Market Overview

| Study Period | 2020 - 2031 |

|---|---|

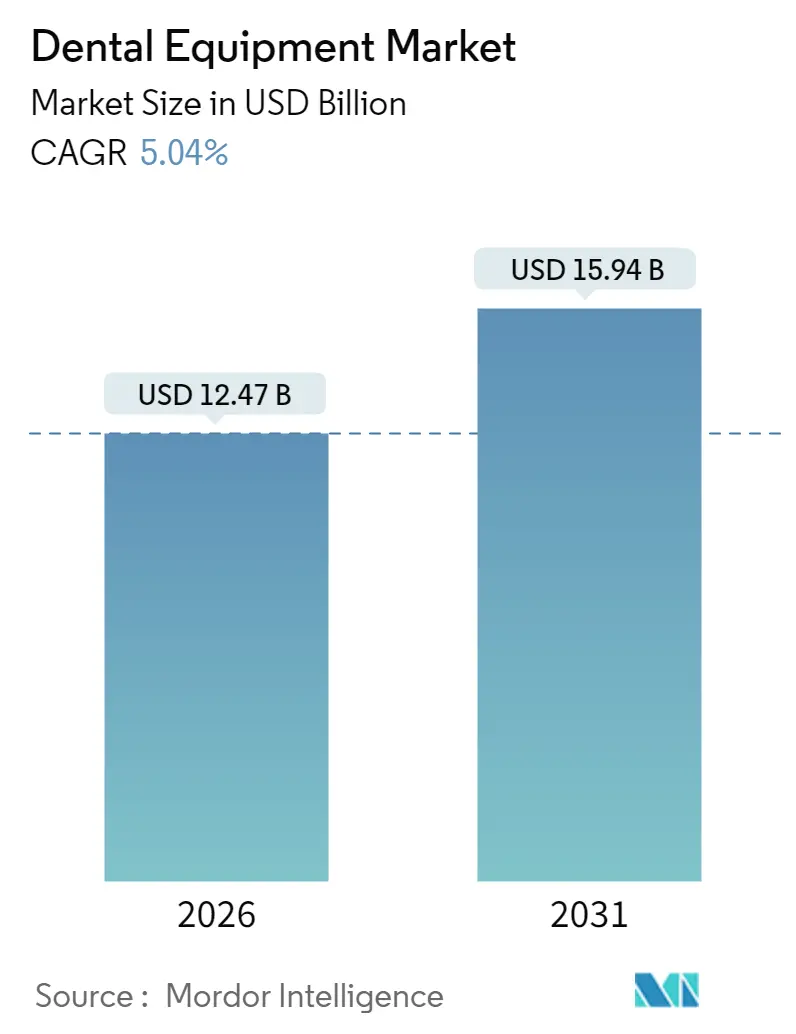

| Market Size (2026) | USD 12.47 Billion |

| Market Size (2031) | USD 15.94 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

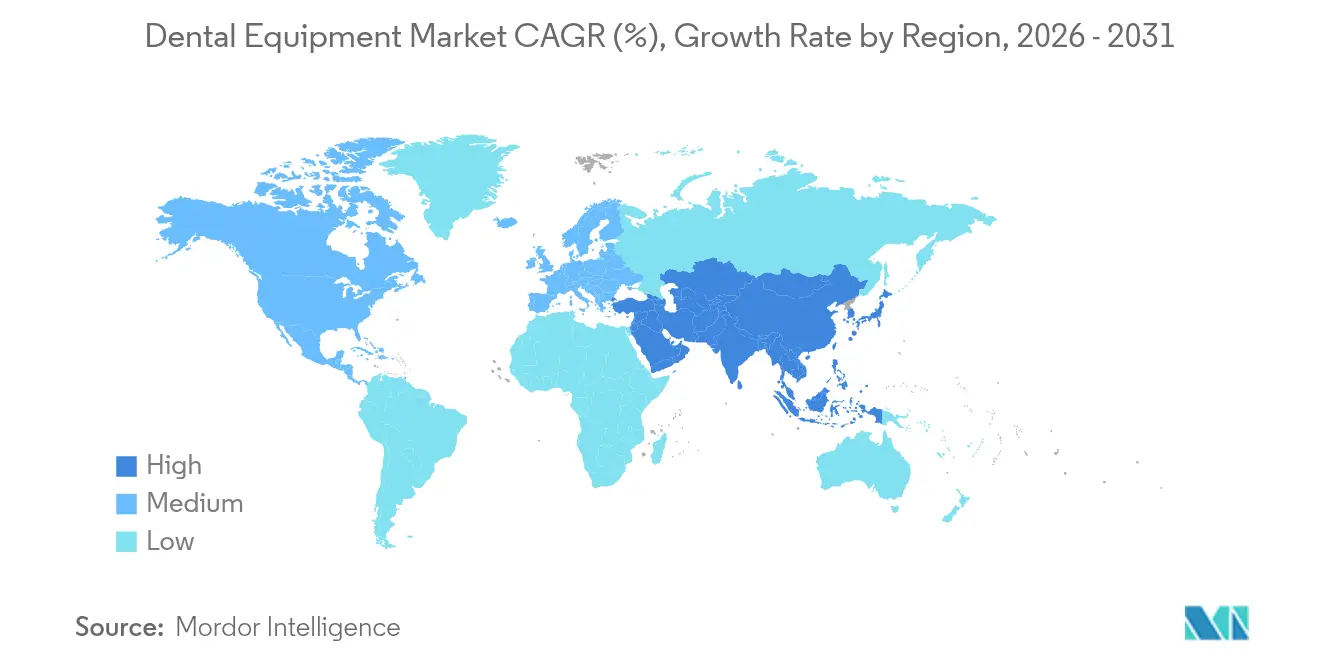

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Equipment Market Analysis by Mordor Intelligence

The Dental Equipment market is expected to grow from USD 11.87 billion in 2025 to USD 12.47 billion in 2026 and is forecast to reach USD 15.94 billion by 2031 at 5.04% CAGR over 2026-2031.

Adoption of digital imaging, artificial intelligence, and chairside manufacturing is shortening procedure times, improving diagnostic accuracy, and lifting patient acceptance rates. Demand is further supported by rising incidences of dental caries and periodontal disease, steady growth in elective cosmetic procedures, and a strong pipeline of restorative materials that pair high strength with natural aesthetics. Consolidation among large manufacturers is creating scale advantages in research, procurement, and global distribution, while new entrants concentrate on narrow specialties such as AI-based image analytics, robotic surgery aids, and bioceramic implants. Asia-Pacific clinics, buoyed by dental tourism and government incentives for digital radiography, are reshaping the competitive balance by purchasing advanced systems in bulk and offering cost-effective care. At the same time, stricter infection-control rules continue to drive recurring investments in sterilization equipment, instrument tracking, and autoclave upgrades.

Key Report Takeaway

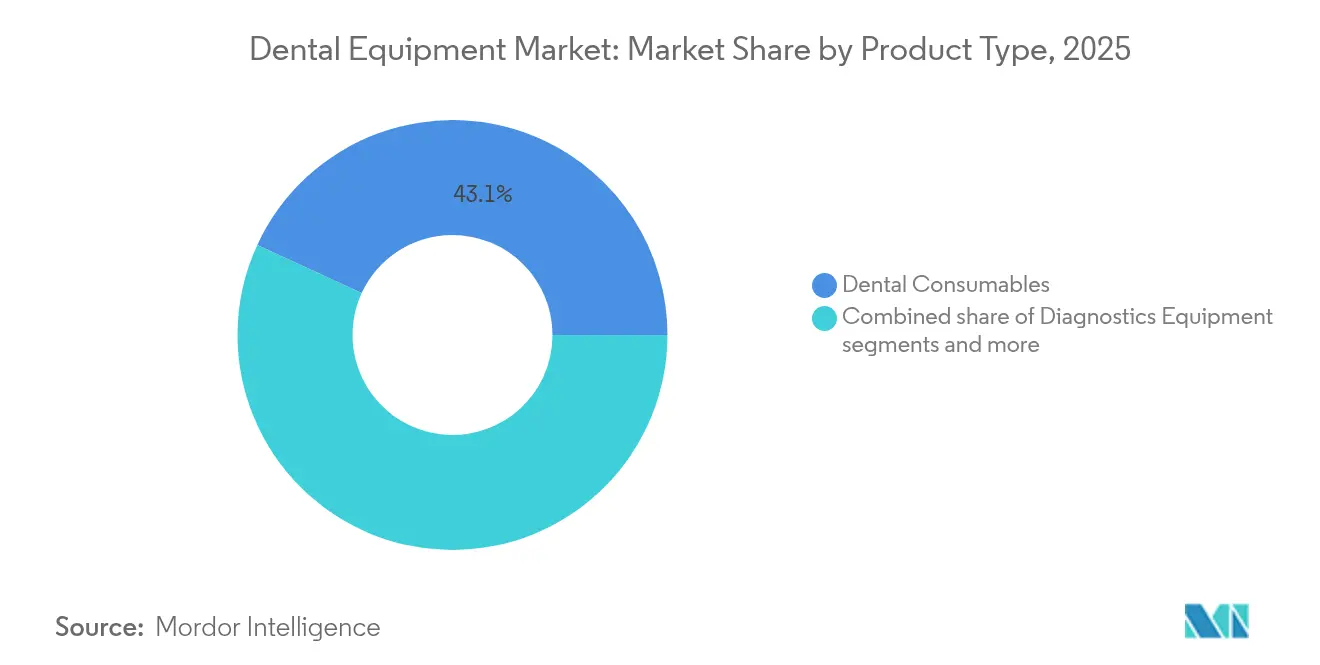

- By product type, dental consumables held 43.12% of the dental equipment market share in 2025. Dental equipment is projected to register the fastest 6.05% CAGR between 2026 and 2031.

- By treatment, prosthodontics accounted for 38.05% of the dental equipment market size in 2025. Orthodontic treatments are forecast to record a 6.74% CAGR through 2031.

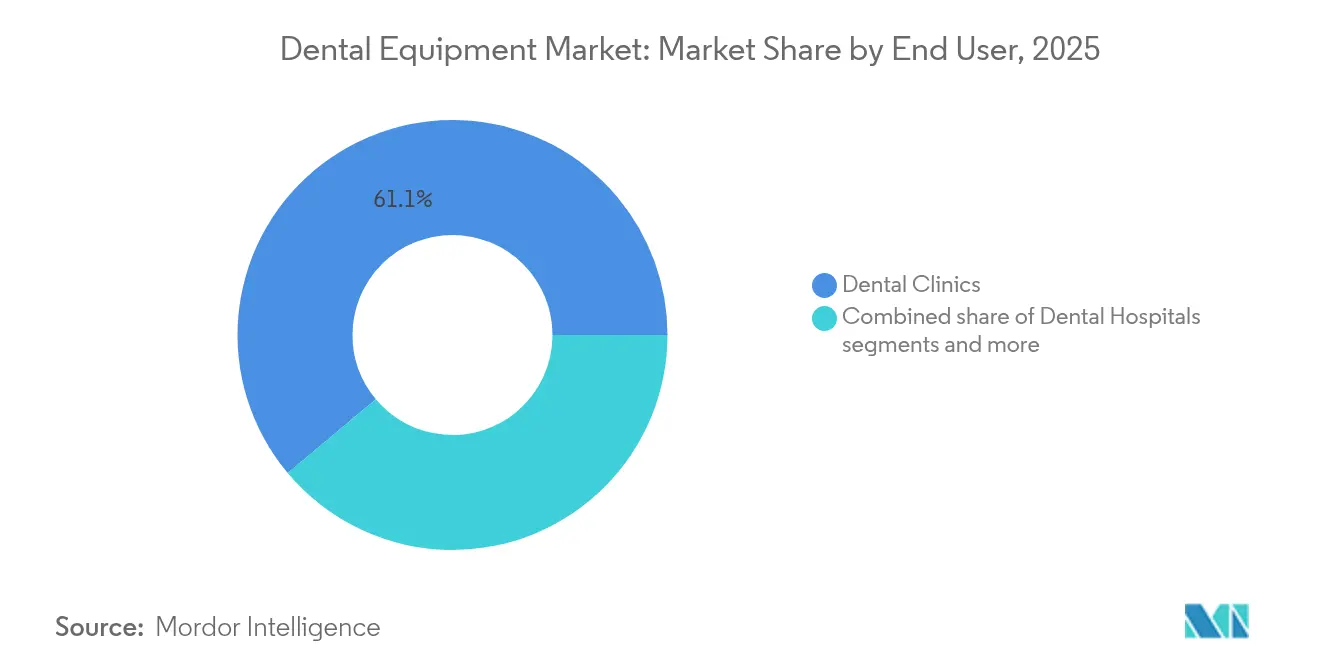

- By end user, dental clinics captured 61.10% of revenue in 2025, while also showing the highest 6.52% CAGR outlook to 2031.

- North America remained the largest regional contributor in 2025; Asia-Pacific is the fastest-growing region, advancing at more than twice the global pace

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Equipment Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries & periodontal diseases | +0.4% | Global, with higher impact in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Integration of AI-driven imaging & diagnostics accelerating equipment upgrades | +1.1% | North America & Europe, with growing adoption in Asia-Pacific | Medium term (2-4 years) |

| Growing dental tourism driving clinic expansion & equipment investments | +0.7% | Asia-Pacific (Thailand, India), Eastern Europe (Hungary, Turkey) | Medium term (2-4 years) |

| Government incentives for digital radiography in Japan & South Korea | +0.5% | Japan, South Korea, with potential expansion to other Asian countries | Short term (≤ 2 years) |

| Emergence of chairside 3-D printing cutting prosthetic turnaround times | +0.8% | North America, Europe, with expansion to Asia-Pacific | Medium term (2-4 years) |

| Reusable-instrument sterilization demand amid stricter infection-control rules | +0.6% | Global, with emphasis on developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of dental caries and periodontal disease

Global epidemiological studies show continuing growth in untreated decay and gum infection, particularly among aging adults and children in emerging economies. The resulting clinical workload sustains demand for basic restorative items, endodontic files, and periodontal instruments. National oral-health campaigns in India and Indonesia are bringing more first-time patients into clinics, expanding routine prophylaxis volumes and boosting sales of prophylaxis pastes and sealants[1]Source: American Dental Association, “Dental Care Spending, 2025,” ada.org . This mounting preventive-care demand indirectly strengthens the dental equipment market

AI-enabled imaging and diagnostics accelerating equipment upgrades

AI algorithms integrated into cone-beam CT and intraoral imaging platforms flag minute lesions, quantify bone levels, and auto-generate treatment plans that dentists can share chairside. Early adopters report 10-20% growth in case acceptance when AI visuals accompany explanations, sparking an upgrade cycle across mid-size practices. Overjet’s regulatory-cleared software now processes millions of radiographs per month, signalling rapid normalization of AI diagnostics and reinforcing the dental equipment market.

Dental tourism prompting clinic expansion and device spending

Price-sensitive patients from the United States, Western Europe, and Australia regularly fly to Bangkok or Budapest for full-arch implants that can cost 50-70% less than at home. To compete for this inflow, destination clinics outfit operatories with premium CAD/CAM mills, optical scanners, and implant navigation systems. Cluster effects emerge as local suppliers, training schools, and maintenance providers co-locate, reinforcing regional hubs and enlarging the dental equipment market.

Government incentives for digital radiography

Japan’s Ministry of Health subsidizes up to 40% of certified digital imaging purchases, aiming to equip 80% of dental offices with low-dose CBCT by 2027. South Korea’s Digital Healthcare Innovation Plan offers tax credits for cloud-connected sensors, driving a nationwide migration from film to pixel arrays. These programs sharply compress the upgrade timeline and lift regional sales of sensors, software, and picture-archiving systems, further accelerating growth in the dental equipment market..

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement gaps for laser-assisted treatments | -0.8% | North America, Europe, with significant impact in rural and underserved areas | Medium term (2-4 years) |

| Shortage of skilled technicians for advanced CAD/CAM workflows | -0.6% | Global, with acute impact in emerging markets | Long term (≥ 4 years) |

| High upfront cost of incorporating AI imaging into small clinics | -0.5% | Global, with particular impact on solo practices and rural clinics | Medium term (2-4 years) |

| Supply-chain fragility in zirconia & titanium for implant production | -0.4% | Global, with concentration risk in China and Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited insurance reimbursement for laser-assisted treatments

Insurers often classify laser gum surgery and caries ablation as elective, shifting costs to patients and slowing adoption despite shorter healing times and improved clinical outcomes. Manufacturers respond with hybrid devices that allow dentists to toggle between conventional and laser modes to remain within coverage limits.

Shortage of technicians skilled in complex CAD/CAM workflows

Advanced design software and five-axis mills require specialised operators. Dental schools and vocational institutes currently graduate fewer lab technologists than open positions, extending equipment learning curves and delaying return on investment for practices, particularly in Latin America and the Middle East.

Segment Analysis

By Product Type: Consumables dominate while equipment accelerates

Dental consumables captured 43.12% of the dental equipment market in 2025 thanks to their recurring use in every clinical visit. Steady demand for impression materials, composites, burs, and anesthetics shields this segment from macro-economic cycles. Bioceramic implants and bio-active restoratives are gaining traction as ageing populations seek durable, naturally coloured options. Conversely, equipment sales, while smaller in absolute value, are rising faster. Diagnostic scanners, digital radiography panels, chairside mills, and diode lasers together are projected to grow at a 6.05% CAGR through 2031, fuelled by AI software updates and subscription models that smooth cash flows for clinics. Bundled service contracts and cloud licences increasingly define revenue for manufacturers, signalling a pivot from hardware outright sales to lifetime value. The dental equipment market size for high-value equipment is therefore widening faster than historic averages, offering suppliers diversified growth beyond consumables.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Treatment: Prosthodontics leads while orthodontics innovates

Prosthodontic procedures generated 38.05% of global revenue in 2025, anchored by implant-supported crowns, bridges, and full-arch rehabilitations that command high per-case spending. Immediate-load protocols and low-dose CBCT planning streamline treatment, sustaining volume even in tighter economic climates. Orthodontics, however, is set to expand the fastest at a 6.74% CAGR to 2031 as clear aligners tap into adult demand for discreet cosmetic correction. Remote monitoring apps reduce in-office visits and attract digitally savvy patients, widening market reach. The dental equipment market share commanded by aligner systems is therefore growing at the expense of fixed brackets in developed economies, though traditional appliances still dominate in cost-constrained regions. Combination therapy that blends limited aligner stages with final bracket finishing has emerged as a middle-ground option, influencing device kits and bonding adhesives upstream.

By End User: Dental clinics drive market momentum

Independent practices and small group networks represented 61.10% of global spending in 2025 because most routine care and elective aesthetics occur in office-based settings. Consolidation into Dental Service Organizations (DSOs) is accelerating, allowing centralised purchasing of imaging suites, sterilisation centres, and unified software licences. DSOs often standardise on a single supplier across hundreds of operatories, creating large block orders that shape product roadmaps. Dental hospitals and university clinics still lead in complex oral-surgery procedures and advanced research but account for a smaller share of overall volume. The dental equipment market size allocated to clinics is expected to outpace institutional segments, reflecting growing patient preference for convenient community-based care that now offers the same digital capabilities once limited to tertiary centres.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

North America remains the largest contributor to dental equipment revenue due to high per-capita expenditure, insurance penetration, and widespread adoption of AI imaging and CAD/CAM fabrication. U.S. insurers reimburse intraoral scans for aligner case submission, reinforcing digital uptake. Workforce shortages and rising labour costs, however, encourage practices to automate documentation and sterilisation, raising demand for integrated software suites.

Europe ranks second, with Germany, France, and the United Kingdom leading purchases of premium implant systems and low-dose CBCT units. Sustainability regulations accelerate replacement of mercury-based amalgam separators and single-use plastics, pushing clinics toward eco-designed tools. EU conformity updates under the Medical Device Regulation have lengthened certification lead times, favouring established suppliers that possess the resources to comply.

Asia-Pacific is the fastest-growing region. Japan’s public insurance now reimburses select CAD/CAM crowns, lifting scanner installations, while South Korean clinics advertise fully digital smile design to regional tourists. India’s urban centres witness rapid expansion of mid-market chains offering clear aligner packages priced for the rising middle class. China continues to invest in domestic 3-D printer brands and zirconia block manufacturing, aiming to reduce import dependency. Overall, the dental equipment market size in Asia-Pacific is expected to double across the decade, driven by both volume and technology mix upgrades.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The top five suppliers—Dentsply Sirona, Envista, Straumann Group, Align Technology, and Planmeca—collectively control roughly majority of global revenue, resulting in a moderately consolidated environment. Scale enables these firms to fund multi-year R&D pipelines, integrate AI into hardware, and negotiate long-term raw-material contracts. Mid-tier specialists differentiate through focused portfolios: Vatech excels in imaging, W&H in rotary instrumentation, and GC Corporation in restorative chemistry. Start-ups such as VideaHealth and Pearl concentrate on AI-as-a-service models that sidestep capital equipment barriers for clinics.

Strategic alliances multiply: Straumann acquired GalvoSurge for implant decontamination[2]Source: Straumann Group, “Annual Report 2023,” straumann.com , adding value across its implant line; Planmeca partners with Overjet to embed lesion-detection algorithms natively into its Romexis software. The field is shifting from single-SKU competition toward full-workflow ecosystems that blend hardware, consumables, and cloud analytics.

Dental Equipment Industry Leaders

3M

Dentsply Sirona

GC Corporation

A-Dec Inc.

Aseptico Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Planmeca introduced the Viso G1 CBCT unit, ProX GO handheld X-ray, and Onyx wireless scanner, complemented by Romexis 7 software featuring integrated AI tools for automated pathology detection.

- March 2025: Dentsply Sirona unveiled greener packaging and energy-efficient milling units while pledging carbon-neutral operations by 2030

- January 2025: NovaBone partnered with BEGO to distribute bone-graft dental putty cartridges across Europe, strengthening regenerative portfolios

Global Dental Equipment Market Report Scope

As per the scope of the report, dental equipment refers to tools used by dental professionals to provide dental treatment. These include tools to examine, manipulate, treat, restore, and remove teeth and surrounding oral structures. Standard instruments are used to examine, restore, extract teeth, and manipulate tissues.

The dental equipment market is segmented by product, treatment, end user, and geography. The product segment is further divided into operatory and treatment center equipment, dental laboratory equipment, dental lasers, and diagnostic dental equipment. The operatory and treatment center equipment is further divided into dental units, dental handpieces, dental light-curing equipment, electrosurgical systems, and others. The dental laboratory equipment segment is further segmented into CAD/CAM systems, milling equipment, 3D printing equipment, casting machines, ceramic furnaces, and others. The dental lasers segment is further segmented into soft tissue lasers and hard tissue lasers. The diagnostic dental equipment segment is further divided into extraoral imaging systems and intraoral imaging systems. The treatment segment is further divided into orthodontic, endodontic, periodontic, and prosthodontic. The end-user segment is further segmented into hospitals, clinics, and other end-users. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

By Product

| Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra-oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair & Equipment | ||

| Therapeutic Equipment | Dental Hand Pieces | |

| Electrosurgical Systems | ||

| CAD/CAM Systems | ||

| Milling Equipment | ||

| Casting Machine | ||

| Other Therapeutic Equipments | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns & Bridges | ||

| Other Dental Consumables | ||

| Other Dental Equipments | ||

By Treatment

| Orthodontic |

| Endodontic |

| Periodontic |

| Prosthodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra-oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair & Equipment | |||

| Therapeutic Equipment | Dental Hand Pieces | ||

| Electrosurgical Systems | |||

| CAD/CAM Systems | |||

| Milling Equipment | |||

| Casting Machine | |||

| Other Therapeutic Equipments | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns & Bridges | |||

| Other Dental Consumables | |||

| Other Dental Equipments | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Periodontic | |||

| Prosthodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

1. What is the current size of the dental equipment market?

The dental equipment market stands at USD 12.47 billion in 2026 and is forecast to reach USD 15.94 billion by 2031.

2. Which product segment leads global revenue?

Dental consumables lead with 43.12% of worldwide sales, reflecting their routine use across all clinical procedures.

3. Which treatment type is growing the fastest?

Orthodontic therapies, especially clear aligner systems, are projected to grow at a 6.74% CAGR through 2031.

4. Why is Asia-Pacific expanding faster than other regions?

Rapid clinic construction, dental tourism, and government support for digital radiography are driving double-digit equipment purchases across China, India, Japan, and South Korea.