Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

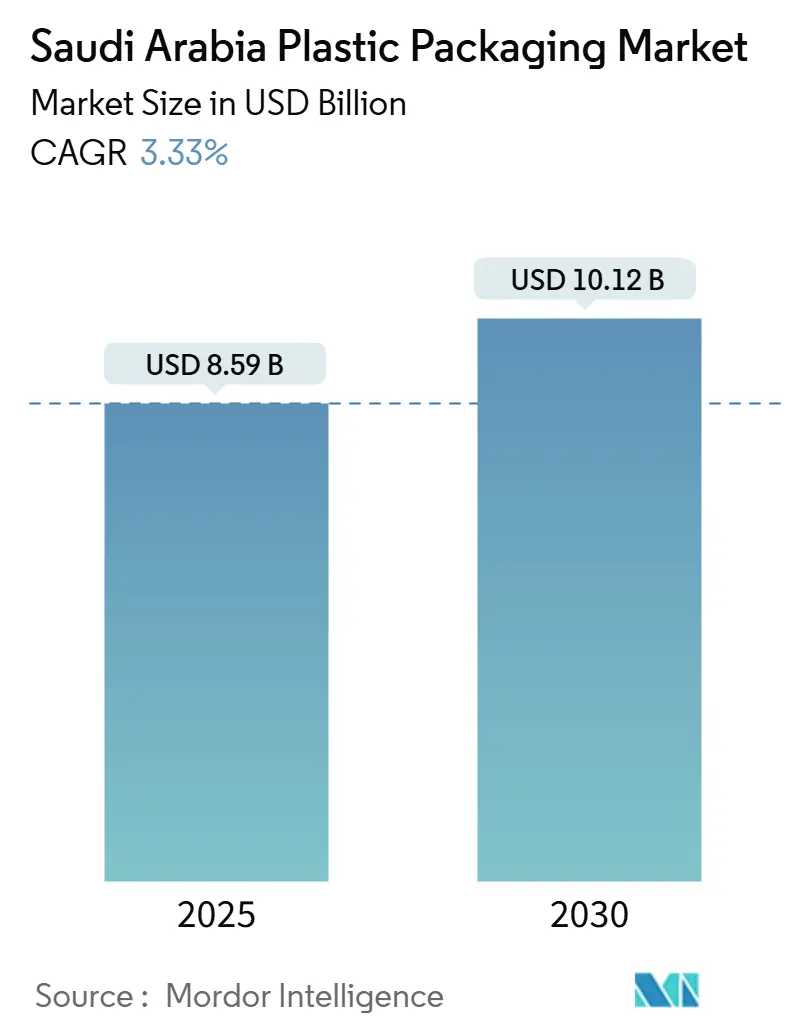

| Market Size (2025) | USD 8.59 Billion |

| Market Size (2030) | USD 10.12 Billion |

| Growth Rate (2025 - 2030) | 3.33% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Plastic Packaging Market Analysis by Mordor Intelligence

The Saudi Arabia plastic packaging market size stands at USD 8.59 billion in 2025 and is forecast to climb to USD 10.12 billion by 2030, reflecting a 3.33% CAGR. The steady pace of expansion aligns with Vision 2030’s localization incentives that draw global converters into specialized clusters such as NEOM and Ras Al Khair. Rising non-oil exports, a vibrant food-and-beverage sector, and sustained population growth underpin demand for lightweight, high-barrier formats. Brand owners are shifting toward multilayer pouches and recyclable mono-material films to curb logistics costs and comply with Saudi Standards, Metrology and Quality Organization (SASO) requirements. Meanwhile, integrated petrochemical producers leverage feedstock advantages to stabilize resin pricing for domestic converters amid global volatility.[3]“Saudi Arabia - Country Commercial Guide: Labeling/Marking Requirements,” International Trade Administration, trade.gov

Key Report Takeaways

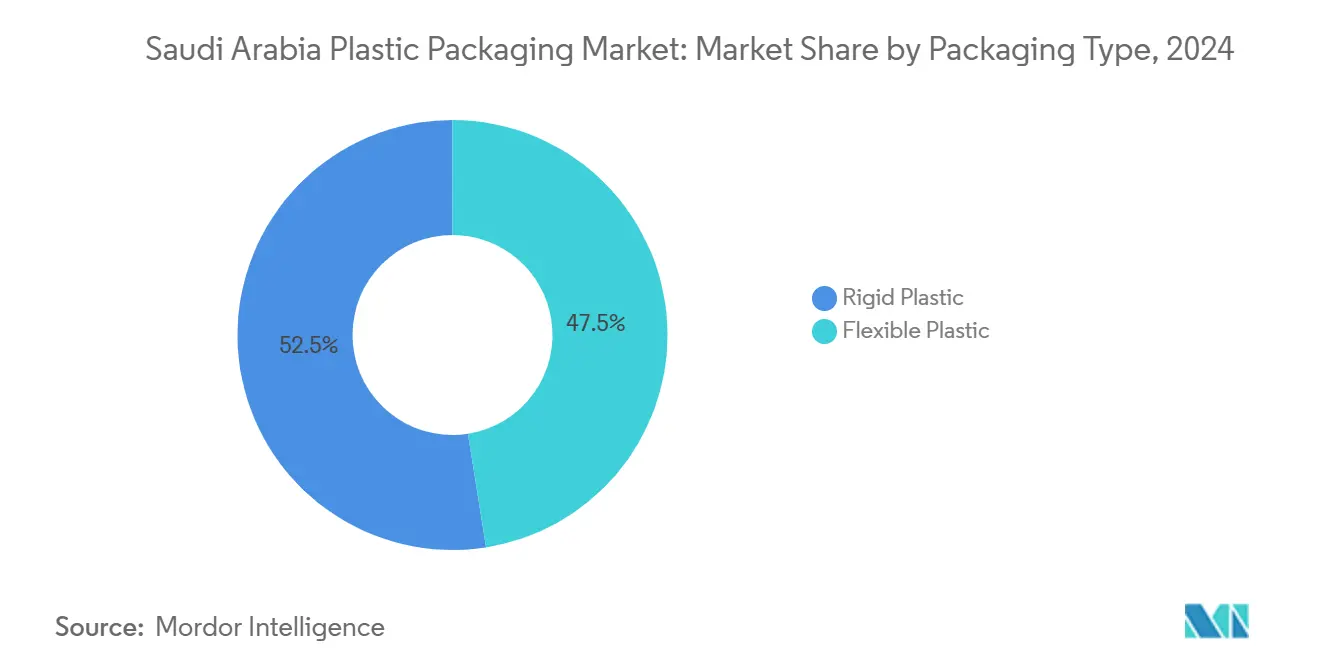

- By packaging type, rigid formats led with 52.73% of the Saudi Arabia plastic packaging market share in 2024 while flexible formats are projected to post the fastest 4.43% CAGR through 2030.

- By material, polyethylene accounted for 31.62% of the Saudi Arabia plastic packaging market size in 2024; ethylene-vinyl alcohol and other specialty barriers are set to expand at a 4.51% CAGR over the same horizon.

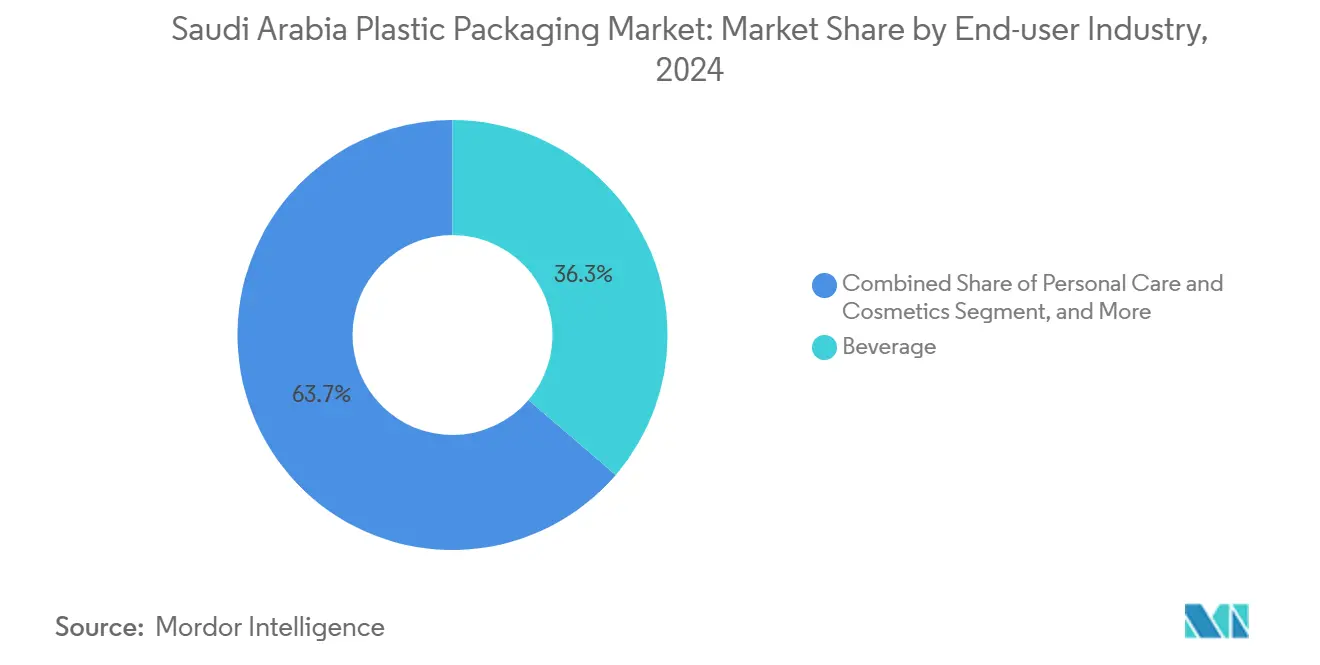

- By end-user industry, beverages held 36.28% revenue share in 2024, whereas personal care and cosmetics are on track for the highest 4.68% CAGR to 2030.

- By pack format, bottles and jars commanded 33.46% of revenue in 2024; pouches and sachets headline growth with a 4.37% CAGR toward 2030.

- By geography, the Eastern Province benefits most from Vision 2030’s downstream chemicals policy, while the NEOM corridor is poised for the quickest uptake of sustainable packaging solutions at a 4.9% CAGR to 2030.

Saudi Arabia Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising food-and-beverage demand for lightweight packs | +0.8% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Oxo-biodegradable compliance requirements | +0.6% | National; early pilots in NEOM, Ras Al Khair | Long term (≥ 4 years) |

| E-commerce expansion favoring flexible packs | +0.9% | National; early gains in major cities | Short term (≤ 2 years) |

| Vision 2030 pharmaceutical localization | +0.7% | King Abdullah Economic City, NEOM | Medium term (2-4 years) |

| Cluster-level conversion incentives | +0.5% | Ras Al Khair and NEOM | Long term (≥ 4 years) |

| Surge in date exports needing high-barrier pouches | +0.4% | Al-Qassim, Eastern Province | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Food and Beverage Sector for Convenient Lightweight Packaging

Rapid urbanization and a median age below 30 propel on-the-go consumption that favors portion-controlled pouches and resealable stand-up bags. Domestic manufacturers expanding chilled ready-meal lines rely on multilayer films to prolong shelf life and cut food waste. Vision 2030’s ‘Saudi Made’ labeling initiative magnifies export opportunities, driving converters to adopt higher oxygen-barrier laminates fit for trans-continental shipping [2]“Package of Services and Programs to Increase Contribution of Non-Oil Exports to GDP,” Saudi Press Agency, spa.gov.sa. Retailers also push for downgauged rigid bottles to reduce freight emissions, helping the Saudi Arabia plastic packaging market achieve incremental volume gains without proportional resin growth.

Government Regulations Promoting Oxo-Biodegradable Plastics Compliance

The National Center for Waste Management targets a 40% recycling rate by 2035, spurring mandatory oxo-biodegradable additives in single-use shopping bags. Early adoption zones in NEOM and Ras Al Khair function as regulatory sandboxes where converters test ISCC+-certified resins supplied by SABIC under its TRUCIRCLE program. As SASO standards tighten life-cycle assessments, brand owners lock in longer-term supply contracts for certified polymers, supporting mid-single-digit price premiums that buoy margins across the Saudi Arabia plastic packaging market.

Expansion of E-commerce and Modern Retail Accelerating Flexible Packaging Uptake

Online sales now exceed 20% of national retail turnover, forcing fulfillment centers to prioritize cube-optimized, puncture-resistant films over rigid formats. Flexible mailer pouches cut dimensional weight fees by up to 35%, a tangible cost advantage for electronics and personal-care shippers. Hypermarkets reconfigure shelf facings around peg-display packs, while convenience chains list single-serve drink sachets suited to mobile consumers. These shifts fast-track flexible film line installations, lifting capital-equipment imports to a record USD 310 million in 2024

Growing Pharmaceutical Manufacturing Under Vision 2030 Boosting Sterile Packaging

Generics plants inside King Abdullah Economic City require cyclic olefin copolymer vials, blister films, and UV-sterilizable shrink sleeves that meet EU and U.S. Pharmacopeia. Domestic converters scaling up clean-room capacity secure multi-year supply deals with multinational drug makers seeking local content compliance. Technical barriers shield margin structures, reinforcing a modest consolidation trend within the sterile segment of the Saudi Arabia plastic packaging industry

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-derived resin price volatility | -0.7% | National; strongest impact on SME converters | Short term (≤ 2 years) |

| Limited recycling infrastructure | -0.5% | Collection gaps outside Riyadh and Jeddah | Medium term (2-4 years) |

| Water-rationing curbing bottled-water sales | -0.3% | Nationwide; pronounced in western regions | Long term (≥ 4 years) |

| Duty-free paper substitutes | -0.4% | Beverage cups and food-service trays nationally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Crude-Derived Resin Prices Squeezing Converter Margins

Spot LDPE prices swung 27 % across 2024–2025, eroding the gross margin of non-integrated converters by nearly 400 basis points. SABIC posted a SAR 1.2 billion net loss in early 2025, citing unfavorable spreads between naphtha and polyethylene. Smaller film companies struggle to hedge costs, prompting accelerated interest in long-term off-take with domestic crackers.

Low Domestic Plastic Recycling Infrastructure Limiting Circular Packaging Adoption

Recycling capacity tops out at 13% of total polymer waste, constrained by manual sorting and scant food-grade reprocessing lines. Although the Saudi Investment Recycling Company broke ground on a 120 kt/yr PET reclamation plant in 2024, full commissioning will not occur until 2027. Converters therefore pay premiums for imported r-PET to meet brand owner pledges, reducing cost competitiveness at home.

Segment Analysis

By Packaging Type: Resilient Rigid Base, Rapid Flexible Upside

Rigid containers generated 52.73% of 2024 revenue, anchored by PET water bottles and HDPE jerrycans that satisfy stringent SASO drop-test criteria. That base ensures predictable throughput across the Saudi Arabia plastic packaging market size even as unit growth slows to 2.1% annually. Flexible formats, however, are tracking a 4.43% CAGR, thanks to better cube efficiency and lower last-mile damages for e-commerce shipments. Converter orders for 11-layer blown-film lines surged 18% in 2024, allowing local firms to supply high-oxygen-barrier snack pouches previously imported. Supermarkets amplify uptake by dedicating 15% more shelf space to stand-up bags of rice and pulses, validating retailer willingness to reconfigure planograms in favor of flexible packs.

Demand drivers vary by channel: HORECA buyers cling to rigid gallon jugs for water dispensers, whereas beauty brands launch refill pouch programs that cut plastic weight by 70% per use cycle. The combined result supports a gradual, rather than disruptive, substitution pattern that keeps overall tonnage balanced while lifting value density in the Saudi Arabia plastic packaging market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Commodity Polyethylene Dominance Meets Specialty Barrier Momentum

Polyethylene retained 31.62% revenue share in 2024, its versatility spanning shrink film, squeezable tubes, and detergent bottles. Volume resilience ensures that polyethylene still represents over one-third of the Saudi Arabia plastic packaging market share despite feedstock gyrations. Specialty barriers led by EVOH, cyclic olefins, and metallized PET record a 4.51% CAGR, buoyed by date export pouches and pharma blister demand. SABIC’s pilot plant for advanced barrier resins inside Riyadh Techno-Valley will scale to 50 kt/yr by 2027, offering local converters secure supply of high-oxygen-barrier grades.

Polypropylene enjoys steady traction in snack-food overwraps where stiffness and clarity edge out LDPE. PET remains dominant in carbonated soft drinks due to carbonation retention and cost parity with returnable glass. Conversely, PVC clings to industrial chemical duty lines but faces gradual phase-out in consumer goods following SASO hazard labeling updates.

By End-User Industry: Beverage Leadership, Personal-Care Surge

Beverages captured 36.28% of revenue in 2024, powered by humid climate consumption patterns and broad retail distribution. The category underpins baseline throughput for preform and closure suppliers throughout the Saudi Arabia plastic packaging market. Yet personal care and cosmetics are forecast to compound at 4.68% yearly as women’s workforce participation climbs from 37% to 46% by 2030, expanding demand for local skin-care brands packaged in high-gloss PET jars. Flexible laminated tubes with in-mold holographic features cater to premium cosmetics, enabling mid-tier converters to capture value-added niches.

Food applications hold second-largest tonnage, lifted by frozen poultry exports that call for low-temperature-resistant PE films. Pharmaceutical volumes scale with localization of blister lines for generic tablets, boosting demand for Alu-Alu foil laminates in the Saudi Arabia plastic packaging industry. The industrial chemicals segment retains steady demand for 25 L HDPE drums used in water-treatment chemicals for desalination plants.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pack Format: Bottles Steady, Pouches on the Rise

Bottles and jars maintained 33.46% market revenue in 2024, leveraging entrenched filling lines centered around PET and HDPE. Closure suppliers roll out tethered-cap designs ahead of EU-style mandates, positioning local bottlers for export compliance. Meanwhile, pouches headline growth at 4.37% CAGR, spanning doypack sauces, pharmacy refill pouches, and 200 g date snack packs.

Stretch and shrink film usage follows manufacturing output; newly inaugurated white-goods plants in Jazan drive pallet-shroud volume. Trays and tubs remain stable in dairy but face thin-wall PP lightweighting to shave resin use by 11% without compromising stack strength. Caps and dispensing systems evolve into smart closures incorporating NFC tags for anti-counterfeit tracking.

Geography Analysis

Eastern Province dominates resin supply given integrated SABIC and Aramco crackers that channel polyethylene and polypropylene feedstock at sub-export netbacks. The region’s converters benefit from co-location synergies, lowering transport costs by 9 % versus central Saudi producers and thus safeguarding margins amid price swings. Riyadh’s consumer clustering drives branded food and beauty demand, encouraging investment in offset-printed shrink-sleeve lines to serve marketing-driven SKUs.

The NEOM corridor registers the fastest forecast growth at 4.9% CAGR as green-field FMCG plants near operational readiness. State-backed subsidies on renewable energy lower utilities bills for extrusion lines by 18%, reinforcing cost competitiveness of the Saudi Arabia plastic packaging market in the northwest. Jeddah’s Red Sea logistics gateway eases export flows into East Africa, prompting converters to certify operations under ISO 22000 to align with regional food-safety import checks.

Less-industrialized northern provinces lag, constrained by limited recycling infrastructure and longer haul distances for resin deliveries. Government tender programs for school milk pouches, however, inject demand seasonally, granting smaller film companies counter-cyclical revenue streams. Across all regions, SASO harmonizes labeling norms, but enforcement intensity varies, giving rise to cluster-level compliance advisory services that support SMEs.

Competitive Landscape

The Saudi Arabia plastic packaging market features a top-five concentration of 46%, yielding a moderately fragmented arena. SABIC anchors the value chain with 1.2 million t/yr of conversion-grade resins and the TRUCIRCLE portfolio aimed at 1 million t/yr circular products by 2030 [1]“SABIC and Saudi Investment Recycling Company Sign Pyrolysis Oil Agreement,” SABIC, sabic.com. Takween Advanced Industries positions as a mid-stream converter focusing on thin-wall injection and multilayer blow-molding for dairy. Arabian Plastic Industrial Company capitalizes on pharmaceutical GMP certification to supply BFS (blow-fill-seal) vials for localized vaccine fill-finish lines.

Strategic moves orbit around vertical integration and circularity. In 2025 SABIC partnered with the Saudi Investment Recycling Company to trial pyrolysis oil as cracker feed, eyeing 50 kt/yr capacity by 2027. Takween installed a 9-layer Reifenhäuser line to service snack-food exporters, projecting 14% internal rate of return by replacing imported high-barrier film. International entrants like Amcor signed a memorandum with NEOM authorities to co-develop a smart-pack plant utilizing 100% renewable energy, targeting go-live in 2028.

Competitive pressure intensifies in commodity PET preforms where Asian imports land at sub-12% duty, prompting local players to differentiate via tethered caps or plant-based resins. Conversely, high-barrier pharmaceutical blister remains protected: only three converters hold ISO 15378 certification, buttressing price realization by 21% above commodity levels.

Saudi Arabia Plastic Packaging Industry Leaders

-

Zamil Plastic Industries Co.

-

National Paper Products Company

-

Sealed Air Saudi Arabia Co. Ltd

-

Arabian Plastic Industrial Company Limited

-

Advanced Flexible Packaging Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: SABIC reported a SAR 1.5 billion net profit recovery for FY 2024, citing 135 new products in films and sheets that broaden portfolio reac

- August 2024: At CHINAPLAS 2024 SABIC unveiled recyclable PPc for cosmetic packs and FORTIFY POE backsheets for solar modules

- July 2024: ASG Plastic Factory filed a Nomu-Parallel Market IPO to fund expansion of PET bottle and disposable-utensil capacity

- June 2024: SABIC and Lamb Weston debuted UCO-derived polyethylene films for frozen potato exports, spotlighting bio-feedstock innovation

Saudi Arabia Plastic Packaging Market Report Scope

Plastic packaging is a part of the multi-faceted system for providing products, from the point of manufacture to the point of consumption. Its principal purpose is to guard and ensure the safe and secure delivery of the product in flawless and perfect condition to the end user (manufacturer of product or consumer). Its role in a circular economy is to sustain the value of a product for as long as required and to help remove product waste.

The market for plastic packaging in Saudi Arabia is segmented by Packaging Rigid (material (Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), Polystyrene (PS), and Expanded Polystyrene (EPS), Polyvinyl Chloride (PVC)), End User Industry (Food, Beverage, Healthcare and Pharmaceutical, Cosmetics and Personal Care), Flexible (material (Polyethene (PE), Bi-orientated Polypropylene (BOPP), Cast Polypropylene (CPP), Polyvinyl Chloride (PVC)), End User Industry (Food, Beverage, Cosmetics and Personal Care), Product type (Plastic Films, Pouches, and Bags)). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Packaging Type

| Rigid Plastic |

| Flexible Plastic |

By Material

| Polyethylene (HDPE, LDPE, LLDPE) |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP and BOPP/CPP) |

| Polystyrene and EPS |

| Polyvinyl Chloride (PVC) |

| Ethylene-Vinyl Alcohol (EVOH) and Other Barrier Plastics |

By End-user Industry

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Personal Care and Cosmetics |

| Household and Industrial Chemicals |

By Pack Format

| Bottles and Jars |

| Caps, Closures and Dispensing Systems |

| Pouches and Sachets |

| Trays, Cups and Tubs |

| Stretch and Shrink Films |

| By Packaging Type | Rigid Plastic |

| Flexible Plastic | |

| By Material | Polyethylene (HDPE, LDPE, LLDPE) |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP and BOPP/CPP) | |

| Polystyrene and EPS | |

| Polyvinyl Chloride (PVC) | |

| Ethylene-Vinyl Alcohol (EVOH) and Other Barrier Plastics | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Household and Industrial Chemicals | |

| By Pack Format | Bottles and Jars |

| Caps, Closures and Dispensing Systems | |

| Pouches and Sachets | |

| Trays, Cups and Tubs | |

| Stretch and Shrink Films |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Saudi Arabia plastic packaging market?

The Saudi Arabia plastic packaging market size is USD 8.59 billion in 2025 with a projected rise to USD 10.12 billion by 2030.

Which packaging type holds the largest share?

Rigid formats, primarily PET bottles and HDPE containers, accounted for 52.73% of 2024 revenue.

Which segment is growing fastest through 2030?

Flexible pouches and sachets are forecast to register a 4.37% CAGR, outpacing all other pack formats.

How will Vision 2030 influence local packaging production?

Incentives in clusters like NEOM and Ras Al Khair reimburse up to 30% of capex, accelerating domestic conversion capacity and lowering import dependence.

What are the main sustainability pressures facing converters?

Mandatory oxo-biodegradable compliance, limited recycling infrastructure, and brand commitments to recycled content are raising the bar on material circularity.

Page last updated on: