Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Metal Cans Market Analysis by Mordor Intelligence

The India metal cans market size is expected to grow from USD 1.72 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.21 billion by 2031 at 4.24% CAGR over 2026-2031. Rising demand for recyclable packaging, continued capacity additions by global and domestic converters, and aluminum’s cost advantage underpin this steady expansion. The India metal cans market benefits from the country’s 4.1 million-ton annual aluminum output, which secures local feedstock availability even as global metal prices remain volatile. Ongoing policy support through Extended Producer Responsibility (EPR) rules effective April 2025 reinforces metal’s appeal over single-use plastics, while investments such as CANPACK Group’s USD 150 million greenfield site in Uttar Pradesh confirm long-term confidence among international stakeholders. Rapid growth in ready-to-drink beverages, personal-care aerosols, and pharmaceutical inhalers continues to widen end-user diversity, allowing producers to spread risk across multiple consumer categories. Competitive intensity is gradually rising, yet fragmentation persists as regional specialists grow alongside multinational entrants.

Key Report Takeaways

- By material type, aluminum led with 69.92% of the India metal cans market share in 2025; steel is forecast to post the fastest 5.21% segment CAGR through 2031.

- By can structure, two-piece formats captured 52.74% of the India metal cans market size in 2025, while monobloc aerosol variants are projected to expand at a 5.61% CAGR to 2031.

- By capacity, 250-500 ml cans held 31.05% share of the India metal cans market size in 2025, yet ≤250 ml formats are advancing at a 5.72% CAGR through 2031.

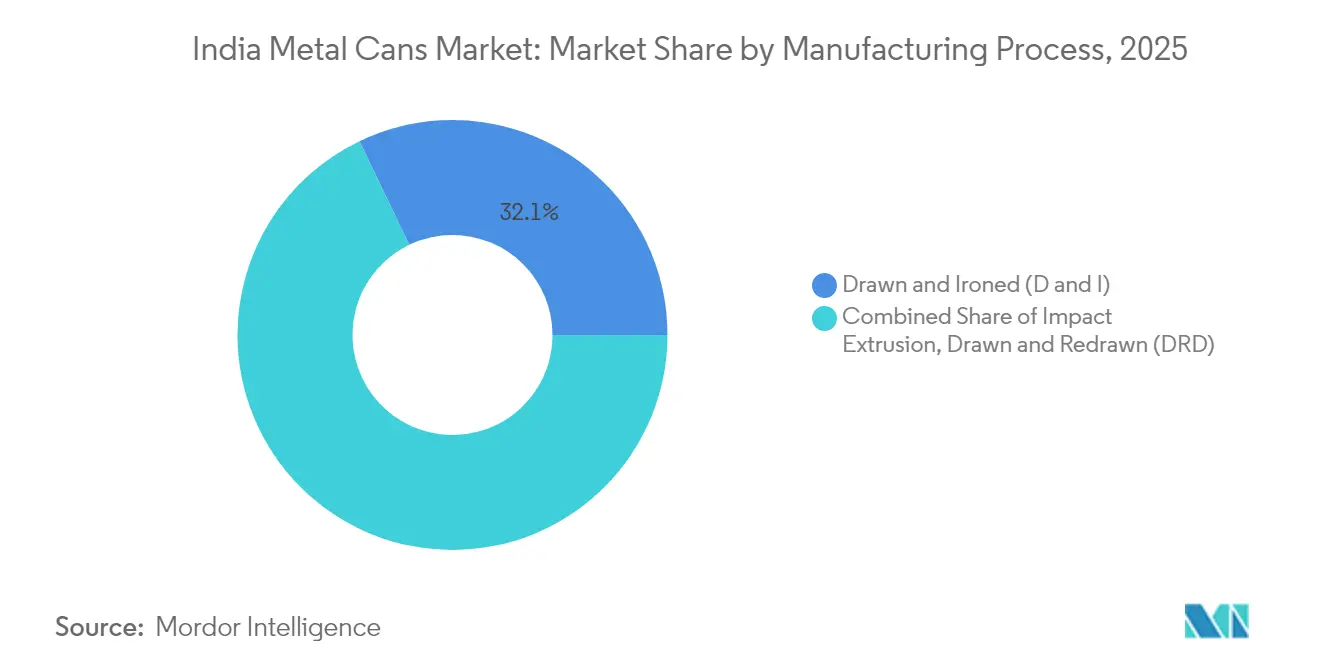

- By manufacturing process, Drawn and Ironed (D and I) accounted for 32.12% of the India metal cans market size in 2025; impact extrusion is registering the highest 5.55% CAGR on the back of aerosol demand.

- By end-user industry, beverages commanded 39.88% revenue in 2025, whereas pharmaceuticals register the strongest 5.78% CAGR through 2031.

- By geography, Maharashtra and Gujarat together represented 47.62% of the India metal cans market size in 2025, supported by integrated aluminum supply chains and port access.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Metal Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in convenience and RTD foods | +1.20% | National; early gains in Mumbai, Delhi, Bengaluru | Medium term (2-4 years) |

| Increasing beverage-can uptake in craft beer and energy drinks | +0.80% | Urban centers in Maharashtra, Karnataka, Goa | Short term (≤ 2 years) |

| Higher recycling rates and circular-economy regulations | +0.70% | National; compliance focus in major cities | Long term (≥ 4 years) |

| Aerosol demand surge in personal-care segment | +0.90% | Urban and semi-urban India | Medium term (2-4 years) |

| Rise of indigenous chai/coffee-in-a-can SKUs | +0.60% | National; premium channels | Medium term (2-4 years) |

| Rural fruit-processing clusters adopting canning | +0.40% | Maharashtra, Andhra Pradesh, Karnataka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Convenience and RTD Foods

Shelf-stable ready-to-drink meals and beverages are pushing manufacturers to adopt metal packaging that supports 18-month ambient life spans, minimizes refrigeration costs, and allows premium positioning on modern retail shelves. The government’s Pradhan Mantri Kisan Sampada Yojana has earmarked INR 6,000 crore (USD 720 million) toward food-processing infrastructure, directly backing 42 mega parks that house new canning lines. Brands such as Tata Consumer Products capitalized on this support by introducing 180 ml RTD coffee cans in October 2024, priced 15–20% above PET alternatives yet registering higher off-take in metro supermarkets.[2]World Aerosols, “Latest Magazine Volume 8 Issue 3,” worldaerosols.comAluminum’s strong barrier against oxygen and light maintains flavor integrity, allowing processors to promise authentic chai or coffee taste without cold chain reliance. Subsidies covering 35% of capital cost for canning equipment further tilt the economics in favor of metal, especially for small-format packs geared toward portion-control and premium margins. As organized retail penetration climbs past 12% of India’s grocery turnover in 2025, the India metal cans market gains a durable growth engine.

Increasing Beverage-Can Uptake in Craft Beer and Energy Drinks

Aluminum’s light weight reduces logistics expenses by around 30% compared with glass, crucial for independent breweries shipping to distant metros.[3]Times of India, “Japan’s Nippon Paint Looks at Fresh Investments,” timesofindia.indiatimes.com Craft labels in Goa, Maharashtra, and Karnataka increasingly choose 330 ml and 500 ml sizes that fit premium pricing while safeguarding carbonation. Energy-drink makers tout aluminum’s thermal conductivity for rapid chilling an important impulse-purchase trigger in India’s hot climate. Industry feedback indicates 25% quicker inventory rotation for canned SKUs thanks to extended shelf life and lower breakage. Moreover, the Bureau of Indian Standards’ IS 18427 certification, finalized in 2024, gives alcoholic-beverage producers a clear compliance path that removes earlier regulatory ambiguity. As these niche categories scale, the India metal cans market receives incremental high-margin volume that offsets softer demand in commoditized soft-drink segments.

Higher Recycling Rates and Circular-Economy Regulations

EPR rules effective April 2025 oblige manufacturers to ensure 70% recycling of aluminum packaging by 2027, a target well within the metal can industry’s current urban recovery performance of 85%. Aluminum’s closed-loop recyclability saves 95% of the energy required for primary smelting, delivering tangible carbon-footprint reductions a metric large consumer-goods firms now disclose in annual ESG reports. Hindalco’s INR 45,000 crore (USD 5.4 billion) investment into a 500,000-ton scrap-processing network guarantees feedstock and lowers cost volatility. Reverse-logistics incentives embedded in EPR guidelines are expected to expand collection from tier-2 cities, boosting the India metal cans market while allowing converters to market cans as “near-zero-carbon” packaging.

Aerosol Demand Surge in Personal-Care Segment

Total aluminum aerosol shipments to India climbed to an estimated 650 million units in 2024, driven by deodorants, hair sprays, and rising men’s grooming categories. Local producer Sterling Enterprises now supplies monobloc cans as small as 50 ml, addressing demand for travel-size packs favored by e-commerce shoppers. Impact-extrusion lines can produce thinner walls without compromising pressure ratings, lowering metal input per can by 15% and improving margins. National disposable-income growth supports premiumization, while urban consumers demonstrate higher willingness to pay for recyclable metal over non-recyclable plastic propellant containers. These trends sustain a robust 5.94% CAGR for monobloc aerosols inside the India metal cans market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and flexible-packaging substitution pressure | −1.1% | National; higher impact in cost-sensitive segments | Short term (≤ 2 years) |

| Volatility in aluminum and tin-plate costs | −0.8% | National; all manufacturers | Medium term (2-4 years) |

| Domestic tin-plate supply bottlenecks | −0.6% | National; food clusters | Medium term (2-4 years) |

| EPR cost-pass-through uncertainty | −0.4% | National; small manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PET and Flexible-Packaging Substitution Pressure

PET bottles and retort pouches still undercut cans by 20–30% on material cost, swaying price-sensitive fillers in carbonated soft drinks and edible oils. Private-equity firm PAG’s INR 8,400 crore (USD 1.01 billion) purchase of Manjushree Technopack in November 2024 underscores investor appetite for plastics. PET’s clarity caters to consumers who prefer visual product validation, while flexible packs enable stand-up pouches that occupy less shelf space. Plastic players are investing in bottle-to-bottle recycling infrastructure to blunt aluminum’s sustainability edge, an effort that could temper the India metal cans market’s near-term growth in mass-market segments. Even so, aluminum retains dominance where internal pressure or taste protection is non-negotiable, giving cans a secure beachhead despite substitution risk.

Volatility in Aluminum and Tin-Plate Costs

London Metal Exchange cash prices swung 25% during 2024, moving between USD 2,100 and USD 2,700 per ton as energy costs and geopolitical disruptions roiled the market. Tin-plate imports account for 60% of Indian demand, exposing canners to currency fluctuations and antidumping duties. Smaller converters lacking hedging mechanisms saw EBITDA margins shrink below 8% in late 2024. Large players mitigate risk via long-term supply agreements and in-house scrap recovery, but volatility remains an operating headache. Persistent metal-price swings could accelerate consolidation within the India metal cans industry as undercapitalized firms exit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Secures Leadership

Aluminum retained 69.92% share of the India metal cans market in 2025, supported by domestic smelter capacity that shields converters from import exposure. The segment is set to post a 4.95% CAGR, underpinned by Hindalco’s recycling expansion, which lowers input costs by 20% versus primary metal. Tin-coated steel holds niche relevance in foods demanding elevated sulfur-corrosion resistance, yet its weight disadvantage limits penetration in beverages and aerosols. Consumers increasingly associate aluminum with premium, eco-friendly credentials, reinforcing its dominant role across multiple pack sizes. Supply-chain resilience and regulatory favorability ensure aluminum’s grip on the India metal cans market remains firm.

Secondary products such as steel cans for curries and pickles exploit three-piece construction that allows necking and shaping flexibility. However, limited domestic tin-plate manufacturing forces dependence on imports, increasing landed cost and constraining growth. Continuous investments in lightweight aluminum alloys and water-based interior lacquers further widen the performance gap, confirming aluminum as the mainstay of the India metal cans market.

By Can Structure: Two-Piece Dominance and Aerosol Upswing

Two-piece drawn-and-wall-ironed (DWI) cans delivered 52.74% share in 2025 thanks to material efficiency and high-speed production lines exceeding 2,000 cans/minute. Seamless walls prevent micro-leaks in carbonated beverages, supporting extended distribution cycles vital in a country where refrigeration grids remain uneven. CANPACK’s Uttar Pradesh facility breaking ground in February 2025 will add over 2 billion DWI units annually, easing supply tightness. Monobloc aerosol formats, though only 8.12% of unit volume, are expanding at a market-leading 5.61% CAGR as grooming habits evolve and pharmaceutical inhalers gain traction.

Three-piece bodies continue to serve food staples like ghee and condensed milk, where internal vacuum rather than pressure is the chief concern. Yet sustained capital inflows into DWI automation suggest two-piece cans will keep absorbing market share, once again highlighting productivity as a central lever in the India metal cans market.

By Capacity/Size: Mid-Range Leads, Small Formats Accelerate

Pack sizes between 250 ml and 500 ml accounted for 31.05% of 2025 volume, aligning with single-serving soft-drink and beer consumption norms. Smaller ≤250 ml units, including Tata Consumer’s 180 ml RTD coffee can, are riding a 5.72% CAGR wave, fueled by portion-control trends that resonate with weight-watching urban professionals. Mini-cans also help brands achieve premium price-points per milliliter, enhancing revenue per kilogram of aluminum consumed. Larger formats above 1,000 ml remain the domain of institutional paints and automotive lubricants, but growth here is muted by the emergence of composite containers and HDPE drums that offer cost advantages.

By Manufacturing Process: D and I Technology Rules

Drawn and Ironed technology handled 32.12% of 2025 output, prized for reducing aluminum usage by up to 15% relative to Drawn and Redrawn lines. The India metal cans market size for D and I cans is projected to expand at a stable 4.62% CAGR as additional high-speed lines arrive from Europe and China. Impact extrusion, the technology behind aerosol monoblocs, posts a quicker 5.55% CAGR. Automation upgrades such as robotics for can-end lining and in-line vision inspection lower defect rates below 150 ppm, a benchmark demanded by multinational fillers. Ball Corporation’s 2025 patent for reclosable ends demonstrates continuous innovation in this mature process, illustrating how incremental features can defend share against other pack formats

By End-User Industry: Beverages on Top, Pharma Rising Fast

Beverages owned 39.88% revenue in 2025 as beer, energy drinks, and flavored water brands prioritized aluminum’s pressure tolerance and flavor neutrality. The India metal cans market size for beverages is expected to grow at a steady 4.12% CAGR through 2031, aided by the craft-beer boom and vending-machine rollouts in tier-1 cities. Pharmaceuticals, although a modest 3.08% share today, exhibit a 5.78% CAGR driven by metered-dose inhalers that rely on aluminum canisters for sterility and dimensional accuracy. Personal-care aerosols also log above-average growth as grooming spends rise by double digits in metro markets. Paints, chemicals, and automotive fluids round out demand but remain sensitive to economic cycles, leading converters to diversify into high-margin specialty coatings to protect earnings.

Geography Analysis

Western India namely Maharashtra and Gujarat hosts nearly half of national manufacturing thanks to port access, raw-material proximity, and generous tax incentives. Maharashtra leverages its consumer base around Mumbai and Pune to fast-track new beverage launches, while Gujarat’s aluminum-rolling ecosystem tightens supply chains for can-body stock. Southern states such as Karnataka and Tamil Nadu specialize in pharmaceutical aerosols and specialty foods, harnessing skilled labor and biotech clusters. Shetron Limited’s plants in Bengaluru and Raigad highlight a dual-state model that balances logistics between northern and southern demand pockets. Northern India is now attracting large investments, with CANPACK’s Uttar Pradesh megasite positioned to serve the Delhi-NCR belt India’s largest single consumption zone while tapping dedicated freight corridors to reach eastern states. The east remains underdeveloped but could surface as a manufacturing hotspot post-2027 once corridor upgrades shrink transit times to ports like Kolkata and Paradip. Regional policy differentials in electricity tariffs, land-lease rates, and recycling mandates will continue shaping where new capacity lands, keeping location strategy a live question for every participant in the India metal cans market.

Competitive Landscape

The India metal cans market displays moderate fragmentation, with the top five players controlling just under 60% of capacity. Global firms such as CANPACK, Crown Holdings, and Ball Corporation partner with or acquire stakes in local converters to bypass regulatory learning curves and secure land quickly. Domestic champions Hindustan Tin Works and Kaira Can Company leverage long-standing FMCG relationships and agility in short runs to defend regional share. Vertical integration into scrap collection and secondary-ingot casting is a clear trend: Hindalco leads with a 500,000-ton recycling build-out that offers 20% input-cost savings.[1]India Brand Equity Foundation, “Get Insights into the Metals and Mining Industry in India,” ibef.org Meanwhile, technological differentiation, exemplified by Ball’s reclosable-end patent, enables premium pricing in an otherwise commoditized container business. New entrants face high capital barriers each high-speed DWI line costs USD 55–60 million plus rigorous quality certifications, conferring incumbents a defensible moat. M&A chatter persists, centered on aerosol specialists and regional food-can players, signaling that market consolidation is likely to inch higher over the next five years.

India Metal Cans Industry Leaders

Casablanca Industries Pvt. Ltd

Can-Pack S.A.

Ball Corporation

Hindustan Tin Works Ltd.

Oricon Enterprises Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: CANPACK Group broke ground on a USD 150 million beverage-can plant in Uttar Pradesh, the sector’s largest single-site investment to date

- February 2025: Ball Corporation secured a patent for reclosable aluminum can ends, enhancing convenience for carbonated beverages

- December 2024: Sonoco finalized purchase of Eviosys, creating a global metal-packaging leader with expanded R&D bandwidth relevant to India

- November 2024: Ball Corporation completed acquisition of Alucan’s European aerosol assets, broadening technology that may feed into Indian operations

India Metal Cans Market Report Scope

Metal cans are well suited for the mobile lifestyle of the consumer as they can be carried or transported easily to outdoor events, festivals, and beaches. In contrast, glass is typically forbidden because of its breakability. Additionally, the affordability and recyclability of cans, the rising popularity of energy drinks, and the launch of new goods all contribute to the growth of the market studied. The study tracks the consumption in the market considering the revenue generated from sales of metal cans in the domestic market.

The Indian metal cans market is segmented by type (aluminum, steel) and end user (food, beverage, cosmetic and personal care, pharmaceuticals, paints, automotive). The market sizes and forecasts are provided in terms of value in USD million for all the above-mentioned segments.

By Material Type

| Aluminium |

| Steel |

By Can Structure

| Two-Piece |

| Three-Piece |

| Monobloc Aerosol |

By Capacity / Size

| ≤250 ml |

| 250–500 ml |

| 500–1,000 ml |

| >1,000 ml |

By Manufacturing Process

| Drawn and Ironed (D & I) |

| Drawn and Redrawn (DRD) |

| Impact Extrusion |

By End-User Industry

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Paints and Industrial Chemicals |

| Automotive Fluids and Lubricants |

| Other End-User Industry |

| By Material Type | Aluminium |

| Steel | |

| By Can Structure | Two-Piece |

| Three-Piece | |

| Monobloc Aerosol | |

| By Capacity / Size | ≤250 ml |

| 250–500 ml | |

| 500–1,000 ml | |

| >1,000 ml | |

| By Manufacturing Process | Drawn and Ironed (D & I) |

| Drawn and Redrawn (DRD) | |

| Impact Extrusion | |

| By End-User Industry | Food |

| Beverage | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Paints and Industrial Chemicals | |

| Automotive Fluids and Lubricants | |

| Other End-User Industry |

Key Questions Answered in the Report

What is the current size of the India metal cans market?

The India metal cans market size is valued at USD 1.79 billion in 2026 and is set to reach USD 2.21 billion by 2031.

Which material leads India’s can production?

Aluminum dominates with 69.92% share, driven by local smelting capacity and strong recycling economics.

Which end-use segment is growing fastest?

Pharmaceuticals, particularly aerosol drug delivery systems, are advancing at a 5.78% CAGR through 2031.

How do EPR rules affect can makers?

EPR mandates 70% recycling of aluminum packaging by 2027, favoring cans because urban recovery rates already exceed 80%.

Which region attracts the most new capacity?

Western India remains the core hub, but northern Uttar Pradesh is emerging thanks to CANPACK’s large greenfield investment.

Page last updated on: