Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

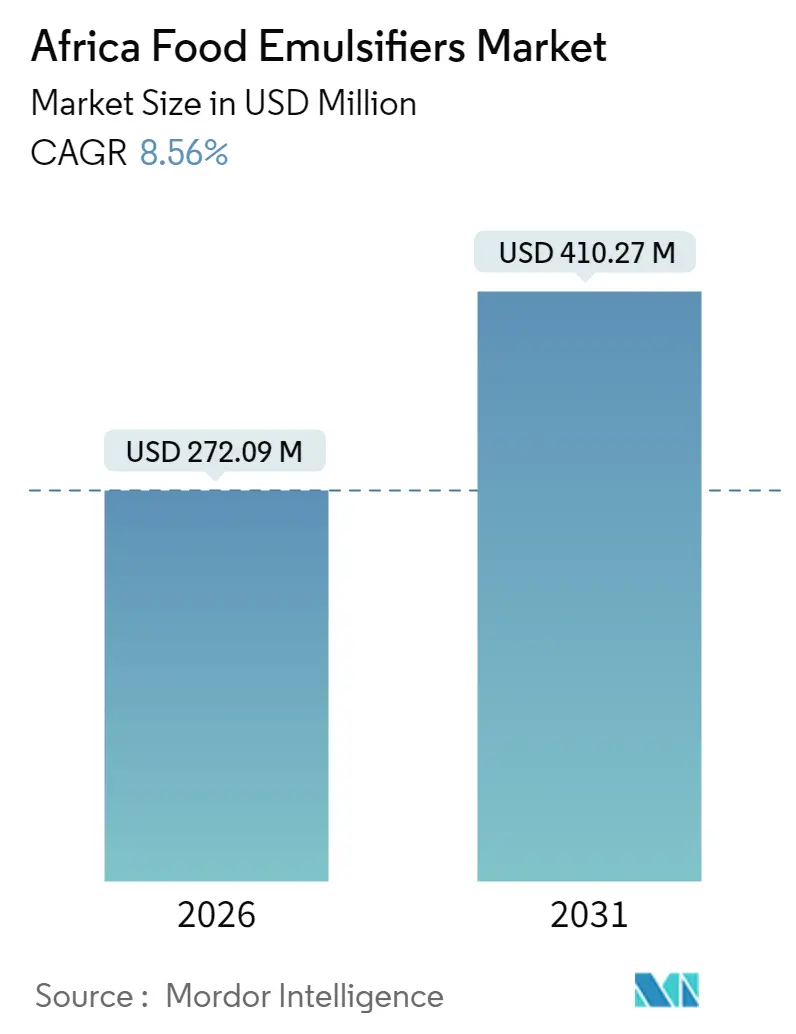

| Market Size (2026) | USD 272.09 Million |

| Market Size (2031) | USD 410.27 Million |

| Growth Rate (2026 - 2031) | 8.56% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Food Emulsifiers Market Analysis by Mordor Intelligence

The Africa food emulsifiers market was valued at USD 250.64 million in 2025 and estimated to grow from USD 272.09 million in 2026 to reach USD 410.27 million by 2031, at a CAGR of 8.56% during the forecast period (2026-2031). Factors driving this growth include rapid urbanization, over USD 5 billion in new food manufacturing projects since 2024, and the increasing adoption of automated bread production lines, which enhance efficiency and output in the bakery sector. Additionally, clean-label preferences among consumers are prompting manufacturers to adopt natural emulsifiers, while the emergence of local soy lecithin supply in East Africa is reducing their dependency on imports. Regional trade liberalization is also facilitating easier movement of goods, further boosting market growth. However, the market faces challenges such as volatile import prices driven by fluctuating exchange rates, inflationary pressures affecting consumer purchasing power, and skepticism toward E-number additives, which are perceived as artificial and less healthy by some consumers.

Key Report Takeaways

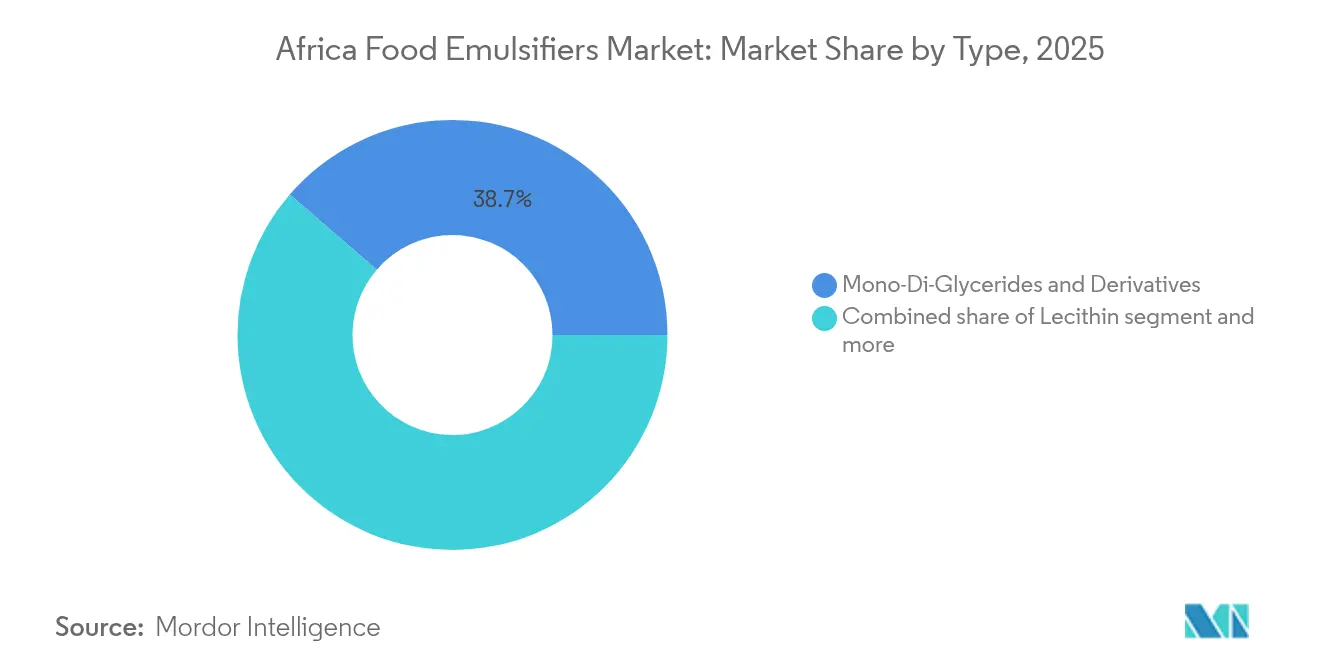

- By product type, mono-and diglycerides led the Africa food emulsifiers market with 38.67% of the market share in 2025, while lecithin is forecast to expand at a 8.74% CAGR between 2026 and 2031.

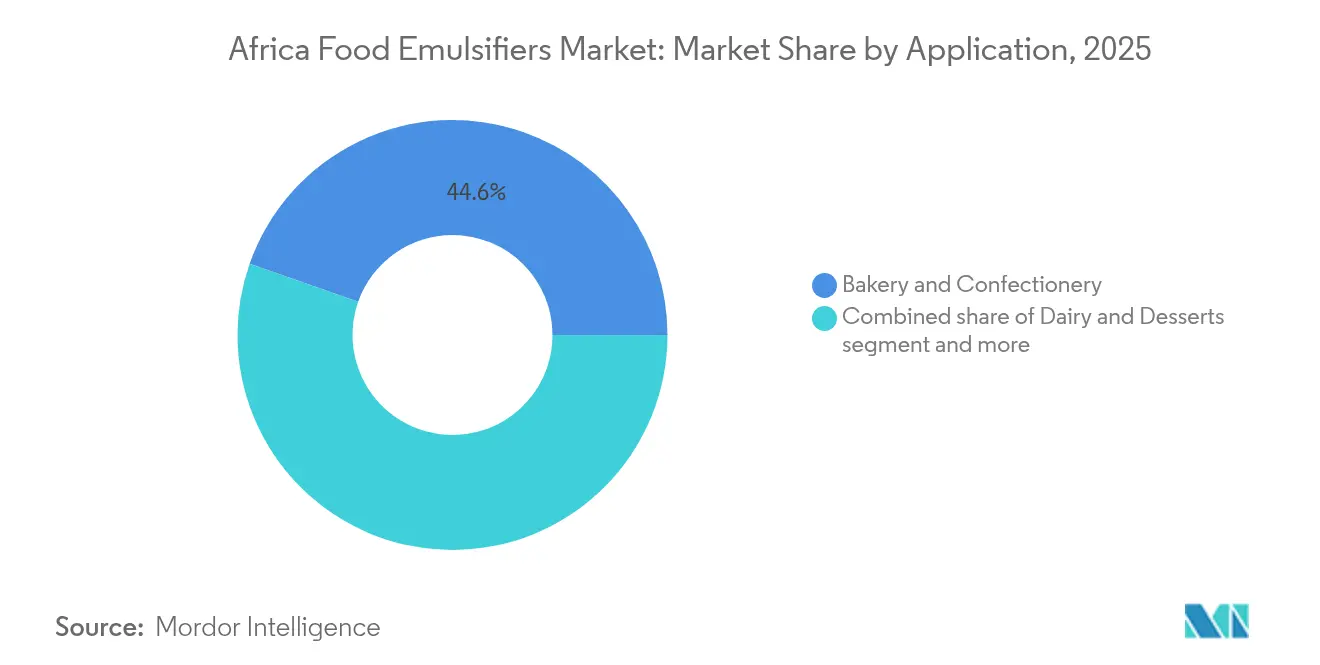

- By application, bakery and confectionery accounted for 44.62% of the Africa food emulsifiers market size in 2025, and dairy and desserts are projected to advance at a 9.23% CAGR through 2031.

- By geography, South Africa held a 27.95% revenue share in 2025; Nigeria is expected to record the fastest growth, with an 8.66% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Food Emulsifiers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods | +1.8% | Global, with concentration in Nigeria, South Africa, Egypt | Medium term (2-4 years) |

| Rapid penetration of industrial bread lines across West Africa | +1.5% | West Africa core (Nigeria, Ghana, Côte d'Ivoire), spill-over to Francophone markets | Short term (≤ 2 years) |

| Increased adoption of clean-label and plant-derived emulsifiers | +1.3% | South Africa, Egypt, urban Nigeria; export-oriented processors | Medium term (2-4 years) |

| Investments in food manufacturing capacity in Nigeria, Kenya, and South Africa | +2.1% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Price advantages of locally crushed soy-lecithin in East Africa | +0.9% | East Africa (Kenya, Ethiopia, Uganda), with trade linkages to Tanzania | Long term (≥ 4 years) |

| Growing demand for emulsifier blends for cost optimization in food processing | +1.2% | Global, particularly Nigeria and Egypt where currency volatility drives cost sensitivity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for processed and convenience foods

The increasing demand for processed and convenience foods across Africa is a key driver of the food emulsifiers market's growth. Factors such as rapid urbanization, rising disposable incomes, and busier lifestyles are contributing to higher consumption of packaged snacks, sauces, ready meals, and other shelf-stable products. These products depend on emulsifiers to maintain texture, stability, and shelf life. As manufacturers scale up production to meet this demand, the need for functional ingredients such as emulsifiers, stabilizers, and thickeners is increasing, creating opportunities for ingredient suppliers across the continent.In South Africa, this trend is further supported by the structure and scale of the food and beverage industry. The sector is one of the most diversified manufacturing segments in the country, dominated by a few large firms with significant domestic market influence. According to the Trade and Industrial Policy Strategy 2025 report, the food processing sector alone comprises over 1,800 companies [1]Source: TIPS, "Trade and Industrial Policies Strategies," tips.org.za. This concentration of large manufacturers, along with a broad network of smaller processors, drives demand for high-quality emulsifiers that ensure consistent product quality, shelf stability, and innovation in processed and convenience foods.

Rapid penetration of industrial bread lines across West Africa

West Africa's bakery market is undergoing rapid industrialization. In July 2024, Bühler and Flour Mills of Nigeria inaugurated a Grains Application Centre in Lagos to pilot high-throughput milling and baking technologies for local and regional clients. This facility, along with Bühler's Grains Processing Innovation Centre in Kano and SnackFix modular lines for small and medium enterprises, highlights a transition from artisanal to automated bread production. This shift necessitates consistent emulsifier performance in high-speed dough mixing and proofing processes. Industrial bread production requires emulsifiers that ensure rapid hydration, gluten strengthening, and crumb softening on a large scale. While mono- and diglycerides are well-suited for these functions, enzyme-modified lecithins present additional opportunities by reducing dough stickiness and improving machinability. Flour Mills of Nigeria has committed USD 1 billion to capacity expansion, while JBS has invested USD 2.5 billion in Nigerian food manufacturing, both focusing on processed foods where emulsifiers play a critical role in formulation [2]Source: Food Beverage Trade, "Consumer Trends in SA Processed Foods: What’s Popular?," foodbevtrade.co.za. The strategic implication for emulsifier suppliers is clear: those who establish technical support and blending facilities near these new industrial bread lines, providing just-in-time delivery and application labs, are likely to gain a significant competitive advantage as processors aim to minimize working capital tied up in imported ingredients.

Increased adoption of clean-label and plant-derived emulsifiers

As consumers across Africa, particularly in developed markets like South Africa, become increasingly health- and environment-conscious, the demand for foods made with simpler, natural ingredients is growing. This shift, known as the "clean-label" trend, has led food and beverage manufacturers to prioritize plant-derived emulsifiers, such as lecithin from sunflower or soy, gum arabic, and pectin, over traditional synthetic stabilizers. In South Africa, heightened environmental awareness is influencing food choices, with sustainable practices, including eco-friendly packaging and ethically sourced ingredients, becoming essential [3]Source: African Development Bank Group, "Nigeria’s Special Agro-industrial Processing Zones (SAPZ) Phase II, Boosted with a Whopping $2.2 billion Investment Interest at the Africa Investment Forum (AIF) 2024," afdb.org. This has positioned clean-label and plant-derived emulsifiers as not only functional necessities but also as key factors in aligning with consumer values. As the market for processed and convenience foods, bakery products, dairy alternatives, sauces, and dressings expands, the demand for natural emulsifiers is increasing. This presents a significant growth opportunity for ingredient suppliers capable of meeting clean-label and sustainability requirements.

Investments in food manufacturing capacity in Nigeria, Kenya, and South Africa

Investments in food-processing and manufacturing infrastructure across key African markets are driving significant growth in the demand for emulsifiers and related functional ingredients. In countries such as Nigeria, Kenya, and South Africa, new processing facilities, modernized plants, and expanding industrial capacities are being developed. This growth is fueled by rising urban populations, increasing demand for processed and convenience foods, and higher disposable incomes. As companies expand manufacturing capabilities to produce packaged foods, snacks, sauces, dairy alternatives, bakery products, and ready-to-eat meals, they increasingly depend on emulsifiers, stabilizers, and texturizers to ensure consistent texture, extended shelf life, and product stability. Consequently, the emulsifier ingredient market is directly benefiting from the expansion of food processing infrastructure. In South Africa, the food-processing sector remains one of the most diversified manufacturing segments and continues to attract investments. Recent analyses indicate growth in the processed food and export sectors, supported by advanced processing technologies, export expansion, and trade integration opportunities under regional and continental trade frameworks. This structural growth at the factory level provides a stable and scalable customer base for emulsifier suppliers. Large-scale manufacturers, as opposed to fragmented artisanal producers, contribute to improved economies of scale, higher demand volumes, and sustained long-term growth in the emulsifiers market across Africa.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import reliance and price volatility of imported mono and diglycerides | -1.4% | Nigeria, Egypt, Kenya (high import dependence on European/Asian suppliers) | Short term (≤ 2 years) |

| Consumer skepticism toward E-number additives | -0.8% | South Africa, urban Egypt, export-oriented processors | Medium term (2-4 years) |

| Currency volatility increasing raw material procurement costs | -1.6% | Nigeria, Egypt, Ghana (currencies under depreciation pressure) | Short term (≤ 2 years) |

| Price sensitivity among consumers restricting premium formulation adoption | -1.1% | Rural Nigeria, low-income segments across sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High import reliance and price volatility of imported mono and diglycerides

Africa's emulsifier supply chain heavily relies on imports from Europe and Asia, making processors vulnerable to foreign exchange fluctuations and freight-rate volatility. Mono- and diglycerides, which accounted for 39.24% of the product-type share in 2024, are primarily imported. The depreciation of the Nigerian naira and Egyptian pound in 2024 increased landed costs by 20% to 35%, despite stable ex-works prices in Europe. A key challenge is the lack of backward integration into emulsifier manufacturing within Africa. The continent has no mono-diglyceride production facilities, and efforts to establish local production are hindered by the high capital costs of esterification reactors and distillation columns. This creates a persistent cost disadvantage compared to processors in Asia or Latin America, who source emulsifiers domestically. Consequently, there is a structural incentive to substitute mono-diglycerides with locally available alternatives, such as lecithin or enzyme-modified starches, even if their technical performance is inferior.

Price sensitivity among consumers restricting premium formulation adoption

African consumers, particularly those in rural areas and low-income urban segments, prioritize affordability over label claims or functional benefits. This limits processors' ability to adopt premium emulsifiers. In Nigeria, bread consumption is predominantly focused on low-cost, unbranded loaves sold through informal channels, where price competition is intense. Processors are unable to pass on the 15% to 25% cost premium associated with lecithin or enzyme-modified emulsifiers without risking a loss in volume to competitors using commodity mono-diglycerides. The African Continental Free Trade Area's tariff reductions are intensifying competition by facilitating cross-border trade in processed foods. This increased competition is compressing margins and reinforcing the emphasis on cost minimization. Smaller processors, lacking economies of scale, face a choice between maintaining low prices with commodity emulsifiers or targeting niche premium segments, which are too small to justify dedicated production lines. Consequently, innovation in the market is concentrated among large multinationals and export-oriented players, while the mass market remains focused on cost-driven formulations.

Segment Analysis

By Product Type: Lecithin Gains on Clean-Label Momentum

Mono- and diglycerides accounted for 38.67% of the Africa food emulsifiers market share in 2025. However, lecithin is expected to surpass the overall compound annual growth rate (CAGR) of 8.56%, with a projected growth rate of 8.74% through 2031. The increasing demand for clean-label products in South Africa and Egypt, combined with untapped crushing capacity in Kenya, is improving local supply prospects. Multinational companies are blending lecithin with gums to optimize cost and functionality, highlighting how performance blends are challenging the long-standing dominance of the mono- and diglycerides category. As regional crushers enhance refining processes, locally sourced lecithin could reduce price disparities and support longer-term supply contracts within the Africa food emulsifiers market.

Manufacturers targeting price-sensitive mass markets are likely to continue relying on mono- and diglycerides for their dough conditioning and antistaling properties. However, premium bakers, confectioners, and dairy producers are increasingly turning to lecithin to meet export standards and enhance label appeal. Wilmar’s specialty fats line in North Africa and Tate & Lyle’s expanded hydrocolloid offerings are facilitating the development of multifunctional systems that offset the higher costs associated with phospholipids. Consequently, competition within the Africa food emulsifiers market is shifting from individual ingredients to integrated solutions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Dairy and Desserts Outpace Bakery

In 2025, the bakery and confectionery segment accounted for 44.62% of the Africa food emulsifiers market, driven by Nigeria’s 81% bread penetration and the increasing automation of production lines in West Africa. Looking ahead, the dairy and desserts segment is expected to achieve the highest compound annual growth rate (CAGR) of 9.23%, supported by Nigeria’s National Dairy Policy, which aims to reduce USD 1.5 billion in annual milk powder imports. Additionally, ice cream manufacturers in East Africa are utilizing air-entraining emulsifiers to enhance texture quality in warmer climates, contributing to market growth.

Beverage manufacturers are using emulsifiers to stabilize oil-in-water flavor systems. In the meat processing sector, companies upgrading sausage and processed meat production lines, following JBS’s investment in Nigeria, depend on fat-binding emulsifiers. Similarly, soups, sauces, and dressings benefit from gum-phospholipid blends that prevent phase separation during non-refrigerated transport. As a result, market demand is more influenced by new plant start-ups than by per-capita consumption, linking the Africa food emulsifiers market closely to capital investment cycles.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, South Africa accounted for 27.95% of the revenue in the African food emulsifiers market, driven by its advanced manufacturing base, well-established blended-ingredient hubs, and robust dairy production capabilities. The country's investments in precision fermentation highlight a growing interest in plant-derived systems, which are expected to shape future demand. However, challenges such as currency fluctuations and a reliance on imports continue to add cost pressures. These factors are encouraging formulators to explore regional sourcing options to mitigate risks and reduce dependency on external markets.

Nigeria is projected to achieve the highest compound annual growth rate (CAGR) of 8.66% through 2031, supported by over USD 3.5 billion in new capacity across bakery, dairy, and meat production. The Lagos Grains Application Centre is playing a pivotal role in enhancing high-throughput bread production, addressing the growing demand for bakery products. Additionally, policy initiatives aimed at localizing dairy production are driving the adoption of stabilizers in milk powders and yogurts, further strengthening the market.

Kenya, Ethiopia, and Uganda present significant growth opportunities, particularly due to under-utilized soy crushers that could supply lecithin to regional markets once investments in refining address existing quality gaps. These countries are well-positioned to benefit from the African Continental Free Trade Area (AfCFTA), which has introduced tariff reductions to facilitate cross-border ingredient flows. This development is expected to encourage multimarket distribution strategies, enabling these nations to play a more prominent role in the regional food emulsifiers market.

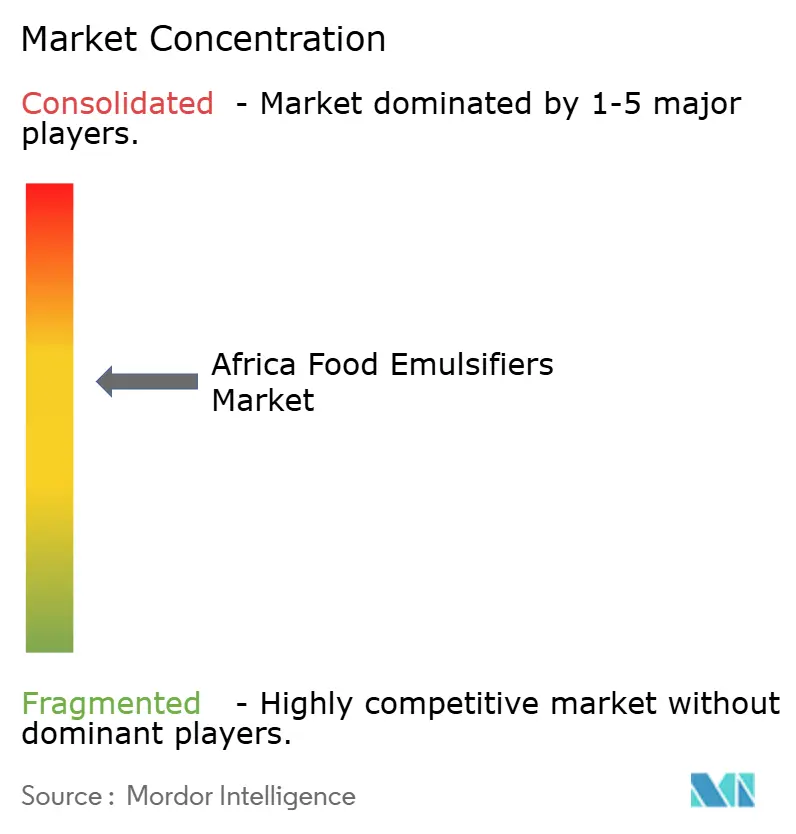

Competitive Landscape

The Africa food emulsifiers market exhibits a moderate concentration level, with global companies such as Cargill, ADM, Kerry, and IFF competing alongside regional players like Wilmar International. Corbion's planned exit from the emulsifiers market in 2024 will remove a supplier that previously catered to export-oriented processors. This development is expected to prompt some customers to renegotiate contracts with the remaining providers, potentially reshaping the competitive landscape. The market dynamics highlight the importance of adaptability and strategic partnerships among suppliers to maintain their foothold in the region.

Market participants are focusing on differentiation strategies that go beyond price competition. These include establishing local application centers, engaging in technical co-development, and leveraging digital formulation tools to meet the specific needs of customers. For example, Cargill's NutriHarvest initiative combines agricultural outreach with ingredient sales, fostering stronger connections between farmers and processors in key markets such as Kenya and Tanzania. Such initiatives not only enhance supply chain efficiency but also foster long-term relationships with stakeholders, providing a competitive edge in the market.

Additionally, innovation is emerging as a key driver of growth in the Africa food emulsifiers market. Start-ups like South Africa's De Novo Foodlabs, supported by public grants, are exploring advanced technologies such as precision fermentation to develop new emulsifier solutions. This signals a potential shift in the market toward more sustainable and innovative products. Overall, supplier success in this market hinges on effectively combining regional logistics expertise with specialized knowledge to mitigate currency risks and cater to the diverse requirements of the customer base.

Africa Food Emulsifiers Industry Leaders

-

DuPont de Nemours, Inc.

-

Cargill, Incorporated

-

BASF SE

-

Corbion NV

-

Archer-Daniels-Midland Company (ADM)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Kerry Group, a global taste and nutrition company, inaugurated its first "taste manufacturing" facility in Kigali, Rwanda, as part of its broader investment strategy in emerging markets. The new plant is designed to supply local food and beverage manufacturers in East Africa with high-quality ingredients and tailored "taste solutions," combining Kerry's global expertise with regional preferences. The facility emphasizes sustainability, incorporating energy-efficient utilities, a wastewater treatment system, and a "zero waste to landfill" policy.

- September 2024: DSM-Firmenich announced the opening of its new Animal Nutrition & Health premix and additives manufacturing plant in Sadat City, Egypt. Officially inaugurated on 12 September 2024, the facility demonstrates the company's commitment to addressing the growing demand from mid-range and large livestock farms, as well as feed millers, for premixes and innovative feed additives. This new production unit will cater to customers in Egypt, the Middle East, Southern Europe, and Africa. By enhancing supply reliability and delivering high-quality products, the facility aims to provide DSM-Firmenich's customers with greater assurance, aligned with the company's dedication to excellence.

Africa Food Emulsifiers Market Report Scope

Middle East and Africa food emulsifier market is segmented by type into lecithin, monoglyceride, diglyceride, and derivatives, sorbitan ester, polyglycerol ester, other types. Additionally, the study focusses on the revenues generated through dairy and frozen products, bakery, meat, poultry, and seafood, beverage, confectionery, and other applications. By geography, the market covers South Africa and Saudi Arabia.

By Product Type

| Mono-Diglycerides and Derivatives |

| Lecithin |

| Sorbate Esters |

| Other Emulsifier |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

By Geography

| South Africa |

| Egypt |

| Nigeria |

| Rest of Africa |

| By Product Type | Mono-Diglycerides and Derivatives |

| Lecithin | |

| Sorbate Esters | |

| Other Emulsifier | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications | |

| By Geography | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Africa food emulsifiers market in 2031?

The market is forecast to reach USD 410.27 million by 2031, growing at an 8.56% CAGR.

Which product type is expected to grow fastest through 2031?

Lecithin is set to post the highest 8.74% CAGR due to clean-label demand and emerging local supply.

How does currency volatility affect emulsifier procurement?

Depreciating currencies inflate imported ingredient costs, prompting processors to favor local-currency deals and cost-optimized blends.

Which application will outpace others over the forecast period?

Dairy and desserts categories are projected to advance at a 9.23% CAGR as local milk processing scales up.