When India simplified GST into just two slabs (5% and 18%) in September 2025, it did more than cut paperwork. It set off a chain reaction across fields, factories, and shelves. Farmers face new margin opportunities, processors see pricing flexibility, and consumers may find healthier options within reach. For leaders steering strategy, this is not a minor adjustment, it is a reset. Here, we explore what’s changing, what risks emerge, and where the next wave of growth could come from.

The New GST Landscape: What’s Changed & Why It Matters

GST Reforms 2025: Sector-Wise Changes

| Segment | Previous GST Rate(s) | New Rate | Key Change | Why It Moves the Needle |

| Agricultural inputs (fertiliser, pesticides, farm tools) | 12% – 18% | 5% | Significant drop in input cost | Farmers’ margins increase, leading to more reinvestment in inputs & efficiency |

| Processed foods | Often 12% / 18% | 5% | Lower rate on many finished goods | Processed goods become more affordable; demand shifts upward |

| Staple / daily essentials | 5% or exempt | Remains 5% / exempt | Less change here | But removal of complexities helps logistics & pricing consistency |

| Beverages (healthy vs. sugary / aerated) | Mixed: many taxed at higher rate | Healthy drinks mostly 5%; others retain higher rates | Policy creating differentiation | Encourages healthier consumption; old categories pressured |

Source: Mordor Intelligence

Farmers and Processors: What Could Change

- Improved Farm-Gate Profitability: With inputs like fertiliser and equipment now taxed at 5%, some farmers may see a 4-8% improvement in profitability. This additional income could support investment in seeds, machinery, or sustainable practices.

- Machinery Uptake: The Indian agricultural machinery market is valued at USD 18.15 billion in 2025 and projected to reach USD 27.29 billion by 2030 (8.5% CAGR). Reduced costs may make tools like harvesters and precision equipment more accessible.

- Tractor Market Transformation: The India agricultural tractor market size stands at USD 7.92 billion in 2025 and is forecast to reach USD 10.95 billion by 2030, advancing at a 6.70% CAGR. According to The Centre for Monitoring Indian Economy (CMIE), 150 million people were employed in India's agriculture sector in the financial year 2024. However, the number of employees was the highest in fiscal year 2022 at over 158 million.

- Simpler Supply Chains: A streamlined tax structure can reduce compliance and transaction costs by 3-5%. This may help medium and large processors manage operations more efficiently, particularly benefiting the INR 4,556.93 crore government investment in farm mechanization under Sub-Mission on Agricultural Mechanization (SMAM).

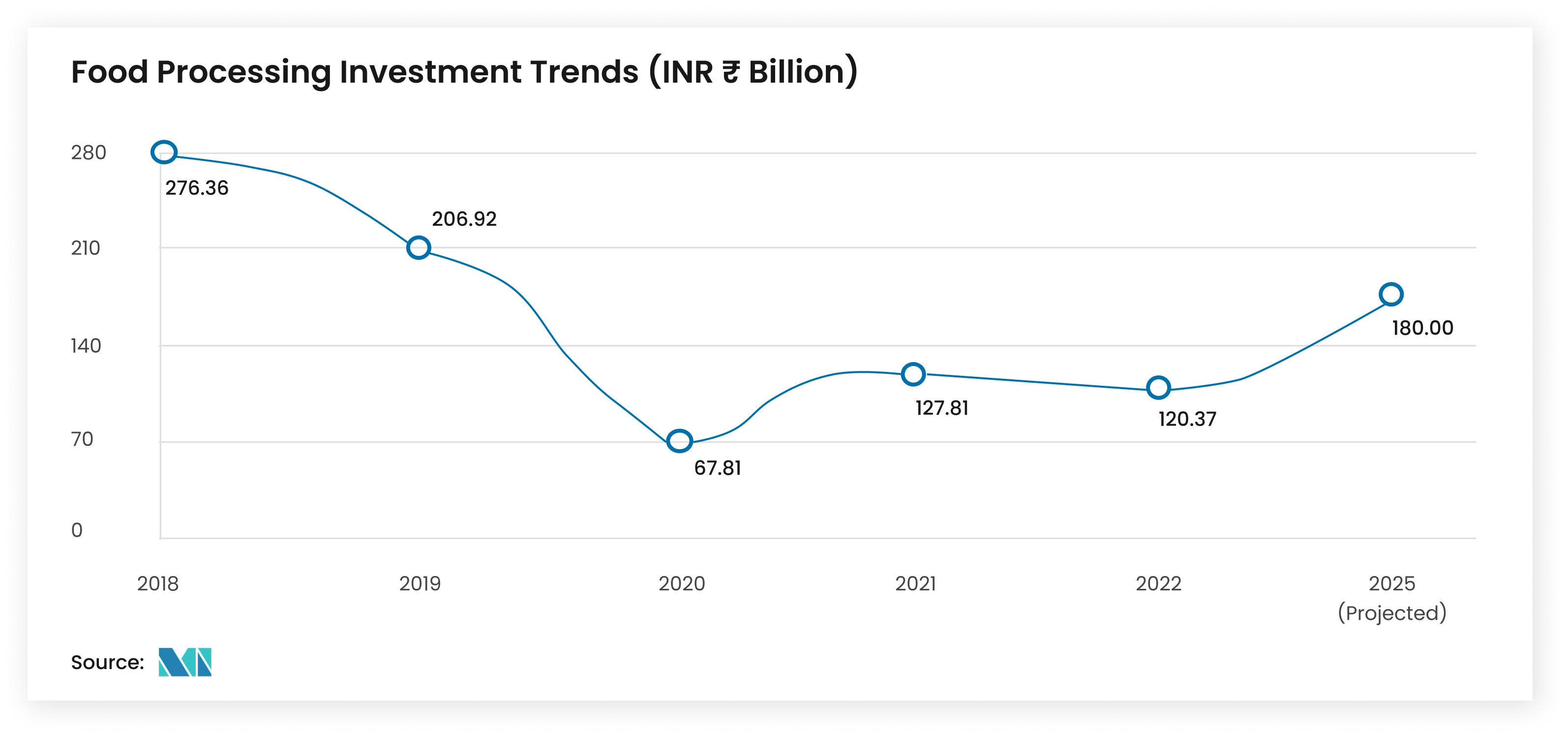

Processed Foods: Demand, Innovation & Margin Trade-offs

- Demand Surge Incoming: With many processed goods now bearing only 5% GST, Mordor Intelligence projects 15–20% demand growth in the next 18 months. This comes not just from price cuts but from wider access, Tier-2 and Tier-3 towns will matter more.

- Export Leverage Enhancement: India’s agricultural exports rose by 6.47% in FY 2024-25, reaching USD 51.91 billion, according to the Union Ministry of Commerce. Within this impressive growth, the dairy sector saw a 54% jump in export value, reaffirming India’s emerging position in global value-added dairy markets.

- Margin Decision Points: Producers face a choice, they can either absorb the savings and gain market share, or reinvest them into product innovation (better packaging, healthier versions), logistics, or branding. Those who choose the latter may command stronger loyalty and higher growth later.

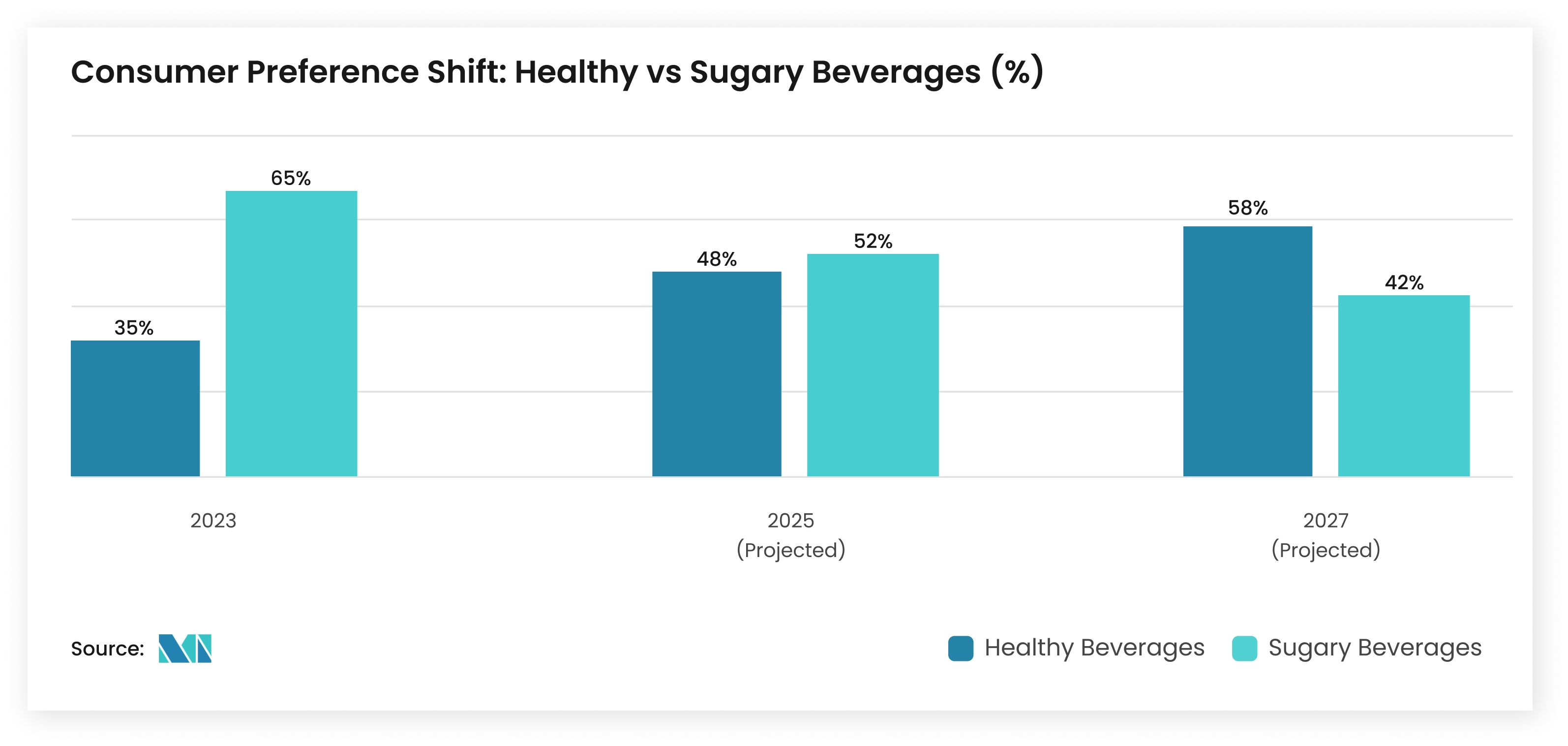

Beverages: Forcing a Rebalance

GST reforms impose a subtle "nudging" effect on consumer behaviour.

- Health-oriented drinks such as natural juices and fortified beverages are now mostly taxed at 5%, making them more affordable.

- Classic soft drinks and sugary or aerated beverages remain at higher rates, which creates cost pressure.

Market data shows that 57% of Indian consumers already spend more on genuine green and healthy products across Tier-1 and Tier-2 cities. With 77 million diabetes patients, the second-largest globally, health consciousness is increasingly shaping beverage choices.

A 20–28% consumer shift toward healthier beverages is projected over the next two years. Brands with flexible portfolios are positioned to adapt more easily, while those concentrated in fizzy or sugary drinks may need to rebalance through product reformulation, marketing adjustments, or portfolio diversification.

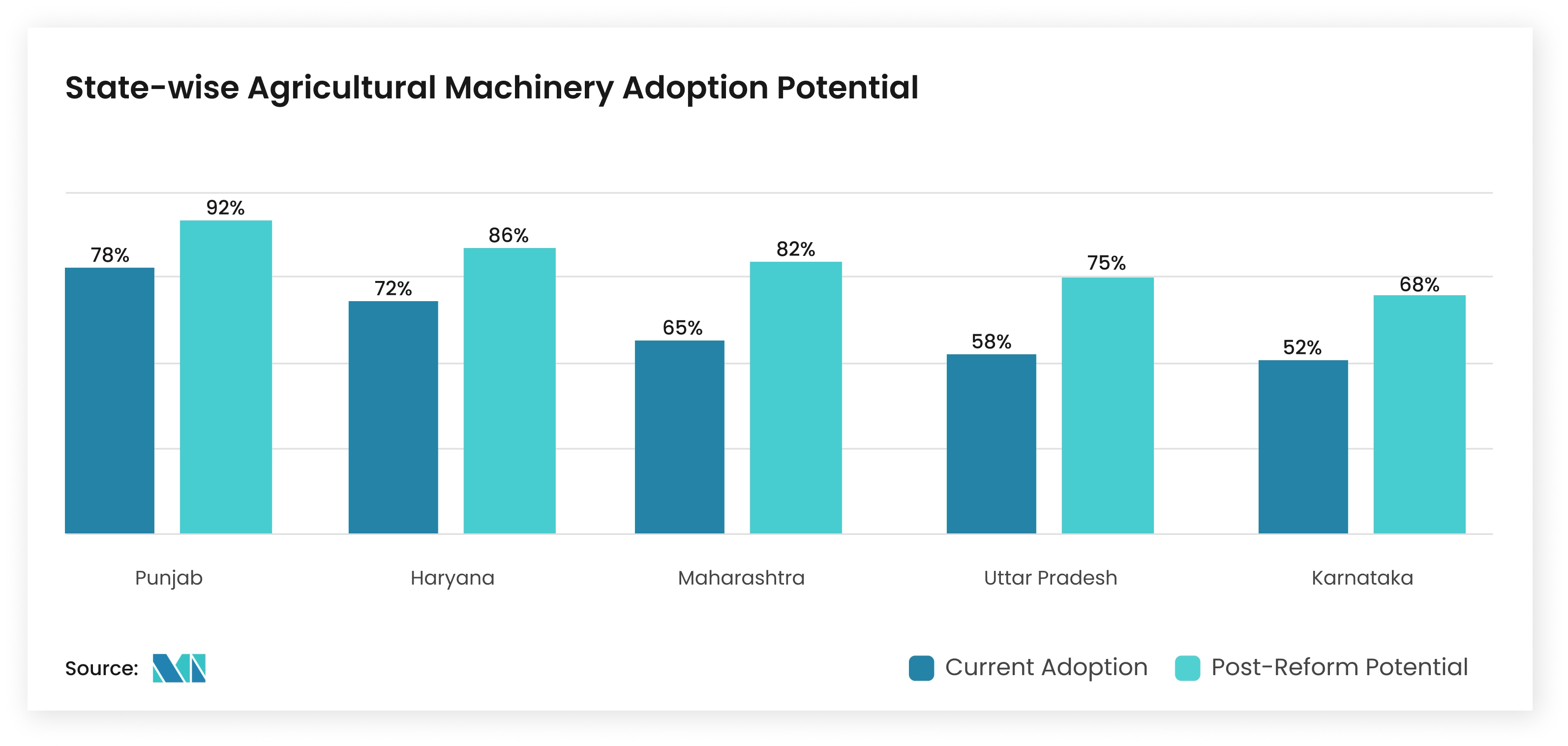

The Rural Story & Where Complexity Lurks

Rural economies, which account for most of India’s consumption and production, are expected to feel the impact strongly. States such as Punjab, Maharashtra, and Haryana could record 18–22% higher value addition in select agri-food clusters within three years if farmers and processors are able to capture input cost savings.

However, complexity remains. Not every processed product benefits from the full GST reduction, as some categories such as packaging and specific additives continue to face higher rates. Small and medium-sized enterprises may also face challenges in reclassifying SKUs, updating billing systems, and aligning existing supply contracts.

Industry Moves After GST Reform

Amul Story

Amul has announced that it will pass on the benefits of GST reduction directly to consumers by lowering retail prices across several product categories. This move establishes a precedent for other fast-moving consumer goods companies and strengthens consumer trust.

Other Brand Moves

- ITC is reportedly recalibrating its packaged food portfolio, with plans to adjust pricing in biscuits and snacks to capture rural demand growth.

- Nestlé India is focusing on product innovation and smaller SKUs, especially in dairy and nutrition, to ensure affordability post-GST.

- PepsiCo India may face pressure on its sugary beverage segment but is doubling down on juice and hydration brands to align with consumer health trends.

Five “GST Dividends” to Watch

Business Responses and Market Impact

| Dividend | How It Could Play Out | What Businesses Might Do | Market Impact |

| Cost Efficiency | Input cost reductions of 5–11% | Adjust procurement and pricing strategies | USD 2-3B savings industry-wide |

| Market Expansion | Wider affordability in smaller towns | Explore Tier-2/3 distribution and new SKUs | 15-20% demand growth |

| Investment Appeal | Better margins attract investors | Use improved economics to raise capital | USD 5-7B additional FDI potential |

| Export Competitiveness | Lower costs boost global positioning | Benchmark with peers, revisit trade agreements | 25-30% export growth |

| Technology Adoption | Savings may be reinvested | Invest in digital supply chains, packaging, and agri-tech | 40-50% automation uptake |

Source: Mordor Intelligence

Key Risks & Trade-Offs

- Distribution of gains may lag: Large agri-processors or brands are likely to capture savings first, and it could take time before the benefits reach small farmers and end consumers.

- Compliance and reclassification challenges: SKU classifications, input versus output tax credits, and state-level implementation differences carry the risk of delays or disputes.

- Partial benefit leakage: Packaging materials and non-essential ingredients may continue to be taxed at higher rates, and not all manufacturers will be able to reformulate quickly, leaving some costs in place.

Next Steps for Businesses

Here are some practical steps companies could consider:

- Review cost structures and identify where GST reductions apply.

- Update procurement contracts to reflect new rates.

- Test pricing adjustments in Tier-2 and Tier-3 markets.

- Reinvest part of the savings into product innovation or supply chain technology.

- Help smaller partners in the supply chain adapt to the new system.

- Track ongoing government updates, as finer clarifications may follow.

Final Thought: Not an Adjustment but a Reset

The 2025 GST reforms simplify taxation while reshaping cost structures and competitiveness across India’s agri-food sector. The opportunity lies not only in capturing immediate savings but in channelling them toward innovation, expansion, and stronger supply chains.

For executives, the challenge is to balance urgency with discipline, moving quickly to realize efficiencies while making deliberate choices about where to reinvest. Those who align cost advantages with long-term strategy will be best positioned to navigate shifts in affordability, consumer preference, and export competitiveness over the coming decade.

Want deeper insights on how GST reforms are reshaping India’s agri-food market? Explore our latest Agriculture & Food Report.

Related Reports

Agricultural Machinery Market

North America,Europe,Asia Pacific,South America,Middle East,Africa

Food And Beverage Market

North America,Europe,Asia Pacific,South America,Middle East and Africa

Soft Drinks Market

North America,Europe,Asia Pacific,South America,Middle East and Africa

Synapse

Intelligent market analysis tool to get your insights straight Intelligent market analysis tool to get your insights straight.

Book A Demo