expanded portfolio of natural colorants for food, beverages, and supplements at SupplySide West 2024, highlighting the increasing market demand for natural alternatives.

- September 2024: Givaudan Sense Colour has launched its Amaize line of corn-derived anthocyanins, offering a natural alternative to Red 40 to address regulatory changes and evolving consumer demands.

- December 2023: Archer Daniels Midland Company acquired Revela Foods, a Wisconsin-based developer and manufacturer of innovative food ingredients and solutions. The purpose of this acquisition was to expand the company’s product portfolio.

North America Food Colorants Market Report Scope

Food colorants, commonly referred to as food colors or color additives, are substances infused into food to enhance its color. The North American food colorant market is segmented into product type, color, application, form, and country. Based on product type, the market is segmented into natural color and synthetic color. Based on color, the market is segmented into blue, red, green, yellow, and others. Based on the application, the market is segmented into bakery and confectionery, dairy dairy-based products. beverages, nutraceuticals, snacks & cereals, other applications. The beverages segment is further segmented into alcoholic beverages and non-alcoholic beverages. Based on form, the market is segmented into powder and liquid. Based on countries, the market is segmented into the United States, Canada, Mexico, and the rest of North America. The market sizing has been done in USD value terms for all the abovementioned segments.

By Product Type

| Natural Color |

| Synthetic Color |

By Color

| Blue |

| Red |

| Green |

| Yellow |

| Others |

By Application

| Bakery and Confectionery | |

| Dairy-based Products | |

| Beverages | Alcoholic Beverages |

| Non-alcoholic Beverages | |

| Nutraceuticals | |

| Snacks and Cereals | |

| Other Applications |

By Form

| Powder |

| Liquid |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Natural Color | |

| Synthetic Color | ||

| By Color | Blue | |

| Red | ||

| Green | ||

| Yellow | ||

| Others | ||

| By Application | Bakery and Confectionery | |

| Dairy-based Products | ||

| Beverages | Alcoholic Beverages | |

| Non-alcoholic Beverages | ||

| Nutraceuticals | ||

| Snacks and Cereals | ||

| Other Applications | ||

| By Form | Powder | |

| Liquid | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the North American food colorant market size today and in 2031?

The market stands at USD 1.26 billion in 2026 and is forecast to reach USD 1.65 billion by 2031.

Why are natural pigments gaining North American food colorant market share?

Regulatory bans on synthetic dyes, clean-label consumer demand, and technological advances that improve natural pigment stability are driving adoption.

Which application segment will grow fastest through 2031?

Nutraceutical products, owing to pigments’ dual visual and antioxidant benefits, are projected to grow at an 8.48% CAGR.

What regulatory deadlines should manufacturers note?

All petroleum-based synthetic dyes must exit the U.S. food supply by 31 Dec 2026 under the FDA phase-out plan.