Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

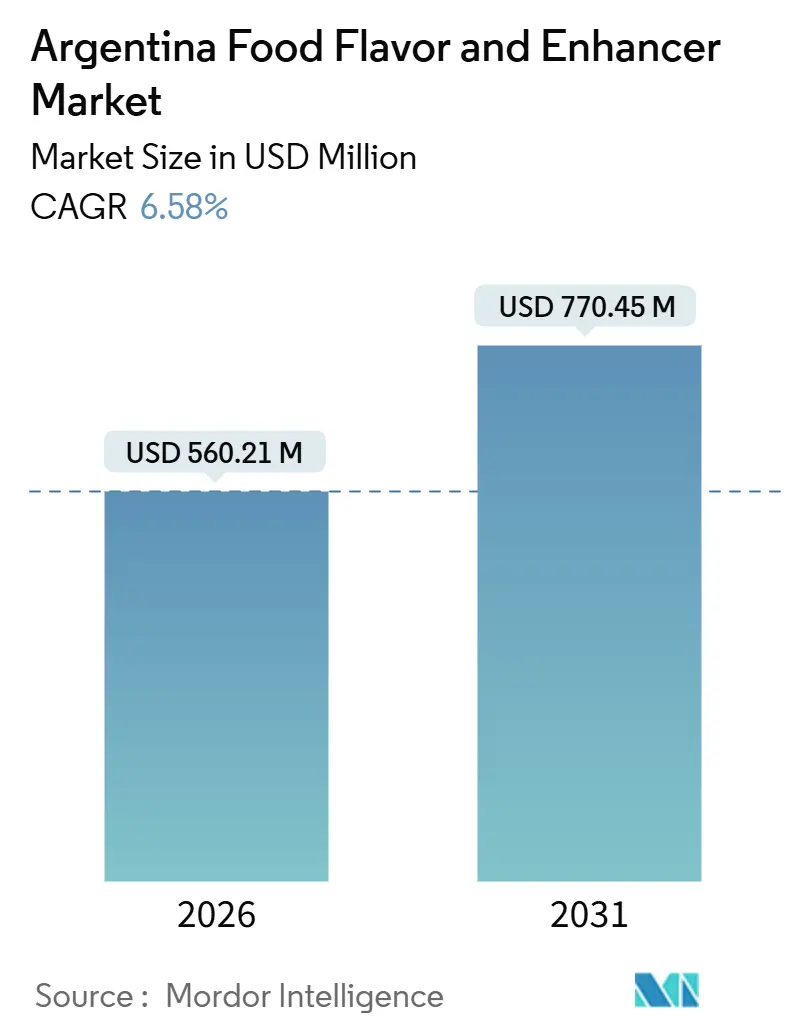

| Market Size (2026) | USD 560.21 Million |

| Market Size (2031) | USD 770.45 Million |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Food Flavor And Enhancer Market Analysis by Mordor Intelligence

The Argentina food flavor and enhancer market is projected to reach USD 560.21 billion by 2026 and USD 770.45 billion by 2031, with a CAGR of 6.58%. The availability of natural raw materials, the implementation of front-of-pack warning labels, and increasing urbanization are encouraging processors to use botanical extracts instead of artificial additives. Lemon essential oil, which represents 37% of global exports, plays a key role in the domestic supply chain for clean-label initiatives, as it aligns with consumer demand for natural and sustainable ingredients. Additionally, Argentina's 4 million hectares of organic certified farmland provide traceability assurances for markets in Europe and North America, ensuring compliance with stringent import regulations and quality standards. Research and development efforts in yeast extracts, nano-encapsulation, and fermentation-derived umami compounds enable sodium reductions of 30-40% without compromising taste. These innovations support premium positioning in beverages, dairy products, and savory snacks, catering to health-conscious consumers seeking reduced-sodium options without sacrificing flavor.

Key Report Takeaways

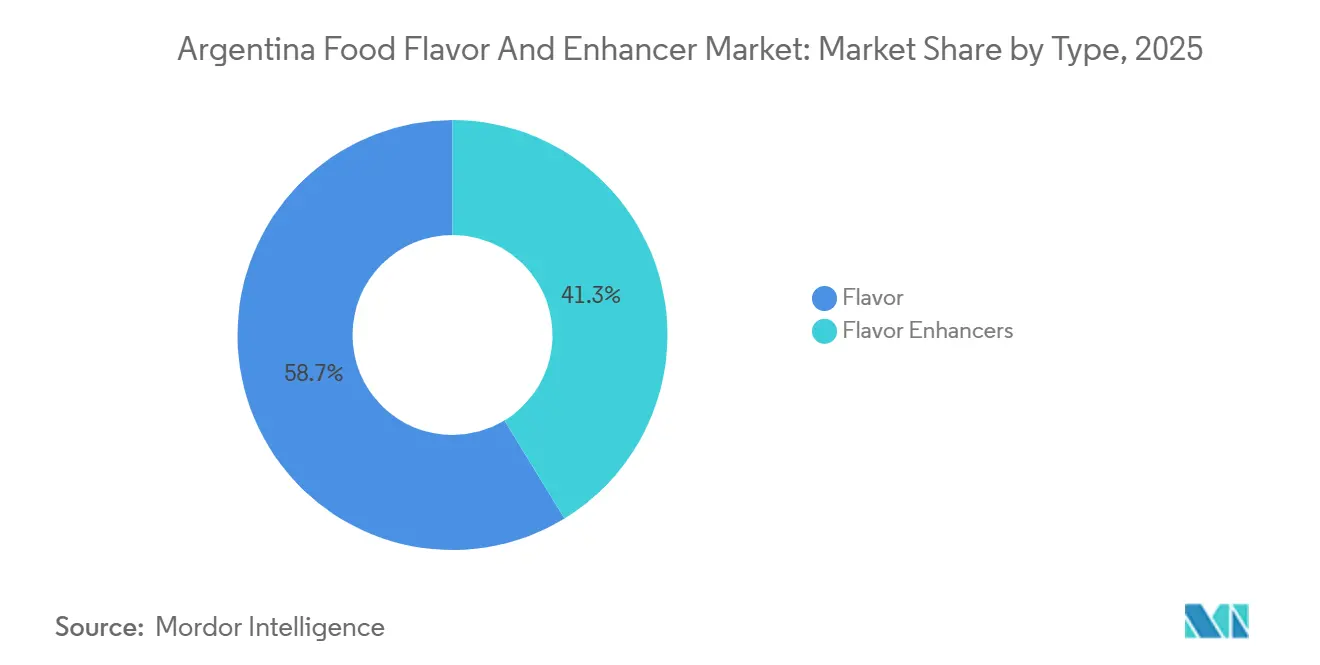

- By type, the flavor segment led with 58.71% Argentina food flavor and enhancer market share in 2025, while the flavor enhancer segment is advancing at a 6.95% CAGR through 2031.

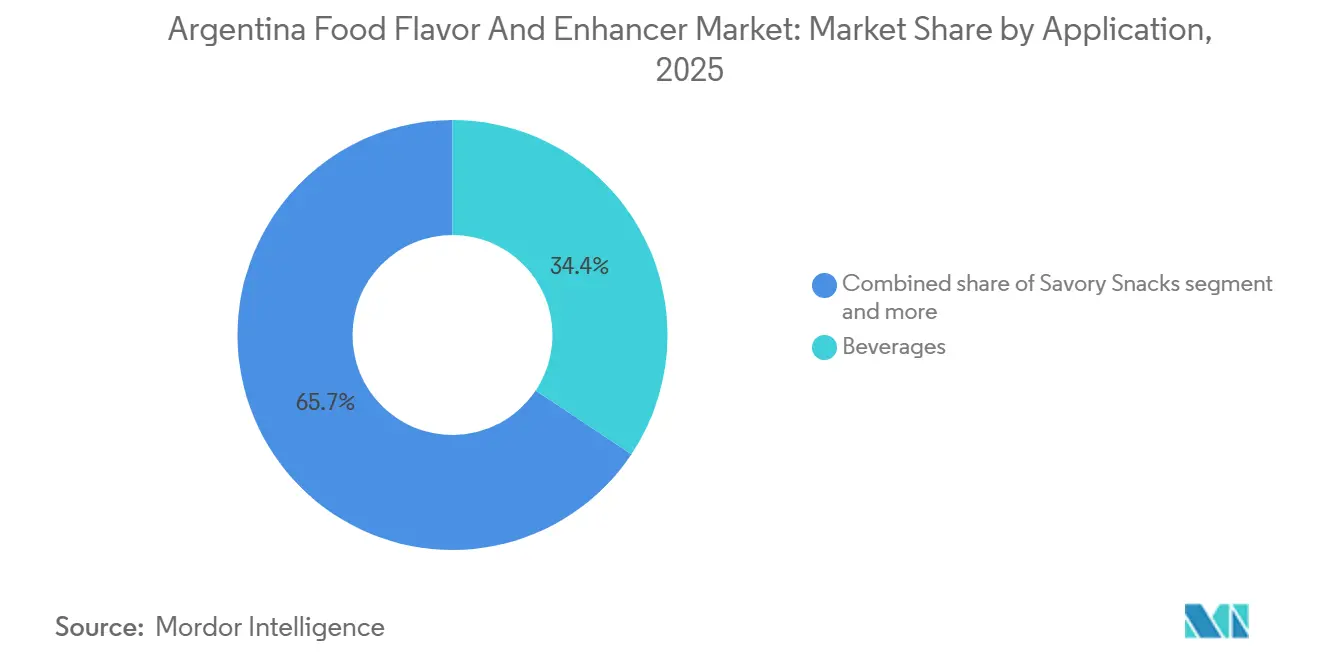

- By application, beverages captured 34.35% revenue share in 2025; savory snacks show the fastest 7.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Food Flavor And Enhancer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of processed and convenience foods | +1.2% | National, with concentration in Greater Buenos Aires, Córdoba, and Rosario industrial corridors | Medium term (2-4 years) |

| Rising demand for clean-label natural flavorings | +1.5% | National, accelerated in export-oriented dairy and confectionery clusters (Santa Fe, Entre Ríos) | Long term (≥ 4 years) |

| Pivot towards plant-based flavor enhancer ingredients | +0.9% | Urban centers (Buenos Aires, Mendoza, Tucumán), spillover to provincial markets | Medium term (2-4 years) |

| Multinational research and development investments and advanced delivery tech | +1.1% | National, with research and development hubs in Buenos Aires and technology transfer from Brazil/Mexico facilities | Long term (≥ 4 years) |

| Government support for local food processing and value-added agriculture | +0.8% | Northwest provinces (Tucumán, Salta, Jujuy) for aromatic crops; Pampa region for grain-based ingredients | Medium term (2-4 years) |

| Robust domestic processed meat and savory food culture | +1.0% | National, strongest in Buenos Aires, Santa Fe, and Patagonia beef-processing zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of processed and convenience foods

Argentina is among the most urbanized countries in Latin America, with urbanization having a significant impact on consumer behavior. The prevalence of busier lifestyles, smaller household sizes, and an increasing dependence on packaged and ready-to-eat meals are notable trends. Urban residents are dedicating less time to preparing traditional meals, leading to a growing demand for convenience-focused food products. This trend has directly increased the demand for flavors and flavor enhancers, which play a crucial role in maintaining consistency and appeal in processed foods. According to the World Bank, approximately 92.58% of Argentina's population lived in urban areas in 2024 [1]Source: World Bank Organization, "Urban population (% of total population) - Argentina", worldbank.org. Yeast extract has become a key ingredient in premium convenience foods, particularly those marketed as “MSG-free.” It is extensively used to enhance the flavor profiles of ready-to-eat soups, sauces, and seasoning sachets, aligning with urban consumers’ preference for clean-label, flavorful products. For instance, Nissin Cup Noodles Beef, which contains yeast extract, is readily available through online platforms in Argentina. These products rely heavily on flavors and flavor enhancers to provide quick and consistent taste experiences.

Rising demand for clean-label natural flavorings

In Argentina, there is a growing consumer preference for products made with natural and minimally processed ingredients, reflecting an increased emphasis on health, wellness, and transparency. This trend is encouraging food manufacturers to use clean-label natural flavorings that provide bold and authentic tastes without artificial additives. These flavorings are particularly in demand for ready-to-eat meals, snacks, and convenience foods. Ingredients such as yeast extracts, botanical extracts, and plant-based umami enhancers are becoming more popular due to their ability to deliver flavor while supporting clean-label claims. This shift in consumer demand is driving innovation and portfolio expansion within the food flavor and enhancer market. Both local and multinational flavor companies are developing solutions that offer taste consistency, versatility, and natural attributes to meet the needs of urban, health-conscious consumers. Clean-label natural flavorings are increasingly regarded as premium differentiators, influencing product development strategies and positioning the market for continued growth.

Pivot towards plant-based flavor enhancer ingredients

The Argentine food flavor and enhancer market is being significantly impacted by the rapid expansion of the plant-based food industry, which is driving demand for enhancers that improve and complement plant-derived flavors. According to the Association of Plant-Based Producers, comprising 1,200 companies, 130 of these companies reported growth of at least 35% in 2021. Additionally, a 45% growth is projected within two years, with investments in the sector expected to increase from USD 2 billion to USD 7 billion by 2024 [2]Source: Vegconomist, "Plant-Based Movement Steadily Gaining Momentum in Beef-Loving Argentina", vegconomist.com. This underscores the strong potential for natural ingredients, such as yeast extract, in plant-based and health-oriented product lines. The growth of this sector is encouraging food manufacturers to adopt enhancers that address sensory challenges commonly associated with plant-based products, such as blandness or undesirable off-notes, while aligning with clean-label and sustainability requirements. Ingredients like yeast extracts, botanical extracts, and fermentation-derived taste modulators are becoming critical for product developers, enabling the creation of consistent, savory, and natural flavors in meat alternatives, dairy-free beverages, soups, and sauces. This trend positions the market for continued growth.

Multinational research and development investments and advanced delivery tech

The Argentine food flavor and enhancer market is experiencing growth driven by substantial investments from multinational companies in research, development, and advanced flavor delivery technologies. Global flavor manufacturers are utilizing their research and development capabilities to develop solutions that enhance taste consistency, stability, and sensory appeal across various products, including ready-to-eat meals, plant-based alternatives, and beverages. Advanced delivery systems, such as encapsulation, controlled-release technologies, and flavor masking platforms, help manufacturers preserve authentic flavor profiles, even in complex or processed formulations. These advancements support local food producers in meeting consumer demand for high-quality, natural, and clean-label products, while addressing formulation challenges, increasing product variety, and fostering innovation in Argentina’s convenience and processed food segments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over MSG and sodium-based enhancers | -0.7% | National, with heightened sensitivity in urban, higher-income segments (Buenos Aires, Córdoba) | Short term (≤ 2 years) |

| Front-of-pack warning law tightening additive labelling | -0.9% | National, compliance mandatory for all packaged foods sold in Argentina | Medium term (2-4 years) |

| Rising concerns over synthetic flavors | -0.5% | Urban centers, driven by social-media campaigns and consumer advocacy groups | Medium term (2-4 years) |

| High development costs for functional or clean-label/natural flavor systems | -0.6% | National, disproportionately affects small and medium-sized processors with limited research and development budgets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over MSG and sodium-based enhancers

Health concerns associated with MSG and sodium-based flavor enhancers are becoming a notable restraint for Argentina's food flavor and enhancer market. In 2024, the prevalence of hypertension among adults aged 30–79 is projected to reach 51%, significantly higher than the global average of 34% [3]Source: World Health Organization, "Argentina Hypertension profile", who.int. This alarming statistic has heightened consumer awareness regarding the adverse effects of high sodium intake on cardiovascular health, prompting a shift in dietary preferences. Urban populations and health-conscious consumers are increasingly seeking products that provide flavor without compromising health, such as low-sodium alternatives, natural umami ingredients, or yeast extracts. These alternatives not only cater to health-conscious demands but also align with the growing trend of clean-label products, which emphasize natural and minimally processed ingredients. This shift has placed significant pressure on manufacturers to reformulate processed foods, ready-to-eat meals, and convenience products. Reformulation efforts require a delicate balance between maintaining flavor intensity and meeting health-oriented claims, often involving the adoption of innovative ingredients and production techniques. These adjustments can increase production complexity, elevate costs, and reduce reliance on traditional MSG- or sodium-based enhancers, presenting both challenges and opportunities for market players.

Front-of-pack warning law tightening additive labelling

The implementation of stricter front-of-pack warning regulations in Argentina is a significant restraint for the food flavor and enhancer market. These regulations mandate manufacturers to clearly label additives, including flavor enhancers, which can significantly influence consumer perception and purchasing behavior, particularly among health-conscious and urban consumers. The labeling requirements aim to provide greater transparency, enabling consumers to make informed choices about the products they purchase. As a result, food producers are under increasing pressure to reformulate products using cleaner-label or natural alternatives to avoid unfavorable labeling. This reformulation process often involves extensive research and development efforts, adding complexity and increasing costs in product development. The regulatory framework restricts the unrestricted use of certain enhancers, promotes transparency, and drives innovation toward natural, plant-based, or low-intensity flavor solutions. However, it also poses challenges for traditional additive-heavy formulations, compelling manufacturers to adapt to evolving consumer preferences and regulatory demands.

Segment Analysis

By Type: Flavors Dominate Amid Regulatory Reformulation

Flavors accounted for 58.71% of the market share in 2025, driven by front-of-pack warning regulations that discourage synthetic additives and promote the use of botanical extracts, which are perceived as "clean" by consumers. Flavor enhancers, while smaller in absolute volume, are projected to grow at a compound annual growth rate (CAGR) of 6.95% through 2031, marking the fastest growth among all type segments. This growth is attributed to the use of yeast extracts and fermentation-derived umami compounds, which enable sodium reduction without compromising taste intensity.

Nature-identical flavors occupy an intermediate position, offering cost benefits compared to natural extracts while avoiding the "artificial" label that deters consumers. These molecules, chemically identical to their botanical counterparts but synthesized in reactors, provide a cost-effective solution for mid-tier brands that cannot absorb the 40-60% cost premium associated with natural alternatives. Synthetic flavors face challenges due to social media campaigns linking ingredients like vanillin and ethyl maltol to petrochemical feedstocks. However, they remain essential in value-tier confectionery and beverages, where cost limitations make natural substitution unfeasible.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Beverages Lead While Savory Snacks Surge

The beverages segment accounted for a 34.35% application share in 2025, driven by the popularity of yerba mate-based drinks, which hold strong cultural significance in various regions. Additionally, reformulated carbonated soft drinks have gained traction as manufacturers aim to avoid front-of-pack sugar warnings, aligning with consumer demand for healthier options. This segment reflects a balance between traditional preferences and modern health-conscious trends, making it a key area of focus for market players. The reformulation efforts in beverages underscore the industry's adaptability to regulatory changes and shifting consumer priorities.

The savory snacks segment is projected to grow at a CAGR of 7.09% through 2031, representing the fastest growth among all applications. This expansion is largely attributed to the increasing consumer preference for portable, high-protein snacks such as extruded chickpea crisps and baked lentil chips. These products require robust flavor stability to withstand thermal processing, highlighting the importance of innovation in flavor delivery systems. Meanwhile, dairy products, including dulce de leche, yogurt, and ice cream, remain a stable mid-tier segment. In this category, natural vanilla and caramel flavors face growing competition from fermentation-derived diacetyl and acetoin, which replicate buttery notes at a lower cost. Noodles, soups, and sauces collectively account for 12-15% of application volume, with chimichurri and salsa criolla driving demand for heat-stable herb extracts capable of withstanding retort sterilization.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Argentina's food flavor and enhancer market demonstrates significant regional disparities. Greater Buenos Aires, Córdoba, and Rosario industrial corridors account for 65-70% of domestic consumption, driven by concentrated food-processing capabilities and higher per-capita incomes that support demand for premium and clean-label products. In contrast, the northwest provinces, Tucumán, Salta, and Jujuy, serve as raw-material production hubs, contributing 80% of the nation's paprika, cumin, and chili. Despite an 80-year cultivation heritage, local value addition remains minimal, as most aromatic crops are exported in bulk for processing in Buenos Aires or abroad.

Mendoza and San Juan provinces lead in oregano cultivation, with ongoing initiatives to obtain geographic indication (GI) status. This designation could enable price premiums of 15-25% in European markets by linking the region's terroir to flavor intensity and volatile-oil composition. In Patagonia, beef-processing zones in Río Negro and Neuquén drive demand for asado-seasoned convenience meats. Flavor systems in this region must endure freeze-thaw cycles and extended cold storage without oxidative degradation.

The coastal and riverine provinces, particularly Santa Fe and Entre Ríos, are key centers for grain and vegetable processing, including soy, corn, and tomato-based products. These ingredients are essential for sauces, soups, and snacks, fueling demand for flavor enhancers that ensure taste consistency in high-volume processed foods. Additionally, there is growing interest in natural and clean-label solutions to meet the preferences of urban consumers across the country.

Competitive Landscape

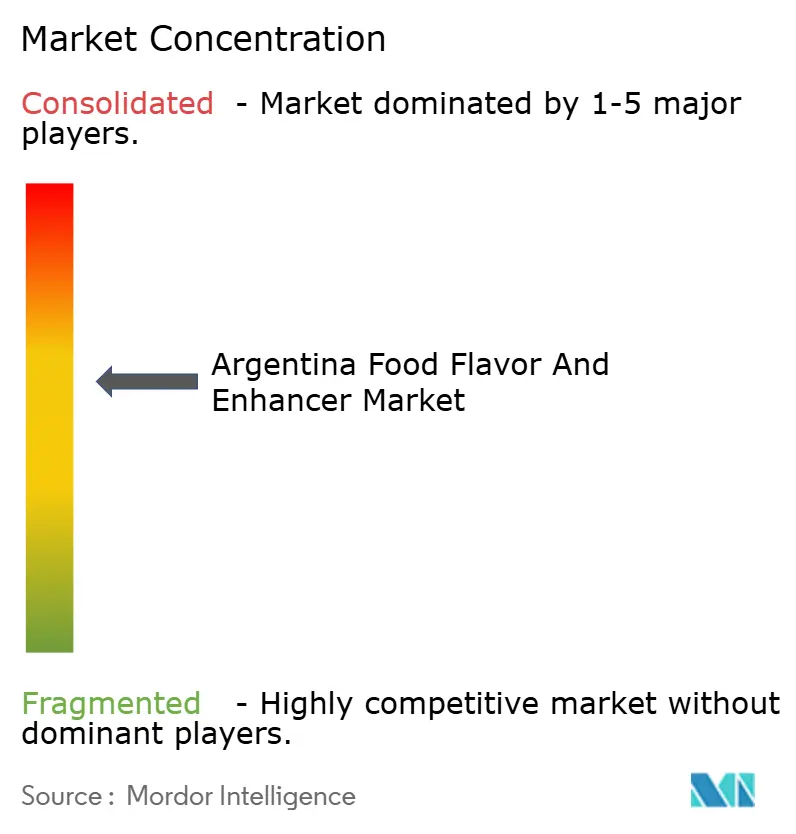

The Argentina food flavor and enhancer market is moderately consolidated, with multinational companies such as Givaudan, Kerry, DSM-Firmenich, IFF, and Symrise holding a significant market share. These companies maintain vertically integrated supply chains that encompass botanical sourcing, fermentation, encapsulation, and application laboratories. This integration allows them to streamline operations and maintain control over the entire production process. Regional specialists, including the Arcor-Ingredion joint venture, and local players like Novarom Sabores, leverage their proximity to end-users and their ability to provide faster turnaround times for custom formulations, giving them a competitive edge in catering to specific market demands.

Yeast-extract suppliers, including Lesaffre, Angel Yeast, and Ajinomoto, are emerging as disruptors in the market by offering turnkey sodium-reduction platforms. These platforms bypass traditional flavor houses, employing a vertical integration strategy that compresses margins for established players. Historically, these incumbents provided both reformulation consulting and flavor concentrates, but the new approach by yeast-extract suppliers challenges this model. Strategic trends reveal a division in the market, with multinational companies focusing on clean-label differentiation through fermentation and biotechnology, while local players prioritize cost-performance optimization. The latter achieve this by using nature-identical molecules that avoid "artificial" labels and are 40-60% less expensive than natural extracts, appealing to cost-conscious consumers.

Opportunities for growth exist in fermentation-derived dairy flavors, such as diacetyl and acetoin, which replicate butter and cream notes without relying on animal inputs. This segment represents a technical gap that companies like Angel Yeast aim to address. Angel Yeast's 11,000-ton yeast-protein line (AngeoPro) is designed to meet this demand by offering proteins with over 80% purity. These proteins serve as emulsifiers and mouthfeel enhancers, providing functional benefits while aligning with the growing demand for plant-based and animal-free products. This innovation highlights the potential for further advancements in fermentation technology to meet evolving consumer preferences.

Argentina Food Flavor And Enhancer Industry Leaders

-

Givaudan SA

-

Kerry Group plc

-

dsm-firmenich

-

International Flavors & Fragrances (IFF) Inc.

-

Ajinomoto Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Sensient Flavors & Extracts has launched BioSymphony, a portfolio of natural flavor compounds developed through biotransformation using nature-derived ingredients. This range is globally recognized as natural, simplifying labeling for food and beverage manufacturers and streamlining formulations. BioSymphony aims to enhance flavor sophistication, broaden flavor profiles, and address ingredient challenges in diverse applications, delivering deeper, more nuanced tastes while managing formulation complexities.

- October 2023: Symrise has introduced SET Flavors, a global flavor solutions platform that utilizes selective enrichment and advanced processing technologies to develop authentic, high-value taste profiles from natural raw materials and food industry by-products. This platform supports food and beverage manufacturers in creating complex, sustainable, and natural flavors, fostering innovation across various categories while optimizing resource utilization.

Argentina Food Flavor And Enhancer Market Report Scope

The Argentine food flavor and enhancer market is segmented by type into the natural flavor, synthetic flavor, nature identical flavoring, and flavor enhancers. Additionally, the market studied is segmented by application into bakery, confectionery, beverages, dairy, processed food, and other applications.

By Type

| Flavor | Natural Flavors |

| Nature-Identical Flavors | |

| Synthetic Flavors | |

| Flavor Enhancers |

Application

| Bakery and Confectionery |

| Beverages |

| Dairy Products |

| Noodles |

| Soups and Sauces |

| Savory Snacks |

| Other Applications |

| By Type | Flavor | Natural Flavors |

| Nature-Identical Flavors | ||

| Synthetic Flavors | ||

| Flavor Enhancers | ||

| Application | Bakery and Confectionery | |

| Beverages | ||

| Dairy Products | ||

| Noodles | ||

| Soups and Sauces | ||

| Savory Snacks | ||

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Argentina food flavor and enhancer market by 2031?

The market is expected to reach USD 770.45 billion by 2031.

Which segment will grow fastest in the next five years?

Flavor enhancers are poised for the quickest advance at a 6.95% CAGR through 2031.

Why do beverages dominate demand today?

Yerba mate-based energy drinks and reformulated carbonated soft drinks account for 34.35% of 2025 value, lifting beverage demand.

How does front-of-pack labeling influence formulation?

Black octagon warnings and QR-code ingredient disclosures encourage manufacturers to replace synthetic additives with clean-label botanicals and yeast extracts.