Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

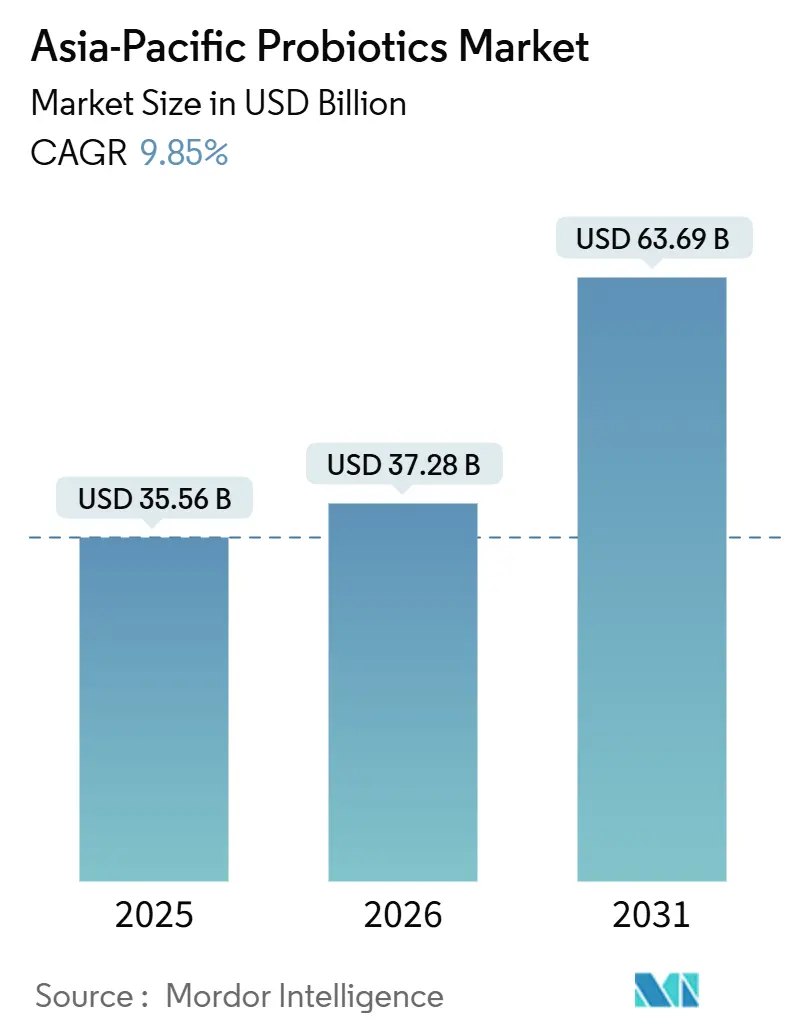

| Base Year Market Size (2025) | USD 35.56 Billion |

| Market Size (2026) | USD 37.28 Billion |

| Market Size (2031) | USD 63.69 Billion |

| Growth Rate (2026 - 2031) | 9.85% CAGR |

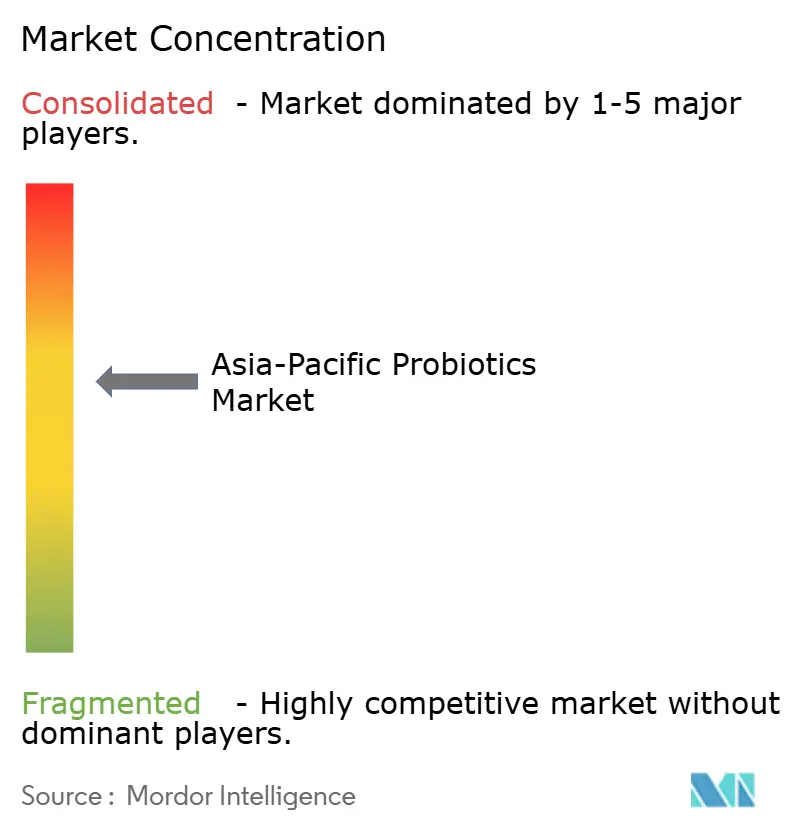

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Probiotics Market Analysis by Mordor Intelligence

The Asia-Pacific probiotics market size is expected to grow from USD 35.56 billion in 2025 to USD 37.28 billion in 2026 and is forecast to reach USD 63.69 billion by 2031 at 9.85% CAGR over 2026-2031. Consumers are shifting from reactive drug regimens toward microbiome-targeted functional nutrition, which elevates demand for clinically validated strains and convenience-oriented delivery formats. Multinational ingredient suppliers continue to license patented organisms to regional brands, while local champions expand vertically to secure fermentation and last-mile reach. Online channels integrate telemedicine and microbiome testing, broadening access in vast geographies. Meanwhile, regulatory bodies in Australia, Japan, and China tighten strain-level disclosure rules that favor companies with strong research pipelines and quality systems.

Key Report Takeaways

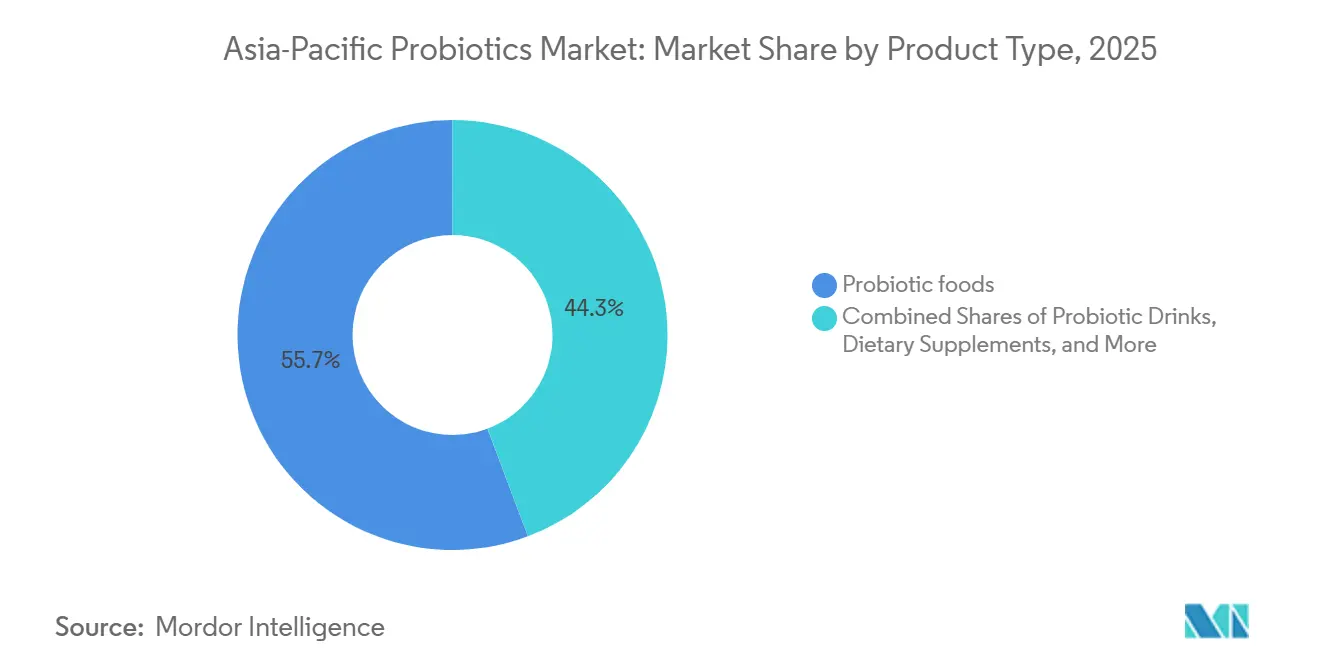

- By Product Type, Probiotic foods led with 55.71% of the Asia-Pacific probiotics market share in 2025, whereas dietary supplements are advancing at a 10.62% CAGR through 2031.

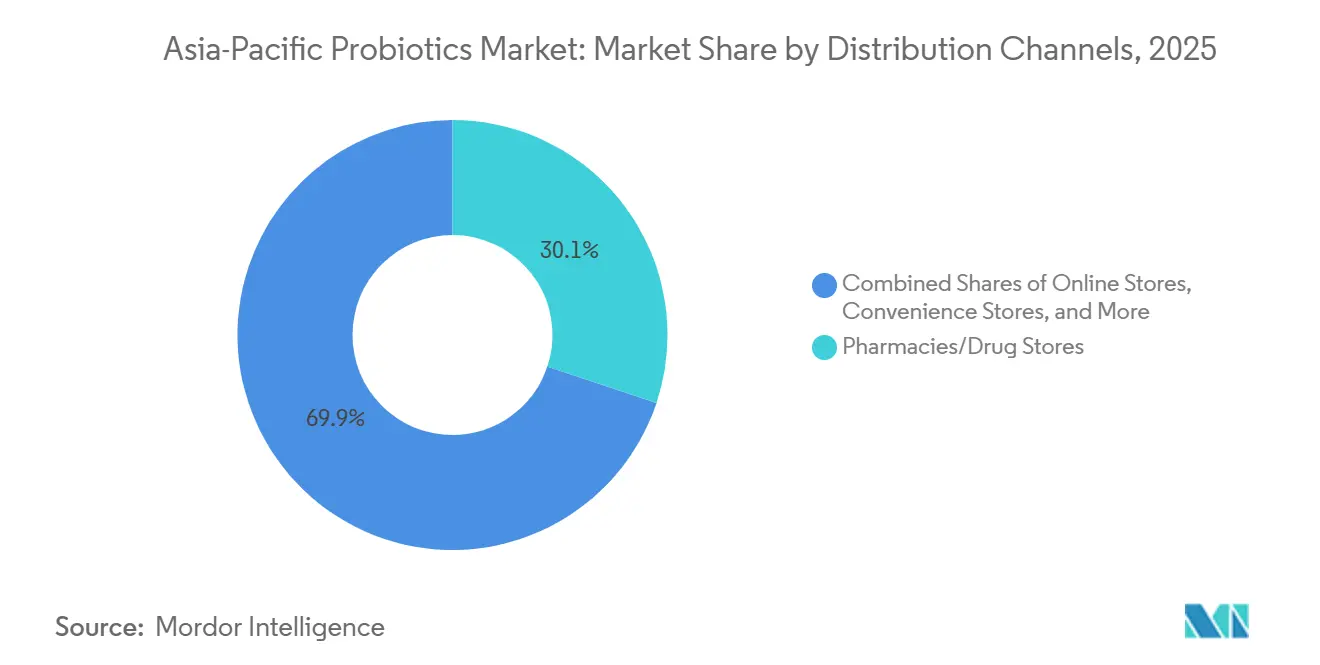

- By Distribution Channel, Pharmacies and drug stores controlled 30.12% of the 2025 value, yet online stores are projected to grow at 10.21% CAGR to 2031.

- By Geography, China contributed 34.15% of regional revenue in 2025, while India is forecast to expand at a 12.89% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Probiotics Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand For Functional Foods And Beverages | +2.3% | China, Japan, South Korea; spillover to Southeast Asia | Medium term (2-4 years) |

| Rising Incidence Of Digestive Disorders Fuels Market Expansion | +2.1% | Pan-Asia, with acute burden in urbanized hubs (Tokyo, Seoul, Shanghai, Mumbai) | Long term (≥4 years) |

| Growing Preference For Natural, Organic, And Non-GMO Probiotics | +1.4% | Australia, Japan, urban India; niche demand in China tier-1 cities | Medium term (2-4 years) |

| Proliferation Of Retail And E-Commerce Distribution Channels | +1.8% | China, India, Southeast Asia; pharmacy chains in Japan and South Korea | Short term (≤2 years) |

| Advancing Research And Clinical Validation | +1.2% | Japan, South Korea, Singapore; research hubs in China and India | Long term (≥4 years) |

| Emerging Microbiome-Based Personalized Nutrition Solutions | +0.9% | Japan, South Korea, Australia; early adoption in China tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Functional Foods and Beverages

In 2025, functional food and beverage categories dominated the consumption of probiotic ingredients. However, a notable shift towards strain-specific formulations is altering the dynamics for suppliers. In July 2024, Morinaga Milk Industry received regulatory approval in China for its Bifidobacterium longum subsp. infantis M63. This move is strategically aimed at infant formula producers keen on mimicking the oligosaccharide metabolizing prowess of breastfed infants' gut microbiota. Also in July 2024, Nestlé kicked off the STARLIT clinical trial in China. The trial focuses on an infant formula enriched with human milk oligosaccharides (specifically 2' fucosyllactose and lacto N neotetraose) and probiotics. This formulation is crafted to meet the premarket efficacy data stipulation set by China's National Health Commission for novel food ingredients. In October 2025, Yakult unveiled Y1000 in Singapore. This fermented milk drink boasts Lacticaseibacillus paracasei strain Shirota, delivering 10 billion CFU per 100 mL. Marketed for its benefits on stress reduction and sleep quality, this marks a departure from Yakult's traditional focus on digestive health, aligning with the heightened emphasis on mental wellness in the post-pandemic landscape. Kirin Holdings, in 2025, revealed plans for its plasma lactic acid bacteria, Lactococcus lactis strain Plasma. Set to debut in Taiwan in 2025, the brand eyes expansions into Australia and Southeast Asia by 2027, bolstered by immune modulation claims backed by over 30 peer-reviewed studies.

Rising Incidence of Digestive Disorders Fuels Market Expansion

By 2024, the prevalence of irritable bowel syndrome (IBS) stood at 16.7% in Japan, 13% in China, and 12.9% in South Korea. However, less than 30% of these patients were administered probiotics as a primary treatment. This notable treatment gap has caught the attention of pharmaceutical and nutraceutical companies, prompting them to initiate physician education programs. In 2024, Changi General Hospital in Singapore kicked off a clinical trial focusing on multi-strain probiotics for post-infectious IBS. This condition, prevalent in 10 to 15% of travelers returning from Southeast Asia, an area known for endemic enteric pathogen exposure, has become a focal point for the hospital. Meanwhile, the DIVINE trial in Indonesia, backed by DSM Firmenich, investigated the effects of Bifidobacterium lactis HN019 on constipation-predominant IBS. After 4 weeks, results showcased a 40% uptick in bowel movement frequency compared to the placebo group. Such compelling evidence is influencing insurers in Japan and South Korea to consider reimbursing probiotic supplements for patients diagnosed with IBS. This policy shift, driven by the Ministry of Health, Labour and Welfare, Japan, has the potential to generate an additional USD 200 to 300 million in annual demand by 2028[1]Source: Ministry of Health, Labor and Welfare, "Foods with Function Claims: Heat-Killed Probiotics Approval." mhlw.go.jp.

Growing Preference for Natural, Organic, and Non-GMO Probiotics

In Australia and Japan, consumers are increasingly demanding organic and non-GMO certifications, emphasizing the importance of ingredient sourcing and manufacturing transparency. In 2024, Food Standards Australia New Zealand mandated that all probiotic products must clearly label strain designations[2]Source: Food Standards Australia New Zealand, “Probiotic Labeling Requirements,” foodstandards.gov.au. This regulation poses challenges for suppliers who typically use the broader "Lactobacillus blend" terminology. Meanwhile, Japan's Ministry of Health, Labour and Welfare made a notable move in 2024 by adding heat-killed probiotics, or postbiotics, to its Foods with Function Claims registry. This change allows brands to sidestep cold chain expenses while still promoting immune modulation benefits. Notably, this regulatory shift is drawing interest from China and South Korea, who are contemplating its adoption. In a significant investment, BY-HEALTH, the leading dietary supplement manufacturer in China, allocated RMB 500 million (approximately USD 70 million) in 2024. Their goal is to cultivate proprietary strains that not only steer clear of genetically modified organism (GMO) issues but also meet the organic certification criteria set by China's GB/T 19630 standard. Additionally, Yili Group, between 2024 and early 2026, secured 28 patents related to the production of human milk oligosaccharides. This strategic move positions Yili Group to offer non-GMO prebiotics, enhancing both infant formulas and adult dietary supplements with complementary probiotic formulations.

Proliferation of Retail and E-Commerce Distribution Channels

Pharmacy chains and online platforms are merging into omnichannel ecosystems, offering bundled services such as diagnostic testing, personalized recommendations, and subscription fulfillment. In 2024, Watsons Philippines expanded its footprint to 1,166 stores, adding 80 new locations and launching 400 community pharmacies. These pharmacies not only stock refrigerated probiotics but also provide consultations to help customers select the right strains. As of 2024, Guardian Malaysia operated 554 stores, commanding roughly 24% of the health and beauty market. In March 2025, they rolled out an AI driven loyalty program that tailors probiotic product recommendations based on individual purchase histories and self-reported health objectives. China's e-commerce platforms, during 2024 to 2025, saw a 6% year over year uptick in probiotic supplement sales. Notably, JD.com and Alibaba Health have begun offering telemedicine consultations, enabling them to prescribe specific strains for gastrointestinal issues. In South Korea, online sales of health functional foods experienced an 18% boost in 2024. This surge was largely attributed to direct to consumer brands that sidestep traditional pharmacy markups, enticing customers with subscription discounts ranging from 15% to 20%.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Research And Development Costs | -0.8% | Japan, South Korea, Australia; emerging in China tier-1 research hubs | Long term (≥4 years) |

| Intense Competition From Alternative Wellness Products | -0.6% | Pan-Asia, particularly urban centers with diverse supplement options | Medium term (2-4 years) |

| Limited Consumer Awareness In Certain Regions | -0.5% | Southeast Asia (Indonesia, Thailand, Vietnam), rural India, rural China | Short term (≤2 years) |

| Stringent Regulatory Hurdles And Restricted Product Claims | -0.7% | Australia, New Zealand, Japan; tightening in China and India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Elevated Research and Development Costs

Established multinationals, with their deeper pockets, find it easier to navigate the capital-intensive landscape of strain characterization, stability testing, and clinical trials. Bringing a novel probiotic strain from the lab to regulatory approval demands an investment of USD 5 to 10 million and a commitment of 3 to 5 years. This lengthy and costly process often deters investments in niche areas like oral health or dermatology. In Japan, the Ministry of Health, Labor and Welfare has set a high bar for food submissions, requiring human clinical trials with participant numbers exceeding 50. This poses a challenge for smaller formulators, who often rely on contract research organizations for support. Meanwhile, in 2024, China's National Health Commission mandated whole genome sequencing for novel probiotic strains. This step, aimed at screening out antibiotic resistance genes and virulence factors, adds an extra USD 50,000 to 100,000 to pre-market costs. Down under in Australia, the Therapeutic Goods Administration made waves in 2024 by reclassifying high-dose probiotics as complementary medicines. This shift brought about stringent Good Manufacturing Practice audits and pharmacovigilance reporting, leading to a 20 to 30% hike in compliance overheads.

Intense Competition from Alternative Wellness Products

In the realm of functional nutrition, probiotics vie for consumer attention alongside prebiotics, postbiotics, digestive enzymes, herbal adaptogens, and fermented foods. Postbiotics, which consist of heat-killed bacterial cells and their metabolites, gained momentum in Japan and South Korea during 2024 and 2025. Their appeal lies in their ability to sidestep cold chain logistics and boast an extended shelf life. However, it is worth noting that the clinical evidence supporting their efficacy is not as robust as that for live probiotics. Meanwhile, fermented staples like kimchi, miso, and natto offer a diverse range of microbes at a price point that is more accessible than supplements. This affordability strikes a chord in budget-conscious markets such as Indonesia and Vietnam. In India and China, herbal digestive aids like ginger, turmeric, and peppermint oil hold sway in traditional medicine circles. Here, practitioners of Ayurvedic and Traditional Chinese Medicine often endorse these botanical remedies before turning to Western probiotics.

Segment Analysis

By Product Type: Dietary Supplements Outpace Traditional Formats

Dietary supplements are projected to grow at a CAGR of 10.62% through 2031, driven by urban professionals favoring convenience and targeted benefits over traditional dairy formats. In 2025, probiotic foods commanded a 55.71% market share, bolstered by yogurt's widespread popularity in Japan and South Korea, where annual per capita consumption surpassed 15 kg. However, growth is slowing as consumers pivot to capsules, which offer higher CFU counts without the drawbacks of added sugars or refrigeration. In 2025, probiotic drinks, divided into dairy and non-dairy categories, garnered substantial market value. Non-dairy variants, including coconut, almond, and oat-based options, are witnessing a surge in Australia and urban India. This growth is largely attributed to the high prevalence of lactose intolerance (60 to 70 percent in East Asia) and the rising trend of vegan diets. While animal feed and nutrition represent a smaller segment, they are rapidly gaining traction in aquaculture-heavy nations like Vietnam, Thailand, and Indonesia. Here, strains like Bacillus subtilis and Lactobacillus are supplanting traditional antibiotic growth promoters in shrimp and tilapia farming, leading to an 8 to 12 percent boost in feed conversion ratios and a decrease in pathogen loads, as noted by FAO Fisheries and Aquaculture.

Yogurt continues to dominate the probiotic food landscape, but it is grappling with margin pressures from private label rivals and a growing consumer disinterest in single-strain offerings. The 2024 to 2025 period saw infant formulas and baby foods carve out a lucrative niche. Notably, Morinaga's Bifidobacterium longum subsp. Infantis M63 received the green light in China, allowing manufacturers to charge a 20 to 30 percent premium over standard offerings. While bakery items, breakfast cereals, snacks, and confections accounted for under 5 percent of probiotic ingredient usage in 2025, limited by thermal processes that deactivate live cultures, innovations are on the horizon. Heat-stable postbiotic formats are beginning to change the game. In 2024, Japan's Foods with Function Claims registry approved heat-killed Lactobacillus strains for baked goods, signaling a potential boom in this segment. Regulatory clarity in South Korea and Japan is proving advantageous for dietary supplements. Their health functional food frameworks allow claims like "helps maintain healthy cholesterol levels," a privilege not extended to conventional foods. This regulatory edge not only bolsters compliance but also paves the way for premium pricing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channels: Online Platforms Disrupt Pharmacy Dominance

Online stores, projected to grow at a 10.21% CAGR through 2031, are set to erode the 30.12% market share that pharmacies and drug stores held in 2025. This shift comes as e-commerce platforms increasingly integrate telemedicine consultations, subscription models, and direct-to-consumer microbiome testing. While pharmacies enjoy structural advantages in Japan and South Korea, where consumers trust pharmacist recommendations and prefer inspecting refrigerated products before purchase, China's JD Health and Alibaba Health made significant inroads. They captured 15 to 18% of probiotic sales in 2025 by offering 24-hour delivery and AI-driven product matching based on symptom inputs. Supermarkets and hypermarkets, leveraging ambient stable probiotic formats that bypass cold chain constraints, accounted for a significant market share. This strategy resonates in Southeast Asia, where modern retail penetration lags behind Northeast Asia. In Japan and South Korea, convenience and grocery stores, though fragmented, serve as impulse purchase channels for single-serve probiotic drinks. Notably, Yakult's direct sales model (Yakult Ladies) delivered 8 million bottles daily in 2024, bolstering brand loyalty through personal relationships and home delivery.

In 2024, Watsons Philippines expanded its footprint to 1,166 stores, adding 80 new locations. They also launched 400 community pharmacies, stocking refrigerated probiotics and offering pharmacist consultations. This hybrid model seamlessly blends retail convenience with professional guidance. Meanwhile, Guardian Malaysia, operating 554 stores as of 2024 and capturing roughly 24% of the health and beauty market, rolled out an AI-driven loyalty program in March 2025. This program recommends probiotic products based on individual purchase history and self-reported health goals. Online platforms are increasingly bundling probiotics with complementary products to boost average order value. This tactic proves challenging for brick-and-mortar retailers, who grapple with shelf space constraints. The "others" category, encompassing direct sales, multi-level marketing, and institutional channels like hospitals and clinics, accounted for under 10% of distribution in 2025. However, it is witnessing growth in India where Amway and Herbalife leverage network marketing models to penetrate tier 2 and tier 3 cities, areas often overlooked by modern retail.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, China held a dominant 34.15% share of the Asia-Pacific probiotic revenue. However, as regulatory measures tighten and tier-1 cities become saturated, brands are shifting focus to tier-2 and tier-3 urban centers. Here, per capita consumption lags at under 2 servings weekly. A new mandate from the National Health Commission in 2024, requiring whole-genome sequencing for novel strains, has added an extra USD 50,000-100,000 to pre-market costs per strain. This move has inadvertently favored established players like BY-HEALTH and Yili Group over smaller formulators. Meanwhile, India's probiotic market is on a rapid ascent, boasting a 12.89% CAGR through 2031. This surge, the fastest in the region, is largely attributed to a 2024 clarification from the Food Safety and Standards Authority. They permitted health claims for probiotics, provided CFU thresholds exceed 10^6 per serving at shelf life end. This regulatory nod has given compliant brands a marketing edge.

Japan's probiotic landscape is evolving, with a focus on postbiotics and paraprobiotics. The Ministry of Health, Labour and Welfare has conferred "Foods with Function Claims" status to heat-killed Lactobacillus strains. This designation not only sidesteps cold-chain logistics but also extends shelf life to an impressive 18-24 months. In a strategic pivot, Yakult unveiled its Y1000 fermented milk drink in Singapore this October. Infused with the Lacticaseibacillus paracasei strain Shirota at a potent 10 billion CFU per 100 mL, Y1000 is marketed for its stress-reducing and sleep-enhancing benefits. This marks a departure from Yakult's traditional focus on digestive health, aligning seamlessly with the growing emphasis on mental wellness. While Australia and New Zealand witness robust annual growth, they're also grappling with a 2024 mandate from Food Standards Australia New Zealand. This rule, requiring strain-level disclosure on labels, poses challenges for suppliers accustomed to generic "Lactobacillus blend" descriptors, pushing some towards reformulation or even market exit. In Southeast Asia, Indonesia, Thailand, and Malaysia together account for 12-15% of the regional revenue.

Yet, with per capita consumption under 0.5 servings weekly, growth is stunted. Challenges arise from a limited cold-chain infrastructure, a fragmented retail landscape, and a general lack of consumer awareness about probiotic benefits beyond yogurt. South Korea's Ministry of Food and Drug Safety greenlit 23 new probiotic ingredients for health functional foods between 2024 and early 2026[3]Source: Food Safety and Standards Authority of India, “CFU Threshold Guidelines,” fssai.gov.in. Among these are multi-strain consortia aimed at enhancing cognitive function through the gut-brain axis. This regulatory pathway offers claims related to disease-risk reduction, a privilege not commonly found in many other markets. Meanwhile, the broader Asia-Pacific region, including nations like Vietnam and the Philippines, is witnessing growth fueled by rising disposable incomes, urbanization, and the expansion of pharmacy chains. However, a significant hurdle remains: regulatory fragmentation. Each country has its unique approval processes, leading to delays in product launches by 12-18 months and escalating compliance costs.

Competitive Landscape

In the Asia Pacific probiotics market, multinational corporations compete alongside innovative regional players and emerging biotech firms. Companies with strong clinical validation, expertise in navigating regulatory frameworks across regions, and extensive distribution networks—spanning both traditional and digital channels—hold a competitive edge. The market is shifting its focus toward strain-specific differentiation rather than generic probiotic blends. Leading firms are prioritizing investments in proprietary research to develop targeted therapeutic solutions for digestive health, immune support, and growing wellness categories.

Technological innovations are driving competitive advantages, with companies adopting advanced manufacturing techniques, microencapsulation technologies, and personalized nutrition platforms that align specific probiotic strains with individual consumer needs. Recent collaborations, such as Evonik's joint ventures, highlight a trend toward industry consolidation by combining biotechnology expertise with regional manufacturing capabilities.

Firms proficient in navigating the complex regulatory environments of the Asia Pacific region not only ensure compliance but also achieve quicker market entry and broader geographic expansion. The competitive landscape favors companies that effectively integrate scientific innovation with commercial execution, particularly those that transform clinical research into accessible consumer products offering measurable health benefits while meeting stringent regulatory standards across various markets.

Asia-Pacific Probiotics Industry Leaders

-

PepsiCo Inc.

-

Danone SA

-

Yakult Honsha Co. Ltd

-

Nestle SA

-

Bio-k Plus International

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: PepsiCo has announced the launch of its first-ever Pepsi® Prebiotic Cola in the traditional cola category, introducing a functional cola beverage containing 3 grams of prebiotic fiber, 5 grams of cane sugar, and only 30 calories per can.

- June 2025: Bioma Probiotics has officially launched a novel probiotic product aimed at revolutionizing gut health and consumer wellness in the functional foods. The supplement targets digestive health, immune support, and mental clarity through microbiome balance.

- July 2024: Yakult Danone India expanded its product portfolio by launching Yakult Light Mango Flavour. The product offers the same signature probiotic strain, Lactobacillus casei Shirota, in a mango-flavored, reduced-sugar beverage tailored to Indian consumer preferences.

- March 2024: TrueNorth launched innovative probiotic solutions under the brand ‘Sensibiotics’ targeted at sensitive gut and feminine health. These supplements were developed to provide targeted, preventive care for modern health concerns, marking a significant expansion in TrueNorth’s portfolio for specialized probiotic products.

Asia-Pacific Probiotics Market Report Scope

Probiotics are a combination of beneficial bacteria and yeasts that help humans and animals maintain intestinal microbial balance.

The Asia-Pacific probiotics market is segmented by product type into probiotic foods, probiotic drinks, dietary supplements, and animal feed and nutrition. Probiotic foods are further segmented into yogurt, bakery and breakfast cereals, infant formula and baby foods, snacks and confectionery, and others. Probiotic drinks are further segmented into dairy-based and non-dairy-based products. By distribution channels, the market is segmented into supermarkets/hypermarkets, pharmacies and drug stores, convenience/grocery stores, online stores, and others. By geography, the market is segmented into China, India, Japan, Australia, Indonesia, Thailand, Malaysia, South Korea, and the rest of the Asia-Pacific. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Probiotic Foods | Yogurt |

| Bakery and Breakfast Cereals | |

| Infant Formula and Baby Foods | |

| Snacks and Confectionery | |

| Others | |

| Probiotic Drinks | Dairy-based |

| Non-dairy | |

| Dietary Supplements | |

| Animal Feed and Nutrition |

By Distribution Channels

| Supermarket/Hypermarkets |

| Pharmacies and Drug Stores |

| Convinience/Grocery Stores |

| Online Stores |

| Others |

By Geography

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| Thailand |

| Malaysia |

| South Korea |

| Rest of Asia -Pacific |

| By Product Type | Probiotic Foods | Yogurt |

| Bakery and Breakfast Cereals | ||

| Infant Formula and Baby Foods | ||

| Snacks and Confectionery | ||

| Others | ||

| Probiotic Drinks | Dairy-based | |

| Non-dairy | ||

| Dietary Supplements | ||

| Animal Feed and Nutrition | ||

| By Distribution Channels | Supermarket/Hypermarkets | |

| Pharmacies and Drug Stores | ||

| Convinience/Grocery Stores | ||

| Online Stores | ||

| Others | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| South Korea | ||

| Rest of Asia -Pacific | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will the Asia-Pacific probiotics market be by 2031?

It is projected to reach USD 63.69 billion by 2031, expanding at a 9.85% CAGR from 2026.

Which segment is growing fastest within the region?

Dietary supplements are advancing at a 10.62% CAGR, outpacing foods and drinks.

Why is India recording the highest growth?

FSSAI’s 2024 CFU-threshold clarification unlocked clear probiotic health claims, stimulating launches and accelerating adoption at a 12.89% CAGR.

How are online platforms influencing sales?

E-commerce integrates telemedicine, AI product matching, and same-day delivery, pushing online channels to a 10.21% CAGR through 2031.