Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

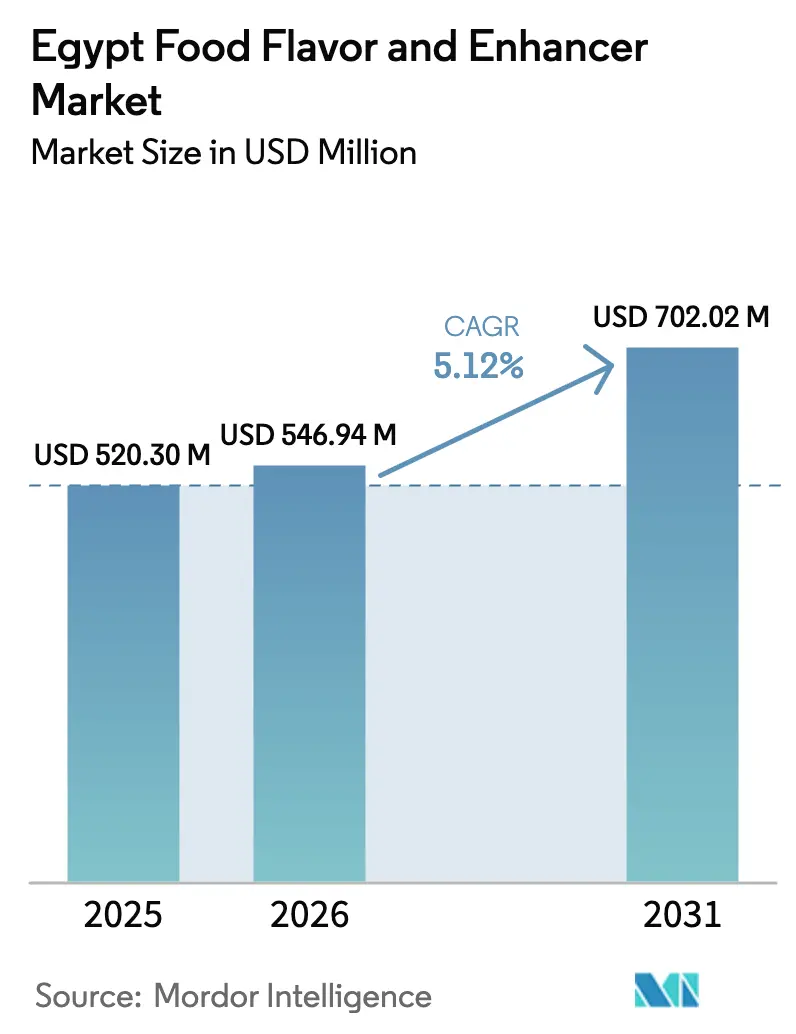

| Base Year Market Size (2025) | USD 520.30 Million |

| Market Size (2026) | USD 546.94 Million |

| Market Size (2031) | USD 702.02 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Food Flavor And Enhancer Market Analysis by Mordor Intelligence

The Egyptian food flavors and enhancers market size in 2026 is estimated at USD 546.94 million, growing from 2025 value of USD 520.30 million with 2031 projections showing USD 702.02 million, growing at 5.12% CAGR over 2026-2031. Expansion of Egypt’s food‐processing base, rising exports, and sustained tourism recovery are reinforcing demand for specialty taste solutions. The beverage industry anchors current consumption, while ready-to-eat foods post the quickest uptake as urban lifestyles accelerate. Global suppliers are scaling regional innovation hubs and patent-backed platforms, yet localization incentives under Egypt Vision 2030 are also nurturing agile domestic firms. The competitive landscape remains moderately concentrated, creating room for both scale efficiencies and niche flavor customizations.

Key Report Takeaways

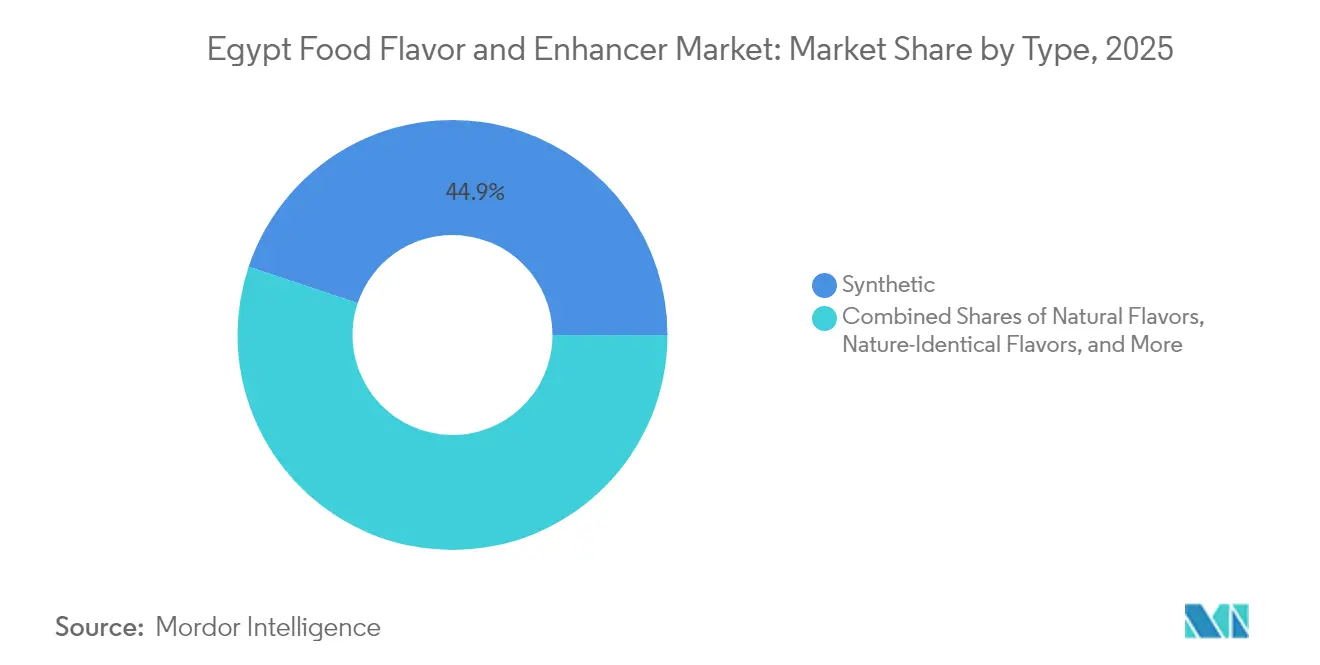

- By type, synthetic flavors led with 44.86% of Egypt food flavors and enhancers market share in 2025, while flavor enhancers are projected to expand at a 5.62% CAGR through 2031.

- By form, powder solutions commanded 53.64% share of the Egyptian food flavors and enhancers market size in 2025 and are advancing at a 5.74% CAGR to 2031.

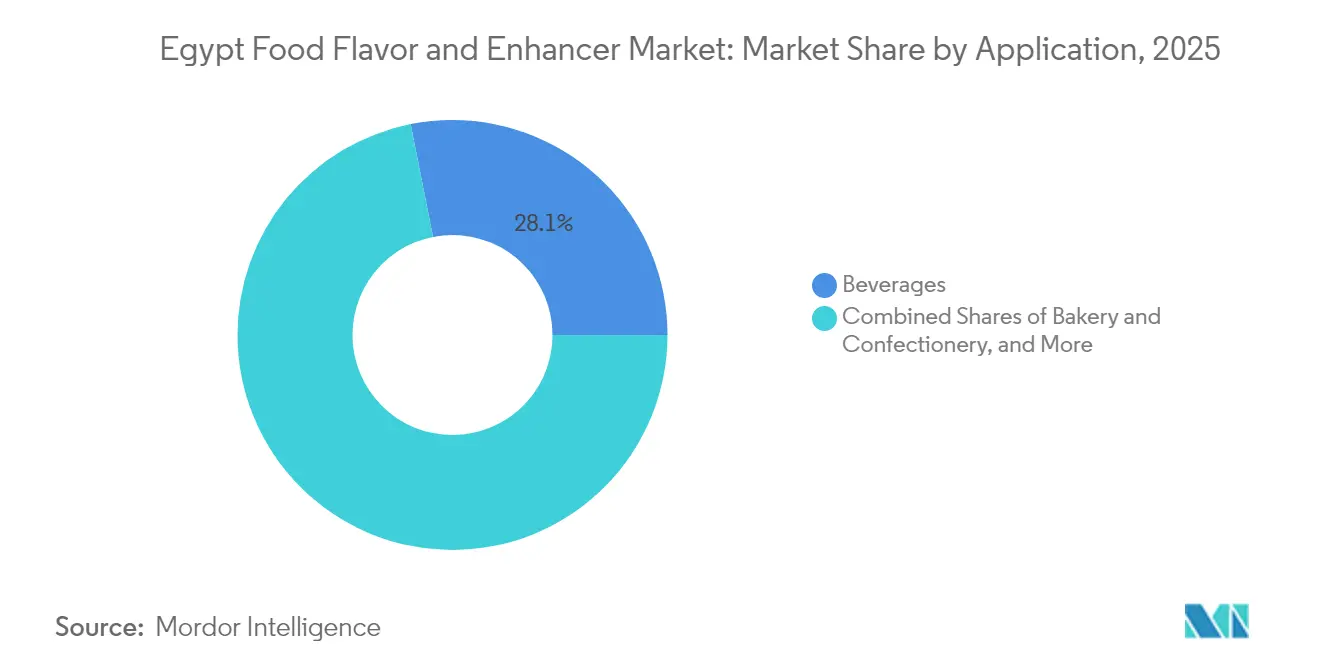

- By application, beverages accounted for a 28.12% slice of the Egyptian food flavors and enhancers market size in 2025; ready-to-eat foods are forecast to grow at a 6.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Food Flavor And Enhancer Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods | +1.2% | National, with concentration in Cairo and Alexandria urban centers | Medium term (2-4 years) |

| Clean label, natural, and organic ingredient trends | +0.8% | Global trend with local adaptation, strongest in tourist-facing establishments | Long term (≥ 4 years) |

| Technological advancements in Flavor Development | +0.9% | Global innovation with regional application centers in Dubai and Cairo | Medium term (2-4 years) |

| Localisation incentives under Egypt Vision 2030 & "Future" agri-megaproject | +1.1% | National, with early gains in New Delta and Sadat City industrial zones | Long term (≥ 4 years) |

| Micro-encapsulation tech enabling heat-stable flavour solutions | +0.7% | Global technology with MENA regional manufacturing hubs | Medium term (2-4 years) |

| Customization of flavors for local tastes and ethnic cuisine | +0.6% | National, with spillover to MENA export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed and Convenience Foods

In 2024, Egypt's processed food sector achieved a record export value of USD 6.1 billion, marking a 21% rise from the prior year. This growth is largely attributed to urbanization and evolving lifestyles, especially within Egypt's burgeoning middle class. Furthermore, the tourism sector, aiming to boost its visitors from 14.9 million in 2023 to 30 million by 2028, is fueling a heightened demand for sophisticated flavor solutions in hotel, restaurant, and institutional food services, as noted by USDA FAS[1]United States Department of Agriculture, "Food Service - Hotel Restaurant Institutional Annual", www.apps.fas.usda.gov. Local giants, such as Juhayna Food Industries, are reaping the benefits, posting a 42% revenue surge in FY2023 to EGP 16.128 billion. Notably, their concentrates and agri segment saw an impressive 164% year-over-year growth. The company's introduction of a 4-flavor Fruits Yogurt swiftly garnered a 20% market share within just three months, underscoring the market's enthusiasm for innovative flavors.

Clean Label, Natural, and Organic Ingredient Trends

Consumer awareness of food labeling in Egypt remains relatively low, with only 55.6% of consumers reading food labels, yet those who are informed actively avoid products containing artificial additives like MSG (61.9% avoidance rate) and aspartame (68.9% avoidance rate). This creates a significant opportunity for natural flavor solutions, particularly as Egyptian research institutions advance green extraction technologies. A 2024 study by the National Research Centre in Cairo demonstrated that olive oil maceration can effectively extract rosemary essential oils with 70% efficiency compared to traditional hydrodistillation, while supercritical CO2 extraction showed superior antimicrobial properties. Global flavor leader DSM-Firmenich is responding to this trend by investing in natural ingredient capabilities, including a new EUR 30 million production facility in Parma, Italy, scheduled for completion in Q1 2027, which will serve the Middle East market with concentrated powder flavors and advanced encapsulation processes for plant-based products. The trend toward clean labeling is further supported by Egypt's Mediterranean dietary heritage, which emphasizes traditional ingredients like olive oil, herbs, and spices that align with natural flavoring preferences.

Technological Advancements in Flavor Development

Microencapsulation technology is revolutionizing flavor delivery systems in Egypt's food industry, with spray drying, cyclodextrin inclusion, and coacervation techniques enabling heat-stable flavor solutions essential for the country's hot climate and cooking methods. Givaudan has established a Middle East Innovation Hub in Dubai in 2023 and maintains active operations in Egypt, leveraging digital platforms like Customer Foresight and AI-driven formulation tools to accelerate product development. The company's investment in sustainable ingredient technologies, including SunThesis® for citrus oil replacements and TasteCollections Fire for smoky flavor portfolios, addresses supply chain resilience concerns while meeting local taste preferences. DSM-Firmenich's recognition as a "Top 100 Global Innovator" in the 2025 LexisNexis Innovation Momentum Report, managing over 16,000 patents across 2,600 patent families, demonstrates the technological sophistication driving the market. Local companies are also embracing innovation, with Dina Farms operating what it claims is the Middle East's largest herb-drying facility, integrating cultivation, processing, and flavor extraction capabilities across more than 10,000 acres

Localisation Incentives Under Egypt Vision 2030 & "Future" Agri-megaproject

The implementation of Vision 2030 and the "Future of Egypt" megaproject has enhanced Egypt's food processing and ingredient manufacturing capabilities. The project's Phase I encompasses grain silo complexes equipped with analysis, weighing, and pest-control systems, complemented by industrial zones for agro-industrial growth, according to the State Information Service[2]State Information Service, "President El-Sisi Inaugurates 2024 Harvest Season of 'Egypt’s Future' Agricultural Project and Industrial Zone Phase I", www.sis.gov.eg. Through expanded sugar beet cultivation across 780,000 feddans producing over 3 million tonnes annually, Egypt reached sugar self-sufficiency in 2025. Supporting these developments, the Italian government's Mattei Plan allocated EUR 8 billion for investments in agricultural mechanization and sustainable livestock management. Small and medium-scale manufacturers benefit from the MSME Development Law No. 152 (2020), which provides tax incentives, industrial zone allocations, and public procurement quotas.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening NFSA traceability & additive rules | -0.4% | National regulatory enforcement with port-level controls | Short term (≤ 2 years) |

| Fluctuations in raw material prices | -0.6% | Global supply chains with Egypt import dependency | Short term (≤ 2 years) |

| Health concerns over artificial additives | -0.3% | Urban centers with higher consumer awareness | Medium term (2-4 years) |

| Supply chain disruptions impacting ingredient availability and costs | -0.5% | Global supply chains affecting Egypt's import-dependent market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening NFSA Traceability & Additive Rules

Egypt's National Food Safety Authority is implementing regulatory reforms under its 2023-2026 strategy to enhance inspection infrastructure, laboratory testing capabilities, and supply chain monitoring for flavor and enhancer manufacturers. The authority's Decision No. 16/2022 introduced mandatory food traceability requirements in October 2022, establishing new compliance protocols for ingredient suppliers and food processors. In 2024, Egyptian Customs[3]Egyptian Customs Authority, "tax treatment of food additives, spice oils, and flavoring components", www.customs.gov.eg issued multiple circulars regarding the tax treatment of food additives, spice oils, and flavoring components, signaling increased regulatory oversight of ingredient imports. The FSSC 22000 version 6, with its implementation deadline of March 31, 2025, requires food additive manufacturers to establish food safety culture documentation, quality control systems, and enhanced allergen management protocols. These regulations strengthen food safety standards but increase compliance costs and testing requirements, particularly affecting smaller manufacturers without established quality management systems.

Supply Chain Disruptions Impacting Ingredient Availability and Costs

Egypt's heavy dependence on imported raw materials, with approximately 90-95% of food ingredient inputs sourced internationally primarily from India and China, creates significant vulnerability to supply chain disruptions. The Ukraine-Russia conflict has particularly impacted ingredient costs, as Egypt historically sourced 30% of its wheat from Ukraine and 50% from Russia, with the war creating broader inflationary pressures on fertilizers, freight costs, and agricultural yields. Egypt experienced significant port congestion in 2022-2023, with USD 8.5 billion worth of goods stuck at ports due to foreign exchange shortages and letter of credit requirements, demonstrating the system's vulnerability to currency and trade finance disruptions. Food inflation reached 40.5% year-over-year in April 2024, though it has since moderated following government intervention and improved foreign exchange availability. The government's temporary export ban on onions in 2024 due to price spikes from EGP 12 to EGP 35 per kilogram illustrates how quickly supply disruptions can trigger policy responses that affect ingredient availability and pricing for food processors.

Segment Analysis

By Type: Synthetic Dominance Amid Enhancer Innovation

Synthetic flavors hold the largest slice of the Egyptian food flavors and enhancers market, driven by affordability and consistent functional performance that suits price-sensitive processors. They secured 44.86% of Egypt's food flavors and enhancers market size in 2025 and remain essential in mainstream beverages and confectionery lines. Domestic soft-drink concentrate exports exceeding USD 532 million affirm continuing reliance on engineered flavor molecules. Natural formats, however, gain traction in premium yogurts and gourmet snacks as wellness awareness rises.

Flavor enhancers, notably yeast extracts and nucleotide blends, post the fastest expansion at 5.62% CAGR to 2031. Tourism venue chefs seek umami boosters that outperform legacy MSG while aligning with clean-label messaging. Givaudan’s AI-guided enhancer prototypes and DSM-Firmenich’s taste-modulation patents illustrate the pipeline depth feeding this shift. Egypt’s self-sufficiency in sugar and expansion of herb acreage widen local access to carrier substrates, facilitating cost-effective enhancer manufacture within the Egyptian food flavors and enhancers market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Powder Solutions for Heat-Stability

Powder products hold 53.64% of Egypt's food flavors and enhancers market size in 2025, growing at a CAGR of 5.74%. The stability of spray-dried and microencapsulated powders in Egypt's high temperatures ensures optimal flavor preservation during transportation and long-term storage conditions. Food manufacturers, particularly in the snack segment, prefer powder formats due to their precise dosing capabilities, uniform distribution across product batches, and ability to maintain consistent shelf life in varying environmental conditions.

Liquid flavors remain essential in carbonated beverages and dairy products, with significant investments like Al Ahram Beverages' EUR 30 million malt expansion supporting market growth. Recent advancements in emulsion technology enable manufacturers to reduce sugar content in sodas while maintaining desired taste profiles. While DSM-Firmenich's new Parma facility will increase powder production capabilities and intensify market competition, liquid flavors maintain their strong position in applications requiring rapid dissolution and effective color distribution throughout the Egyptian food flavors and enhancers market. The liquid format proves particularly valuable in beverage applications where immediate flavor release and uniform mixing are critical manufacturing requirements.

By Application: Beverages Lead While Ready-to-Eat Foods Accelerate

Beverages hold the largest application share at 28.12% in 2025, driven by Egypt's strong position in soft drink concentrate exports and increased tourism sector demand. The ready-to-eat foods segment shows the highest growth potential with a 6.07% CAGR through 2031, influenced by urbanization and evolving consumer preferences for convenience foods. Juhayna Food Industries demonstrates this market strength, reporting 164% growth in its concentrates and agri segment during FY2023, while maintaining market leadership in spoonable yogurt (64% share) and plain milk (57% share).

The bakery and confectionery segment benefits from Egypt's significant wheat flour export growth, showing a 250% increase from January to May 2024, establishing Egypt as a primary supplier to African and Middle Eastern markets. A major global chocolatier's announcement to establish a factory in Egypt in 2024 reinforces the country's confectionery manufacturing potential. The dairy and frozen foods segment continues to develop, supported by an extension of halal dairy certification requirements to December 31, 2025. This extension maintains market access for international suppliers while domestic manufacturers expand operations. The savory snacks category shows promise, with Givaudan reporting robust growth across the South Asia, Middle East & Africa region in 2024.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Egypt's food flavors and enhancers market leverages the country's position as a regional food processing hub, with processed food exports reaching USD 6.1 billion in 2024, a 21% increase from the previous year. The market concentrates in industrial zones, with Cairo and Alexandria functioning as main manufacturing centers, while the New Delta region develops under the "Future of Egypt" agri-megaproject. In export distribution, Arab countries comprise 54% of Egypt's processed food exports at USD 3.276 billion, with the European Union following at USD 1.168 billion, showing 32% growth.

The tourism sector shapes flavor demand patterns across Red Sea resorts, Cairo, and Luxor, driving requirements for flavor solutions in hotels, restaurants, and institutions. With tourist numbers reaching 14.9 million in 2023 and a target of 30 million by 2028, flavor suppliers face expansion opportunities. The Suez Canal Economic Zone strengthens its position in flavor manufacturing, exemplified by the Egyptian-Indian Flex PET factory's USD 110 million investment in Ain Sokhna.

Givaudan's performance in the South Asia, Middle East & Africa region, showing 20.9% like-for-like growth in 2024, indicates opportunities beyond Egypt's borders. The company operates in Egypt and sources jasmine from the Nile Delta through local suppliers who maintain transparency through plantations and farmer partnerships. Italy's Mattei Plan, focusing on agricultural mechanization and sustainable livestock projects, creates opportunities for expanding raw material availability for flavor extraction across Egypt's agricultural regions.

Competitive Landscape

The Egyptian food flavors and enhancers market shows moderate concentration with a 6 out of 10 rating, where established global companies operate alongside local manufacturers. Global companies Givaudan and DSM-Firmenich are expanding their presence, with Givaudan achieving 20.9% like-for-like growth in the South Asia, Middle East & Africa region in 2024. DSM-Firmenich is developing its production capabilities through a EUR 30 million Parma facility, set for completion in 2027.

These companies maintain their market position through advanced technologies, including AI-driven formulation tools, sustainable ingredients like SunThesis® for citrus alternatives, and extensive patent portfolios spanning 16,000 patents across 2,600 families. Local companies have established strong market positions through vertical integration and regional expertise. Dina Farms operates the Middle East's largest herb-drying facility across 10,000 acres, while Juhayna Food Industries holds a 64% market share in spoonable yogurt.

Market opportunities exist in clean-label solutions, microencapsulation technologies for heat-stable applications, and flavor customization for Egypt's ready-to-eat foods segment, which is growing at a 6.34% CAGR. The National Food Safety Authority's 2023-2026 modernization strategy has introduced regulatory requirements that create entry barriers for smaller companies while benefiting those with established quality management systems and traceability capabilities.

Egypt Food Flavor And Enhancer Industry Leaders

-

International Flavors & Fragrances Inc.

-

Archer Daniels Midland Company

-

DSM-Firmenich

-

Givaudan SA

-

Symrise AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2024: Agrumaria Reggina expanded its production facility in Egypt. The facility has an area of 24,000 sq. Ft and is equipped with JBT Technology, designed to enable Agrumaria Reggina to produce a diverse range of citrus products, including flavors and oils.

- August 2023: Ofi expanded its new herb processing facility in Beni-Suef, Egypt, enhancing its operations across the sector, including snacks. The new ofi facility is expected to process 3,000 metric tons (MT) of herbs every year (basil, fennel, marjoram, parsley, and dill) sourced directly from local farmers

Egypt Food Flavor And Enhancer Market Report Scope

The Egypt food flavor and enhancer market is segmented by type into food flavors such that natural, synthetic, and natural identical flavors and enhancers. Moreover by end-user into dairy products, bakery, confectionery, processed food, beverage, and others.

By Type

| Natural Flavors |

| Synthetic Flavor |

| Nature-Identical Flavors |

| Flavor Enhancers |

By Form

| Liquid |

| Powder |

By Application

| Beverages |

| Bakery and Confectionery |

| Dairy and Frozen Foods |

| Ready to Eat Foods |

| Savory Snacks |

| Others |

| By Type | Natural Flavors |

| Synthetic Flavor | |

| Nature-Identical Flavors | |

| Flavor Enhancers | |

| By Form | Liquid |

| Powder | |

| By Application | Beverages |

| Bakery and Confectionery | |

| Dairy and Frozen Foods | |

| Ready to Eat Foods | |

| Savory Snacks | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current Egypt Food Flavor and Enhancer Market size?

The Egypt Food Flavor and Enhancer Market is projected to register a CAGR of 5.12% during the forecast period (2026-2031)

Who are the key players in Egypt Food Flavor and Enhancer Market?

Givaudan, International Flavors & Fragrances Inc., Archer Daniels Midland Company, Koninklijke DSM N.V. and DuPont de Nemours, Inc are the major companies operating in the Egypt Food Flavor and Enhancer Market.

What years does this Egypt Food Flavor and Enhancer Market cover?

The report covers the Egypt Food Flavor and Enhancer Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Egypt Food Flavor and Enhancer Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.