Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

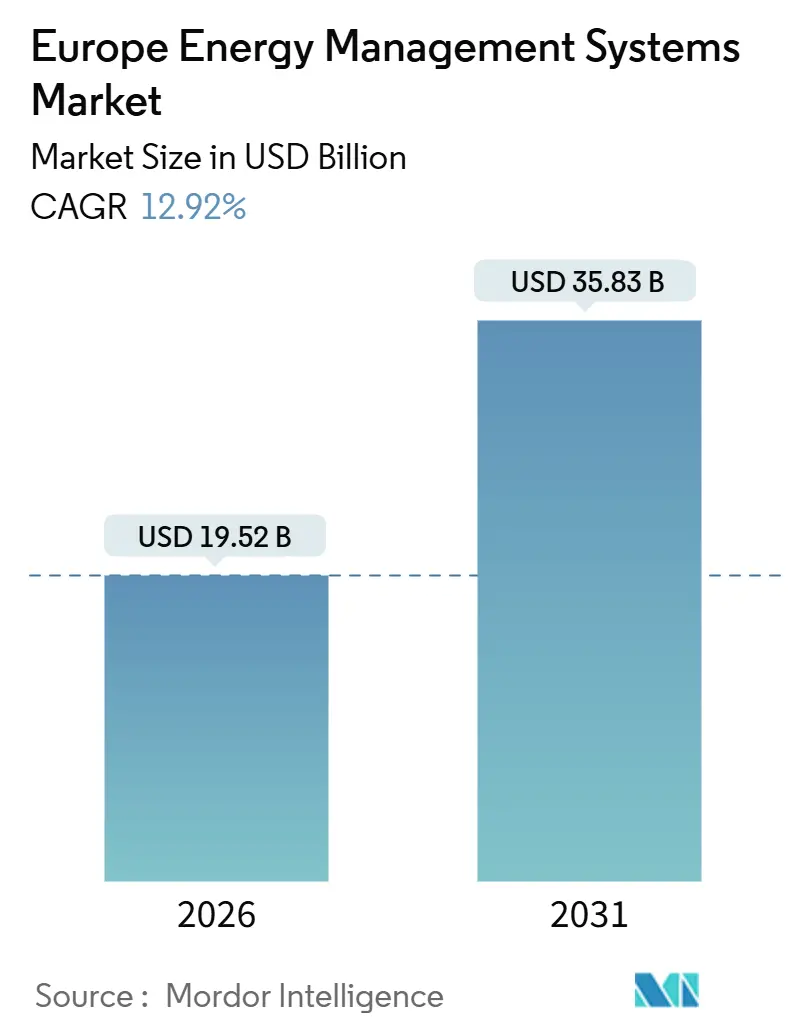

| Market Size (2026) | USD 19.52 Billion |

| Market Size (2031) | USD 35.83 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Energy Management Systems Market Analysis by Mordor Intelligence

The Europe energy management systems market size is USD 19.52 billion in 2026 and is projected to reach USD 35.83 billion by 2031, translating into a 12.92% CAGR over the period. The upward trajectory is anchored by binding EU efficiency mandates, surging corporate net-zero pledges, and a rapid shift toward AI-enabled optimization that turns real-time load data into actionable insights. Heightened investment in smart-grid infrastructure, large-scale smart-meter rollouts, and the growing appeal of demand-response revenues strengthen the expansion path, while software-defined architectures lower entry costs for smaller enterprises. Competitive dynamics remain intense as hardware incumbents defend their installed bases against cloud-native challengers courting clients seeking vendor-agnostic solutions. Early adopters in Germany, France, and the Nordics are achieving double-digit efficiency gains, creating proven business cases that are now rippling across Southern and Eastern Europe.

Key Report Takeaways

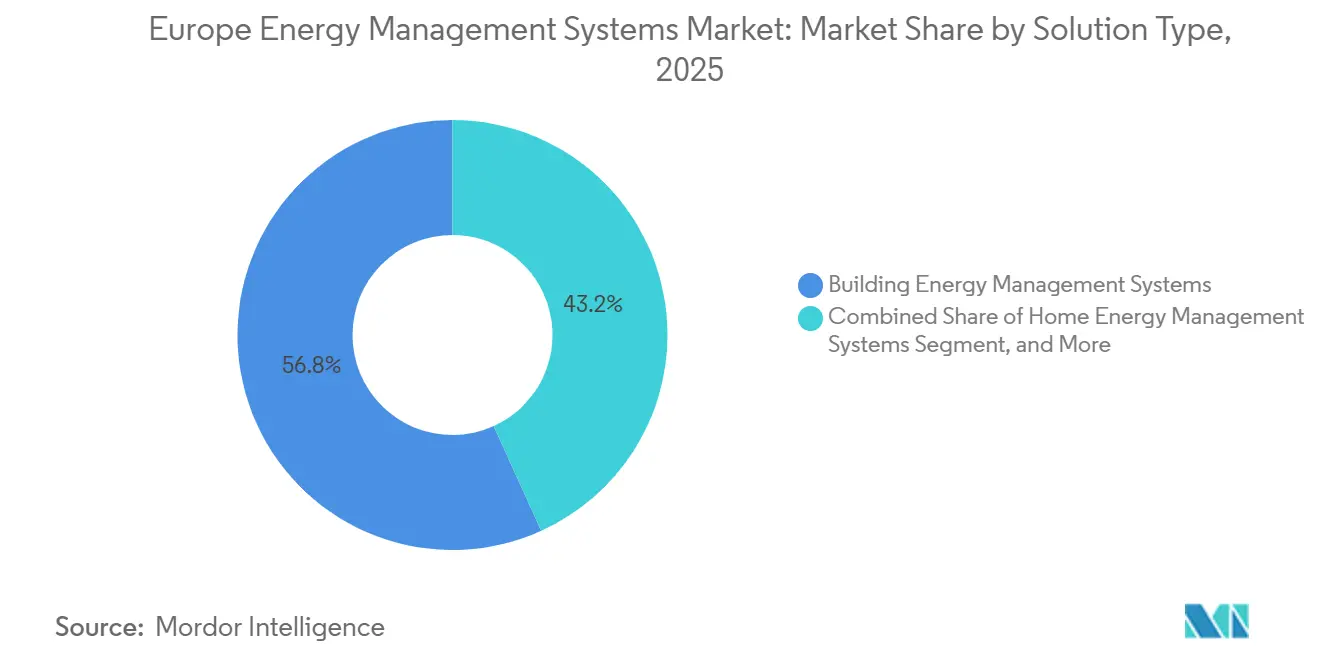

- By solution type, building energy management systems led with a 56.78% of the Europe energy management systems market share in 2025, while home energy management systems are forecast to expand at a 13.89% CAGR through 2031.

- By component, hardware accounted for 47.93% of spending in 2025, but software is expected to advance at a 13.66% CAGR through 2031.

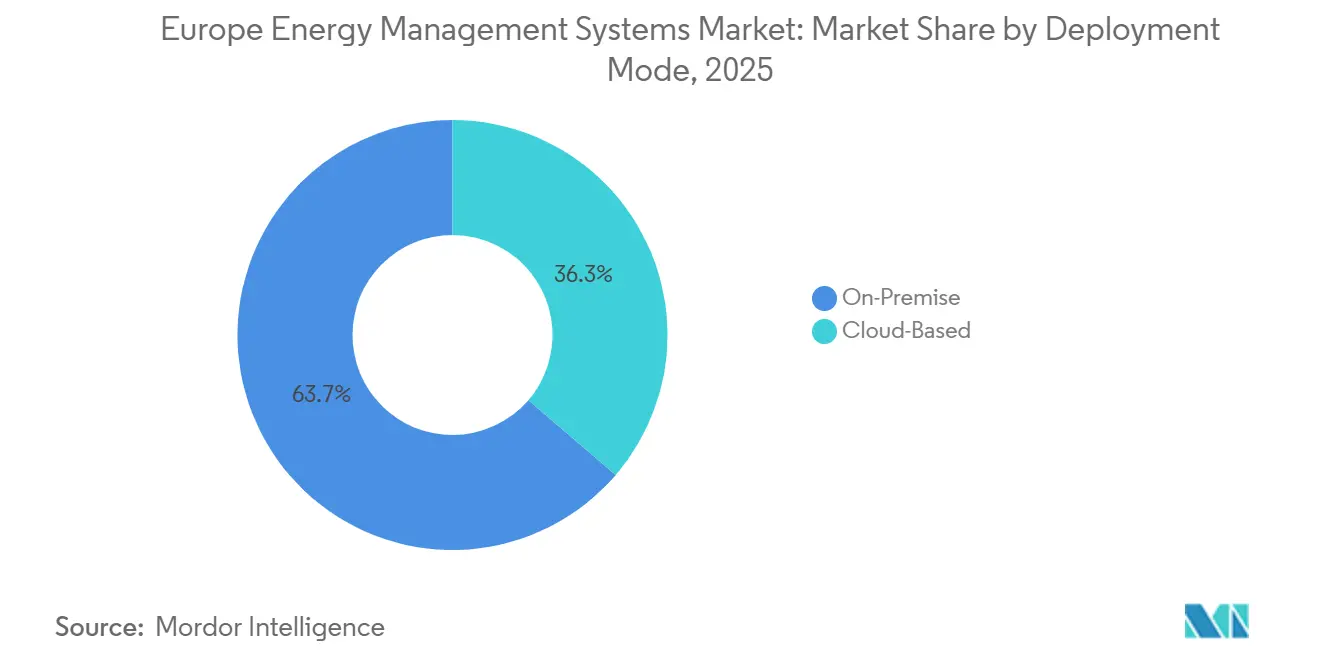

- By deployment mode, on-premises installations accounted for 63.71% of the Europe energy management systems market share in 2025, whereas cloud-based platforms are projected to grow at a 13.47% CAGR through 2031.

- By end user, commercial and retail sites accounted for 39.63% of the Europe energy management systems market share in 2025, yet the residential segment is poised for the fastest 14.11% CAGR over the forecast period.

- By country, Germany captured 25.71% of regional revenue in 2025, while Spain is set to post the highest CAGR of 14.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Energy Management Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Deployment of Smart-Grid Infrastructure | +2.3% | Germany, France, Nordics, Benelux, Spain | Medium term (2-4 years) |

| EU Fit-for-55 Energy-Efficiency Mandates | +3.1% | All member states, strongest in Germany, France, Italy | Short term (≤ 2 years) |

| Corporate Net-Zero Targets Accelerating EMS Adoption | +2.0% | United Kingdom, Germany, Nordics, Southern Europe | Medium term (2-4 years) |

| Building-Level AI and ML Optimization of HVAC Loads | +1.8% | Germany, France, United Kingdom, Spain, Italy | Long term (≥ 4 years) |

| Rise of Flexibility Markets and Demand-Response Revenues | +1.5% | Spain, Germany, France, Italy, Nordics | Medium term (2-4 years) |

| Edge-to-Cloud Cybersecurity Toolkits Reducing Project Risk | +1.3% | Pan-European, pivotal for industry and healthcare | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Deployment of Smart-Grid Infrastructure

European transmission and distribution operators have earmarked EUR 584 billion for grid upgrades this decade, allocating nearly 40% to digital technologies that turn passive meters into intelligent endpoints.[1]ENTSO-E, “Ten-Year Network Development Plan 2024,” entsoe.eu Germany’s goal to install 50 million smart meters by 2032, combined with France’s completed Linky rollout, provides a granular data backbone that enables energy management platforms to optimize loads in 15-minute increments and synchronize with wholesale market price signals. Nordic utilities already coordinate EMS with district-heating loops, trimming peak demand by up to 12%. These successes validate business cases elsewhere, encouraging Spain and Benelux network operators to fast-track advanced metering. As two-way communication matures, buildings equipped with EMS shift from energy takers to grid assets, capturing new revenue streams from balancing and capacity markets.

EU Fit-for-55 Energy-Efficiency Mandates

Directive 2023/1791 requires enterprises that use more than 85 TJ annually to install certified energy management systems, instantly expanding the mandatory addressable base to roughly 12,000 industrial facilities.[2]European Commission, “Energy Efficiency Directive (EU) 2023/1791,” energy.ec.europa.eu The revised buildings directive slashes the HVAC threshold to 290 kW, adding millions of square meters of retail, hospitality, and office space to the compliance roster. Member states transposed the rules into national codes at record speed. Germany’s Gebäudeenergiegesetz, France’s Décret Tertiaire, and Spain’s Real Decreto 390/2021 each impose aggressive retrofit schedules backed by escalating fines. Because penalties outweigh project paybacks, chief financial officers now classify EMS spending as regulatory capital rather than a discretionary outlay, accelerating procurement cycles from years to quarters.

Corporate Net-Zero Targets Accelerating EMS Adoption

More than 1,400 European firms have validated science-based emissions pathways, and electricity purchases represent up to half of their footprints.[3]Science Based Targets initiative, “Companies Taking Action,” sciencebasedtargets.org EMS platforms provide real-time telemetry that CFOs need to keep production output steady while staying within annual carbon budgets. Surveys show 68% of finance chiefs now rank efficiency investments above other green projects due to quick returns and lower technology risk. Pharmaceutical cleanrooms, automotive paint lines, and grocery refrigeration aisles have already documented double-digit electricity cuts within 18 months of deployment, reinforcing internal confidence in further rollouts and spurring peer benchmarking across sectors.

Building-Level AI and ML Optimization of HVAC Loads

HVAC accounts for 40-60% of commercial energy use, making it fertile ground for machine-learning optimization. Cloud-hosted engines ingest weather forecasts, occupancy trends, and equipment telemetry to recalibrate setpoints every few minutes, routinely shaving 8-15% from electricity bills. Edge computing now embeds inference chips directly in controllers, letting buildings self-tune even if cloud links go down. Early pilots in premium offices, hospitals, and data centers demonstrate consistent savings, but legacy hardware in smaller properties still poses integration hurdles. Vendors respond with retrofit kits that translate proprietary field protocols into open APIs, narrowing the performance gap between blue-chip flagships and mass-market adopters.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Country-Level Building Codes | -1.2% | Entire region, most acute in Southern and Eastern Europe | Medium term (2-4 years) |

| Skill-Set Shortage for Advanced Analytics | -0.9% | Germany, France, United Kingdom, Nordics | Long term (≥ 4 years) |

| Interoperability Gaps Across Legacy BMS Protocols | -0.7% | Italy, Spain, United Kingdom, older stock | Medium term (2-4 years) |

| Inflation-Driven Capex Deferrals in SMEs | -0.8% | Spain, Italy, Central Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Country-Level Building Codes

While EU directives set high-level goals, each member state specifies its own technical test points, sensor densities, and inspection cadences, creating 27 parallel compliance tracks. Vendors must customize firmware and documentation to satisfy divergent national norms, adding as much as 30% to integration costs and 18 months to go-to-market timelines. Smaller suppliers struggle most, effectively ceding pan-regional deals to large incumbents that can absorb the overhead. Harmonization efforts are underway, but until a common rulebook emerges, deployment speed in Southern and Eastern Europe will lag behind that of the core markets of Germany and France.

Skill-Set Shortage for Advanced Analytics

Machine-learning tools unlock the next wave of savings, but they demand talent versed in time-series modeling, thermodynamics, and cloud orchestration. Europe is short roughly 150,000 such specialists, and energy firms compete head-to-head with finance and tech for recruits. Facilities managers steeped in mechanical systems often lack Python or TensorFlow expertise, forcing vendors to bundle managed services, which drives up the total cost of ownership. National training programs and university curricula will eventually fill the gap, yet most will not graduate cohorts before 2027, constraining near-term scaling.

Segment Analysis

By Solution Type: Residential HEMS Gains Momentum

The Europe energy management systems market generated its highest revenue from building energy management systems in 2025, capturing 56.78% of total revenue, thanks to decades-old installations in offices, factories, and hospitals. Growth, however, is tilting toward home energy management systems, which boast a 13.89% forecast CAGR as heat-pump subsidies proliferate and dynamic tariffs create lucrative arbitrage windows for households. Europe installed more than 3 million new residential heat pumps in 2024, and smart meters now cover over 70% of dwellings in several member states, providing HEMS with the data granularity needed for automated load shifting.

Momentum builds further because the Energy Performance of Buildings Directive requires a smart-readiness label for every new home from 2027. Platforms such as Schneider Electric’s Wiser Home already equip half a million European residences with predictive scheduling that cuts gas use by up to 12%. Industrial EMS solutions, while slower-growing, remain critical for heavy-process sectors where energy equals 30-40% of operating costs. Niche categories, including data-center power optimization, round out the mix, underscoring how the Europe energy management systems market continues to diversify across building classes and use cases.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Software Outpaces Hardware Growth

Hardware controlled 47.93% of component revenue in 2025, covering sensors, gateways, and actuators that form the nervous system of an EMS. Software, however, is the star performer with a projected 13.66% CAGR, propelled by cloud analytics that monetize anonymized multi-site datasets and enable subscription pricing. Digital twins, portfolio dashboards, and open APIs that sync with BIM and ERP suites transform raw data into executive-ready KPIs. Vendors now preload edge controllers with flexible compute blocks that host local AI models, blending real-time control with cloud-level insight for resilience and bandwidth savings.

Services revenue holds steady as integrators bundle design, commissioning, and analytics management, yet self-service portals and automated device discovery are slowly compressing margins. The shift toward code-heavy value propositions mirrors broader Industry 4.0 trends, ensuring that software will continue to expand its share of the Europe energy management systems market even as hardware upgrades roll out.

By Deployment Mode: Cloud Architectures Gain Share

On-premises implementations accounted for 63.71% of the market in 2025, reflecting historical preferences for isolated networks and direct control. Cloud deployments, advancing at a 13.47% CAGR, cut upfront spending and deliver evergreen feature updates without local server maintenance. ISO 27001-certified hyperscale data centers now exceed the cyber-compliance thresholds that once favored air-gapped designs, opening doors even in rigorously regulated verticals such as pharmaceuticals and healthcare.

Hybrid frameworks blend edge gateways for sub-second control with cloud analytics for fleet-wide benchmarking, matching Germany’s data-residency rules while preserving cross-site learning loops. The European Data Act, effective in 2025, further boosts adoption by mandating data portability, reducing lock-in concerns, and prompting multi-tenant property managers to migrate legacy on-premises stacks to the cloud.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Residential Segment Leads Growth

Commercial and retail facilities dominated demand in 2025, with a 39.63% share, driven by office landlords seeking LEED, BREEAM, and WELL certifications and by supermarket chains optimizing refrigeration systems. The residential slice is forecast to register the fastest CAGR of 14.11%, supported by smart-meter saturation, renewable self-consumption schemes, and app-centric user experiences that resonate with tech-savvy homeowners. France’s MaPrimeRénov grants and Spain’s 40% heat-pump subsidy catalyze consumer uptake, while United Kingdom households prepare for Future Homes Standard requirements that effectively embed HEMS at the construction stage.

Industrial plants, healthcare campuses, and public institutions round out the user landscape, each driven by sector-specific mandates and incentives. Industrial players exploit EMS to synchronize energy with production cycles and to bid flexibility into capacity markets, whereas hospitals value continuous compliance with temperature and humidity. Government buildings leverage EMS to showcase fiscal prudence and meet climate targets, underscoring the multifaceted appeal of the Europe energy management systems market across stakeholder groups.

Geography Analysis

Germany’s leadership stems from the Energiewende framework, which mandates 4-year industrial audits and demands automation in non-residential buildings above 290 kW of HVAC. Manufacturing, which accounts for 28% of the nation’s power consumption, has documented 9-13% energy savings by leveraging EMS to coordinate motor drives and chillers. Spain’s emergence as the fastest-growing economy correlates with renewables delivering 60% of its 2025 electricity mix; EMS orchestrate load shifting and battery dispatch to counterbalance intermittent wind and solar output.

The United Kingdom’s Future Homes Standard compels builders to slash residential carbon footprints by 75%, driving HEMS integration with heat pumps and rooftop PV as the default. France confronts a building stock in which 60% predates modern energy-efficiency codes; the MaPrimeRénov program funnels billions into insulation, heating upgrades, and EMS retrofits, unlocking large-scale savings potential.

Italy grapples with a post-Superbonus hangover that briefly cooled residential demand, yet scaled-back tax deductions still fund 65% of EMS retrofit costs, and new loan-bundling models keep pipelines active. Nordic nations exploit advanced district-heating networks, deploying EMS to manage thermal tanks that soak up surplus wind energy and release it on peak winter evenings, lifting overall system efficiency by nearly 18%. In Benelux markets, which are dense and highly interconnected, firms explore price-arbitrage algorithms that capitalize on cross-border wholesale differentials. Central Europe, fueled by the European Investment Bank’s modernization line, accelerates public-building retrofits, inching closer to Western performance benchmarks.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The Europe energy management systems market is moderately fragmented. The top five manufacturers, Schneider Electric, Siemens, Honeywell, ABB, and Johnson Controls, collectively account for roughly 40-45% of 2025 revenue. These incumbents leverage massive installed bases and long-standing maintenance contracts to upsell cloud analytics and machine-learning add-ons. Software-native players, exemplified by C3.ai, mCloud, and Veritone, court customers with hardware-agnostic platforms that integrate via open APIs, sidestepping proprietary gateways. Utilities and energy-service companies such as Enel X and ENGIE Digital bundle EMS within broader demand-response aggregation offerings, winning clients who prefer outcome-based contracts over capital purchases.

Patent filings under the European Patent Office’s G06Q 50/06 class jumped 22% between 2023 and 2025, showcasing intense R&D around HVAC reinforcement learning, blockchain-verified energy trades, and OT cybersecurity. The small and medium enterprise segment remains white space; firms with annual energy bills below EUR 500,000 often lack expertise to tune algorithms, encouraging disruptors to offer turnkey packages with pre-configured vertical templates. Edge computing accelerates by embedding inference engines in field controllers, delivering millisecond response times vital for motor-drive optimization on factory floors.

Regulation also shapes competition. Platforms achieving IEC 62443 and ISO 27001 certifications enjoy fast-track procurement in regulated sectors, while the forthcoming Cyber Resilience Act will elevate conformity thresholds and may limit smaller vendors unable to finance third-party audits. Overall, rivalry centers on balancing cybersecurity assurances, open-system flexibility, and demonstrable ROI, setting a dynamic backdrop for the energy management systems market through 2031.

Europe Energy Management Systems Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

ABB Ltd

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: The European Investment Bank allocated EUR 1.8 billion to energy-efficiency projects in Central and Eastern Europe, prioritizing industrial EMS retrofits.

- November 2025: Schneider Electric introduced EcoStruxure Building Advisor, a cloud analytics suite now live at more than 2,000 European sites.

- October 2025: Siemens and Microsoft announced plans to link Desigo CC with Azure AI services across 5,000 buildings by 2027.

- September 2025: Honeywell purchased a minority position in GridPoint to bolster virtual-power-plant capabilities for European clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe energy management systems (EMS) market as the aggregated annual revenue generated from purpose-built hardware, software, and managed services that monitor, control, and optimize electricity, heating, and cooling loads in residential, commercial, and industrial facilities across EU-27, the United Kingdom, Norway, Switzerland, and Iceland. These solutions encompass building, home, and factory-level EMS that communicate with on-site or cloud analytics to cut energy intensity and emissions.

Scope Exclusion: Stand-alone utility SCADA platforms and wholesale energy-trading applications are outside the study.

Segmentation Overview

- By Solution Type

- Building Energy Management Systems

- Home Energy Management Systems

- Industrial Energy Management Systems

- Other Solution Types

- By Component

- Hardware

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud-Based

- By End-User

- Commercial and Retail

- Residential

- Industrial Facilities

- Healthcare

- Other End-Users

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Benelux

- Nordics

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed EMS software architects, facility managers, and energy-service contractors across Germany, Spain, the Nordics, and Benelux. These discussions clarified typical project ticket sizes, cloud-migration rates, and subsidy uptake, enabling us to stress-test desk assumptions and fine-tune cost-per-meter figures before final modeling.

Desk Research

We began with public macro and policy data sets such as Eurostat energy balances, the European Commission's Fit-for-55 impact assessments, ENTSO-E grid statistics, and International Energy Agency building end-use models. Trade associations, including Eurelectric and the European Heat Pump Association, helped us size installed equipment bases that drive EMS demand. Company 10-Ks, prospectuses, and EU environmental product declarations offered vendor pricing cues, while patents retrieved through Questel revealed emerging control algorithms. Our team also screened news and financial releases via Dow Jones Factiva and mapped player footprints with D&B Hoovers to triangulate addressable revenues.

The sources cited above illustrate, rather than exhaust, the wider pool consulted for data collection, validation, and clarification.

Market-Sizing & Forecasting

Top-down modeling starts with Eurostat sectoral electricity use, which is then adjusted by building-level automation penetration, average EMS spend per square meter, and national retrofit grant availability. Results are cross-checked through selective bottom-up roll-ups of supplier revenues and sampled average-selling-price × unit installations. Key variables like smart-meter rollout pace, carbon price trajectory, heat-pump sales, electricity tariff spreads, and cloud subscription discounts feed a multivariate regression that drives our 2025-2030 forecast. Gaps in country-level bottom-up data are bridged using three-year moving averages of retrofit activity validated during expert calls.

Data Validation & Update Cycle

Outputs undergo variance checks against IEA intensity benchmarks and ENTSO-E demand forecasts; anomalies trigger re-contact with domain experts before sign-off. Reports refresh yearly, and we issue mid-cycle updates when policy or price shocks materially alter the baseline. A final analyst review ensures clients receive the latest vetted view.

Why Mordor's Europe Energy Management Systems Baseline Commands Reliability

Published estimates rarely match because firms choose different geographic cuts, include or exclude service revenues, and refresh at uneven intervals.

Key gap drivers stem from scope breadth, subsidy pass-through assumptions, and currency translations that others fix at prior-year averages, whereas we rerun models each quarter when euro-dollar swings exceed five percent or new policy funding is released.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.27 B (2025) | Mordor Intelligence | - |

| USD 19.64 B (2025) | Regional Consultancy A | Adds utility SCADA services and applies uniform 15 % retrofit premium across all countries |

| USD 12.97 B (2024) | Trade Journal B | Limits scope to building segment and bases penetration on a single pan-EU survey of facility managers |

Taken together, the comparison shows that when definitions widen excessively or narrow to one segment, totals swing by several billion dollars. By anchoring numbers to transparent energy-use data and refreshed policy inputs, Mordor delivers a balanced, reproducible baseline that decision-makers can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe energy management systems market in 2026?

The market is valued at USD 19.52 billion in 2026 and is forecast to climb to USD 35.83 billion by 2031.

What CAGR is projected for Europe through 2031?

The Europe energy management systems market is expected to register a 12.92% CAGR over 2026-2031.

Which solution type commands the largest share today?

Building energy management systems led the region with a 56.78% revenue share in 2025.

Which segment will grow fastest over the forecast period?

Home energy management systems are projected to post the quickest 13.89% CAGR through 2031.

Which country will see the highest growth?

Spain is forecast to grow at a 14.67% CAGR, outpacing all other European markets through 2031.

Why are cloud deployments gaining traction?

Certified hyperscale platforms now meet strict cyber-compliance rules, cut capital outlay, and enable machine-learning upgrades, driving a 13.47% CAGR for cloud architectures.