Market Overview

| Study Period | 2021 - 2031 |

|---|---|

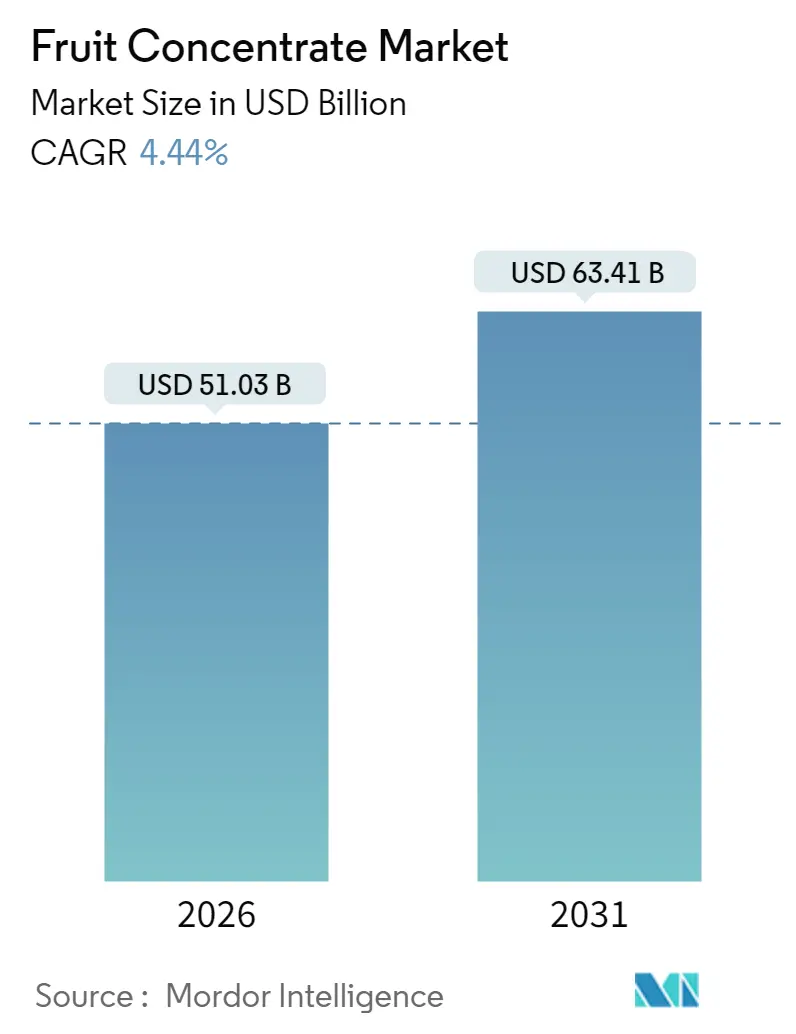

| Market Size (2026) | USD 51.03 Billion |

| Market Size (2031) | USD 63.41 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruit Concentrate Market Analysis by Mordor Intelligence

Fruit concentrates market size in 2026 is estimated at $51.03 billion, growing from 2025 value of $48.86 billion with 2031 projections showing USD 63.41 billion, growing at 4.44% CAGR over 2026-2031. This steady climb reflects a decisive shift from commodity juice bases toward premium functional ingredients, encouraged by the U.S. FDA’s updated “healthy” definition that took effect in February 2025 and tightened limits on added sugars. Heightened consumer preference for natural components, wider adoption of low-energy membrane and freeze-concentration technologies, and greater interest in immunity-supporting beverages are giving processors new revenue streams and higher margins. Meanwhile, supply-chain volatility—exemplified by Brazil’s 27.4% drop in 2024/25 orange output—has amplified the value of geographic diversification and shelf-stable formats, according to the CEPEA - Center for Advanced Studies on Applied Economics[1]Source: CEPEA, "Orange supply may continue below demand in the 2025/26 season", cepea.org.br. Across categories, the fruit concentrates market is transforming from volume-led trading into a platform for clean-label, nutritional, and sustainability solutions.

Key Report Takeaways

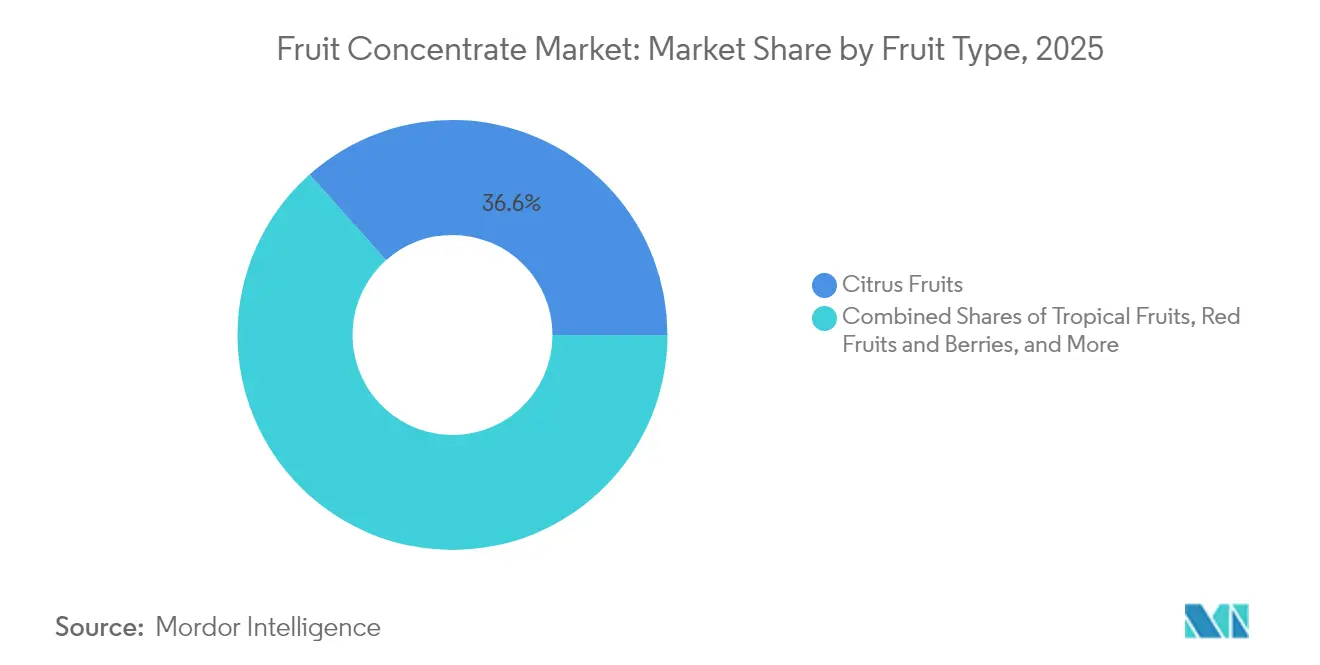

- By fruit type, citrus fruits held 36.58% of the 2025 fruit concentrates market share and tropical fruits are projected to accelerate at a 5.86% CAGR through 2031.

- By product form, liquid concentrates commanded 57.65% 2025 of the market share, whereas powder concentrates are forecast to register a 5.12% CAGR between 2026-2031.

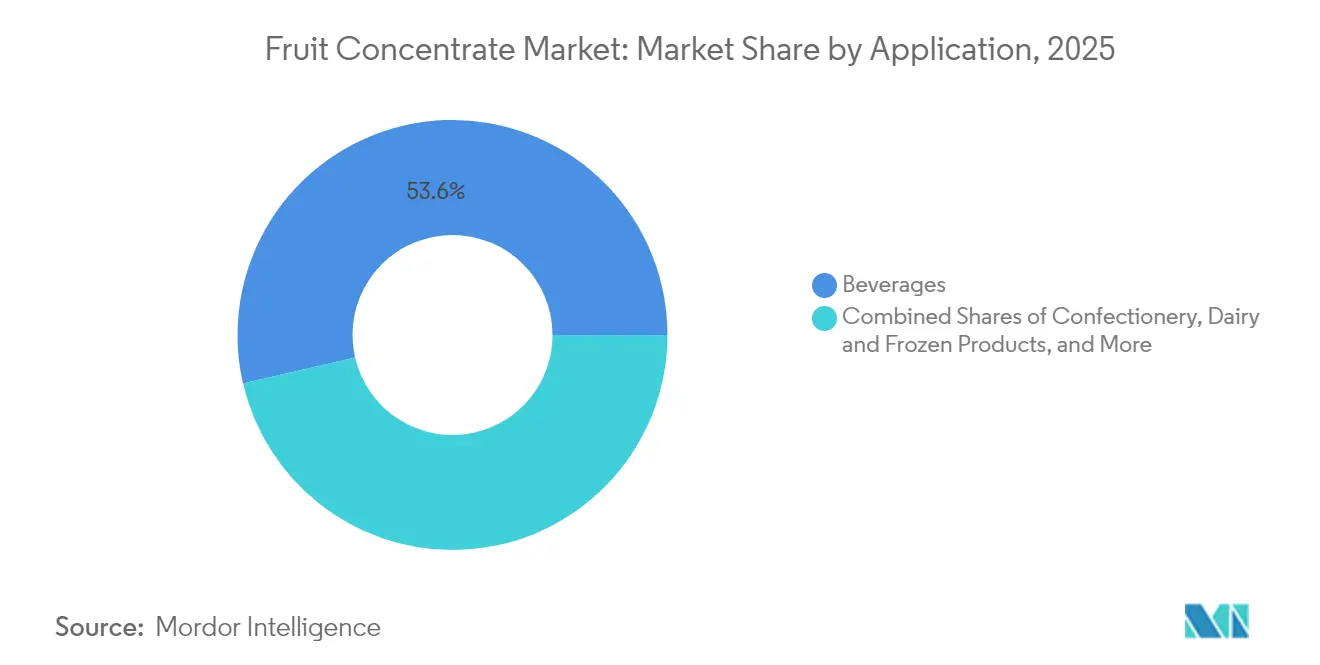

- By application, beverages captured 53.62% of shares in 2025, while dairy and frozen products are poised for the fastest growth at a 5.44% CAGR to 2031.

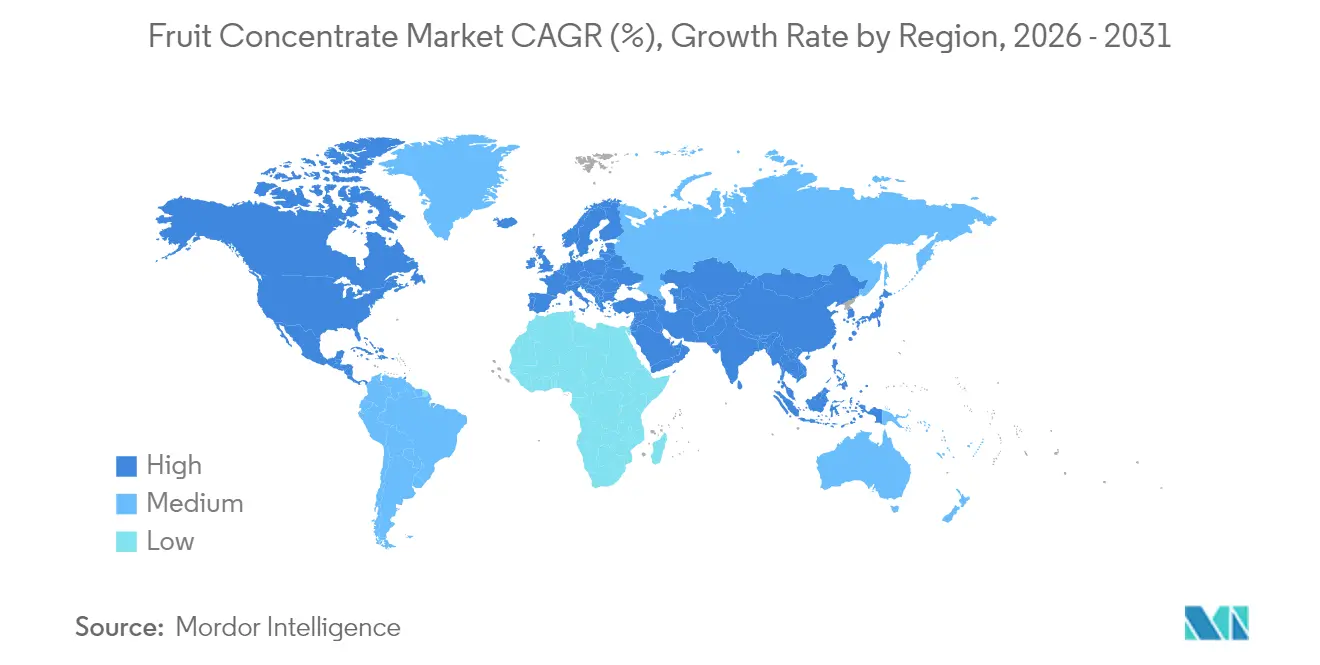

- By geography, North America led with a 31.08% share in 2025, yet Asia Pacific is expected to post a 6.18% CAGR, powered by Chinese and Southeast Asian processing investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fruit Concentrate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural Ingredients | +1.2% | Global, with premium positioning in North America & EU | Medium term (2-4 years) |

| Growth in Functional Beverages | +1.0% | North America & Asia Pacific core, spill-over to EU | Short term (≤ 2 years) |

| Technological Advancements in Production and Processing | +0.8% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Health-driven Sugar-replacement Adoption | +0.9% | North America & EU regulatory-driven, expanding to APAC | Medium term (2-4 years) |

| Rising Growth in Emerging Markets | +0.6% | Asia Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Stable Shelf Life, Driving the Demand | +0.4% | Global supply chain optimization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Ingredients

Kerry's 2025 research reveals that 86% of consumers are ready to pay a premium for functional benefits, underscoring a major shift in fruit concentrate specifications driven by the demand for clean-label products. This trend extends beyond traditional applications, as food manufacturers increasingly replace artificial flavors with fruit concentrates to meet transparency expectations. The California Food Safety Act has further accelerated this transition, prompting many brands to rely solely on natural colors and flavors, thereby driving sustained demand for fruit-based alternatives. Advanced stabilization techniques are improving the performance of natural colors, making fruit concentrates a practical option in applications previously dominated by synthetic alternatives. This change reflects a permanent evolution in the market rather than a temporary trend, as regulatory frameworks continue to favor natural ingredient solutions.

Growth in Functional Beverages

Fruit concentrates are increasingly vital in immunity-boosting formulations, with 51% of consumers focusing on skin support and 44% prioritizing immune benefits in their beverage preferences. The growing popularity of adaptogenic beverages, which combine fruit concentrates with botanical extracts, reflects a shift from traditional juice applications to pharmaceutical-grade functionality. Companies, such as Kerry with its Tastesense technology, are creating specialized concentrate blends that provide specific health benefits while preserving taste, achieving sugar reduction without compromising flavor. To meet the rising demand for low-sugar and gut-health beverages, the industry is utilizing fruit pomace and fiber-rich concentrates. This trend is evident in the increasing number of prebiotic and probiotic drink launches anticipated in 2025. Consequently, the role of fruit concentrates is transforming, moving from basic commodity sweeteners to premium, value-added ingredients.

Technological Advancements in Production and Processing

Innovations in processing technology have emerged as a pivotal differentiator. Membrane distillation and freeze concentration technologies now cut energy consumption by over 60% compared to traditional evaporation methods, all while maintaining organoleptic and nutritional quality, as highlighted by ScienceDirect. Major producers are channeling investments into 3D-printed membranes, enabling the selective extraction of polyphenols and bioactives, thereby amplifying the functional value of their concentrates. This technological evolution isn't confined to industry giants; regional players across Asia and Latin America are embracing modular, energy-efficient equipment, balancing both cost and sustainability. These advancements are closely tied to the industry's push to comply with evolving regulatory standards on quality and labeling, particularly as the FDA and USDA refine their specifications for fruit juice concentrates, as highlighted by Food Compliance International[2]Source: Food Compliance International, "USDA updates specifications for frozen fruit juices", foodcomplianceinternational.com.

Health-driven Sugar-replacement Adoption

Stevia and monk fruit, now approved for use in the UK and EU, have become pivotal in enabling manufacturers to develop zero-calorie beverages with improved taste profiles. The growing demand for natural sweeteners is further fueled by updated FDA guidelines that impose stricter limits on added sugars in foods labeled as "healthy." This regulatory shift is compelling brands to reformulate their products using fruit-based concentrates and innovative sweetener blends. Additionally, this trend is gaining momentum in regions like Southeast Asia and Latin America, where companies such as BlueTree are actively scaling their patented sugar reduction technologies to cater to both local consumers and export markets, thereby addressing the global demand for healthier beverage options.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw Material Prices | -1.3% | Brazil, U.S., EU, China | Short term (≤ 2 years) |

| Stringent Government Regulations | -0.7% | North America, EU, China | Medium term (2-4 years) |

| Seasonality and Supply Chain Issues | -0.6% | Global, with acute impact in Brazil, Southeast Asia | Short term (≤ 2 years) |

| Adoption of Alternative Sweeteners and Ingredient Innovations | -0.5% | North America, EU, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw Material Prices

Raw material price volatility poses a consistent challenge, especially for citrus and tropical fruits. In 2025, weather-induced production declines led to record-high Brazilian orange prices. Simultaneously, European buyers sought reduced contract prices in light of a proposed 50% U.S. tariff on imports. Such disruptions resulted in Brazil's juice stocks hitting zero and a 20% reduction in Florida's orange crop. Additionally, import-export of raw material plays a significant role. According to the Observatory of Economic Complexity data from 2024, Canada imported USD 966 million worth of tropical fruits[3]Source: The Observatory of Economic Complexity, "Tropical Fruits in Canada Trade", oec.world. This underscores the urgency for diversified sourcing and adaptable procurement strategies, as highlighted by the Center for Advanced Studies on Applied Economics. In response, companies are channeling investments into contract farming and regenerative agriculture, aiming to bolster traceability and supply resilience. Additionally, businesses are exploring advanced technologies, such as precision agriculture and blockchain, to enhance supply chain transparency and mitigate risks associated with price fluctuations. These measures are expected to play a crucial role in ensuring long-term sustainability and stability in the citrus and tropical fruit markets.

Stringent Government Regulations

Major markets are grappling with rising compliance costs and complexities due to evolving regulatory frameworks. The FDA's 2025 update to the definition of "healthy" food labeling imposes restrictions on added sugars and saturated fats. This compels brands to pivot towards fruit-based ingredients and natural sweeteners in their reformulations to meet the updated criteria. Concurrently, the USDA has tightened quality and documentation requirements with its revised standards for frozen fruit juices, emphasizing stricter adherence to product specifications and traceability. Meanwhile, the EU is intensifying its focus on sustainability and clean label claims, pushing companies to adopt environmentally friendly practices and transparent ingredient sourcing. These regulatory shifts are driving brands to bolster their analytical capabilities, invest in advanced testing technologies, and enhance supply chain transparency to ensure compliance and maintain access to the market.

Segment Analysis

By Fruit Type: Citrus Leads, Tropical Gains

In 2025, citrus fruits commanded a dominant 36.58% share of the market, underscoring their pivotal role in beverage and food processing. Their widespread use in juices, flavoring agents, and processed foods highlights their entrenched position in the industry. Yet, tropical fruits are surging ahead, boasting a 5.86% CAGR through 2031, fueled by a growing consumer appetite for exotic flavors and bolstered supply chains in Southeast Asia and Latin America. The increasing availability of tropical fruits, such as mangoes, pineapples, and papayas, in processed forms like purees and frozen products is further driving their growth. While red berries and fruits occupy a smaller volume, their rising prominence in functional and premium products caters to the health-conscious demographic. These fruits, including strawberries, raspberries, and blueberries, are increasingly incorporated into products marketed for their antioxidant and nutritional benefits.

The "others" category, encompassing apples, pears, and stone fruits, is reaping rewards from contract farming advancements and sustainability drives, especially in organic and traceable sourcing. These initiatives are enhancing consumer trust and meeting the growing demand for ethically sourced produce. Furthermore, the FDA and USDA's regulatory oversight, particularly concerning juice content and labeling, plays a pivotal role in shaping fruit selection and product positioning. Compliance with these regulations ensures transparency and influences consumer purchasing decisions, further impacting market dynamics.

Note: Segment shares of all individual segments available upon report purchase

By Product Form: Liquid Concentrates Lead, While Powder Concentrates Gain Momentum

In 2025, liquid concentrates commanded a dominant 57.65% market share, bolstered by their adaptability in beverage production and a well-established distribution network. Their versatility allows manufacturers to cater to a wide range of beverage applications, from carbonated drinks to functional beverages, making them a preferred choice across various industries. Meanwhile, powder concentrates emerged as the fastest-growing segment, boasting a 5.12% CAGR. This surge is driven by manufacturers' preference for shelf-stable, lightweight formats, ideal for export and e-commerce channels. Powder concentrates are particularly advantageous for reducing transportation costs and extending shelf life, which are critical factors in global trade. Furthermore, innovations like freeze concentration and membrane filtration are paving the way for high-quality powder concentrates, ensuring flavor and nutritional integrity—crucial for brands focusing on functional beverages. These technologies are enabling manufacturers to meet consumer demand for healthier and more natural products without compromising on taste or quality.

Additionally, the "others" category, encompassing purees and specialty formats, is carving out niche roles in bakery and confectionery. This growth is bolstered by advancements in ingredient blending and a push for clean label formulations. Purees, for instance, are gaining traction in premium bakery products, while specialty formats are being utilized in artisanal confectionery to enhance flavor profiles. To uphold quality and safety standards for end users, product form regulations adhere to guidelines set by 21 CFR Part 146 and its associated standards. These regulations ensure that all product forms meet stringent safety and quality benchmarks, fostering consumer trust and compliance within the industry.

By Application: Beverages Dominate the Market, While Dairy & Frozen Products are Growing

In 2025, beverages dominated the market, claiming a substantial 53.62% share. This underscores the pivotal role of fruit concentrates in crafting juices, soft drinks, and even alcoholic beverages. Fruit concentrates are widely used in these beverages to enhance flavor, provide natural sweetness, and improve shelf life, making them a cornerstone of the segment. Meanwhile, the dairy and frozen products segment emerged as the fastest-growing application, boasting a 5.44% CAGR. Here, fruit concentrates are being harnessed for flavoring, coloring, and boosting nutritional value in items like yogurts, ice creams, and their plant-based counterparts. The growing consumer preference for healthier and more natural ingredients is driving this trend, with manufacturers increasingly incorporating fruit concentrates to meet these demands.

Additionally, the confectionery sector, encompassing candies, gummies, and fruit bars, is turning to fruit pomace and fiber-rich concentrates. This shift is driven by a push to satisfy clean label standards and the demand for functional ingredients. The use of fruit concentrates in confectionery not only enhances taste and texture but also aligns with the rising trend of offering products with added health benefits. Furthermore, regulatory measures, such as 21 CFR 101.30, which governs juice content declarations, play a crucial role in ensuring transparency and fostering consumer trust across these applications. These regulations help maintain product integrity and ensure that consumers are well-informed about the content of the products they purchase.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2025, North America commanded a dominant 31.08% market share, bolstered by its established processing infrastructure, clear regulations, and a robust consumer appetite for functional and clean-label beverages. However, the region's strong supply chain grapples with climate-induced challenges, especially in citrus and cherry production, highlighting the urgent need for investments in diverse sourcing and cutting-edge processing technologies.

Asia Pacific is poised to be the fastest-growing region, projecting a 6.18% CAGR from 2026 to 2031. This growth is driven by a burgeoning middle class, heightened investments in processing capabilities, and the rise of both local and regional brands. China's expansion in citrus production, coupled with Vietnam's embrace of advanced IQF processing, underscores the region's commitment to both volume and quality. Meanwhile, India and Indonesia are making strides with new processing plants and contract farming initiatives, ensuring a steady raw material supply for domestic needs and export opportunities.

Europe's market is navigating a stringent regulatory landscape and an increasing focus on sustainability. The 2023/2024 season saw the European Union's citrus production grappling with challenges posed by droughts and elevated temperatures. Yet, Europe stands at the forefront of clean label and organic certifications, driven by a robust consumer push for ingredient transparency and environmental stewardship. South America and Africa are carving out their niches as pivotal suppliers of tropical and citrus concentrates. Brazil and Ghana, capitalizing on their cost advantages and closeness to major import markets, are leading the charge. Yet, these regions aren't without challenges; they contend with significant supply chain vulnerabilities stemming from weather fluctuations and tariff shifts. In response, there's a noticeable pivot towards bolstering local processing and export infrastructures.

Competitive Landscape

The global fruit concentrate market is highly competitive due to several local and international players. New product launches, partnerships, expansions, and acquisitions are the major global strategies adopted by the leading companies in the fruit concentrate market. Some major global fruit concentrate market players are Döhler, Ingredion Inc., Kerry Inc., and Archer Daniels Midland Company. The fruit concentrates market remains highly fragmented, reflecting a proliferation of regional players and a few global leaders.

Strategic patterns are shifting toward vertical integration and sustainability, as companies seek to secure raw material supply and differentiate through regenerative agriculture and contract farming. Technology adoption, particularly in membrane filtration and freeze concentration, is enabling smaller players to compete on quality and shelf-life, narrowing the gap with incumbents. White-space opportunities are emerging in functional and clean label applications, particularly as regulatory changes favor natural and health-promoting ingredients.

Disruptors are leveraging proprietary technologies for sugar reduction and fiber enrichment, as seen in BlueTree’s patented process and Kerry’s Tastesense platform. Regulatory influence is most pronounced in the U.S. and EU, where compliance with FDA and EFSA standards is both a barrier and a catalyst for innovation. A notable example is ADM’s “re:generations” initiative, which aims to enroll four million acres in regenerative agriculture by 2025, directly linking sustainability commitments to supply chain resilience and market positioning. This strategic alignment of environmental and business objectives is becoming a defining feature of competitive advantage in the sector.

Fruit Concentrate Industry Leaders

-

Ingredion Inc.

-

Kerry Inc.

-

Archer Daniels Midland Company

-

Döhler GmbH

-

SunOpta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2023: iTi Tropicals formulated both a puree and a concentrate from acerola fruit, also known as the Barbados cherry or West-Indian cherry. This product innovation was highlighted for its high vitamin C content and its ability to replace added ascorbic or citric acid, reduce pH, potentially extend shelf life, and impart a tart flavor. The acerola puree and concentrate were introduced for use in a wide range of applications, including jams, jellies, health shots, smoothies, juice blends, gummies, fruit snacks, fruit leathers, sorbets, frozen novelties, sauces, marinades, and dressings.

- October 2023: Okanagan Specialty Fruits opened a new apple processing facility on a 42.5-acre site in Moses Lake, Washington. The plant was built to process, slice, and pack the company’s Arctic apple products and is located near their orchards to enhance operational efficiency, quality, and minimize transportation.

Global Fruit Concentrate Market Report Scope

Fruit concentrate is a fruit with the water removed. Fruit concentrates are made by washing, scrubbing, and crushing the fruit into a pulp. The global fruit concentrate market is segmented into fruit type, product form, application, and geography. The fruits segment of the market includes citrus fruits, red fruits and berries, tropical fruits, and others. By product form, the market is segmented into liquid, powder, and others. The market is segmented by beverage, bakery, confectionery, dairy, and others. Further, the study covers the regional analysis of North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

By Fruit Type

| Citrus Fruits |

| Red Fruits & Berries |

| Tropical Fruits |

| Others |

By Product Form

| Liquid Concentrate |

| Powder Concentrate |

| Others |

By Application

| Beverages | Fruit Juices and Drinks |

| Soft Drinks and Carbonated Beverages | |

| Alcoholic Beverages | |

| Bread and Bakery Products | |

| Confectionery | Candies and Gummies |

| Jellies and Fruit Pastilles | |

| Fruit Bars and Snacks | |

| Others | |

| Dairy and Frozen Products | |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Fruit Type | Citrus Fruits | |

| Red Fruits & Berries | ||

| Tropical Fruits | ||

| Others | ||

| By Product Form | Liquid Concentrate | |

| Powder Concentrate | ||

| Others | ||

| By Application | Beverages | Fruit Juices and Drinks |

| Soft Drinks and Carbonated Beverages | ||

| Alcoholic Beverages | ||

| Bread and Bakery Products | ||

| Confectionery | Candies and Gummies | |

| Jellies and Fruit Pastilles | ||

| Fruit Bars and Snacks | ||

| Others | ||

| Dairy and Frozen Products | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global fruit concentrates market in 2026?

The fruit concentrates market size reached USD 51.03 billion in 2026 and is projected to grow at a 4.44% CAGR to USD 63.41 billion by 2031.

Which fruit type is growing fastest?

Tropical fruit concentrates lead growth with a forecast 5.86% CAGR owing to consumer appetite for exotic flavors and premium positioning.

Why are powder concentrates gaining attention?

Powder formats register a 5.12% CAGR because they offer two-year shelf life, lower freight costs and suitability for e-commerce and sports-nutrition channels.

Which region will post the highest growth through 2031?

Asia Pacific is set for a 6.18% CAGR, driven by processing investments in China, Vietnam and India and rising middle-class consumption.

Page last updated on: